SUI - Sun Communities: UK Woes Present Opportunity For Long-Term Investors

2023-10-17 13:57:23 ET

Summary

- Sun Communities' shares have fallen 24% in the past six months due to concerns over its recently acquired UK business.

- However, the company's core US mobile home/RV/marina business has favorable long-term dynamics, including limited supply growth and increasing demand for affordable housing.

- Sun Communities trades at a compelling valuation compared to its closest competitor, and there is potential for the stock to re-rate in the future.

Shares of Sun Communities (SUI) have been battered recently, with shares falling 24% in the past six months. The market is concerned about shortfalls in its recently acquired UK business which led Sun to reduce guidance with its second-quarter results. More recently, news surfaced that Sun's loan to UK leisure park operator RoyalLife may be impaired, compounding concerns over Sun's international exposure (the UK represents about 10% of NOI).

While UK woes are likely to persist for a while, investors seem to be overlooking Sun's economically resilient mobile home/RV/marina business, which has very favorable long-term dynamics including:

- Nascent new supply

- Favorable demographic trends are driven by a dramatic increase in housing costs in the US, an aging population (age restricted/over 55 parks), and increased interest in RV vacationing.

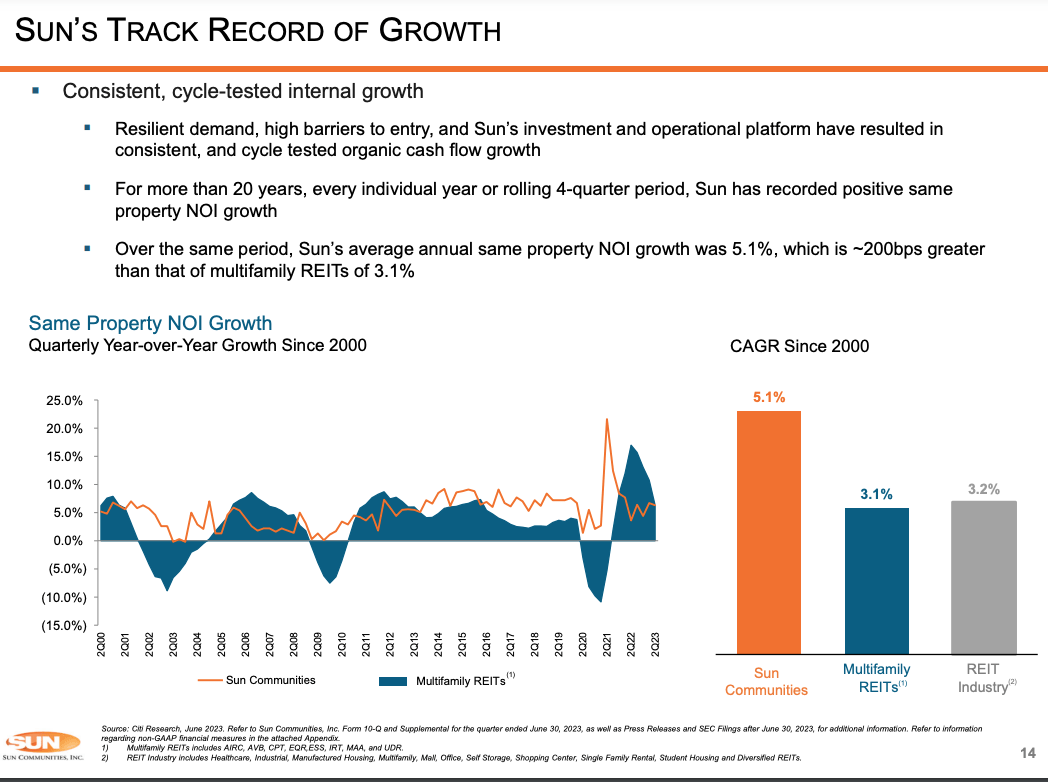

- A track record of same-store NOI growth well in excess of multifamily REITs

At today's price of $105 per share, Sun shares trade at just 15.4x 2024e AFFO and a 6.2% implied cap rate, which is well below historical levels and peer Equity LifeStyle ( ELS ). I see Sun Communities as a compelling investment for long-term, conservative investors.

Recent Results / UK Woes

{kind=link}

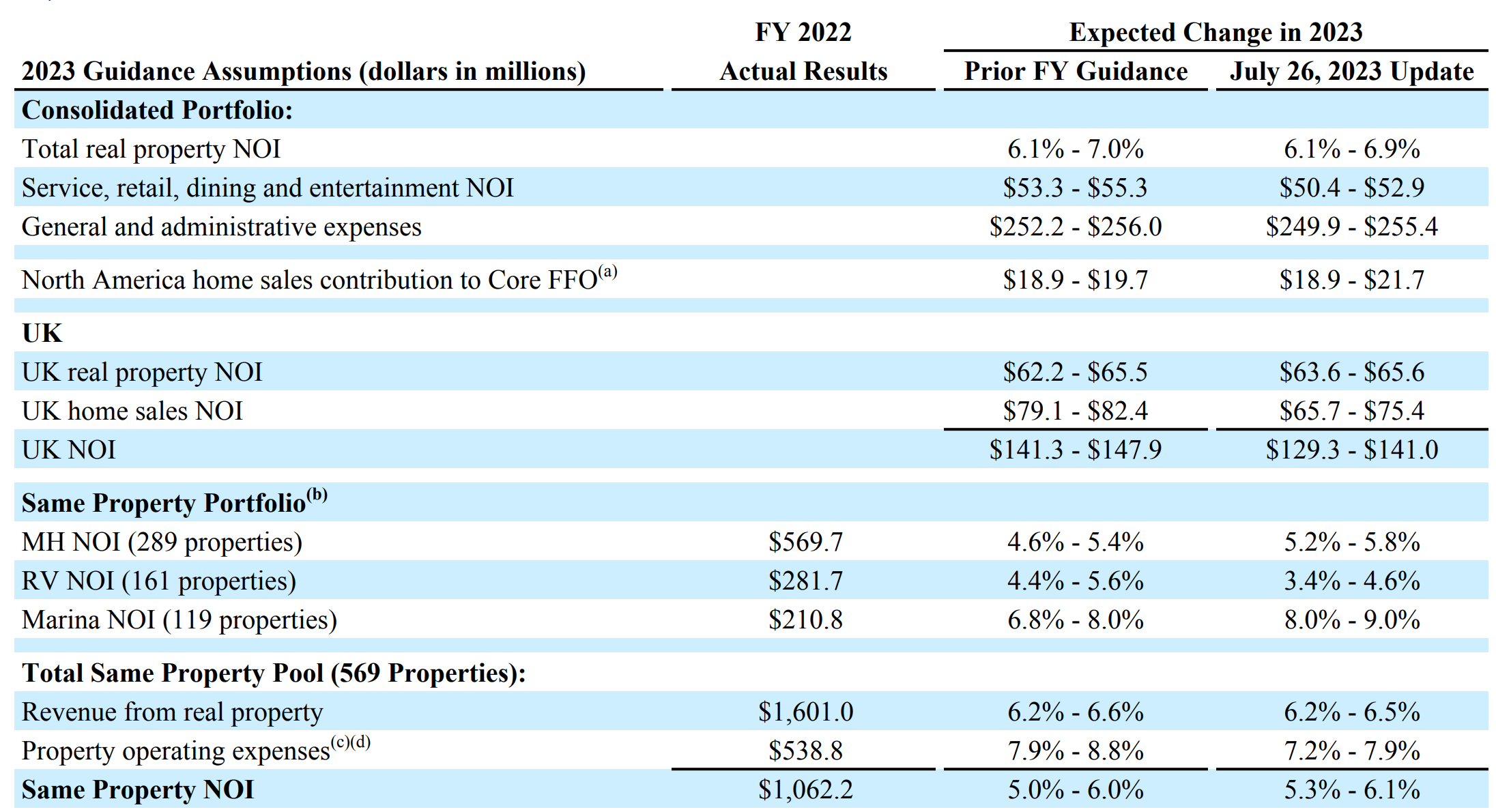

2023 Guidance (Sun Communities Quarterly Supplemental)

As shown above, Sun's core US business (mobile home, RV, marinas) has continued to perform well thus far in 2023 with robust same-store NOI growth of 6.5% in 1H23 (and guidance for 6+% for the full-year real property NOI). The lack of new supply coupled with stable/increased demand continues to produce excellent results in the US business.

However, the market has turned its focus to difficulties facing the UK business (Park Holidays). As you can see above, Sun lowered its expectations for recently acquired Park Holidays by nearly 7%. As you can see, a larger percentage of Park Holidays NOI comes from economically sensitive home sales than rent collected on the ground beneath the home ('real property income'). This represents a stark difference between Park Holidays and Sun's US business, where the vast majority of NOI comes from stable, recurring income (Sun simply collects rent on the ground beneath the tenant-owned mobile home/RV).

Poor UK results coupled with higher-than-anticipated interest expenses caused management to reduce full-year FFO guidance by 2.5%. While 2.5% is not a big number, over the past several years, investors have grown accustomed to Sun meeting or exceeding guidance. In addition, investors seem to be concerned that continued weakness in the UK business (rising interest rates, waning customer confidence) could lead to another cut in guidance. More recently, news of a troubled loan to RoyalLife, has garnered more negative attention (there is not a lot of detail about this yet, but I estimate that a move to 'non-accrual' status for the loan could potentially shave another $0.30, or 4%, off full-year FFO).

Readers may be wondering, 'Given the UK mess, why should I even consider investing in Sun'? Fair question.

Reasons I Own (and have been adding to) Sun Communities

Almost exactly one year ago, I wrote a piece detailing Sun's business model but as a brief re-cap:

- While troubled, the UK is relatively small at only about 11% of NOI.

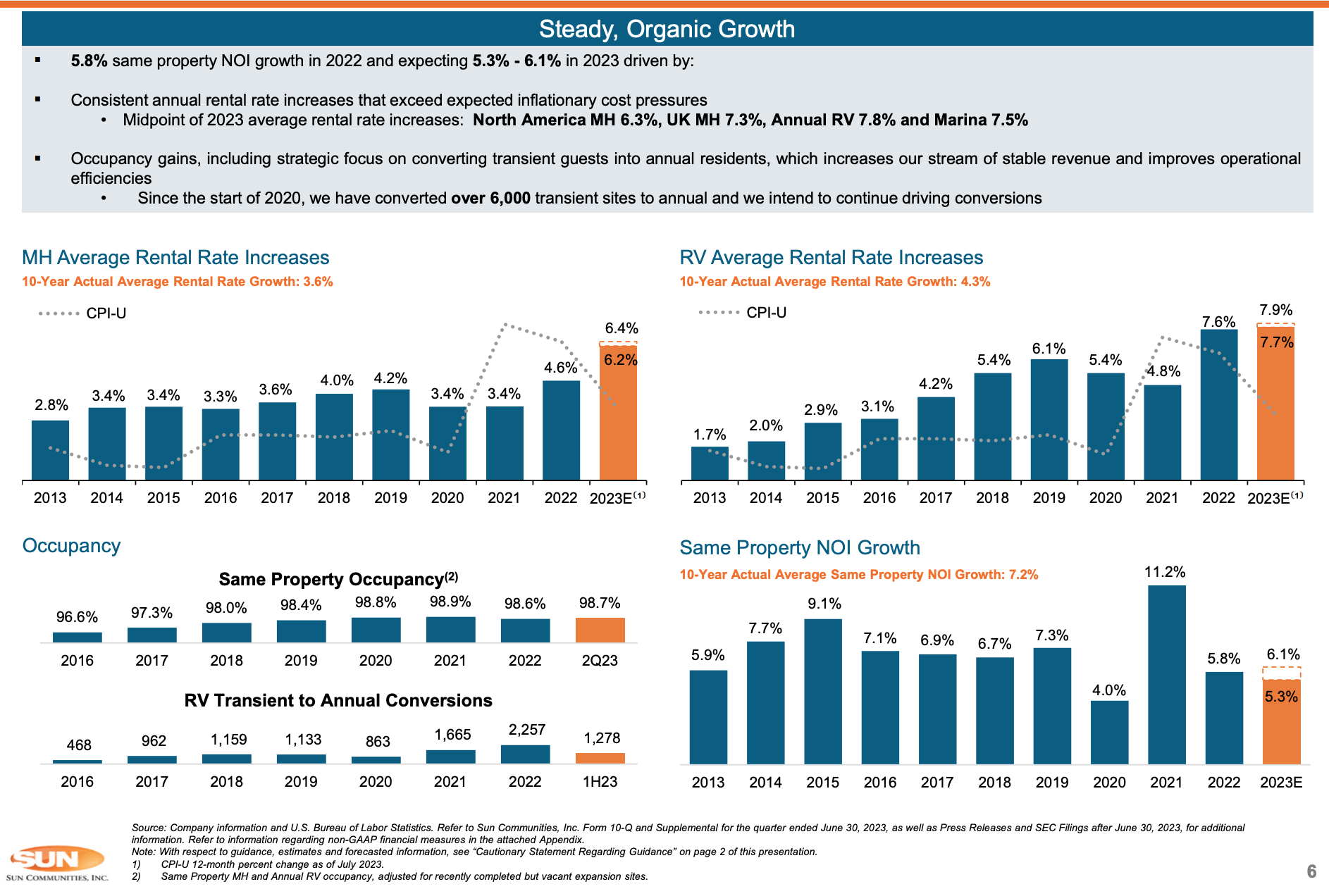

- Sun's core mobile home/RV/marinas operation has generated terrific long-term performance as shown below.

{kind=link}

Steady Long-Term Operating Performance (Sun Communities Investor Presentation)

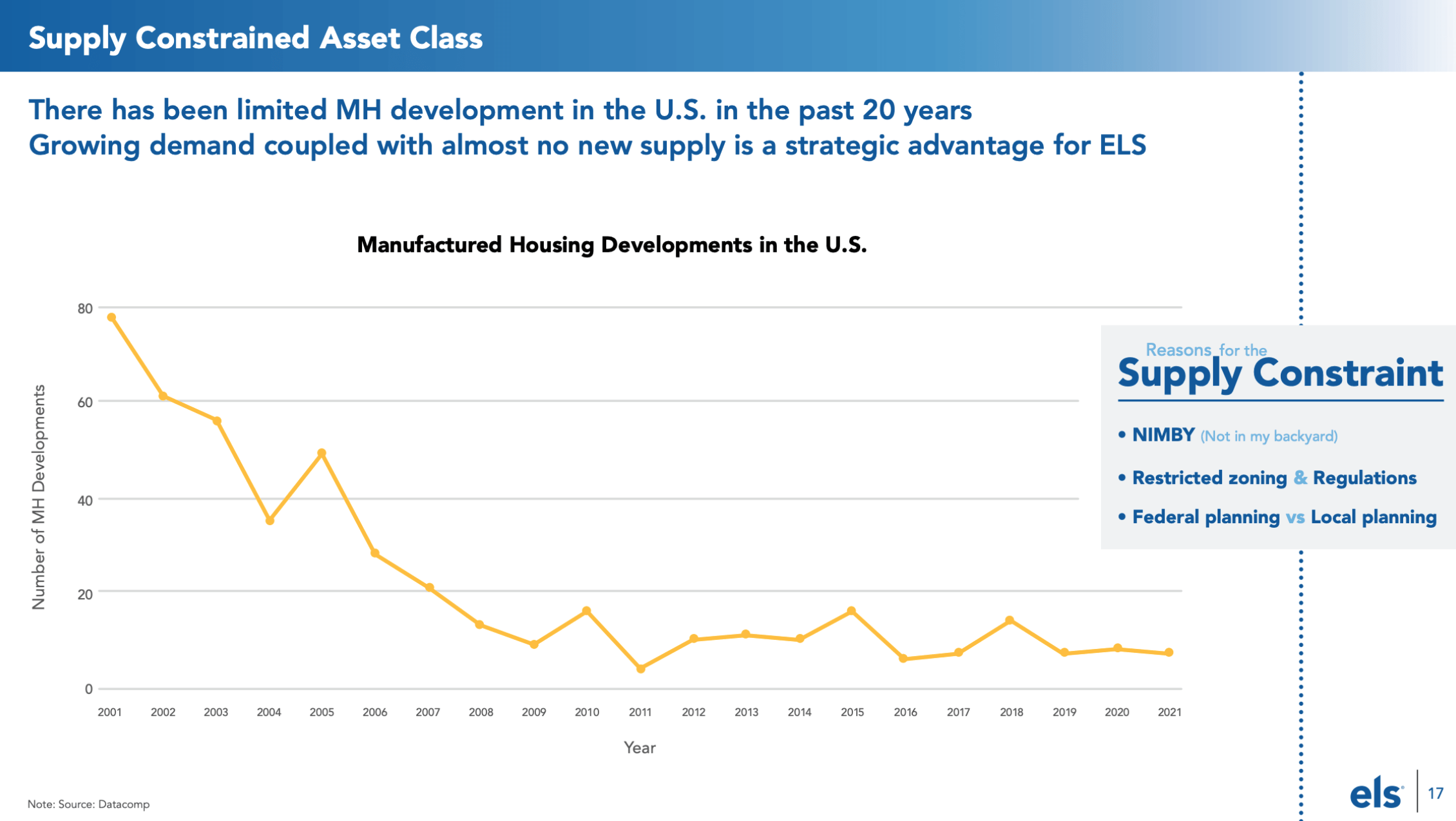

- Unlike most property types, mobile home/RV/marinas see very limited supply growth which leads to steady growth in same-store NOI.

{kind=link}

New Supply or Lack Thereof (Equity Lifestyles Investor Presentation)

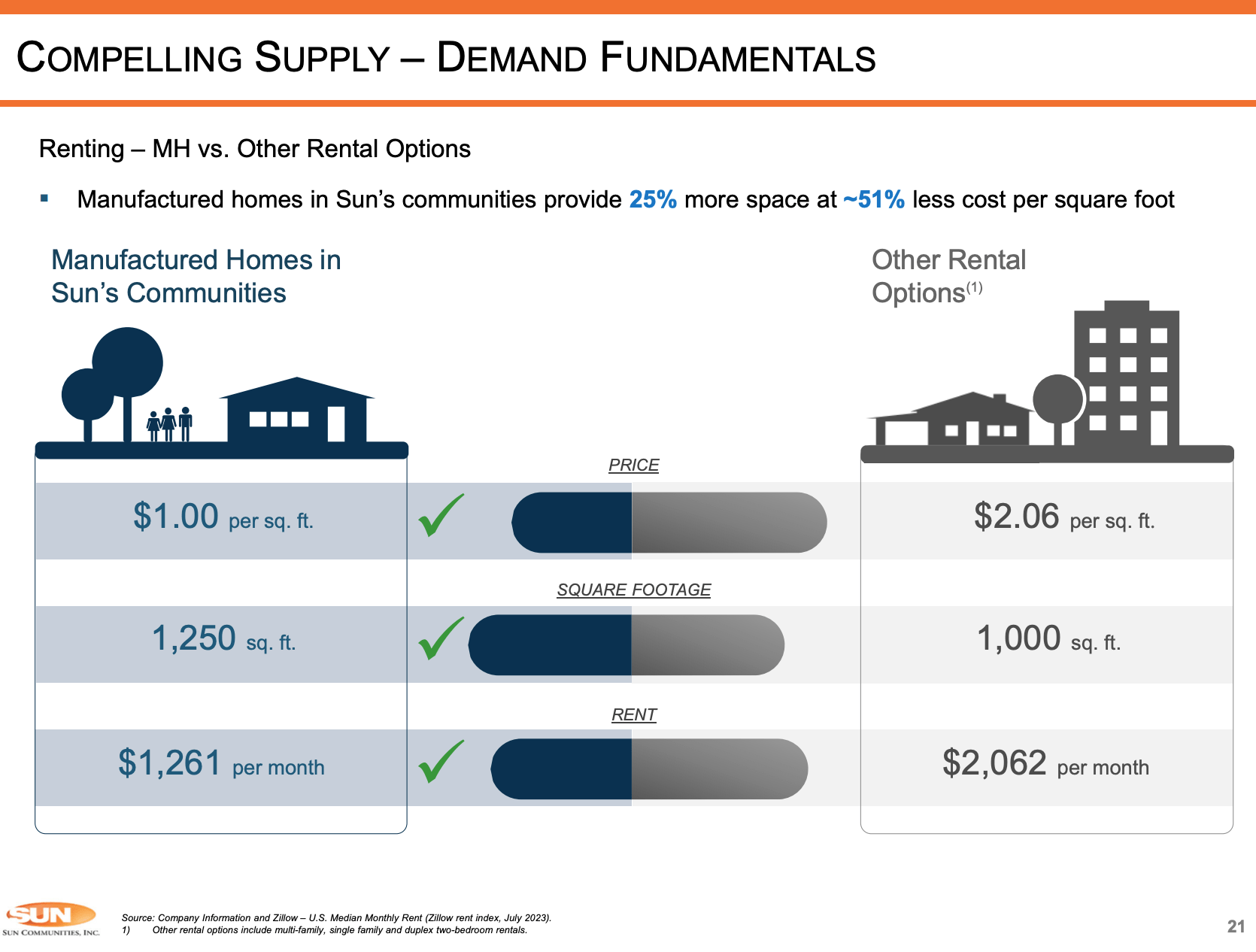

- Rising housing costs (home prices, interest rates, apartment rents) are likely to further increase demand for inexpensive housing. Mobile home parks offer the lowest cost of non-subsidized housing in the US.

{kind=link}

Apartment Rent vs. Mobile Home (Sun Investor Presentation)

In addition, Sun trades at a valuation I find compelling here. For 2024, I strip out my estimate of interest on the RoyalLife loan which gets me to FFO of $7.27 and AFFO of $6.80 which implies a valuation of just 14.4x FFO/15.4x AFFO. This is the bottom end of the 14.4-29x FFO at which Sun has historically traded. By comparison, Sun's closest competitor, Equity Lifestyles, trades at 21.6x 2024e FFO. While Equity Lifestyles has historically traded 2-4x richer than Sun, today's valuation gap is at a decade-long high. Similarly, I have Sun trading at an implied cap rate of 6.2% (using 2024e NOI) versus 5% for Equity Lifestyles. Further, while historically Sun has traded at a premium to multifamily REITs (which have slower growth as shown below), today Sun trades at a discount to most multifamily REITs which are in the 15-17x FFO range

{kind=link}

Sun NOI Growth over Time (Investor presentation)

As UK issues recede (again it is only ~11% of NOI), looking out 2-3 years I believe investors will once again gravitate toward Sun shares and see the stock re-rating back to 20x FFO. Factoring in expected FFO growth, this gets me to a share price of $160 by 2026, representing a 53% upside. In the meantime, investors collect a 3.6% dividend yield.

Conclusion

While the UK has been a trouble spot for Sun Communities in 2023, the core US mobile home/RV/marina business continues to perform well. I believe that patient, long-term investors will ultimately be rewarded.

For further details see:

Sun Communities: UK Woes Present Opportunity For Long-Term Investors