SHGKY - Sun Hung Kai And Hui Xian REIT: 2 Deep Value Picks For 2023 From Asia

Summary

- China and Hong Kong have been negatively impacted by very strict measures to fight the pandemic, and many businesses suffered.

- Many companies still make money and are conservatively funded.

- High dividends ensure investors get paid while waiting for a recovery.

- We believe 2023 will be better for stocks listed in Hong Kong.

Investment thesis

Stock markets are down this year and the sentiment is weak as the consensus is for new lows and a recession in sight.

Many investors have pulled funds out of equity and allocated them to fixed income.

This also opens up many good opportunities in equities for contrarians with a long-term view.

For those that follow us here on Seeking Alpha, or have read some of our earlier articles, you will know that our portfolio, hence our main interest, is for equities in Asia.

It does not mean that we only invest in those, as it is crucial to have a global portfolio.

We want to share with you our two Asian Deep value picks for 2023

Here they are:

Sun Hung Kai & Company

Sun Hung Kai & Co. Limited ( SHGKY ) was established in 1969 in Hong Kong. In its early years, it was controlled by the family that controls Sun Hung Kai Properties ( SUHJY ), with stock brokering and consumer financing as its main business. In 1983, it got listed on the Hong Kong Stock Exchange ( HKXCF ) under the code 0086. In 1986, Allied Properties, now renamed Allied Group, became its controlling shareholder. They also control the REIT ( APYRF ) listed on the Toronto Stock Exchange.

Today, Sun Hung Kai & Co.'s businesses are divided into three pillars.

SHK 3 pillars of businesses (Sun Hung Kai & Co.)

{kind=link}

The Group invests across public markets, alternatives, and real estate and has an established track record of generating long-term risk-adjusted returns for its shareholders.

Most recently, it has extended its strategy to incubate, accelerate and support emerging asset managers in the Asian region.

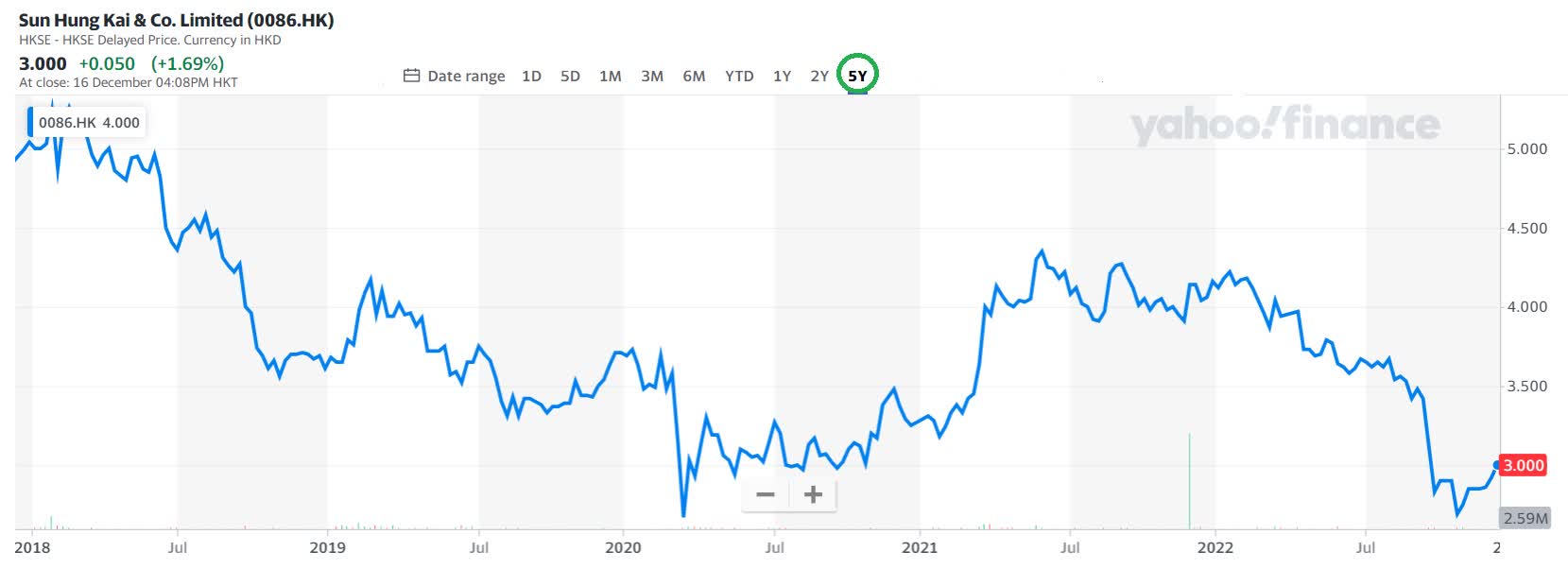

The share price is down 41% over the last 5 years.

SHK 5 year share price development (Yahoo Finance)

{kind=link}

Their interim report for FH of 2022

The Group's revenue in the first half of 2022 was HKD2,056 million, which mainly consisted of interest income from the Financing Business of HKD1,943 million.

Pre-tax loss for the period was HKD55 million as compared to a profit of HKD3,216 million for the first half of 2021. That was an all-time-high record of FH profit as it took into account the sale of their 30% stake in the stock brokering business. The poor results this year are mainly due to the pre-tax loss recorded in the Investment Management business of HKD958 million, primarily attributable to the mark-to-market losses of HKD1,180 million.

In FH of 2021, this mark-to-market brought a gain of HKD1,084 million.

When we look at their cash flow, we get more comfortable.

Cash from operating activities for FH was HKD2,143 million compared to just HKD543 in FH 2021. Cash on hand at end of FH 2022 was HKD8,159 million against HKD5,786 million in 2021.

On the 22nd of November 2022, the management came out with a profit warning stating that as of 31st October this year their unaudited consolidated loss attributable to the owners of the Company for the ten months ended 31 October 2022 is approximately HK$1.38 billion. This was expected as the loss for the ten months ended 31 October 2022 is the mark-to-market loss in financial instruments in the Company's investment management business. It is in stark contrast to the profit of HK$2.92 billion it had in the same period of last year.

NAV per share is HKD12.7.

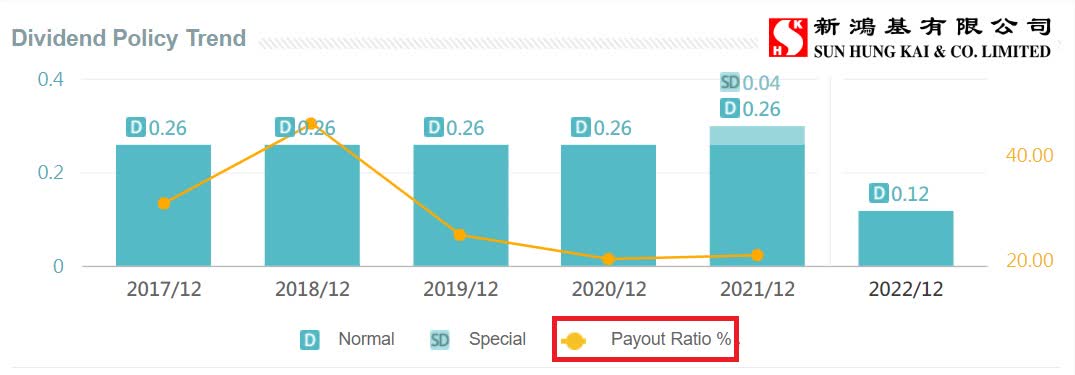

Their dividend policy could perhaps be a bit more shareholder-friendly.

In 2021 when they sold off their remaining 30% of the shares in the stockbroking company to Everbright Securities for HKD2.4 billion we, and other shareholders, had hoped for more than the HK cents 4 they paid out as an extraordinary dividend. It could have been a bit more generous.

As a matter of fact, they have not increased the dividend since 2013. Ten years with no increase is not a good sign.

SHK dividend history (Aastock.com)

{kind=link}

They do also buy back some shares in most years, so the return of capital to shareholders is not too bad. This year, they have bought back 3.59 million shares, roughly costing HKD10.8 million.

Our other pick is:

Hui Xian REIT, an affiliated company of CK Asset

It was listed in Hong Kong in 2011. The largest shareholder is CK Asset ( CNGKY ) with 32.7% of the units. Last year, they received a dividend of HKD311 million from Hui Xian REIT.

Hui Xian REIT's portfolio spans retail, office, serviced apartment, and hotel sectors in four key cities in China, covering an aggregate area of over 11.8 million square feet.

Hui Xian REIT's office portfolio consists of The Tower Offices at Beijing Oriental Plaza, and The Tower at Chongqing Metropolitan Oriental Plaza. The retail portfolio consists of two shopping centers: The Malls at Beijing Oriental Plaza, and The Mall at Chongqing Metropolitan Oriental Plaza.

The hotel portfolio comprises four international chain hotels in four key cities in China. Serviced apartment portfolio comprises The Tower Apartments at Beijing Oriental Plaza with 836 units and The Residences at Sofitel Shenyang Lido with 134 units.

Beijing Oriental Plaza (Hui Xian REIT 2022 Interim Report)

{kind=link}

It did deliver poor results for FH 2022 as expected.

Out of a revenue of RMB 1,100 million, they had an NPI of RMB 657 million. This was 18% lower than the FH of 2021. To put things in context, the NPI is 50% down from the pre-Covid level from FH of 2019 when it was RMB 1,042 million. Hence, our optimism is based on it clawing back most if not all of this going forward.

With properties like the Grand Hyatt Beijing having its average occupancy rate dropping to only 11.0% in FH this year and only 48.9% last year, it is understandable that it has been two very tough years. Retail also suffered as lockdowns in China meant that people could not go shopping or eat outside.

Their Beijing offices recorded a relatively high vacancy level of 16.4%. It was even worse in Chongqing, where the vacancy was 31.5%

Here is their dividend history since it became listed on the stock exchange

Hui Xian REIT's 10-year dividend history (Data from Hui Xian. Graph by author)

{kind=link}

The dividend has been quite good for many years, and it is not too far-fetched to imagine that once the economy starts to improve, the occupancy rates in hotels will improve greatly and lead to higher earnings for this REIT.

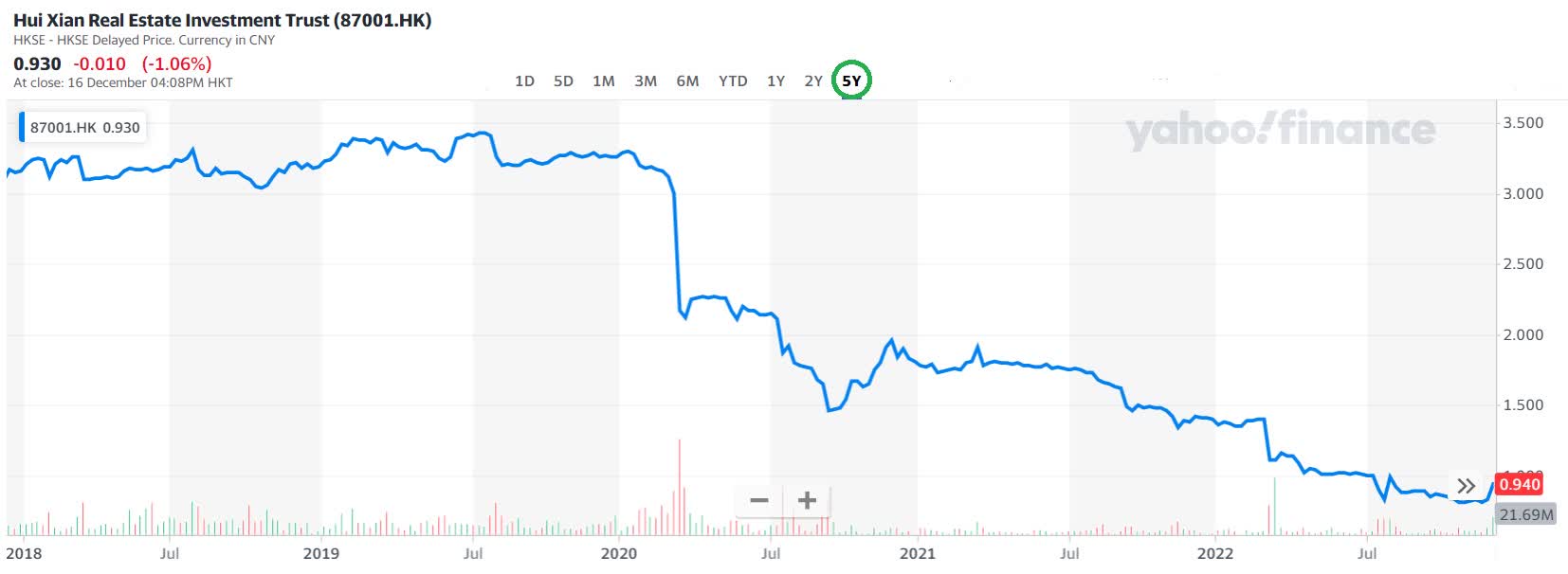

The share price is down 70% over the last 5 years.

Hui Xian REIT 5-year share price development (Yahoo Finance)

{kind=link}

In July this year, we wrote a letter to the Chairman of Hui Xian REIT outlining what we as shareholders thought they should do.

Here is an extract of the letter:

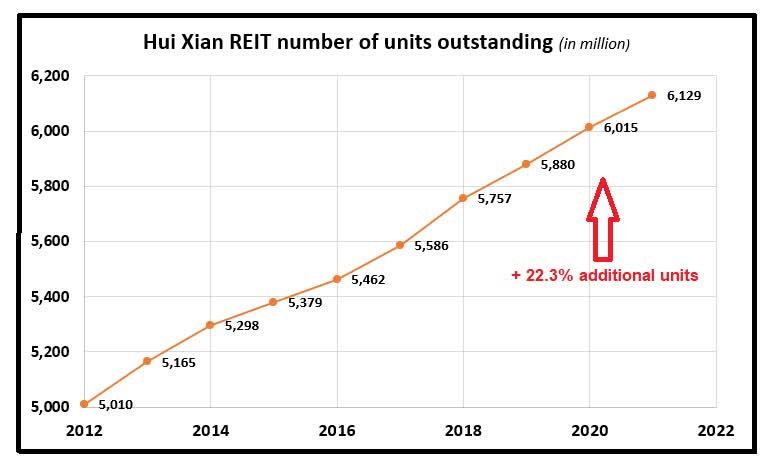

As shareholders in Hui Xian REIT we would like to suggest that the company should seriously consider to stop dilution of shareholders and in fact instead of issuing new shares should be buying back and cancelling as many shares as you could.

When you consider that the NAV/share is RMB 3.99 as of the latest financial results, you have in fact added units to the tune of RMB 4,46 billion without actually adding any productive assets to the trust.

Hui Xian REIT increase in units (Data from Hui Xian, graph by author)

{kind=link}

The worst effect of this type of dilution is that you not only incur a one-off expense like you would if the trust simply paid its manager their agreed management fees and did not issue scrip units to settle distributions. No, in fact, you get expenses that will occur in perpetuity, as these issued units will also be eligible to receive future distributions year in and year out.

To make matter worse, now that the price of your units are trading at roughly RMB 1 per unit as opposed to trading at RMB 3 per unit which it did before, you need to issue 3 times more units to pay for additional units that are issued.

It makes absolutely no sense and is a poor allocation of shareholders' capital. This is also finally starting to dawn on other investors as well.

As your fellow Director, Mr. Lim Hwee Chiang surely is aware of through his close affiliation with ARA Asset Management, he would know that in Suntec REIT in Singapore, where I am also a shareholder, as much as 44.9% of the units voted in April this year against Suntec issuing any new units at this time. Hui Xian REIT is trading at a Price/NAV of only 0.26

It makes it even more obvious, as the lower the ratio the less attractive it is to issue units. As a matter of fact, the wisest thing that the company can do now is to take full advantage of its low unit price and buy back and subsequently cancel these units. That would be a good capital allocation. That is what your sponsor and main shareholders CK Asset and CK Hutchison Holdings often do when opportunities arise.

I do understand that a REIT has an obligation to pay distribution based on a percentage of net property income but with such a low gearing you have room for drawing on such capital to reduce the number of units making each unit more valuable and at the same time saving the company for future payments of distribution.

I hope that your fellow board members also have a chance to read my letter and hope that they too will see what is best for all shareholders."

We were pleased to see that they did take notice. At least, they decided to only take 50% of their fees in new units and the balance in new shares. They also scrapped the option of receiving the dividend as new units.

Valuations

Why did we choose Sun Hung Kai plus Hui Xian REIT?

In terms of being deep value, one of the things we look at is the dividend yield divided by the price to net tangible book value. Let us come right out and state that it is not the only thing we look at. It has to pass certain other litmus tests.

It was a friend of us here in Singapore who runs a small boutique fund with roughly $100 million that had done back testing on how an investor would do if they would buy a small basket of the one with the highest multiples and sell and equal basket of the shares that had the lowest number. This would deliver alpha.

Here is a part of our list that shows Sun Hung Kai and Hui Xian REIT.

Tudor Invest portfolio monitoring (Author)

{kind=link}

Let us first look at the price to net tangible book value. Both these companies trade at or near a 75% discount.

While you wait for the thesis to play out, you get paid between 8.5 and 9% a year.

Other important factors are balance sheets, the quality of its management, and corporate governance. The prospects of the business they operate in are also important.

With regards to their balance sheets, we want to see a conservative debt level, and preferably a very low debt level as this gives us a margin of safety. Both these companies tick that box too.

Risks to the thesis and conclusion

There are many companies out there trading at large discounts to their perceived values.

We have to determine what might be the catalyst that will change people's minds and be interested in owning that particular stock. After all, there is only one way that a share price increases and that is when there are more buyers than there are sellers.

One of the biggest challenges for us value investors is that we can be "right" about the thesis and the catalyst, but we can be wrong about when it will happen. The other day, one of my readers commented on a stock, that he just hoped that it was not a case of "waiting for Godot"

Don't feel ashamed if you do not know who Godot was. I had to look it up too.

One other risk is that the improvement in Hong Kong and China's economy gets delayed. Although, as long as you get paid eight to nine percent to wait, this risk is quite bearable.

Why are these two companies trading at such big discounts?

There has to be some reason(s). It is understandable that a property company with hotels, retail, and office assets in China get hammered in a "zero covid policy" environment. Occupancy level dropped. While most parts of the world learned to live with the pandemic, China has soon suffered for three long years.

Management of Hui Xian REIT could also be much more proactive in deal-making and growing the company. A good example of a China REIT which has done so is CapitaLand China Trust. Let us hope that Hui Xian learns something from them.

It is less clear why Sun Hung Kai is not trading higher.

Looking at the charts we have presented, it's been a nightmare owning these shares. However, the past is just that. We are investing for the future.

Both companies will benefit from China opening up and when consumer and business confidence there starts to flourish again.

Our belief is that this will happen in 2023.

For further details see:

Sun Hung Kai And Hui Xian REIT: 2 Deep Value Picks For 2023 From Asia