NOVA - Sunrun: Secular Tailwinds Will Drive Growth

Summary

- Sunrun is the leader in the residential solar market in the US and continues to show strong growth rates.

- The residential solar market is seeing great growth potential over the next decade as prices drop and adoption increases, driven by tax incentives.

- Sunrun is in an excellent position to benefit from a growing market thanks to its strong business model and large customer base.

- While growth is projected to be strong, the company will also be facing significant challenges with increasing competition and high inflation.

- Sunrun continues to struggle with profitability, and with the company still in growth mode, this is not expected to significantly improve in the near future.

Introduction

Companies focused on green energy generation, primarily solar companies, have had an incredible run over the last couple of years. Despite most of them being unprofitable growth companies, they overly outperformed the global indices last year driven by an energy crisis in Europe and an increased push towards green energy. Even with growth stocks dropping significantly last year driven by higher interest rates, solar companies continued to outperform. To give you some examples:

- SolarEdge ( SEDG ) is up 21% over the last year (up 763% over 5 years)

- Sunnova ( NOVA ) is down by only 11% over the last year (up 77% over 3 years)

- SunPower ( SPWR ) is down by only 7% over the last year (up 229% over 5 years)

- Enphase ( ENPH ) (although very profitable) is up 71% over the last year (up 11,606% over 5 years)

- All compared to the SPY ( SPY ) being down 15% over the last year

And despite these incredible performances, these companies continue to see very strong tailwinds going forward as governments all over the world continue to push for the integration and development of green energy. A prime example of this is the Inflation Reduction Act signed into law by US president Joe Biden on the 16th of August 2022. This bill authorizes $391 billion in spending on energy and climate change. This includes $270 billion in tax incentives. $128 billion is allocated to renewable energy and grid energy storage with solar energy companies most likely the primary beneficiary.

Now, one of the solar companies benefitting from tax incentives, clean energy bills, and continued high demand that I haven't mentioned yet is Sunrun ( RUN ). Sunrun underperformed most of its peers over the last year by losing 15% but is still up by 356% over the last 5 years.

As a provider of photovoltaic systems and battery energy storage products, primarily for residential customers, the company looks well positioned for continued growth driven by the factors named above. It is therefore that I decided to take a deep dive into this company and see if it is a buy at the current price of around $28 per share. To determine this, I will take a look at the company's fundamentals and strengths, growth drivers and expectations, main risks, balance sheet, and valuation.

So, should you buy or avoid it for now? Let's find out!

Sunrun Inc.

For starters, it is crucial to first understand the business model and products that Sunrun offers.

Sunrun was founded in 2007 and is headquartered in San Francisco, California. It is an American provider of photovoltaic systems and battery energy storage products, primarily for residential customers.

The company works with a power purchase agreement business model. This means Sunrun installs and maintains the solar system on a customer's home and sells the generated electricity back to the customer for an agreed-upon rate for a period of 20 to 25 years. This means the customer does not need to pay high upfront costs but also does not get the benefits like tax breaks. In the end, the customer ends up with clean energy at fixed prices and avoids high energy prices and volatility as seen quite recently. Sunrun ends up paying the upfront costs of hardware and installment but earns a fixed fee for a period of 20 to 25 years. In addition to this, Sunrun directly benefits from tax incentives. To make its offerings even more appealing to consumers, Sunrun has a broad network of partners including Costco ( COST ) and Home Depot ( HD ), who allow Sunrun customers to shop in their stores. As a result of this business model, Sunrun creates a very low price for consumers to install solar panels and this has made Sunrun #1 in the residential market. This is also part of the reason why the company can continue to grow at a rapid pace going forward. The one downside to the business model is that it requires capital upfront from Sunrun to install solar installations. As a result, investment costs are quite high for Sunrun. This invested capital will, of course, easily earn itself back in a couple of years' time. The larger the solar installation base is for Sunrun, the larger its revenue stream will become and a very reliable one as well. Also, Sunrun states that typically the 20- or 25-year value stream is financed upfront to fully cover creation costs and generate cash for Sunrun immediately.

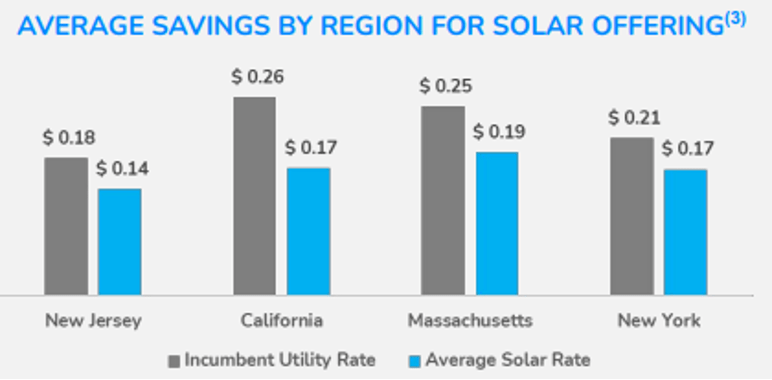

Sunrun says that the estimated annual solar production per home is approximately 9600 KWhrs, while Sunrun holds a price per unit of energy of approximately $0.16. This means Sunrun tends to earn $1536 a year for every installed solar system. The customer can save a lot of money as well, as shown below.

{kind=link}

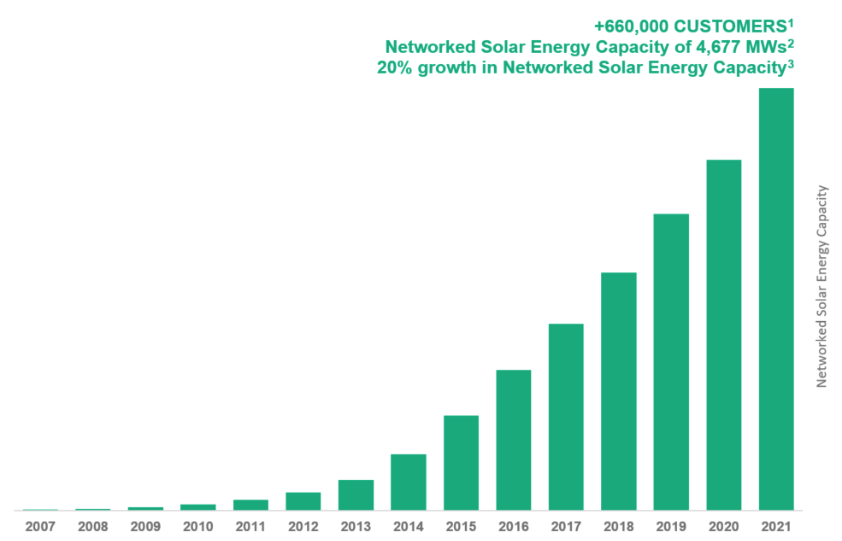

And this brings me to its mission. Important for the performance of any company is a clear mission. So, what is the mission of Sunrun? Sunrun aims to create a planet run by the sun. Yes, this might be a bit too optimistic, but Sunrun has already grown its customer base to a total of 760,000 customers across 22 states, Washington DC, and Puerto Rico. In 15 years of operating history, the company has done a good job at building its solar capacity. Important to take away from this is that Sunrun only operates in the US and Puerto Rico, and not globally.

Sunrun solar capacity growth (Sunrun)

{kind=link}

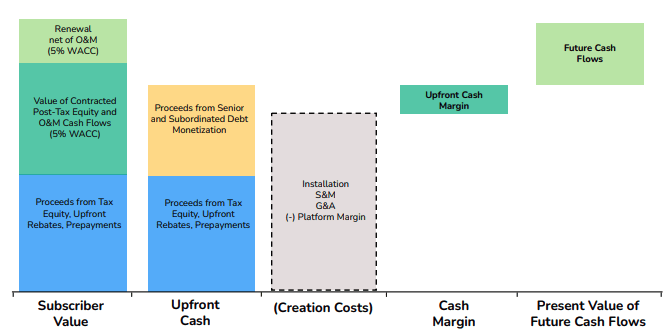

One more important subject to discuss for Sunrun is its cash creation. How much money can it make from this business model? The picture shown below illustrates the cash flows from Sunrun. The company raises non-recourse debt against contracted subscriber value, and this allows it to convert a significant portion of value to cash upfront while it continues to build a long-term recurring revenue stream. A very solid business model is created this way and it assures strong recurring cash flows. The larger Sunrun manages to grow its customer base, the larger the recurring revenue will be. With Sunrun now still in its growth phase, investors should be focused on it growing the customer base. With margins for Sunrun currently sitting around 15%, this isn't something to be overly positive about. It is hard for solar companies to differentiate themselves from the competition while Chinese competitors and price fighting is driving margins lower. Though, we should still expect Sunrun to increase its margins over time as its user base grows. With the company signing contracts of 20- to 25 years, the business is sticky. Also, customers are expected to renew their contracts at the end of the contract as the only other solution is buying the 25-year-old solar system or getting it removed.

{kind=link}

And while Sunrun already has a large customer base, the residential solar market is still underpenetrated and massive. According to Sunrun, even if the industry would grow at the expected 15% CAGR for the next 10 years we would still only have a 17% penetration of US houses as the market grows from 0.2 million to 14.1 million. So far, penetration is only high in the states where this would be most evident like Hawaii and California. To put things into perspective, Sunrun is currently responsible for less than 1% of the US residential electricity market.

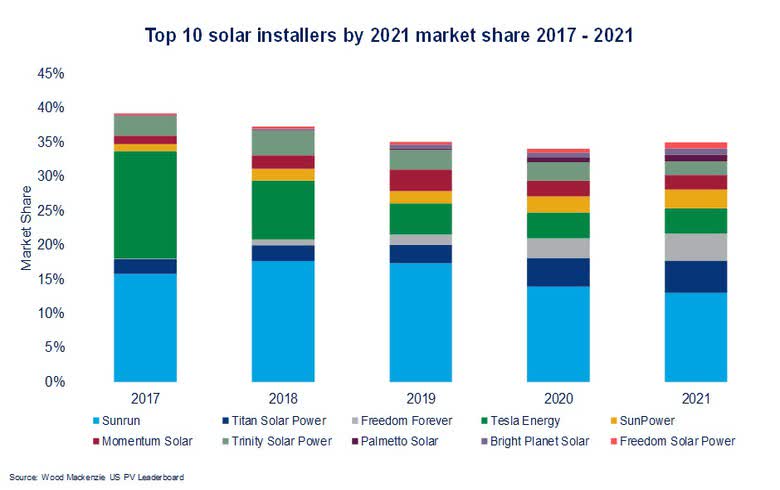

This means there is still massive growth potential remaining for Sunrun and the company is in a pole position as Sunrun is the residential market leader in the US. According to Sunrun itself, it has approximately an 18% market share across the entire US solar market (so not only residential) while holding a 66% market share in solar subscriptions. Although, it should be said that the company is seeing increased competition over the last several years and has seen its market share fall. According to Wood Mackenzie , Sunrun held a 13% market share in FY21 for total installed solar.

Solar market split (Wood Mackenzie)

{kind=link}

According to Grand View Research , the US residential solar PV industry will grow at a 15.4% CAGR until 2030 and therefore confirms the growth rate expected by Sunrun. But what factors are driving this growth besides government incentives and increasing demand for green energy?

While there are many factors driving green energy adoption, I want to highlight three in this article.

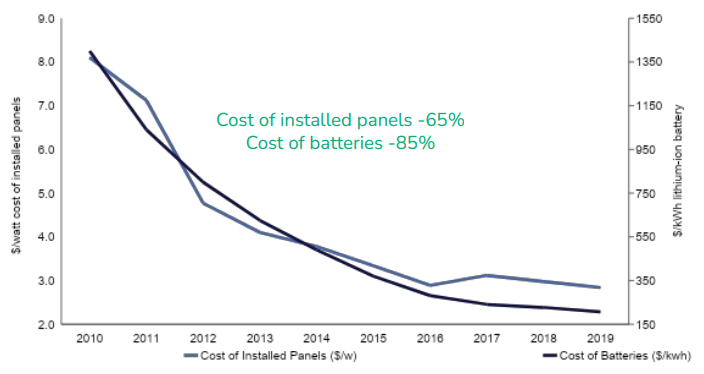

Declining solar and battery costs

The costs for solar installations and batteries have been dropping over the years as adoption increased. Market research predicts that this significant decline in prices will continue for the foreseeable future. Forecasts expect the cost of solar installations to drop by a further 34% over the long term, while battery costs are expected to decline by 64% over the next 10 years. The faster decrease in prices for batteries will also be driven by the increased adoption of electric vehicles. With prices of materials coming down, it is most likely that prices for consumers will also trend down, though most likely at a slower pace with most solar companies preferring higher margins and profitability. Lower prices will allow for increased adoption as it will become more affordable. This should drive both industry growth and growth for Sunrun.

Price of solar and batteries (Sunrun)

{kind=link}

Electric vehicle penetration

That electric car adoption is increasing is no surprise to anyone as shown by the massive growth of Tesla (TSLA) over the last couple of years. This transition is not only expected to continue but to accelerate. Crucial for this shift is the energy supply for all these electric cars. According to Sunrun, vehicle energy needs are expected to grow at an 18.4% CAGR requiring a massive increase in the electrical power supply.

According to this report from the IEEFA the increased adoption of EVs will also be a main contributor to higher residential solar PV penetration. As we have seen over previous years, the adoption of both EVs and solar PV increased at a comparable pace. This is mainly due to the fact that 80% of all charging happens at home. A solar system on your house would then greatly reduce your energy bills and would most likely let you drive for free.

Inflation Reduction Act (IRA)

The IRA is expected to be a significant tailwind for the solar industry. The IRA includes significant tax benefits of 30% for every solar installation, battery storage, or home charger. When the solar system uses domestically produced products, there will even be an additional 10% tax credit. In the end, this means Sunrun (and the entire industry) can realize the same expansion plans, but at a 30-40% discount than previously anticipated. This will most likely increase profit margins, adoption by consumers, and expansion plan realization.

Company-specific growth drivers

The points mentioned above will be able to drive continued growth for the residential PV industry, but what more growth drivers are there for Sunrun?

In its investor presentation of November 2022, Sunrun points out a couple of factors that could drive additional growth. One of these is the opportunity to cross and upsell to existing customers. We should keep in mind here that Sunrun has a 25-year contract with its customers, and this gives it plenty of opportunities to sell the customer additional products and upgrades such as batteries or EV chargers. By doing this, Sunrun can derive higher revenue per customer and increase profitability and revenue.

Also, Sunrun continues to see plenty of margin expansion opportunities. As the business grows its user base, the ARR will also significantly increase which will ensure Sunrun of a solid revenue stream. Still, we should expect the company to remain in growth mode for the foreseeable future as the most important thing right now is to capture market share and outpace competitors. With a contract for 25 years, it is hard to take away customers from competitors, and vice versa. Therefore, it's crucial for Sunrun to focus on customer growth over profitability and we should not expect a significant increase in margins over the next couple of years.

Balance sheet

Now, let's have a look at the balance sheet of Sunrun. I can tell you already, it is not very pretty. Sunrun currently has $672 million in cash on the balance sheet and holds $8.35 billion in total debt. This means that Sunrun currently holds a significant net debt position of above $7.5 billion and this is not great for a company that is still in growth-at-all-costs mode.

Though, it should be said that this matches the business model of Sunrun, which simply requires a lot of upfront investments from Sunrun. These investments will eventually repay themselves through annual recurring revenue from subscription and solar energy contracts. I am therefore not very worried about the current debt level of Sunrun. While I would prefer less debt and more cash, I understand that Sunrun currently continues to focus on capital investments to grow its customer base.

All in all, net debt is quite high, but mostly due to solar lease contracts and PPE agreements, so investors should not be overly worried. Still, I would prefer to see Sunrun lowering the debt burden over the next couple of years.

Valuation

The company definitely is not cheap, but I would also not call it very expensive. While a P/E of 81 does sound very expensive, we should keep in mind that the company is not focusing on profitability and so P/E is not a fair way to value the company.

Sunrun currently receives a B rating for its valuation from Seeking Alpha and is valued at a P/S of 2.58. If we compare this to competitors like SunPower (P/S of 1.91), First Solar ( FSLR ) (P/S of 7.33), and Brookfield Renewable Partners ( BEP ) (P/S of 2.72), we can say that Sunrun is not the cheapest nor the most expensive.

According to Seeking Alpha, the average wall street analyst price target currently stands at $46.24 per share and projects over 66% of potential upside over the next 12 months. With my expectations currently sitting slightly above analyst revenue projections (as I will show you later), I believe we can assume this to be a reliable price target. This means Sunrun has very strong upside potential for the next 12 months.

Outlook

Driven by all points mentioned and discussed in this article, I believe Sunrun will continue to see solid growth over the next decade. Sunrun seems to have a clear growth path ahead. The continued adoption of solar systems is expected to continue over the next decade and even if the industry grows at the expected 15% CAGR, there will still only be a 17% market penetration and so it should be absolutely no problem for Sunrun to expand its business and sell its products. I believe solar to be one of the leading forms of energy supply in the future and am very bullish on the industry for this exact reason.

While Sunrun has an excellent market position, I do expect the industry to become increasingly competitive. Still, Sunrun has a solid business model and will maintain its excellent position in the residential solar industry. With residential solar significantly growing over the next decade, I expect Sunrun to maintain its overall solar market share of between 15 -20%.

Current analyst estimates point to decent growth ahead as shown below. Sunrun will be lapping tough comparable quarters for FY23 after a strong 2022. It is important to point out that estimates are quite far apart as some analysts are much more bullish on the company than others.

I expect Sunrun to report revenue growth of approximately 13% as it continues to benefit from strong solar adoption and tax benefits. Yet, growth will be held back slightly due to higher interest rates, high inflation, and lower consumer spending which could very well be a reason for consumers to postpone any expensive investments (although Sunrun's subscription offering does not require high initial investments). I do expect the economy to avoid a severe recession and we will either avoid a recession at all or end up in a mild recession. In addition to this, the IRA incentives will partially offset economic weakness and boost solar investments.

Growth will most likely accelerate again in FY24 and FY25 to approximately 18% and 25%, respectively. This growth acceleration will be driven by a rebound in consumer spending, lower interest rates, and a rebound for the solar industry after a difficult 2023. I expect to see continued residential solar adoption and Sunrun as the main beneficiary. The IRA will also continue to be a significant tailwind. Growth will most likely slow down to a more normal growth rate of 10-15% for the remainder of the decade, yet Sunrun can continue to grow at a faster clip driven by market share expansion and new product introductions.

That means that my expectations are currently slightly higher than that of analysts although lower than the highest expectations. My expectations guide for Sunrun to report revenue of $2.59 billion for FY23, $3.05 billion for FY24, and $3.82 billion for FY25. Please note, I believe these estimates are still quite conservative and Sunrun could very well outperform my expectations.

Revenue projections (Seeking Alpha)

{kind=link}

Profitability will most likely remain tough for Sunrun, although it is expected to see a positive EPS for FY22. Analysts are currently guiding for EPS to turn negative again for the next 2 years, although, again, analyst estimates lie very far apart. Profitability will primarily rely on the number of continued investments from Sunrun. I believe Sunrun will report a negative EPS for FY23 as investments and Capex will outpace revenue growth due to a slowdown in growth and additional pressure on margins due to continued high inflation causing upfront installation costs to remain elevated. The IRA tax benefits will most likely not be able to completely offset this.

FY24 EPS will be right around zero as revenue will still be catching up to Capex and inflation will most likely fall back to between 2-3% according to current projections. Sunrun will most likely start reporting solid positive EPS again for FY25 and will continue to do so for the following years.

It should be noted that these EPS estimates are highly uncertain as they very much depend on continued Capex, and this is hard to predict for Sunrun. These EPS estimates should therefore be considered highly uncertain, and I would recommend focusing on customer and revenue growth for now with the company still in its growth phase.

Risks

The growth outlook looks strong, but what are the possible risks to the outlook?

One of the main risks for Sunrun will be continued cash burn. The company is still very much struggling to report a positive bottom line as competition is increasing and inflation causes elevated upfront installation and product costs. Sunrun will be able to offset this partially with higher electricity costs for customers, but this will only pay itself back over time. As a result, Sunrun will keep struggling with profitability resulting in a further deterioration of the balance sheet. If these profitability headwinds will turn out worse than expected, this could have a significant impact on EPS estimates, and it could take longer for Sunrun to report solid EPS digits every quarter. Lower EPS expectations will most likely result in a lower share price. The IRA could be a margin tailwind for Sunrun as it offers solid tax benefits of 30% and due to the business mode of Sunrun, they will benefit massively as upfront costs will fall.

Another important factor for Sunrun and current estimates is the health of the US economy. With some analysts guiding for a severe recession and others for a soft landing (and everything in between), it is hard to predict what we should expect this year. While I believe we will avoid a severe recession and should prepare for a soft landing, there is the risk that we will enter a severe recession, and this could then have a significant impact on the business outlook for Sunrun. Consumer spending will fall further impacting the investments consumers will be willing to make in green energy initiatives and this will most likely impact Sunrun as well. As a result of a severe recession, revenue growth expectations would have to come down and profitability will continue to struggle as well. Again, I do not expect the economy to see a severe recession, but it is important to note that this is a significant risk to Sunrun.

Conclusion

Sunrun has a great business model, and I believe the company has a long runway of growth ahead of it. I am bullish on the solar industry, and the residential sector even more. With current penetration still extremely low, we should expect strong continued growth over the next decade, and with Sunrun currently holding the #1 position, it will be the main beneficiary.

I am bullish on Sunrun and expect the company to show excellent revenue and customer growth going forward, although 2023 might turn out to be more challenging due to high inflation, rising interest rates, and the fear of a recession resulting in lower consumer spending.

With EPS expected to turn negative again for 2023, Sunrun might not be for every investor. I expect Sunrun to keep struggling with profitability over the next couple of years, but with ARR increasing at a strong pace, the company is laying down a solid foundation for profitability. Also, Sunrun will benefit from tax incentives which will lower its upfront material and installation costs and drive up margins. Still, the company remains in growth mode, and will likely continue to for the next 5 years at least. I think investors should focus on customer growth and an increasing ARR as signals of a growing business. In addition to this, one needs to be willing to pay for future profitability which might take some years.

All in all, I rate Sunrun a buy at prices of around $28 per share as the company has plenty of upside potential and is very well positioned in the US solar PV market. The IRA and increased solar adoption will remain significant tailwinds for the company. The current valuation is acceptable and in between peers. With Wall Street analysts having an average price target of $46.24, I believe the company offers enough upside potential to warrant a buy rating.

For further details see:

Sunrun: Secular Tailwinds Will Drive Growth