SUNW - Sunworks: Thriving In Solar Power And Energy Storage Growth

2023-03-20 10:14:47 ET

Summary

- Sunworks enjoyed outstanding 60% YoY top line growth this FY'22, due to strong residential installations, which accounted for 88% of its total revenue in FY'22.

- Its focus on improving operating efficiency and financial performance makes its 2023 plan more exciting as the management provides a positive outlook for getting towards breakeven EBITDA.

- SUNW is currently undervalued, despite some financial weaknesses.

- Sunworks' debt-free balance sheet and its positive value-adding catalyst position the company well for future growth and make it an attractive buy candidate in today's bearish environment.

Sunworks, Inc. ( SUNW ), a company operating in the rapidly growing solar energy industry, specializes in providing solar power and storage systems for both residential and commercial markets. This FY'22, SUNW's residential installations accounted for approximately 88% of its total revenue, up from 77% a year ago. Despite this growth, according to the management, distributed residential solar energy has yet to achieve broad market adoption, as it has penetrated less than 5% of its total addressable market in the U.S. residential sector. Today's better Solar Investment Tax Credit , combined with the increasing demand for environmentally friendly and economically beneficial renewable energy sources, positions Sunworks for continued success in the expanding solar energy market .

Company Overview

SUNW operates under three segments: Residential Solar, Commercial Solar Energy, and Corporate. Its main business is providing solar energy solutions for homes. Its Residential Solar segment generated revenue of $139.9 million recorded in FY’22, up from the $72.2 million in 2021. This increase was mostly due to higher installation volumes and the positive impact of its acquisition, Solcius, in 2021. However, we can see that its Commercial Solar Energy segment’s revenue slowed down to $21.9 million from $28.8 million. According to the management, this was due to project delays. In fact, the management boasted their outstanding growth in backlog, as quoted below.

And then in our commercial business, the pipeline I said the backlog is we have about $33 million in our backlog today. We'd expect our backlog to grow in Q1 based on recent order activity and conversations with customers. So we're anticipating revenue growth throughout the year in our commercial business. But again, Q1 is going to be a little light because again, revenue was impacted and delivery dates were impacted by the weather in California.

Overall, SUNW ended FY'22 with $161.9 million in total revenue, representing a 60% year-over-year increase. This impressive growth can be attributed to the company's strategic focus on the residential solar market. As the demand for renewable energy continues to rise, Sunworks is well-positioned to capitalize on the expanding solar energy market.

Additionally, it is interesting to see a growing gross margin despite today's inflationary environment. In fact, looking at the image below, we can see an improving trend.

SUNW: Improving Gross Margin (Source: Data from SeekingAlpha. Prepared by the Author)

Sunworks is taking steps to improve its operations and reduce costs while expanding its offerings in the solar solutions market, as quoted below.

During 2022, we continued to build a leading integrated solar solutions platform across our core regional markets, while continuing to advance our business transformation strategy. Last year, we continued to drive an improved velocity of installation, ensuring improved customer retention between project originations and installations.

We continued to reweight origination toward our direct sales channel, thereby reducing customer acquisition expense. We expanded our procurement relationships with an emphasis on increased access to domestically sourced materials. And we moved further towards a centralized operating model, one that further positions us to move quickly in support of individual customer requirements.

-Source: Q4'22 Earnings Call Transcript

Better SUNW (Source: Earnings Call Transcript)

The company is focusing on various initiatives, including decentralizing design and developing a direct sales team to improve efficiency and financial performance. Management expects 2023 to be a pivot year of profitability as the company accelerates installation velocity and sustains margin expansion. If successful, these efforts could lead to improved efficiency and stronger financial performance.

Additionally, as shown in the image below, SUNW has an outstanding backlog on both of its main operating segments, which supports the company's continued improvement in financial performance.

SUNW: Demand Is Still There (Source: Earnings Call Presentation)

In fact, management provided a positive adjusted EBITDA outlook, as quoted below.

On balance, I'm positive on the outlook for our businesses entering 2023. A combination of sustained market share gains, recent price actions and favorable long-term demand fundamentals, particularly with the added benefit of the IRA, position us to move closer towards EBITDA breakeven .

-Source: Q4'22 Earnings Call Transcript

Potential Entry Point for Investors Despite Today's Bearish Trend

{kind=link}

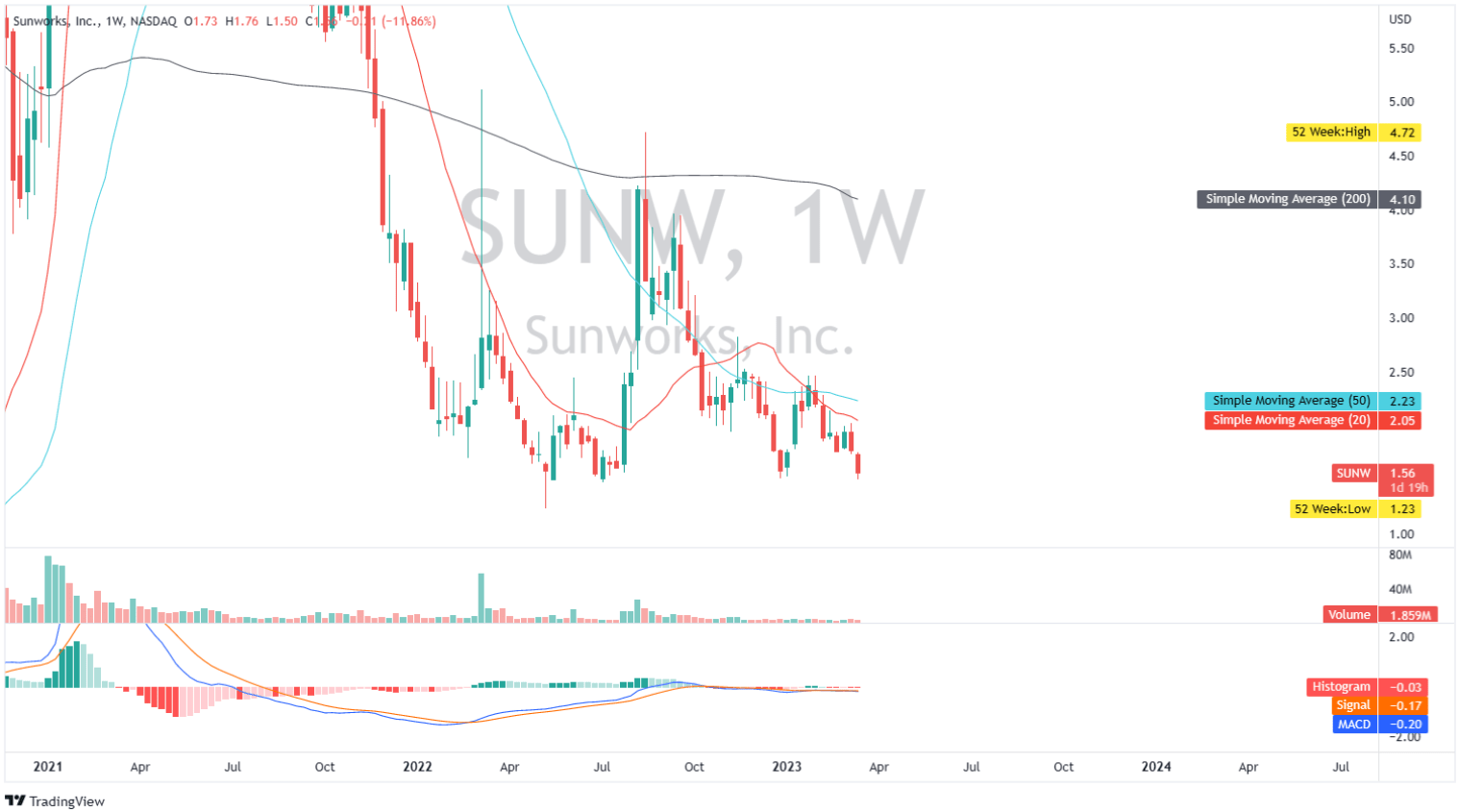

SUNW: Weekly Chart (Source: Author’s TradingView Account)

SUNW is currently facing a strong bearish momentum as shown in the chart above, where its 200-day Simple Moving Average (“SMA”) is trading above the current price, which means the stock might have difficulty getting higher. Additionally, the 50-day SMA is below the 200-day SMA, which suggests a continuation of today's bearish trend.

Despite the current market conditions, it appears that SUNW is currently entering a significant support area. As of this writing, the stock is trading close to the next support level of approximately $1.25, a level where it has shown successful rebounds in the past. This indicates that there may be potential for positive price action in the near future. The MACD line is below the signal line, meaning the stock might decline a bit more in the near term.

In my opinion, scaling in at these levels offers a safer entry point, which provides a positive risk/reward ratio as of this writing. Additionally, a potential break of its 20-day and 50-day SMAs resistance levels could propel the stock higher, making it an attractive stock.

SUNW's positive EBITDA in sight

According to SeekingAlpha Quant Ratings, SUNW has a valuation grade of A , indicating that the company is currently undervalued compared to its sector median and significantly undervalued compared to its historical performance. These findings suggest that SUNW may present a good investment opportunity for investors looking to buy undervalued stocks.

Additionally, SUNW appears to be undervalued by the market, as indicated by its forward and trailing EV/Sales ratios of 0.28x and 0.35x, respectively, which are lower than its 5-year average of 1.36x. Its low EV/Sales ratios and impressive revenue growth presents a favorable opportunity. In fact, SUNW revenue's 5-year CAGR of 15.90% significantly outperforms its peer SunPower Corporation's (NASDAQ: SPWR ) -0.60% 5-year CAGR, further supporting the bullish case for investing in SUNW.

It is important to note, however, that SUNW's financial performance appears to be weak, with negative EBIT, EBITDA, and net income . Furthermore, the company still has a negative cash flow from operations amounting to -$28.19M. These factors may indicate potential risks for investors and suggest that the company is not performing well financially. This is especially true, especially considering its estimated forward P/E in 2024 of -13.20x than its peer SPWR’s of 19.35x in 2024. In my opinion, given SUNW's expanding customer base and their focus on improving installation processes, there is a high likelihood of sustained revenue growth, which in turn could drive improvements in the company's margin performance.

It's worth noting that analysts are now predicting a positive EBITDA of $2.10 million for SUNW in 2024. This could have a significant impact on the company's cash burn rate, which is expected to decrease notably in the coming years. In fact, SUNW's cash flow from operations is expected to improve in 2023, with a positive $2.0 million expected in 2024 .

Final Key Takeaway

SUNW's balance sheet remains liquid, with no long-term debt on its balance sheet. This is attractive in today's high-interest-rate environment, where companies with high debt levels may be at risk. The lack of long-term debt on SUNW's balance sheet may suggest that the company has a lower risk of default, which could make it more attractive especially in today's high interest rate environment.

SUNW ended FY'22 with $7.8 million in cash, which is a positive, but of course the cash burn rate may worry investors. However, management remains confident that they are still liquid and can fund operations in the next full year. If the worst-case scenario were to occur, such as revenue growth not meeting expectations, we could potentially see continued cash burn, which may result in an increase in debt or dilution.

Another growth driver for the company is the passage of NEM 3.0, set to take effect on April 14, 2023, could serve as another catalyst for value addition. It is expected to potentially increase demand for energy storage solutions, as it reduces the export rate of excess solar energy to the grid. This, in turn, could drive greater interest in energy storage solutions like battery storage, enabling customers to store surplus solar energy for later use. This position SUNW well and may potentially benefit from this trend, as indicated below.

So California has been strong. We're starting to book out production slots or install slots into Q2. So if we continue to see the strength that we have seen over the last several weeks, I wouldn't expect a significant drop off in Q3. At the same time, I just want to focus on we're continuing to bring on new dealers and expand these direct sales.

-Source: Q4'22 Earnings Call Transcript

In summary, SUNW has shown some weaknesses in its recent performance, with a negative cash flow from operations and a less favorable valuation compared to its peers. However, the company's growing customer base and backlog indicate a positive trend and make it an attractive investment opportunity. Furthermore, the management's focus on building the direct sales channel is expected to result in cost savings for the company in the long-term, challenging the idea of continued cash burn. In light of these factors, SUNW is considered a good buy candidate in the current bearish investment environment.

Thank you for reading and good luck everyone!

For further details see:

Sunworks: Thriving In Solar Power And Energy Storage Growth