SGHC - Super Group: Betting On Growth

2023-11-17 12:51:43 ET

Summary

- Super Group operates two prominent online gambling sites on an international basis with in-house technology.

- The company's growth has halted as regulatory frameworks in the industry have created challenges.

- If further regulatory changes don't create significant issues for the company, Super Group seems poised for growth that isn't priced into the stock.

Super Group ( SGHC ) operates online gambling sites. The company has battled with regulatory changes slowing down Super Group's plans of significant growth, with a recent exit from the Indian market due to tax changes. If the company's issues subside in the future, I believe that Super Group is positioned for significant growth. In the scenario that Super Group manages to organically grow revenues, the current stock price seems like a very intriguing opportunity.

The Company & Stock

Super Group operates two online gambling brands - Betway, a sportsbook-focused brand, and Spin with an online casino offering. The company operates on an international basis - Americas represent 39% of the company's revenues, Africa represents 29%, Europe represents 16%, with the rest coming from other territories. Unlike many operators in the industry, Super Group prides itself on in-house technology - often sportsbooks and casino sites source odds, UI/UX, and player account management among other things from third-party providers, but Super Group develops the entirety in-house.

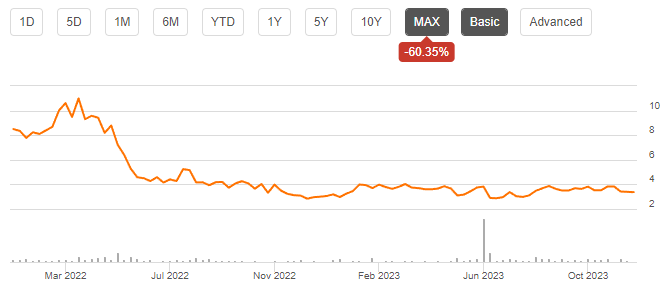

Since Super Group began trading after a SPAC merger in early 2022, the stock has lost the majority of its value as the company's growth has trailed from a desirable level:

Stock Chart From SPAC Merger (Seeking Alpha)

{kind=link}

Financials

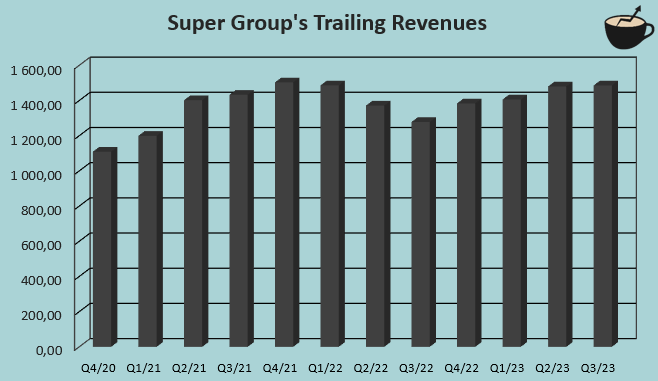

Super Group has achieved some growth, although in recent years the growth has been quite turbulent, and the company has had quarters with decreasing revenues :

Trailing 12-Month Revenues (Author's Calculation Using TIKR Data)

{kind=link}

The company's revenue decreases have been in multiple geographical areas. The most notable year-over-year drop in Q2/2022 was due to weak casino revenues from Canada, an exit from Netherlands and Germany, and weak sportsbook revenues in Europe - different regulatory changes have proven difficult for Super Group. Super Group has mostly achieved a good amount of growth in verticals that haven't seen regulatory changes; if the global regulatory framework doesn't see significant negative changes for the industry in the future, Super Group's growth could be well above the previous years' achieved level. The US seems like a promising market for the company, with Super Group planning to expand in the growing market.

On an offering-based level, Super Group's casino offering has recently performed quite well with the company's casino offering. As of Q3, Super Group's online casino revenues have increased by 5.1% year-to-date on a year-over-year basis, and fixed odd contingencies that are casino-style games under sportsbook licenses grew by an impressive 323.5%, now representing 13.7% of Super Group's revenues. On the other hand, sports betting revenues have decreased by -17.1% as the company has faced regulatory issues in Germany and India, with a recently announced exit from the Indian market.

When looking at Super Group's GAAP earnings, the company's margins seem to fluctuate very widely with a current trailing EBIT margin of 4.8%, down from 2021's level of 15.6%. The company's operational EBITDA gives a more accurate estimate of Super Group's profitability, although the figure doesn't account for investments in growth. The company is aiming for a long-term operational EBITDA margin of 20%, with the company foreseeing a margin of 17.8% for 2023.

Operational EBITDA Performance (Super Group Q3 2023 Presentation)

Valuation

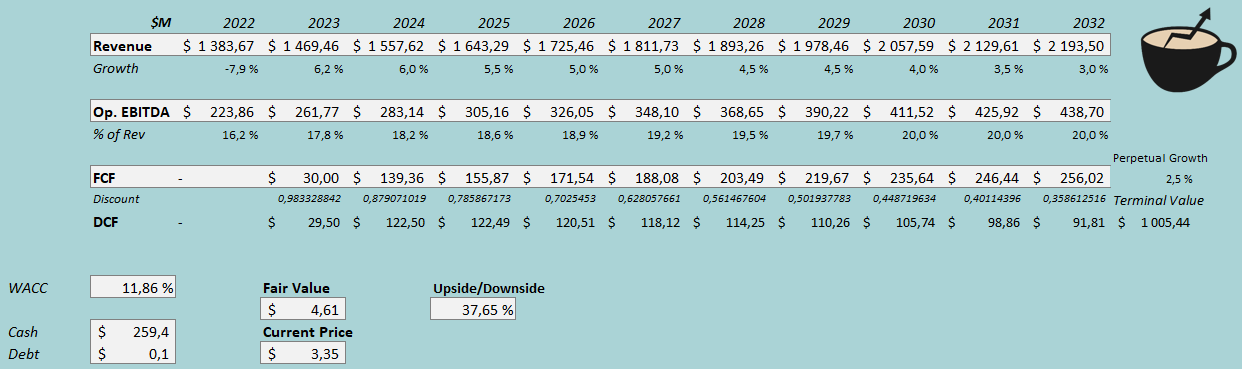

To estimate a rough fair value for the stock, I constructed a discounted cash flow model in my usual manner. In Super Group's case, it seems that other methods of valuation seem quite difficult with complicated earnings and growth prospects. The DCF model only accounts for organic performance, although Super Group's balance sheet seems strong enough for M&A activities. Also, as Super Group's history has demonstrated, the regulatory framework for the gambling industry can be challenging to evaluate especially considering Super Group's international presence; the model assumptions represent a scenario in which further regulation doesn't create very significant issues for the company.

For Super Group's revenues, I estimate quite moderate growth. After 2023, I estimate the growth to be 6%, and to slow down in the coming years slowly into a perpetual growth rate of 2.5%. The company could grow significantly faster than I estimate, but I try to factor in some further regulatory issues slowing Super Group's growth down. Altogether, the revenue growth represents a CAGR of 4.7% from 2022 to 2032.

For the company's margins, I estimate some leverage achieved through the growth. Unlike my usual method of estimating EBIT, I believe that estimating operational EBITDA is a more straightforward way to evaluate the company's earnings. I estimate a margin of 17.8% for the current year, in line with Super Group's outlook. After the year, I estimate the margin to rise slowly with operational leverage into an eventual operational EBITDA margin of 20.0%, achieved in 2030 and forward. The cash flow conversion in the DCF model in my opinion accounts for a fair amount of further investments in technology.

The mentioned estimates along with a cost of capital of 11.86% craft the following DCF model with a fair value estimate of $4.61, around 38% above the stock price at the time of writing:

DCF Model (Author's Calculation)

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Super Group doesn't currently own any significant amount of interest-bearing debt. I don't see the company drawing debt in at least the medium-term future either, if the company doesn't complete a significant acquisition - in my CAPM, I estimate a long-term debt-to-equity ratio of 0%.

On the cost of equity side, I use the United States' 10-year bond yield of 4.53% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the US, made in July. Yahoo Finance estimates Super Group's beta at 0.86 - gambling is mostly defensive in nature. Finally, I add an ESG addon of 1.75% and a liquidity premium of 0.5%, crafting a cost of equity and a WACC of 11.86%.

Takeaway

I see Super Group's current valuation as a good risk-to-reward - due to previous challenges, the stock doesn't seem to be priced for growth that Super Group could achieve. Still, it is important to note that the risk on the investment case is quite high - further regulatory headwinds can easily break the growth story for Super Group, potentially making further losses for investors; the DCF model that estimates upside is based on an assumption that regulatory headwinds stay at a modest level in the future. Still, I see the baseline scenario as quite positive for Super Group, and have a buy rating for the stock for the time being.

For further details see:

Super Group: Betting On Growth