SGHC - Super Group: Canada Is A Growth Catalyst

2023-12-04 06:34:58 ET

Summary

- Canada is the growth catalyst.

- Super Group has a dual-brand strategy with Betway for sports betting and Spin for online casino offerings, which enables it to capture market share.

- Margin should expand to peers' level over time.

Investment overview

I believe Super Group ( SGHC ) stock is worth $4.26, and I am giving it a buy rating. In my opinion, SGHC should have no issues accelerating its growth to the industry level of ~10% over the coming years as Canada opens up its online gambling market. SGHC should also see margin expansion as it grows its revenue due to its go-to-market strategy and operating leverage from owning its tech stack.

Business description

SGHC went public via the merger with Sports Entertainment Acquisition Corporation early last year (2022). SGHC is a digital-only online sports betting [OSB] and iGaming operator that has a presence in multiple regions. As of FY22, 42% of revenue was from North America (primarily Canada), 22% from Asia Pacific, 21% from Africa and the Middle East, 12% from Europe, and the rest from South America. SGHC has two key brands in the market, Betway and Spin, both adopting a different go-to-market approach (more details below) to maximise their distribution reach and unit economics. Pre-covid, performance has been incredibly strong, with revenue jumping from $425 million in FY19 to $1.3 billion in FY21. However, growth started to normalise as the COVID-lockdown period ended, with FY22 revenue falling by 2.2%. On the balance sheet end, SGHC is in a pretty comfortable position due to its net cash position of $90 million and is generating positive free cash flow.

Canada is a growth catalyst

I believe there is still a very long growth runway ahead of SGHC because of the situation in Canada. While SGHC does not disclose how much revenue Canada contributes in the recent filings, we can infer from management comments that Canada is the largest contributor.

"Canada remains an important region for us. Canada ex-Ontario performed well with year-over-year growth, despite adverse movement of the Canadian dollar against the Euro last year." 2Q22 earnings

"We have a good geographical spread with our largest regions being America's, which is mainly Canada for now, Africa and Europe. In 2023 we'll be breaking down Betway into two segments being Betway USA and Betway rest of the world." 25th Annual Needham Growth Conference

Currently, Canada is going through an important transition from a grey to a regulated market, starting with Ontario (on April 4, 2022), which represents around 40% of Canada's population. For historical context, Ontario is the first and currently the only province with legalised and regulated online sportsbooks. I see this as a massive step towards the full legalisation of OSB and iGaming across the entire country in the years to come. While Canada is a very big country, the population is concentrated in four key states : Ontario, Quebec (24%), British Columbia (23%), and Alberta (11.5%). In my opinion, these 3 other states are already "in-progress" on fully legalising the market. In Quebec, online betting is technically legal, as residents can place bets through the government-owned entity Loto-Québec. The same is true for British Columbia and Alberta, where government-owned entities are the sole operators of online betting. As such, it is not something new that the state government needs to study, and if Ontario's transition to an openly regulated market is successful, I think it is only a matter of time before the other states follow through.

As such, I see Canada as a significant catalyst for growth. to give a sense of the potential market expansion. Consider that Ontario has a population size of 15 million and generates around CAD840 billion in GDP, equivalent to around CAD56k GDP per capita. The total population of the other 3 major states is around 19 million and generates a total GDP of ~CAD1 trillion, equivalent to around CAD55k GDP/capita as well. In this sense, I would expect the market size to potentially double. While I do not know exactly when Canada will fully open them up and how big the exact market size is, experts have estimated that within the next 5 years, the size of sports betting could propel from CAD500 million to CAD28 billion, a significant increase.

{kind=link}

Statistics Canada

Favorable business model with own tech stack

I am a believer in adopting hybrid strategies to reap the best of each strategy, if it works. In the case of SGHC, I believe it makes sense to adopt both a single-brand and a multi-brand approach. Betway is SGHC's single-brand approach to OSB. The benefits of a single brand approach are that marketing spend is going to be much more efficient, and it's easier to find an anchor in consumer's mind share as follows:

- SGHC does not need to recreate new marketing collaterals (logos, campaigns, etc.).

- A single ad can be broadcast to the entire nation.

- It is easier for consumers to remember Betway as they keep seeing the same ads everywhere.

Importantly, with a single brand, it makes it easier for SGHC to penetrate into other markets internationally. Especially for online gambling, where there is a strong social stigma, I believe regulators and consumers would prefer a well-known site.

However, the downside to this strategy is that it is hard to pivot and offer new product offerings as consumers have already embedded in their mind that Betway is for OSB. While this drives strong retention, it reduces the potential for more opportunistic growth, like other online casino offerings. This is where SGHC's multi-brand approach makes a lot of sense. Spin is SGHC's multi-brand online casino offering, which offers casino-related offerings. For one, this allows SGHC to capture a larger part of the overall online gambling market. Two, this approach does not result in a major cash burn as it relies on other independent affiliate marketers to distribute its brand and product, and it can focus its reinvestments and efforts on Betway.

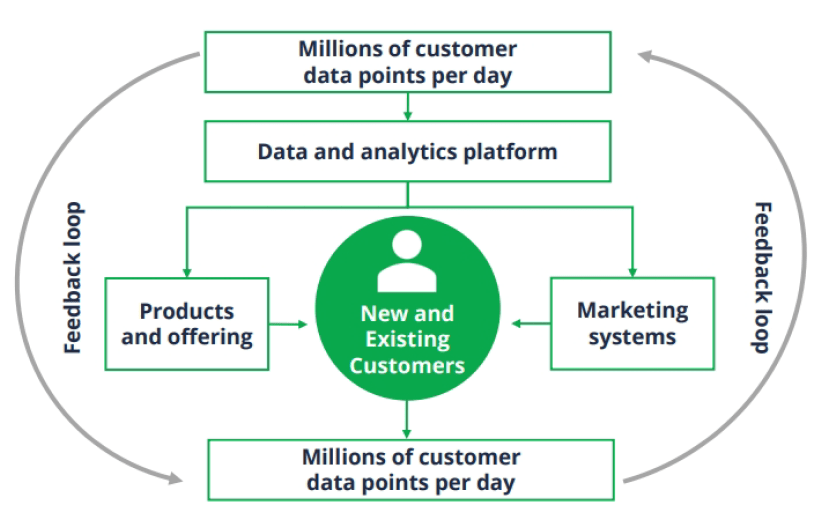

The data-driven approach is also a key factor in SGHC's success, in my opinion. This is an important point to note, as this data drives both customer growth and retention. With this information, SGHC can keep up with the newest betting trends and preferences and know when to give bonuses to customers to keep them on the platform. Simply put, SGHC can use this data to provide a superior customer experience by recommending the right bet at the right time.

{kind=link}

Operating leverage

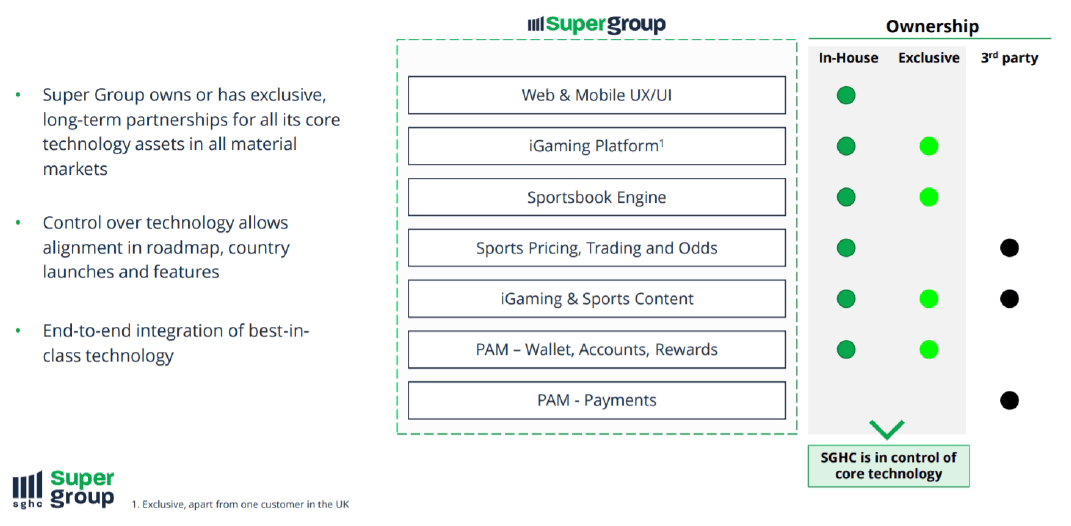

As the SGHC technology stack is developed by itself, I believe it will enable strong operating leverage as it scales. The way I see SGHC is similar to other software companies, only that it deals with consumer gambling. As such, designing and operating its own tech stack will allow it to reap the benefits of more efficient research and development dollars spent over the long term. SGHC will be able to roll out more products and updates easily without the need to re-integrate several parts of its tech stack.

{kind=link}

The question is then: what is SGHC's potential margin as it matures? If we compare SGHC to other global peers like Betsson and Entain PLC, both of them generate an adj. EBITDA margin of 20+% and have similar gross margins as SGHC. As such, I see potential for SGHC to further expand its margin.

Valuation

May Investing Ideas

SGHC share price has been weak recently after the 3Q23 results, which I believe was mainly due to the FX headwinds that impacted results. In my opinion, SGHC continues to showcase strong operating growth as revenue continued its streak of 10+% and monthly active users [MAU] growth accelerated from 37% in 2Q23 to 48% in 3Q23. However, FX had a substantial headwind of more than 10%, as reported revenue grew 9% but constant currency revenue grew 20%. Recognising that FX is going to continue to be a headwind, I believe growth will slow down sequentially in 4Q23 and meet management FY23 guidance. However, as we move into FY24, the FX tailwind should be less impactful given that the USD should see lesser upward strength if rates remain at this level (or move up at a more gradual pace). I expect growth to normalise towards industry growth of ~10% in FY25. As SGHC grows, I expect operating leverage to show up in the P&L and expect margins to be in line with peers at 20+%. With these assumptions, I would also expect SGHC EV/forward EBITDA to gradually recover back to its average of 7.4x. If SGHC performs as I expected, the valuation multiple should at least re-rate back to its -1 standard deviation of 5.3x.

Risk

I think an inherent risk with SGHC is that gambling is not a necessity at all. Without gambling, the world will go on just fine. As such, this is going to be the first spending budget consumers will cut during a steep recession, and SGHC will be greatly impacted.

Conclusion

I am giving a buy rating for SGHC. As Canada progresses towards legalizing online gambling, SGHC stands to benefit substantially. SGHC's dual-brand strategy, combining a single-brand focus with Betway and a multi-brand approach with Spin, strategically positions it to capture diverse market segments efficiently. I also like SGHC's data-driven approach which should increase operational efficiency and customer retention. Overtime, SGHC margin should expand to peers' level as it grows.

For further details see:

Super Group: Canada Is A Growth Catalyst