SGC - Superior Group: No Superior Returns Despite A 50% Tumble

2023-08-08 18:03:14 ET

Summary

- Superior Group of Companies, Inc. experienced strong sales growth during the COVID-19 pandemic, but has since faced challenges including ballooning debt and dwindling profits.

- Superior Group reported a decline in revenues and lowered its sales and earnings guidance, painting a gloomy picture for the company's profitability.

- We believe there are still significant downside risks which can further impact the company's business and squeeze earnings despite attractive valuation.

- We initiate at Neutral as we await any tangible improvement in the company's operational performance.

Investment Thesis

Superior Group of Companies, Inc. ( SGC ) is a leading provider of healthcare apparel (including uniforms, scrubs, lab coats, patient apparel and specialty products) as well as branded merchandise through its uniforms/ branded products. It also offers near shore contact services to small and medium businesses providing inbound and outbound contact services. It has demonstrated solid growth in sales, but the bottom line has been quite volatile over the years and has only worsened recently. It was one of the COVID darlings where in its share price jumped more than 170%+ in the 2 year period since the onset of the pandemic as healthcare goods were in high demand. However, with the end of COVID, fortunes reversed and SGC was left with much more to hold than it can sustain.

Ballooning debt, dwindling profits, cash flow generation that has stalled and inventory write-downs post COVID as management went too aggressive led to share price tumbling more than 50% in past 1 year. Despite it trading at 6x Fwd EV/ EBITDA, SGC risks remains high as it still struggles to turnaround its operations in the wake of challenging macro environment and rising costs. We initiate at Hold to see any visible traction in its operational performance.

Guidance Shocker

SGC reported a 13% decline in revenues on the back of continued weakness in the macro environment missing analyst expectations. Gross margins came in at 36.8%, growing 400 bps+ YoY as it lapped few one-time expenses last year as well as driven by favorable pricing mix in the branded apparel segment and increasing share of the high-margin Contact Center segment to the total revenue. SG&A deleverage by 150 bps YoY as a result of sticky fixed costs and employee-related expenses amidst a declining revenue. All in, EPS came in flat at $0.08 slightly below expectations. The balance sheet position improved relatively with Net Debt improving to $125 mn from $150 mn in the previous quarter, but still remains elevated in the wake of downward revision to the guidance.

It now expects sales of $560 mn at the midpoint for the year compared to its $590 mn guidance provided just three months back. Earnings guidance came in a huge shocker as SGC halved its annual guidance as it expects just $0.50 at midpoint compared to $0.95 previously painting a gloomy picture as the company looks to take a hit on profitability amidst a weakening macro backdrop while maintaining market share.

Valuation

SGC appears cheap on paper, however it is fraught with risks, compared to its peers which have a relatively higher margin and better growth profile. We believe the bottom may be around the corner this year as it laps favorable comparables going forward but would wait for any tangible improvement in its operational performance. We initiate with Neutral rating given visible downside risks.

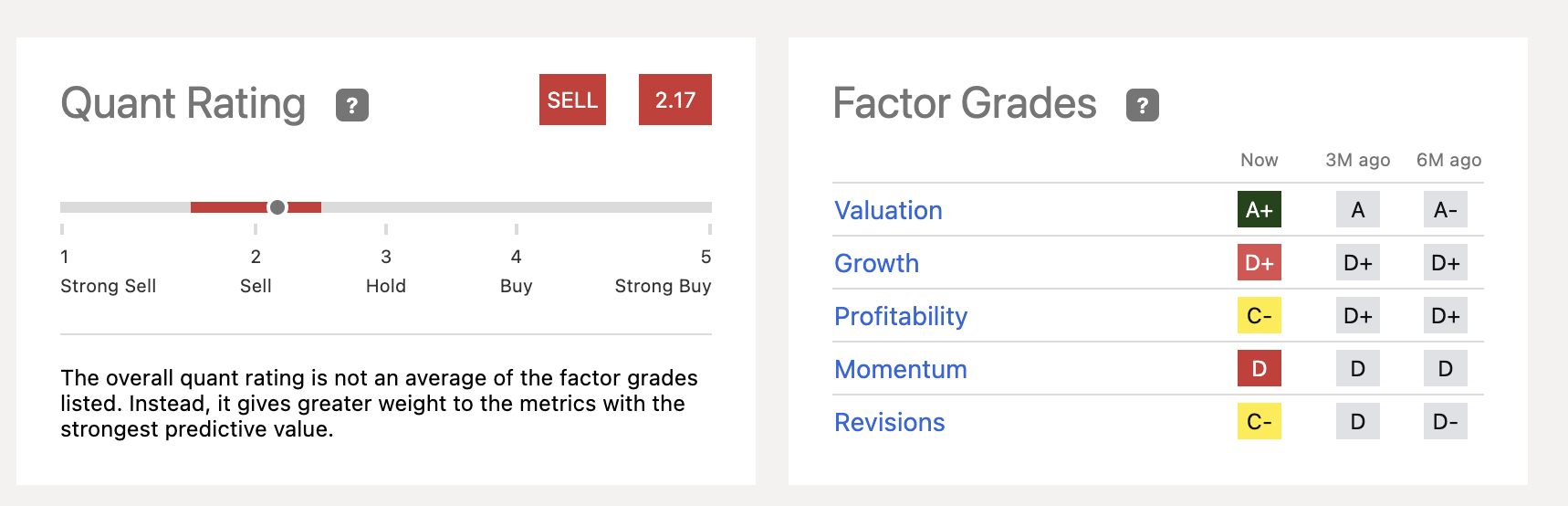

Seeking Alpha's Quant system assigns a strong sell rating to the company as a result of downward revisions, probable dividend cuts (which is soon going to materialize) and meek profitability. However, the valuation grade remains A+ which provides some encouragement to long term investors.

{kind=link}

Risks to Rating

Risks to rating include

1) any change in the macroeconomic environment would have a significant impact on SGC as it has a lower pricing power and any change in the pricing mix could significantly impact earnings

2) SGC operates in a tough space and competitive pressures from larger and well capitalized players within the BPO/ contact center segment as well as apparel segment could further squeeze margins as others go ballistic on maintaining/ growing share in the wake of uncertain macro environment

3) operations in healthcare industry is highly regulated and any changes or inability to maintain safety standards could have a huge damage to the business

Conclusion

SGC had a dream run during COVID which soon fizzled away leading them with significant debt and a truckload of wasteful inventory (which it did write off last year). We believe with the outlook revised downwards the dividend yield would soon be around the normalized 3% range, however, we expect the company to continue paying dividends as it did continue during the previous recessionary periods (during 2008 Financial crisis it maintained the dividend).

We believe Superior Group of Companies, Inc. valuation remains attractive. However, with significant earnings downgrades and a looming dividend cut, we believe there are still downside risks and the current print will likely to send shares spiraling down further. We remain Neutral.

For further details see:

Superior Group: No Superior Returns Despite A 50% Tumble