FIGS - Superior Group Of Companies: A Risky Way To Get Potentially Superior Returns

Summary

- Superior Group of Companies continues to see its sales increase at a nice pace, but this isn't the only thing investors should be paying attention to.

- Profits and cash flows have been difficult in recent quarters and the company has a long history of volatility.

- Given how cheap shares are, upside could be attractive, but it's not without its risks.

In many environments, whether it is a hospital, a hotel, an entertainment destination, etc., there can often be a need for specialized clothing. Although there are some large companies that play in this space, one of the smaller ones that investors should at least be aware of is Superior Group of Companies ( SGC ). Over the past few years, the company has demonstrated a robust ability to grow sales, even as profits and cash flows have been a bit volatile. By no means is this a high-quality firm. But given how shares are priced, it may not make for a bad prospect for value investors who don't mind taking a little risk.

Trying it on for size

At its core, Superior Group of Companies focuses on the production and sale of uniforms, corporate identity apparel, career apparel, and accessories, all for a wide variety of firms across multiple industries. Specific industries include the medical space, health care space, industrial space, commercial space, leisure, and even public safety markets. End customers include hospitals and other healthcare facilities, fast food and other restaurants, retail stores, industrial facilities, transportation companies, hotels, entertainment providers, public and private and security organizations, and more.

In addition to selling uniforms and service apparel to the aforementioned parties, the company also produces and sells other miscellaneous products. These include, but are not limited to, linen that's used for industrial laundry bags, goggles, isolation gowns, COVID-19 testing kits, sanitizers, gloves, and so much more. Through a separate segment, the company also produces branded marketing programs, corporate awards, specialty packaging and displays, etc. In addition to all of these products, the company also provides services centered around remote staffing solutions. But based on data from its 2021 fiscal year, this portion of the enterprise is fairly small, accounting for only 11% of sales. By comparison, the uniforms and service apparel operations accounted for 49% of sales, while the products sold under the promotional category accounted for 40%.

{kind=link}

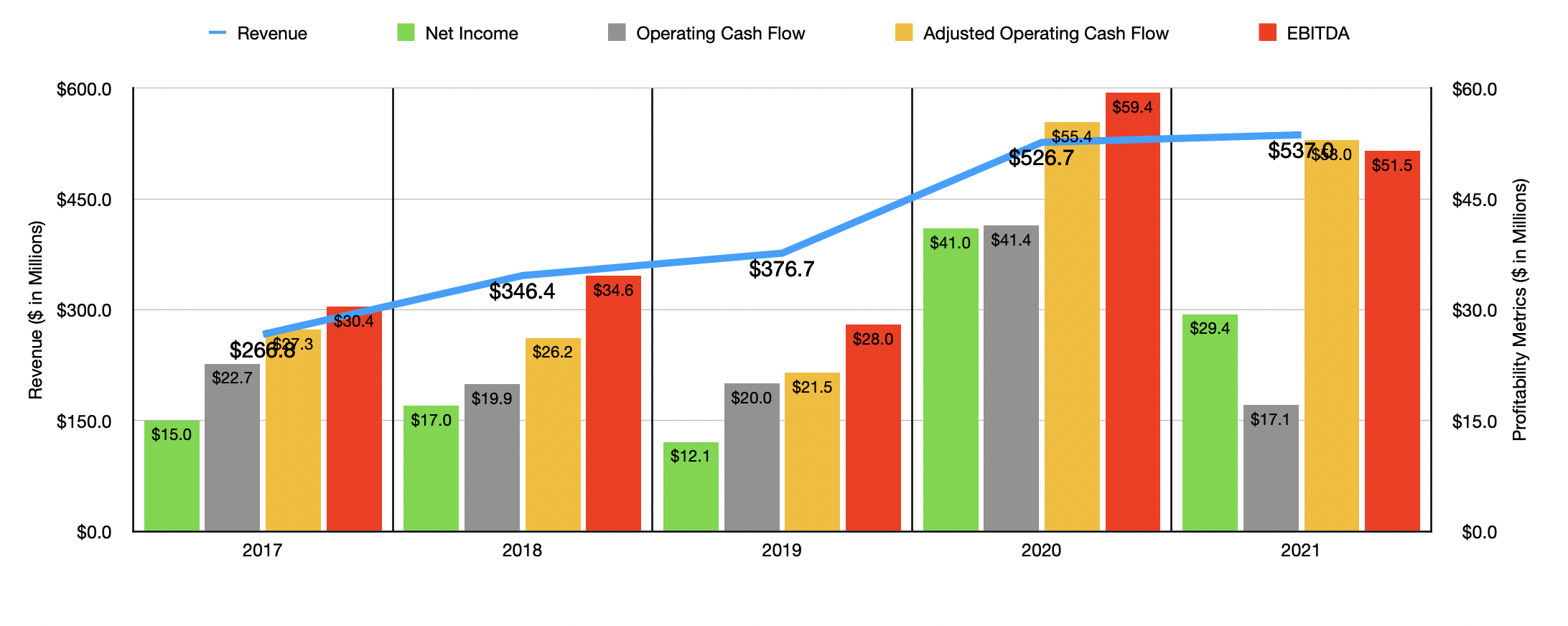

Over the past few years, the management team at Superior Group of Companies has done a good job growing the company's top line. In each year between 2017 and 2021, sales for the company increased, ultimately rising from $266.8 million to $537 million. From 2020 to 2022, sales growth was only about 2%. This was driven by a 51.8% surge in the company's Remote Staffing Solutions operations, with sales climbing from $42.4 million to $64.3 million. This makes sense when you consider how tight the labor market has been over the past year or so. The Uniforms and Related Products segment reported a sales decline of 8.1%. But this was somewhat offset by a 6.8% increase under the Promotional Products category of sales. In addition to benefiting from organic growth on this front, the company also benefited to the tune of $16.9 million from acquisitions that it had made over that time.

The revenue trajectory for the company has been clear. But profitability has been a bit more volatile. Between 2017 and 2019, net income bounced around between $12.1 million and $17 million. In 2020, profits surged to $41 million before pulling back to $29.4 million in 2021. Operating cash flow has shown similar volatility. After peaking at $41.4 million in 2020, it plunged to $17.1 million one year later. If we adjust for changes in working capital, that metric actually would have fallen between 2017 and 2019 before skyrocketing to $55.4 million in 2020. In 2021, it also pulled back, dipping to $53 million. A similar trend can be seen when looking at EBITDA, with the metric ultimately hitting a high of $59.4 million in 2020 before coming in lower at $51.5 million in 2021.

{kind=link}

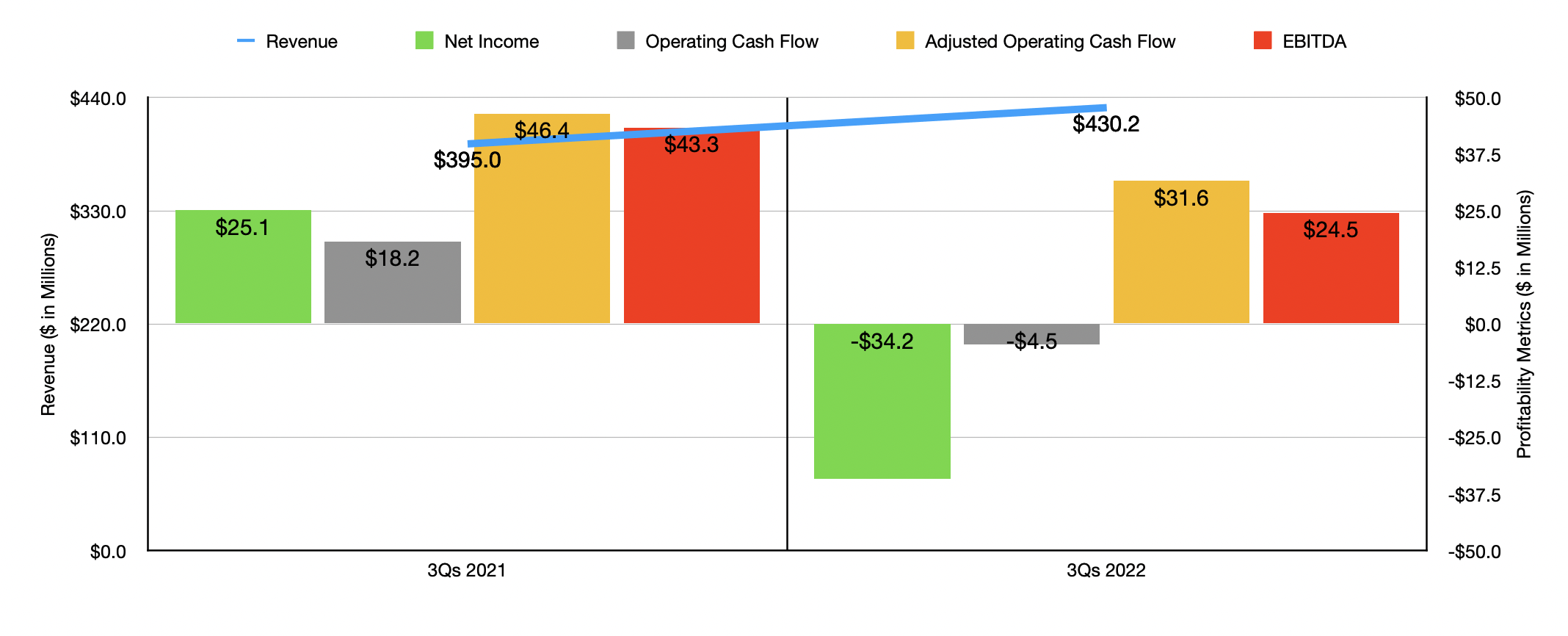

The 2022 fiscal year marked another time of volatility for the company. But before we get into that data, it's worth mentioning that management did make a change to the operating segments that it runs during this time. Starting in the second quarter of 2022, the company realigned these segments, combining its uniform business with its Promotional Products segment to form the Branded Products segment, making the healthcare apparel business its own segment called Healthcare Apparel, and renaming the Remote Staffing Solutions operations as the Contact Centers segment. During the first nine months of the company's 2022 fiscal year, the Contact Centers segment reported revenue growth of 34.4%, while the Branded Products segment grew a more modest but still impressive 16.9%. The real weakness came to the Healthcare Apparel segment, which reported a 20.1% plunge in revenue because of a decrease in demand for healthcare apparel resulting from market conditions that caused saturation in this space thanks to COVID.

On the bottom line, the company experienced some pain. Net income went from $25.1 million to negative $34.2 million. Part of this pain was the result of the company's gross profit margin shrinking from 36% down to 34.5%. Management attributed this largely to inventory write-downs associated with personal protective equipment and discontinued styles. Selling, general, and administrative costs also rose from 26.4% of revenue to 30.7%. According to management, this was largely the result of expense deleveraging because of the decline in Healthcare Apparel sales, as well as an increase in employee costs because of higher headcount aimed at supporting its other two operating segments. Other profitability metrics followed suit. Operating cash flow went from $18.2 million to negative $4.5 million. Even if we adjust for changes in working capital, it would have fallen from $46.4 million to $31.6 million. And over that same window of time, EBITDA for the company dropped from $43.3 million to $24.5 million.

{kind=link}

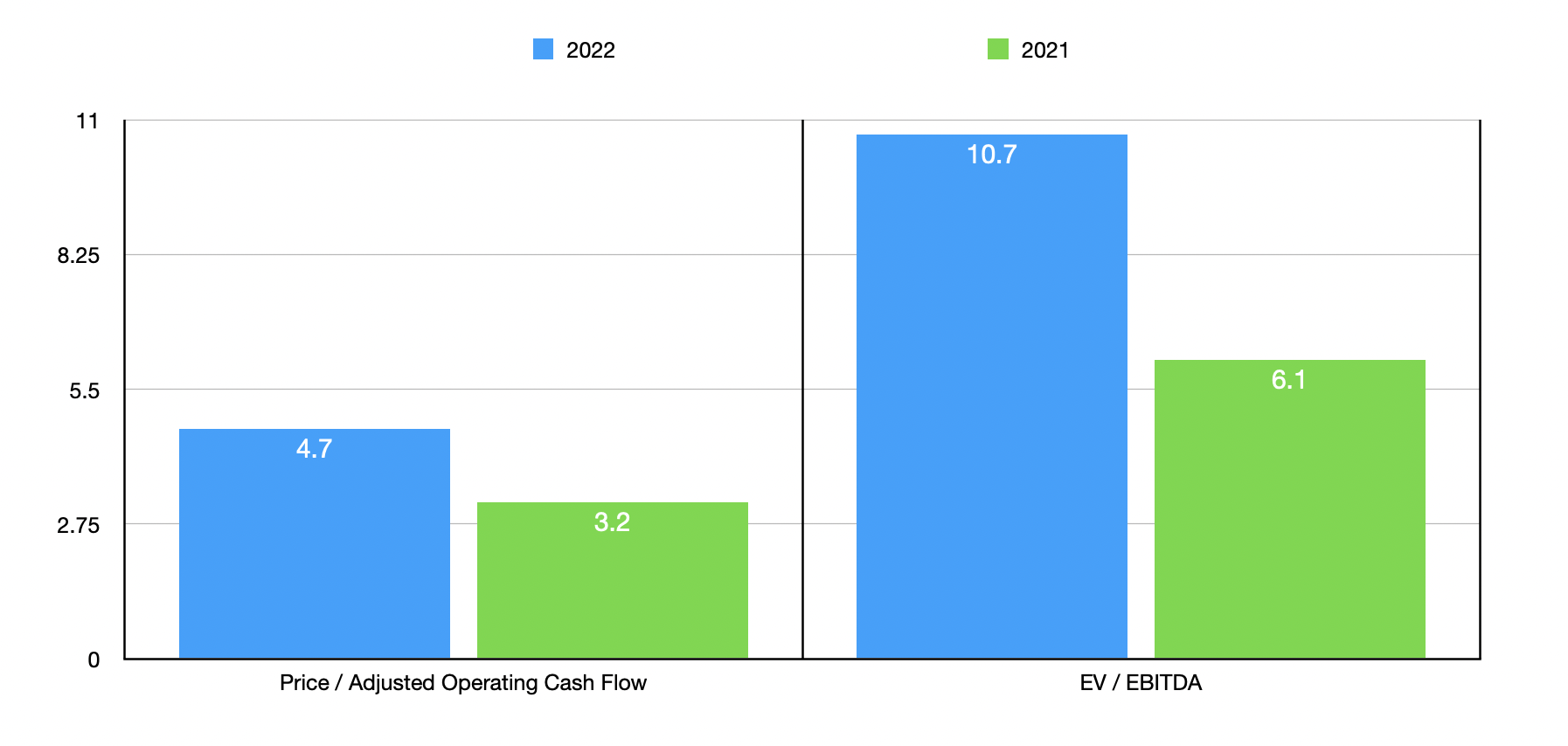

Sadly, the only guidance management gave for 2022 involved revenue. Overall sales should come in at between $570 million and $580 million. That would represent a nice increase over the results achieved in 2021. As for bottom line results, annualizing data seen so far would indicate adjusted operating cash flow of $36.1 million and EBITDA of $29.1 million. Based on these numbers, the company is trading at a forward price to adjusted operating cash flow multiple of 4.7 and at a forward EV to EBITDA multiple of 10.7. By comparison, if we were to use the data from 2021, these numbers would be 3.2 and 6.1, respectively. As I do with other companies when I write about them, I decided to compare Superior Group of Companies to five similar enterprises. On a price to operating cash flow basis, these companies ranged from a low of 16.4 to a high of 230.9. In this case, Superior Group of Companies was the cheapest of the group. And when it comes to the EV to EBITDA approach, the range was from 7.9 to 22.3. In this case, only one of the five companies was cheaper than our target.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Superior Group of Companies |

| 4.7 |

| 10.7 |

| Lakeland Industries ( LAKE ) |

| 20.1 |

| 7.9 |

| FIGS ( FIGS ) |

| 230.9 |

| 21.3 |

| Aramark ( ARMK ) |

| 16.4 |

| 15.5 |

| Cintas Corp. ( CTAS ) |

| 29.5 |

| 22.3 |

| UniFirst Corporation ( UNF ) |

| 26.6 |

| 14.0 |

Takeaway

All things considered, Superior Group of Companies is not exactly a bad prospect. The company lacks the kind of stability that I would like to see, particularly when it comes to bottom line results. In addition, it's clear that fundamentals are currently worsening because of increased costs and weakness in some product categories. At the same time, however, shares do look quite cheap on an absolute basis and they are cheap compared to similar firms. My overall assessment is that this is far from a riskless play. But for investors who want a smaller firm in the uniform space and who don't mind volatility from quarter to quarter or from year to year, the low price being accepted by the market could make this a decent play in the long run. Given the totality of the circumstances, the firm does not quite measure up to what I look for in an opportunity, so I have opted to rate it a 'hold'.

For further details see:

Superior Group Of Companies: A Risky Way To Get Potentially Superior Returns