SGC - Superior Group Of Companies: Rising Interest Expenses Represent A Serious Problem But High Inventories Should Allow Some Deleverage

2023-05-08 11:41:34 ET

Summary

- Net sales steadily increased over the years thanks to continuous acquisitions, but an indebted balance sheet will slow down growth rates.

- Interest expenses skyrocketed during the third and fourth quarters of 2022 as a consequence of higher rates and debt.

- The dividend will likely be temporarily cut (or even canceled) until the balance sheet gets some deleverage as profit margins are depressed.

- High inventories should allow for some deleveraging in the medium term, but short-term weakening demand might pose a problem.

- This is a high risk/high reward turnaround play worth investing.

Investment thesis

Superior Group of Companies ( SGC ) is one of those companies that, despite operating in essential sectors of the economy and presenting a growing dividend, should be bought at the right time to obtain a good dividend yield on cost (and sell when optimism is extremely high) as its operations have been subject to high volatility over the years. Over 2 million essential caregivers wear the company's brands every day, which represents a significant customer base, but the company is currently facing a series of headwinds that are jeopardizing its operations.

Increased production, labor, and transportation costs, as well as inventory write-downs, are sending profit margins to the ground. Furthermore, an increased debt pile and increasing interest rates caused a significant rise in interest expenses, which is making the current dividend payout unsustainable. Despite this, the company has inventories that are close to the total long-term debt, which significantly reduces the risk that the debt entails for the company in the long term as these inventories could be converted into cash to pay it down. Still, weakening demand is putting the possibility of emptying inventories at risk as it would likely lead to unabsorbed labor if not done carefully.

A brief overview of the company

Superior Group of Companies is a manufacturer of apparel and accessories in the United States and internationally. The company was founded in 1922 and its market cap currently stands at $125 million, employing over 6,000 workers worldwide. Insiders own 14.09% of the company's outstanding shares, which means they are beneficiaries of the good performance of the share price.

Superior Group of Companies logo (Superiorgroupofcompanies.com)

The company operates under three main business segments: Branded Products, Healthcare Apparel, and Contact Centers. Under the Branded Products segment, which provided 67% of the company's total net sales in 2022, the company produces and sells customized merchandising solutions, promotional products, and branded uniform programs for a wide range of industries, including retail, hotel, food service, entertainment, technology, transportation, and other industries. Under the Healthcare Apparel segment, which provided 20% of the company's total net sales in 2022, the company manufactures and sells a wide range of healthcare apparel, such as scrubs, lab coats, protective apparel, and patient gowns to healthcare laundries, dealers, distributors, and physical and e-commerce retailers primarily in the United States. And the Contact Centers segment, which provided 15% of the company's total net sales in 2022, provides outsourced, nearshore business process outsourcing, contact, and call-center support services to North American customers.

Currently, shares are trading at $7.60, which represents a 74.09% decline from all-time highs of $29.33 in March 2021. A share price decline as significant (and sudden) as this is usually accompanied by very significant risks of permanent damage to the balance sheet or even bankruptcy, so in this article I am going to break down the different aspects that have led to such a significant pessimism among investors.

First of all, it is very important to review the acquisitions that the company has carried out in recent years to understand where its debt comes from since an aggressive M&A strategy is the main reason for the company's current debt burden.

Recent acquisitions

The company acquired HPI Direct in 2013, a designer, manufacturer, and distributor of uniforms to major domestic retailers, foodservice chains, transportation, and other service industries throughout the United States. Later, in 2016, the company acquired BAMKO, a full-service merchandise sourcing and promotional products company with subsidiaries in Hong Kong, China, Brazil, England, and an affiliate in India.

The acquisition spree continued in 2017 as the company acquired PublicIdentity, a promotional products and branded merchandise agency that provides promotional products and branded merchandise to corporate clients and universities, and later, in 2018, it also acquired CID Resources, a manufacturer of medical uniforms, lab coats, and layers sold through specialty uniform retailers, e-commerce medical uniform retailers, and other retailers.

After some deleverage, in January 2021, the company acquired Gifts By Design, a promotional products and branded merchandise agency that develops and supplies corporate awards, incentives, and recognition programs for some of the world’s biggest brands. Later, in December 2021, the company also acquired Sutter’s Mill Specialties, a vertically integrated manufacturer of high-quality, decorated promotional products. And the most recent acquisition took place in May 2022 when the company announced the acquisition of Guardian Products, one of the leading providers of promotional products to automotive dealers nationwide.

All these acquisitions have boosted meteoric growth in sales for the company while maintaining very healthy margins (except in recent quarters due to current headwinds), which is highly commendable and amplifies potential shareholder returns if the company manages to withstand inflationary pressures and weakening demand until these headwinds fade.

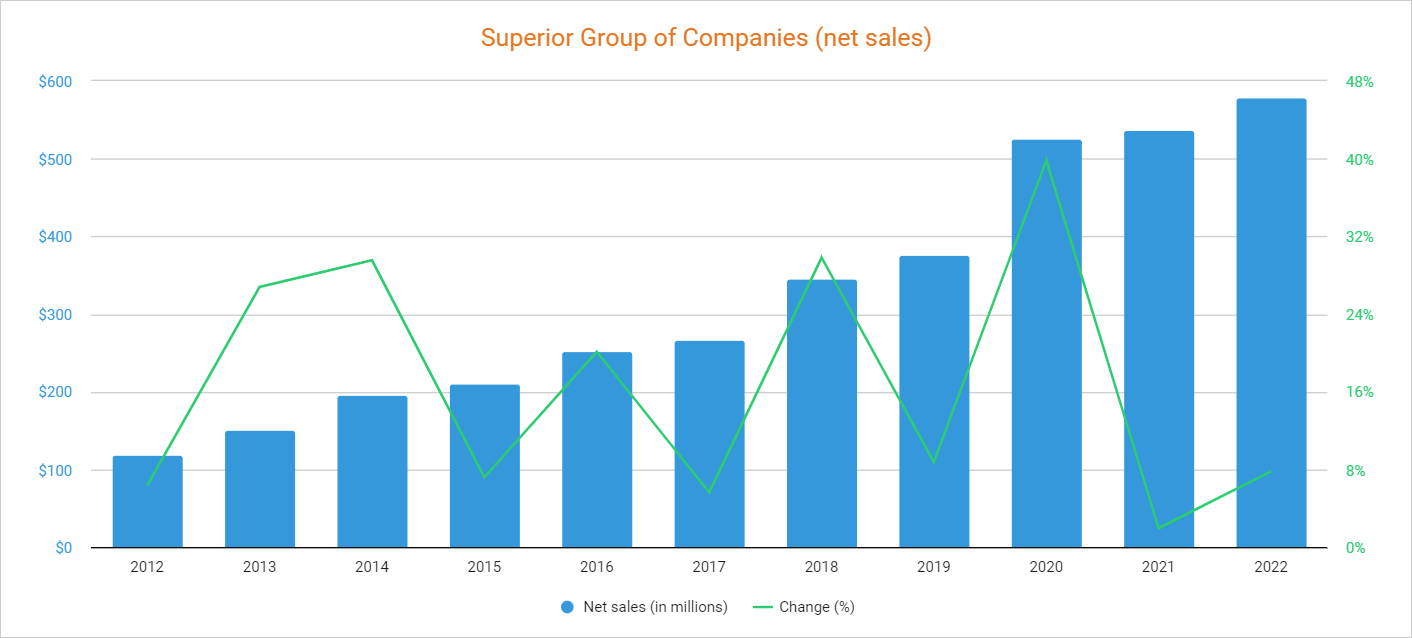

Net sales boomed boosted by acquisitions

The company's sales have increased at a dizzying pace over the past 10 years, thanks to acquisitions, from $119 million in 2012 to $579 million in 2022. This fact, added to very stable profit margins over the years suggests that the acquisition strategy was indeed successful.

{kind=link}

As of more recently, net sales increased by 1.94% year over year in the first quarter of 2022, by 13.11% in the second quarter, 12.47% in the third quarter, and by a softer 4.64% in the fourth quarter as net sales for the Healthcare Apparel segment declined to $26 million (from $31 million during the same quarter of 2021) because of ongoing soft conditions of the broader healthcare market. Still, net sales increased by 7% in the Branded Products segment, and by a whopping 22% in the Contact Center segment (which is indeed a very profitable segment), which means the growing trend continues by now. The management plans to launch a direct-to-consumer channel for the Healthcare Apparel segment in the foreseeable future in order to increase its customer base and offset declining demand. In this regard, net sales are expected to increase by 2.99% in 2023 to $596 million, and by a further 8.21% in 2024 to $645 million.

The continued increase in sales coupled with the recent precipitous decline in the share price has caused a steep decline in the P/S ratio to 0.209, which means the company currently generates net sales of $4.78 for each dollar held in shares by investors, annually.

This ratio is 75.30% below the average of the past decade and represents an 87.15% decline from the peak of 1.627 reached during the second half of 2017. Historically, the company has had quite high gross profit and EBITDA margins, so a P/S ratio of 0.209 is extremely low. In this sense, investors are currently valuing the company's sales much lower than in the past due to two main reasons: a recent contraction in profit margins as a consequence of inventory write-downs and increased production and labor costs, and a worrying increase in the company's interest expenses as a consequence not only of increased debt but also rising interest rates.

Profit margins remain depressed but are showing early signs of improvement

Currently, trailing twelve months' gross profit and EBITDA margins stand at abnormally low levels of 33.41% and -3.48%, respectively, due to inventory write-downs, increased employee costs, higher production and logistic costs, and increased SG&A expenses.

Still, the EBITDA margin improved to 4.64% during the fourth quarter of 2022 as the company reported an EBITDA of $11 million vs. $6 million during the same quarter of 2021. Nevertheless, the gross profit margin declined to 30.15% during the quarter due to a $6 million incremental inventory write-down in the Healthcare Apparel segment. Nevertheless, positive EBITDA margins allowed for a net income of $2.2 million for the quarter after three consecutive quarters of losses.

At this point, three main aspects should be highlighted regarding the current situation. First, the headwinds causing ongoing contraction in profit margins are, in my opinion, temporary due to their direct link to the current macroeconomic and industry context. Second, profit margins are still being impacted by these headwinds and, despite a significant improvement in the past quarter, are not enough to cover interest and capital expenses (and much less if we add the dividends) and are subject to a high risk of being depressed further as pricing actions have their limits before starting to affect demand. And third, the company's ability to generate enough cash from operations to pay down its debt pile is directly related to its ability to empty its inventories in a profitable way, which won't be easy as inflationary pressures are causing soft demand for the company's products.

The company has enough inventories to pay down a significant portion of its debt, and high interest expenses make it a must

As a consequence of the acquisitions carried out in recent years, the long-term debt has grown significantly to this day. During the last earnings call conference, the management stated that emptying current high inventories in order to deleverage the balance sheet is a top priority (which should actually be as debt represents a big risk for the company's sustainability due to increased interest expenses). In this regard, cash and equivalents, despite increasing to $17.72 million boosted by the sale of a corporate office building, is very low compared to long-term debt, so successfully emptying inventories is, in my opinion, the only way to pay down enough debt to make interest expenses a much softer risk for the long term.

As for inventories, they actually increased steadily over the years as the company has grown its business significantly. These inventories come in handy at a time as delicate as the present, because as we will see later, interest expenses have increased very significantly and have put dividends at serious risk.

This should allow a significant reduction in long-term debt, and thus interest expenses, which should give significant leeway to keep on with the acquisition spree in order to fund further growth in the years to come (once margins stabilize). Still, emptying such inventories won't be easy as it would likely lead to unabsorbed labor, and thus lower profit margins. For this reason, the company should carefully monitor its labor structure in order to temporarily decrease its production capacity and, in this way, empty a big portion of its inventories in a profitable way.

The dividend is at high risk as interest expenses outpaced it

The company has a long tradition of paying ever-growing dividends, and the latest raise took place in May 2022 when it announced a 16.67% increase to $0.14 per share. This makes the stock an optimal holding for dividend growth investors (in the long run).

If we add to the continuous rise in the dividend the current fall in the share price, the current dividend payout represents a yield of ~7.4%, which represents an enormous dividend yield on cost considering the cash payout ratio has been historically low. Despite this, the risks are enormous as the management should temporarily cut (or even cancel) the dividend in order to ensure the survival of the company in the short and medium term by offsetting the rise in interest expenses until deleveraging its balance sheet significantly. This is, then, the price dividend investors should pay for a very high dividend yield on cost in the long term: a short-term cut (or even cancellation).

In order to calculate the dividend sustainability over the years, in the next table I have calculated which percentage of the cash from operations has been allocated to the dividend and interest expenses over the years. In this way, one can assess the company's ability to cover both expenses through actual operations. Obviously, this should serve as a reference for the long term, but it is important to take into account that the outlook is currently very complicated due not only to increased interest expenses but also unusually low profit margins as a consequence of ongoing headwinds.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $6.84 |

| $9.91 |

| $11.99 |

| $22.73 |

| $19.86 |

| $20.01 |

| $41.36 |

| $17.09 |

| -$2.60 |

| Dividends paid (in millions) |

| $3.66 |

| $4.26 |

| $4.71 |

| $5.27 |

| $5.84 |

| $6.05 |

| $6.11 |

| $7.24 |

| $8.65 |

| Interest expenses (in millions) |

| $0.48 |

| $0.52 |

| $0.69 |

| $0.80 |

| $3.21 |

| $4.40 |

| $2.00 |

| $1.22 |

| $4.89 |

| Cash payout ratio |

| 60.65% |

| 48.16% |

| 45.00% |

| 26.71% |

| 45.47% |

| 52.21% |

| 19.62% |

| 49.51% |

| - |

As you can see in the table above, the management has historically been very conservative when it comes to cash allocation as the cash payout ratio has remained at very low levels over the years. Nevertheless, cash from operations was negative in 2022 at -$2.60 million, and interest expenses increased to $4.89 million. Worryingly, interest expenses increased to $2.2 million during the fourth quarter of 2022 (from $0.30 million during the same quarter of 2021) due to significantly higher interest rates and higher outstanding debt, so the annual interest expenses will likely rise in 2023 to ~$9 million.

Still, cash from operations showed a significant improvement during the fourth quarter as the company reported cash from operations of $1.9 million, and despite inventories declining by $10.9 million, accounts receivable increased by $6.4 million while accounts payable declined by $2.8 million. The problem is that these figures are hardly enough to cover interest expenses (and much less the dividend) and that the company also needs to fund around $11 million in capital expenditures per year (although the management expects to reduce it by around 30% in 2023). This is the reason the company urgently needs to make use of its inventories in order to deleverage the balance sheet and thus reduce interest expenses until profit margins stabilize at more acceptable levels.

Risks worth mentioning

As a summary of the risks that I have been mentioning throughout the article:

- In my opinion, the main risk investors should consider is related to interest expenses, which are at almost $9 million per year (using fourth-quarter interest expenses as a reference) after a significant increase due to rising interest rates and outstanding debt. With such high interest expenses, and taking into account the cash from operations of the past year, the company could have serious problems meeting its payment while paying down its debt pile with its operations themselves. Luckily, inventories are highly inflated at $124.98 million, with which the company should be able to pay off a significant portion of its long-term debt of $155.32 million. Cash and equivalents are also unusually high at $17.72 million, which will provide the company with some room for maneuvering in the short term, but further inventory write-downs remain a risk.

- Given the increase in interest expenses and the low profit margins as a result of macroeconomic headwinds, it is most likely, in my opinion, that the management will decide to cut (or even completely cancel) the dividend until the macroeconomic context offers more positive prospects for the company's outlook. In this sense, said movement would be very intelligent since it would be possible to use the cash that would have been used to cover the dividend to pay interest expenses and, in this way, be able to pay the debt with inventories.

- In this regard, one risk that is very likely to materialize is that the dividend will be cut or even canceled, and once done, it will stay that way until the current headwinds disappear (or are greatly reduced). Still, the dividend should not take long to be reestablished once the company returns to profitability as insiders have big positions in the company's shares.

- The company could have trouble emptying its inventories as demand is weakening due to ongoing inflationary pressures affecting the purchasing power of consumers and caregivers.

- Another risk I would like to highlight is share dilution. In this regard, the number of shares outstanding increased by 34.51% during the past 10 years, which means each share now represents a significantly smaller size of the company.

This happened despite efforts to reduce the number of shares outstanding as the board of directors approved a share repurchase program of up to 750,000 shares in May 2019.

Conclusion

The situation of Superior Group of Companies is very delicate at the moment, and this is why the share price has suffered such a sharp drop. Profit margins have been hit hard by increased production, labor, and transportation costs, while interest expenses have skyrocketed by rising interest rates.

Whichever way you look at it, it is a high-risk/high-reward turnaround play with no guarantees of success, but there are two things that tip the balance, in my opinion, toward a potentially successful turnaround. First, the company's inventories are very high and cash and equivalents are higher than usual (despite being low in relation to long-term debt). And second, ongoing headwinds impacting profit margins are, in my opinion, of a temporary nature due to their direct link to the macroeconomic context.

The company's P/S ratio is extremely low compared to the past, which means investors' pessimism is very low due to ongoing challenges, and this has pushed the dividend yield on cost to very high levels. While it is true that the dividend will most likely be reduced or canceled in the short term, this represents, in my opinion, a huge opportunity for dividend growth investors with a high appetite for risk and a high dose of patience.

For further details see:

Superior Group Of Companies: Rising Interest Expenses Represent A Serious Problem, But High Inventories Should Allow Some Deleverage