LCII - Superior Industries International: 3 Reasons To Be Optimistic

2023-03-07 11:15:27 ET

Summary

- Superior Industries International has seen a meteoric rise in recent months, with multiple contributors to its upside.

- Fundamentally, the company looks to be doing quite well and management seems to expect that to continue.

- Add on top of this how cheap shares are and the prospect of a buyout, and upside still exists moving forward.

One of the downsides of having a hyper-concentrated portfolio is that you can view a company in a bullish light, turn out to be correct about it, but still miss out on the upside because you didn't buy the stock in question. One really good example of this taking place with my own portfolio involves Superior Industries International ( SUP ), an enterprise that's dedicated to the production and sale of aluminum wheels that are used for vehicles in North America and throughout parts of Europe. Between strong fundamental performance and the very real prospect of a buyout, shares of the company have roared higher in recent months. Even with this movement, I do believe that some additional upside for investors could be on the table. Because of this, I've decided to keep the ‘buy’ rating I had on the stock, even though I acknowledge that the easy money has been made.

Fantastic upside

The last article that I wrote about Superior Industries International was published on December 19th of 2022. In that article, I talked about how well the company had done compared to the broader market over the prior few months. Attractive financial performance on both its top and bottom lines, combined with an offer that was made by another firm to acquire the entire business, was instrumental in pushing the stock significantly higher. Even after that move, however, shares of the company looked cheap enough to warrant additional upside still. Because of that, I kept the business rated a ‘buy’ to reflect my view that shares should generate upside that exceeds what the broader market should moving forward. Since then, the company has not disappointed. While the S&P 500 is up 6%, shares of Superior Industries International have seen upside of 60.9%. For context, since I first rated the company a ‘buy’ back in April of last year, shares have seen upside of 94.3% compared to the 7.7% drop the S&P 500 reported.

{kind=link}

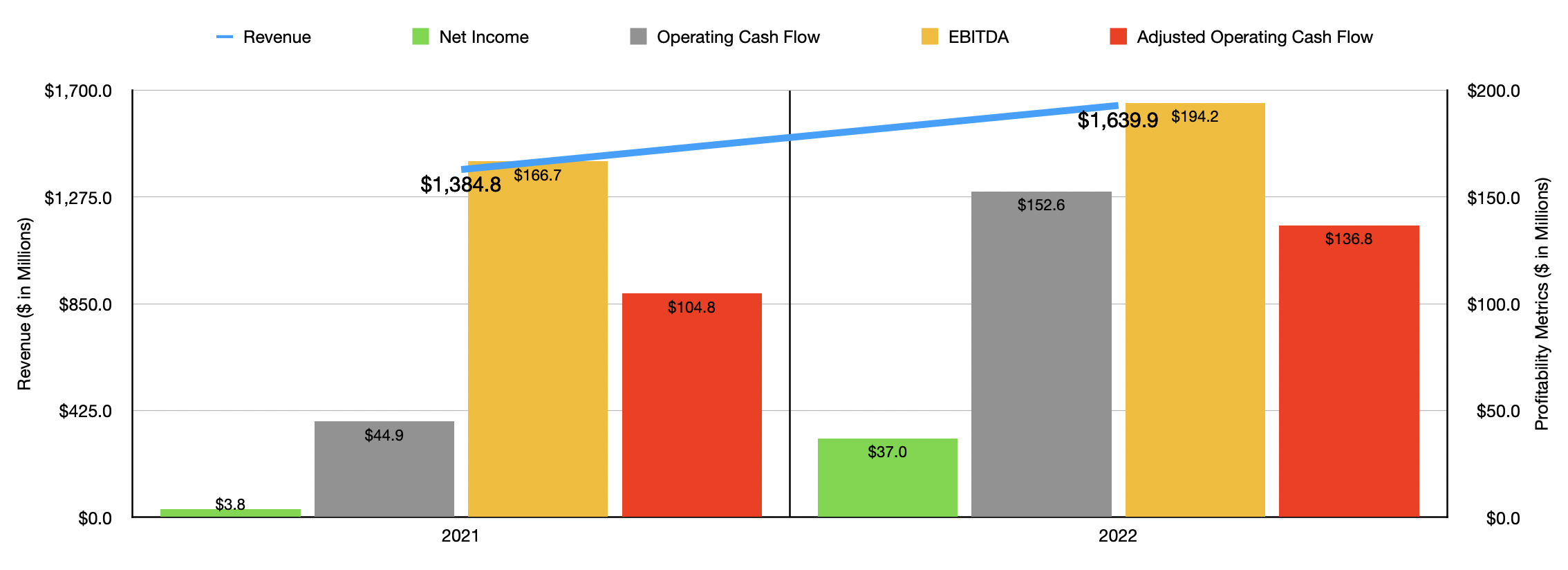

This astronomical return disparity can rarely be chalked up to three things. The first involves the fact that fundamental performance achieved by management has been quite impressive. Consider how the business performed during the final quarter of its 2022 fiscal year. During that time, revenue came in at $402.1 million. That's 9.2% higher than the $368.3 million reported only one year earlier. Value-added sales, which focuses more on the value that the company provides its customers, expanded by 15.5% during this window of time. Interestingly, the sales generated by the company increased even while the number of units that it produced and shipped globally decreased, falling from 3,930 in the final quarter of the 2021 fiscal year to 3,727 in the final quarter of 2022. Management attributed the increase in revenue, then, to the firm's ability to pass through inflationary pressures onto its customers. What this really means is that the firm was successful in pushing more than the cost increase it experienced onto its customers.

{kind=link}

This drastic improvement in pricing was instrumental in pushing the company's bottom line up as well. The firm went from generating a net loss of $3.9 million in the final quarter of 2021 to generating a profit of $16.5 million in the final quarter of 2022. Operating cash flow, meanwhile, expanded from $59.5 million to $78.1 million. If we adjust for changes in working capital, it would have grown from $26.6 million to $35 million. And finally, EBITDA for the firm grew from $37.4 million to $57.5 million.

The results experienced during the final quarter of 2022 were not a one-time event. For 2022 as a whole, revenue for the company totaled $1.64 billion. That's a sizable increase over the $1.38 billion reported only one year earlier. It is worth mentioning that most of this sales increase related to the higher costs the company was able to pass on to its customers. Value-added sales grew more modestly from $753.7 million to $770.6 million. Even with this though, profits for the company shot up from $3.8 million in 2021 to $37 million in 2022. Other profitability metrics followed the same trajectory. Operating cash flow, for instance, grew from $44.9 million to $152.6 million. On an adjusted basis, it expanded from $104.8 million to $136.8 million. And finally, EBITDA for the company expanded from $166.7 million to $194.2 million.

Related to the fundamental performance that management reported is also the fact that the firm is forecasting continued sales growth, or at least a possibility of it, for 2023. Overall revenue should be between $1.55 billion and $1.67 billion. At the midpoint, that would translate to a sales decrease compared to what was seen in 2022. But near the higher end of the scale would get us to an increase. Value-added sales, meanwhile, should range between $755 million and $815 million. At the midpoint, that would translate to a year-over-year increase of 1.9%. Unfortunately, management did not provide any guidance when it comes to profits or cash flows.

{kind=link}

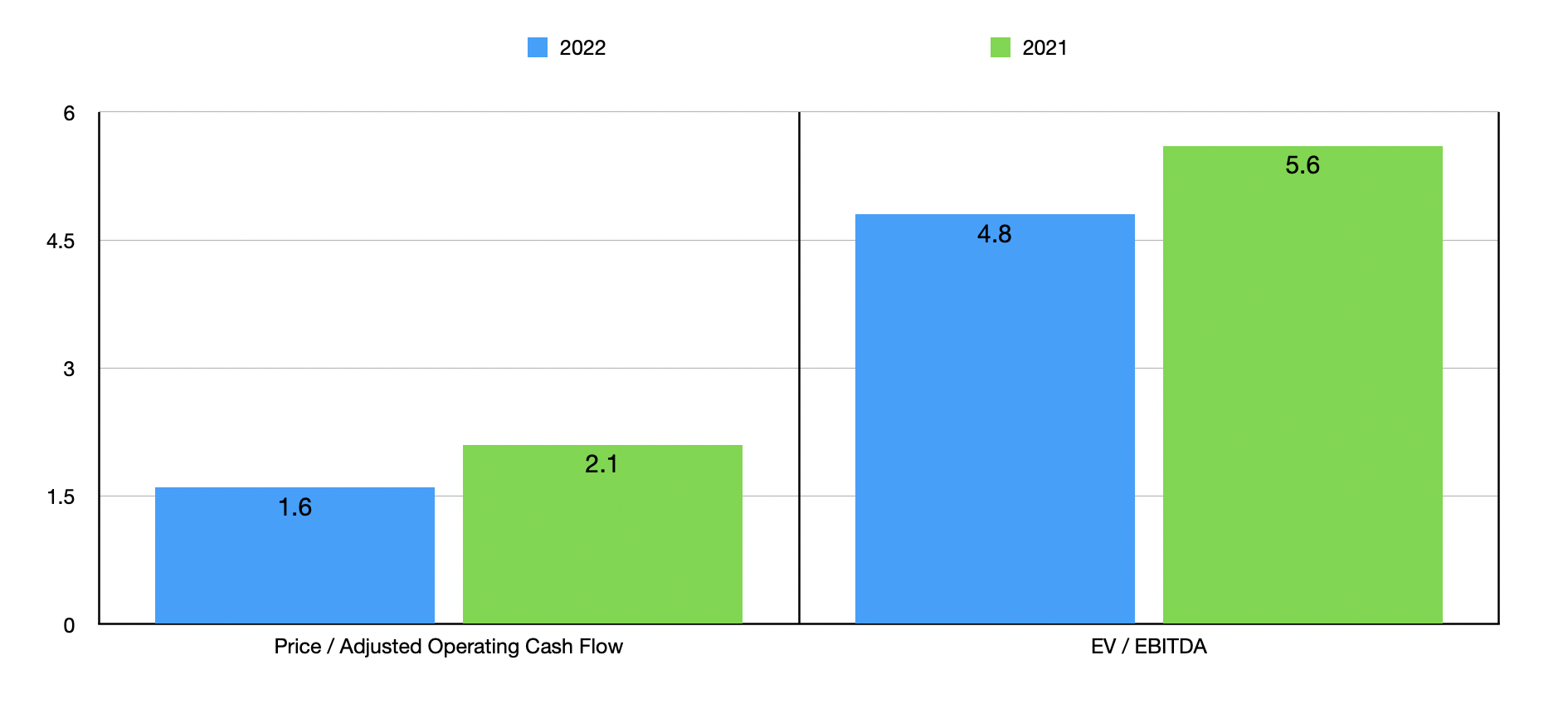

The second reason why shares are up so much relates to the fact that the stock is incredibly cheap. Even after seeing the share price rise significantly, the firm is trading at a price to adjusted operating cash flow multiple of 1.6. That's down from the 2.1 reading that we get using data from 2021. Preferred distributions do not come from operating cash flow and even though the preferred distributions the company is responsible for are being paid in-kind right now, I do see them as an eventual required cash outflow. So this valuation data that you see is after subtracting annualized preferred distributions from the company's cash flow data. SUP stock would be even cheaper if we followed the more traditional route of valuing it. Of course, in addition to preferred stock, the company also has a good deal of debt on its books. This makes the EV to EBITDA approach to valuing the company perhaps more important. On this basis, the company is trading at a multiple of 4.8. That's down from the 5.6 reading that we get using data from the year before. As part of my analysis, I also compared the company to five similar firms. As you can see in the chart below, it is cheaper than all of them, irrespective of which of the two metrics we rely on.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Superior Industries International |

| 1.6 |

| 4.8 |

| Standard Motor Products ( SMP ) |

| 11.6 |

| 7.9 |

| Motorcar Parts of America ( MPAA ) |

| N/A |

| 14.3 |

| LCI Industries ( LCII ) |

| 4.7 |

| 5.8 |

| Visteon Corp ( VC ) |

| 28.2 |

| 15.4 |

| Dorman Products ( DORM ) |

| 64.3 |

| 16.3 |

The third reason why shares of the company seem to be rising so much relates to the fact that there are rumors swirling about a potential acquisition. On the one hand, last year, we had M2 Capital Partners announce that they were intending to issue a tender offer to buy the entire business for $5.85 per share. That would assign the company an equity value of $160 million. We have yet to see that come into play and the stock has since risen to $7.21. Management also recently said that they have not had any discussions with the suitor. Even so, the allure of this is definitely appealing. On the other hand, we also have the fact that a large shareholder of the company, Mill Road Capital Management, continues to add to its stake in the enterprise. As of its filing on August 15th of last year, the business owned 3.66 million shares of Superior Industries International. Today, the number stands even higher at 4.07 million. That works out to just over 15% of the firm's outstanding stock. Whether they are looking to make an offer or whether they just hope to benefit from an offer being made by some other party, is something that we have yet to find out. But to see a major shareholder continue to allocate funds toward a company that has only risen is bullish.

Takeaway

It may seem peculiar for me to remain bullish about a company that has already appreciated so much in less than a year. However, the fundamental health of Superior Industries International continues to improve and shares are trading at incredibly low levels. The company does have a lot of debt and it has preferred stock to worry about. That does create some risk for investors. However, the potential of a buyout is definitely appealing, especially when you consider how cheap shares still remain. All of this combined makes me optimistic about the firm's prospects moving forward. Because of this, I've decided to keep the ‘buy’ rating on the company. But I do this with the understanding that additional upside from here is unlikely to be anywhere near what it has been over the past several months.

For further details see:

Superior Industries International: 3 Reasons To Be Optimistic