SUP - Superior Industries: Mill Road Keeps Buying Should You?

2023-08-23 08:54:49 ET

Summary

- Superior Industries is an OEM that produces aluminum wheels for vehicles in North America and Europe.

- The company's balance sheet is complex, but Superior is set to generate meaningful cash flow in FY23 to reduce leverage.

- Superior should benefit from simplification of their balance sheet and recovering US light vehicle production, and appears significantly undervalued.

Superior Industries (SUP) is an Original Equipment Manufacturer ("OEM") producing aluminum wheels for vehicles in North America and Europe. The company's balance sheet is complex, and the business has suffered from leverage issues as well as low auto production levels since Covid. Common shares traded down from over $30/share in 2016 to $3.50/share today. The business is currently priced at 4.8x EV/EBITDA and is set to generate meaningful cash flow in FY23. Superior should benefit from future deleveraging and a simplification of their balance sheet, with prospects of significant appreciation on today's share price. Mill Road Capital appears to agree , and has been buying shares in the open market .

Background

Superior was founded in 1957 but their leverage problem is new. From 2002-2016, Superior had no net debt, but they levered up in 2017 to gain European exposure through the acquisition of Superior Industries Announces Transformative Acquisition of Germany-based UNIWHEELS AG . Revenues and EBITDA roughly doubled due to this acquisition, but the story grew more complicated thanks in part to the redeemable preferred stock issued to TPG. Superior is now working to clean up their balance sheet before maturities of the debt and convertible preferred stock in 2025.

Superior Real Estate (Superior Investor Presentation)

Most production takes place in Mexico and Poland, with limited operations in Germany. Superior believes their footprint is well-situated to take advantage of re-shoring tailwinds . They own their manufacturing locations and should be able to tap these for liquidity via sale-leasebacks if traditional financing becomes too expensive for their business. If land and buildings were sold near their book cost of $150m, and leased back at 8-10% annually, Superior would retain more flexibility to deal with maturities. Based on commentary on their Q2 call , some rationalization in Europe is likely incoming:

Last quarter, we discussed our 80/20 approach where we are further assessing our current book of business to strategically prune parts that are underperforming. We have done this in North America in our North America business and are shifting focus now more holistically to our European operations.

...

If you look at Europe and the complexity we have there, it's much more complex than our North America business. The technology is complex. The competitive landscape is different. So our focus really now, Gary, just bumping up that margin 400 basis points and if you go through the numbers, frankly, you'll see more opportunity. So our objective is to get as close to that as possible.

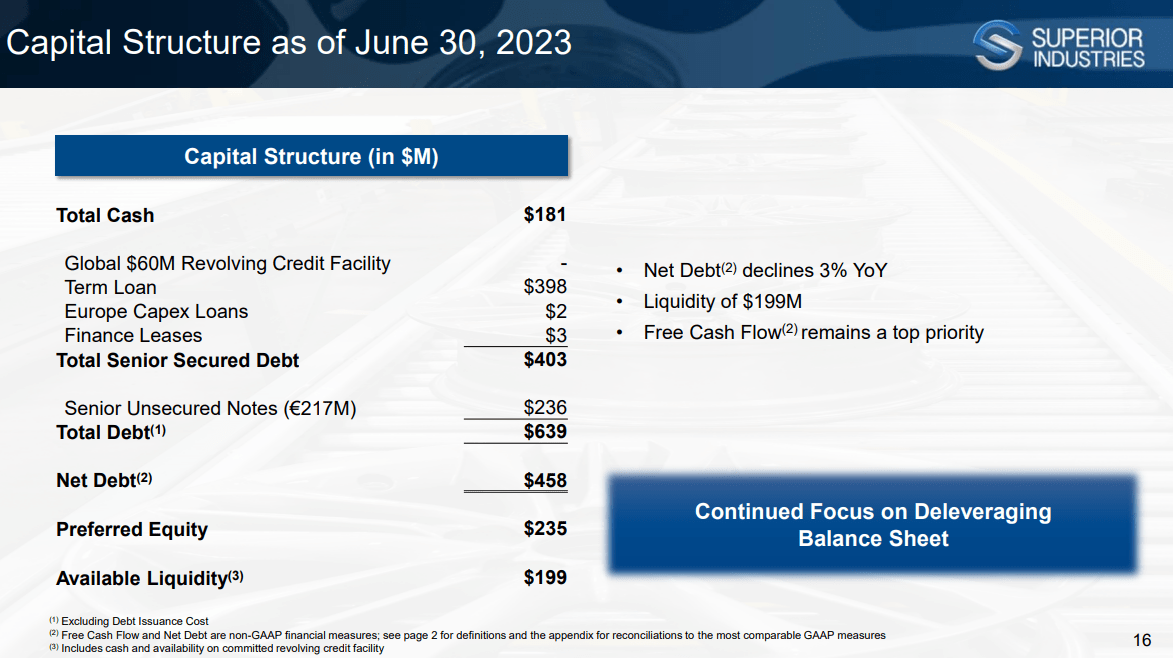

Capital Structure

Superior Capital Structure (Superior Investor Presentation)

{kind=link}

Superior has about 27m shares outstanding, which currently trade at ~$3.50/share - roughly a $100m market capitalization. Superior also carries a $399m term loan, €217m of senior notes (~$236m @ 6/30/23), and $5m other debt against $181m of cash for $458m net debt. Lastly, they have preferred stock, convertible at $28/share with an initial value of $150m, redeemable after September 2025 for $300m in cash or a maximum of 5.3m shares.

Note - the company can possibly defer repayment on the preferred after 2025, per their 10-K : "Under Delaware law, any redemption payment would be limited to the "surplus" that our Board determines is available to fund a full or partial redemption without rendering us insolvent." As the Term Loan with Oaktree is currently agreed, not paying off the notes would accelerate the $400m repayment, so Superior would need to work out a waiver with Oaktree to defer this amount.

If we value the preferred at the full $300m, the total Enterprise Value ("EV") is $100m + $458m +$300m = $858m, which is what it would take to buy the full company today before any equity premium and not giving them any credit for significant owned real estate.

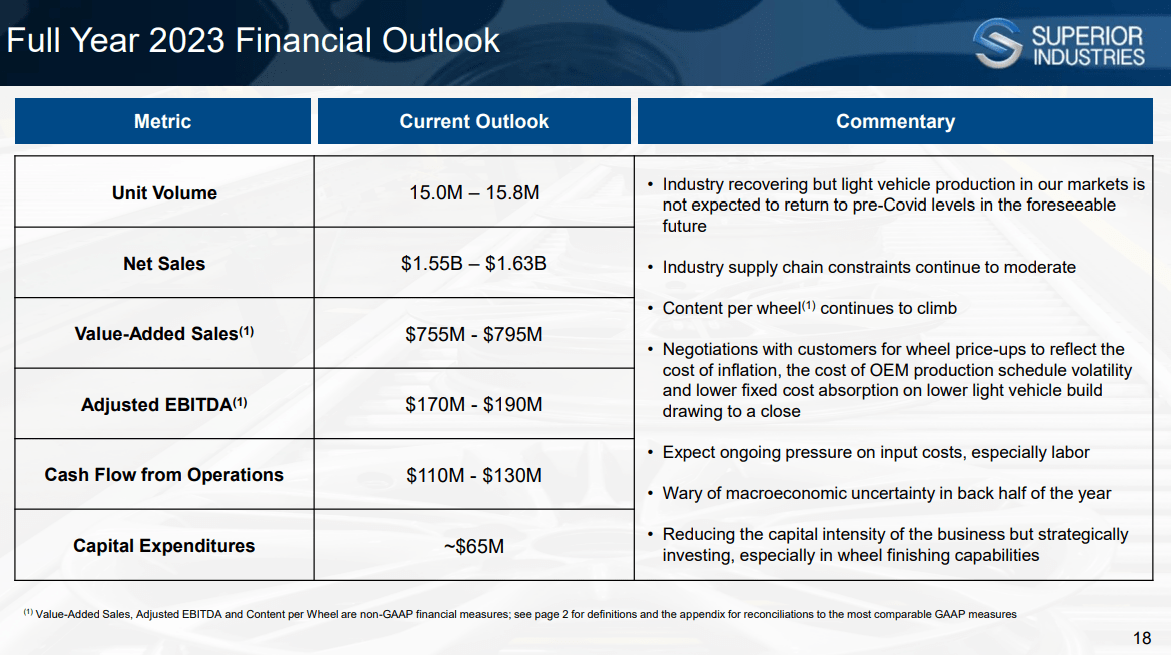

FY23 Guidance

Superior Guidance (Superior Investor Presentation)

{kind=link}

Superior is guiding to a midpoint of $180m Adjusted EBITDA (4.8x EV/EBITDA), $120m of cash from operations in 2022 and $65m of CapEx. Subtracting another $14m for preferred dividends, 2023 free cash flow to equity should be $41m at the midpoint, about a 40% yield to common shareholders and unleveraged yield is almost 15%. Given current auto supply is not exactly at all-time highs, these metrics are not very demanding on what are hopefully depressed earnings. This guidance also suggests they will reverse the negative FCF YTD, due to some fluctuations in aluminum payables (per Q2 call).

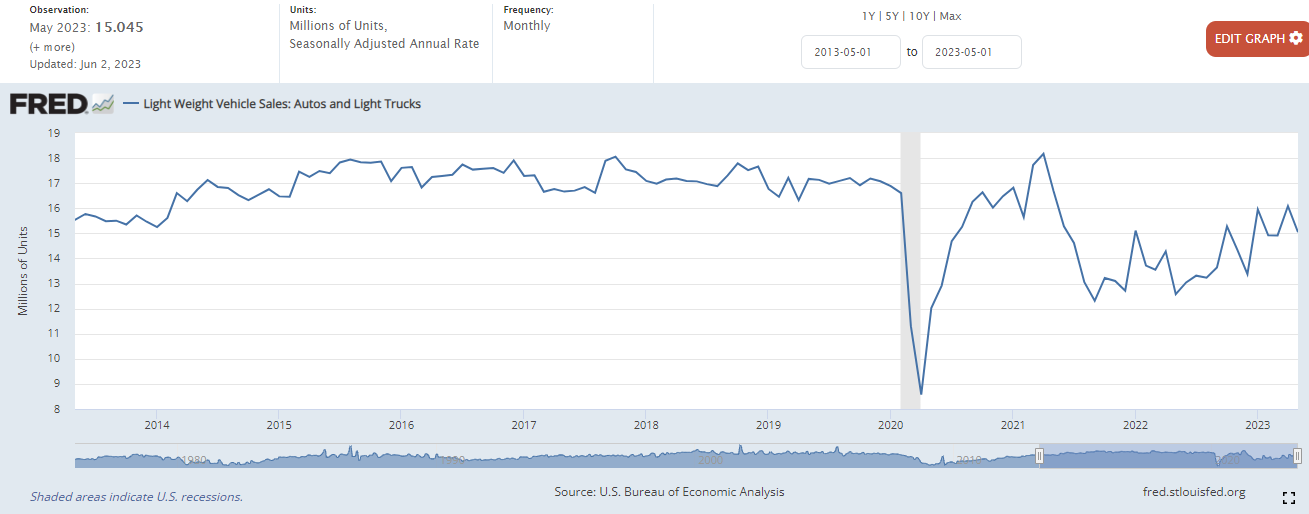

Auto Production

I dislike making macro calls, I.e., predicting the direction of automobile manufacturing. My goal here is to show that I think the most likely direction for demand for Superior's products is up.

US Light Vehicle Production (FRED) US Auto Inventories (FRED)

{kind=link}

{kind=link}

There is a relative lack of vehicles in the US currently, and I expect the result of this to be demand for wheels to remain steady or increase. Sales in Europe also remain far below pre-covid levels. If new vehicles are prohibitively expensive, then hopefully this will increase aftermarket demand (though it is only ~6% of Superior's business). GM, Ford, and VW represented 26, 16, and 14% of FY22 sales respectively, making their production a key driver for Superior investors.

There have been looming talks of a UAW strike , which could certainly harm Superior's main customers.

Valuation

Auto suppliers are generally not great businesses, and I wouldn't be surprised if Superior trades near 5x EBITDA going forward, but there is upside to the stock if it maintains the current multiple.

If FY24 EBITDA can hit $200m with European restructuring and no additional growth, and the stock trades at 4.5x, the resulting $900m EV would only be a $42m accretion to the current EV but would have the tailwind of reduced leverage from cash generated by the business, and all that accretion goes to the equity. Between debt paydown and EBITDA growth, the current share price could easily double to $7 in this scenario.

If we advance to FY25, when the 6% senior notes will be due and the preferred stock will be callable, Superior appears on track to pay the notes off in full or refinance a portion. Interestingly, in this scenario, Superior may be able to settle the preferred using only the 5.3m shares it is redeemable for.

Assumptions:

-

Oaktree debt of $400m remains outstanding

-

2025 notes paid off from cash balance and continuing operations

-

Preferred converts in shares if ($300/5.3)*share price > $300m, meaning Superior would need to trade up to $57/share

-

2025 vehicle production roughly equals 2019 and Superior's improved earnings per wheel scales up as capacity utilization increases

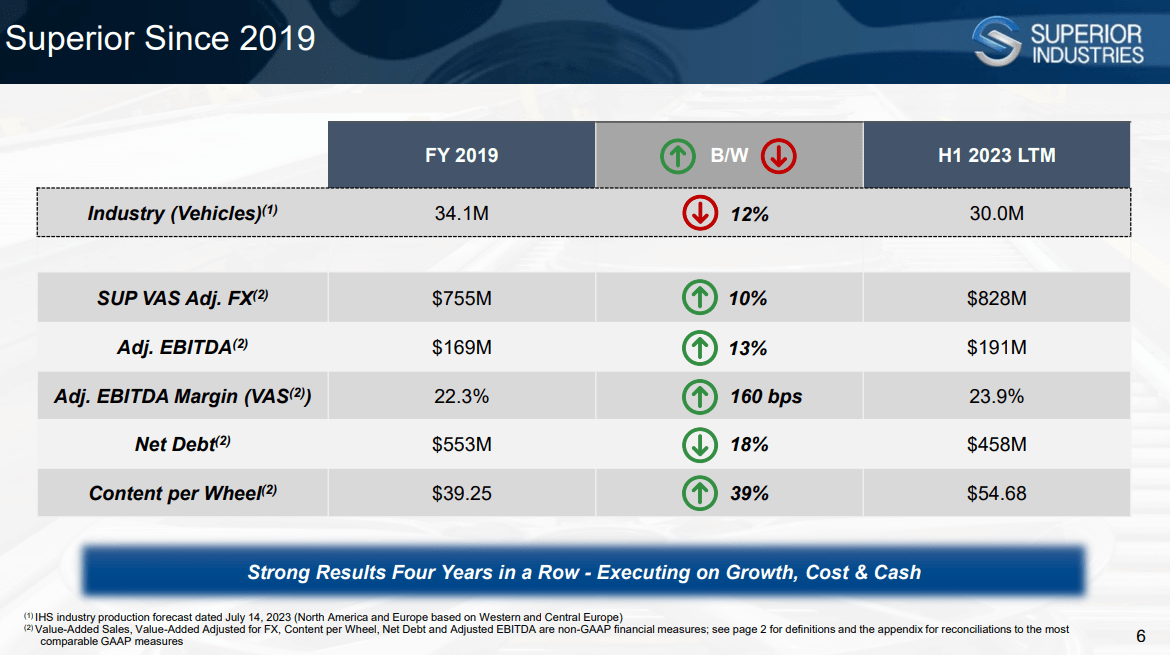

Superior Margin Evolution (Superior Investor Presentation)

{kind=link}

In FY19, Superior was able to sell about 19m wheels against 35m vehicles produced in Europe and North America, earning EBITDA of almost $9/wheel. In FY22, earnings had improved such that 15m wheels earned about $12.50/wheel with vehicle production down about 10% from FY19. If we assume Superior can recover to 2019 production levels, but maintain their better earnings per wheel ($12.50-$15/wheel), FY25 EBITDA could be $250-300m. I would expect with higher factory utilization, margins would increase to the top of this range, but the amount of production Superior can recover remains to be seen.

It seems possible the stock could trade at 7x EBITDA if there is a clear path to eliminating the preferred overhang and leverage is back below 2x EBITDA. Therefore, 7 * 300m = $2.1B EV, less $400m debt plus $150m of cash generated is $1.85B valuation/32.5m shares after conversion = $57/share. This is a blue-sky scenario, but maybe not as outlandish as you would expect for a stock trading under $4 today. This kind of outcome could also be part of some kind compromise with TPG to remove the overhang sooner.

Risks

If I'm going to suggest a stock has this much potential upside, there must be some risks.

-

Leverage is significant. If operations deteriorate, Superior may struggle to pay off or refinance their 2025 notes, or trip covenants on their debt. Investors in Superior should be aware that shares could end up being a donut in this scenario, or they may face significant dilution to address debt issues.

-

Per the Superior 10-K, "In March 2022, the German Federal Cartel Office initiated an investigation related to European light alloy wheel manufacturers, including Superior Industries Europe AG (a wholly owned subsidiary of the Company), on suspicion of conduct restricting competition. The Company is cooperating fully with the German Federal Cartel Office. In the event Superior Industries Europe AG is deemed to have violated the applicable statutes, the Company could be subject to a fine or civil proceedings. At this point, we are unable to predict the duration or the outcome of the investigation." To the extent Superior is found liable for anti-competitive practices, they may face significant legal ramifications. The maximum fine appears to be 10% of annual sales (<$70m) if Superior is out of compliance.

-

Superior discloses two other legal items in their filings, including a $14m dispute with an energy distributor in Poland and $11m dispute with an OEM customer on prior wheel orders. These claims are small relative to Superior's enterprise value but material to their equity valuation.

-

There are no guarantees that volumes will recover in Superior's markets, or that they can maintain current margins. The market shift to Electric Vehicles ("EVs") is believed to be a tailwind for Superior, as EVs use premium wheels due to weight , but in an evolving market there is a risk they lose share to emerging peers.

-

There is no guarantee that Superior will receive a better market multiple if they simplify their business or grow their earnings. To the extent they are unable to meaningfully convert EBITDA to shareholder returns, they will be at the mercy of external market forces.

-

After Superior's Q1 report, the stock rallied to over $7 and insiders sold some shares, including the CFO filing a 10b-5 plan to sell 75k shares. Insiders sell for a variety of reasons, and I don't begrudge reducing your stake by 1/3rd after the stock recently doubled. Seeing buys from Mill Road helps ease this overhang.

-

There was an odd takeover offer last November by M2 Capital for $5.85/share . The offer hasn't been addressed by the company beyond acknowledging a lack of genuine interest after both their press releases . A real tender offer would be significantly complicated by the outstanding preferred shares.

-

If Superior is possibly worth $57/share by 2025, it seems likely that Mill Road, Oaktree, or TPG would make a bid for the whole company before then at a much lower premium. Paying around $1B for a business they could flip for $2B in 3-5 years sounds pretty good, especially given they all have capital sunk into the business already. Shareholders would likely do well in a takeover from current prices.

Conclusion

Superior's acquisition of UNIWHEELS in 2017 led to significant growth in revenues and EBITDA, but the complexity of its capital structure, including the redeemable preferred stock deal, presents a hurdle to overcome before the 2025 debt and convertible preferred stock maturities. This provides opportunities for the company to unlock value for its shareholders as maturities approach. Monitoring the evolving automobile landscape will be essential for potential investors. Tailwinds to the industry may be extremely favorable for Superior shareholders, and Mill Road is seizing the moment.

For further details see:

Superior Industries: Mill Road Keeps Buying, Should You?