SUMXF - Supremex: Without A Q3 Earnings Surprise Optimization Initiatives And M&A Imply Undervaluation

2023-11-22 08:28:24 ET

Summary

- New optimization initiatives in the packaging segment could improve FCF margins.

- The company's M&A strategy remains intact and demand continues to improve, particularly in the packaging market.

- The balance sheet appears healthy, with cash on hand and a solid balance sheet, which could have a positive effect on the company's valuation.

Quarterly revenue figures of Supremex Inc. (SUMXF) did not surprise investors; however, new optimization initiatives in the packaging segment recently announced could bring FCF margin improvements. Given the current state of the balance sheet, I also believe that successful new acquisitions and EPS momentum from the acquisition of Royal Envelope could have a positive effect on the valuation of Supremex. Inflation, failed M&A, and goodwill impairments are risks to take into account; however, I believe that the company appears inexpensive.

Supremex: Delivered Beneficial Long-Term Expectations, M&A Strategy Remains Intact, And Demand Continues To Improve

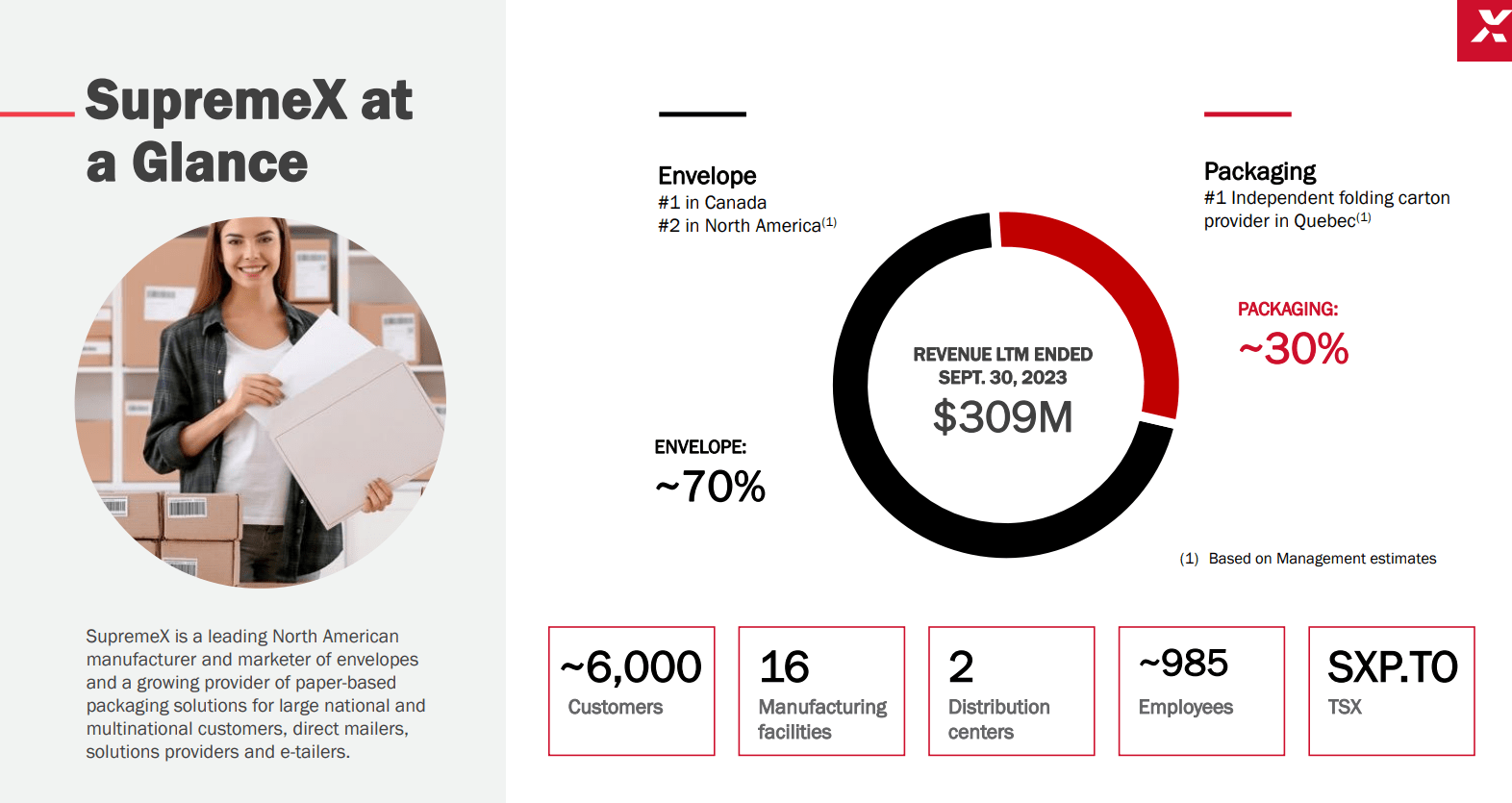

Supremex Inc. is a North American manufacturer and marketer of envelopes. In addition, it is a growing provider of paper-based packaging solutions with close to 6k customers in the United States and Canada.

In the last quarterly report, the company noted that with quarterly revenue of CAD309 million, 70% represented sales from envelopes, and 30% was from packaging revenue.

{kind=link}

Supremex did offer beneficial comments with regards to FCF generation in the quarter, but noted that higher interest rates and inflation may harm the business model in the short term. With that, I think that with cash in hand and a solid balance sheet, its long term M&A strategy remains intact.

The company offered a long presentation in the last quarterly meeting. However, I believe that investors may obtain a good impression about the state of the company from the slide below and some other factors that I included in the article.

Source: Investor Presentation

It is worth noting the words from management about the debt reduction and the repurchase of shares, which may have a beneficial impact on the market as soon as more investors have a look at the release.

Demand continues to improve but somewhat slower than expected with high inflation and interest rates still affecting direct mail and consumer product spending. With continuous efforts to drive efficient working capital management, Supremex generated a solid free cash flow during the third quarter. Taking into consideration the business acquisitions, Supremex reimbursed over CAD9 million of long-term debt and repurchased shares. Source: SupremeX-Announces-Q3-Results

Balance Sheet

The most recent balance sheet reported includes cash of CAD0.7 million, accounts receivable of CAD33 million, and total current assets close to CAD82 million. Total current assets are significantly higher than the current amount of liabilities, so liquidity does not seem a problem.

With property worth CAD53 million and with goodwill of CAD59 million, intangible assets are equal to CAD40 million. Total assets are equal to CAD283 million, so goodwill represents a significant part of the total amount of assets. Hence, Supremex does report a significant expertise in the M&A markets.

Source: SEDAR

With total current liabilities of CAD32 million, long term debt is equal to CAD68 million, and lease liabilities stand at CAD29 million. I am not really concerned about the long term debt. The asset/liability ratio is close to 2x. In sum, I believe that the balance sheet appears quite healthy.

Source: SEDAR

Best Case Scenario: Optimization Initiatives In The Packaging Segment And Successful M&A Could Bring Significant FCF Growth

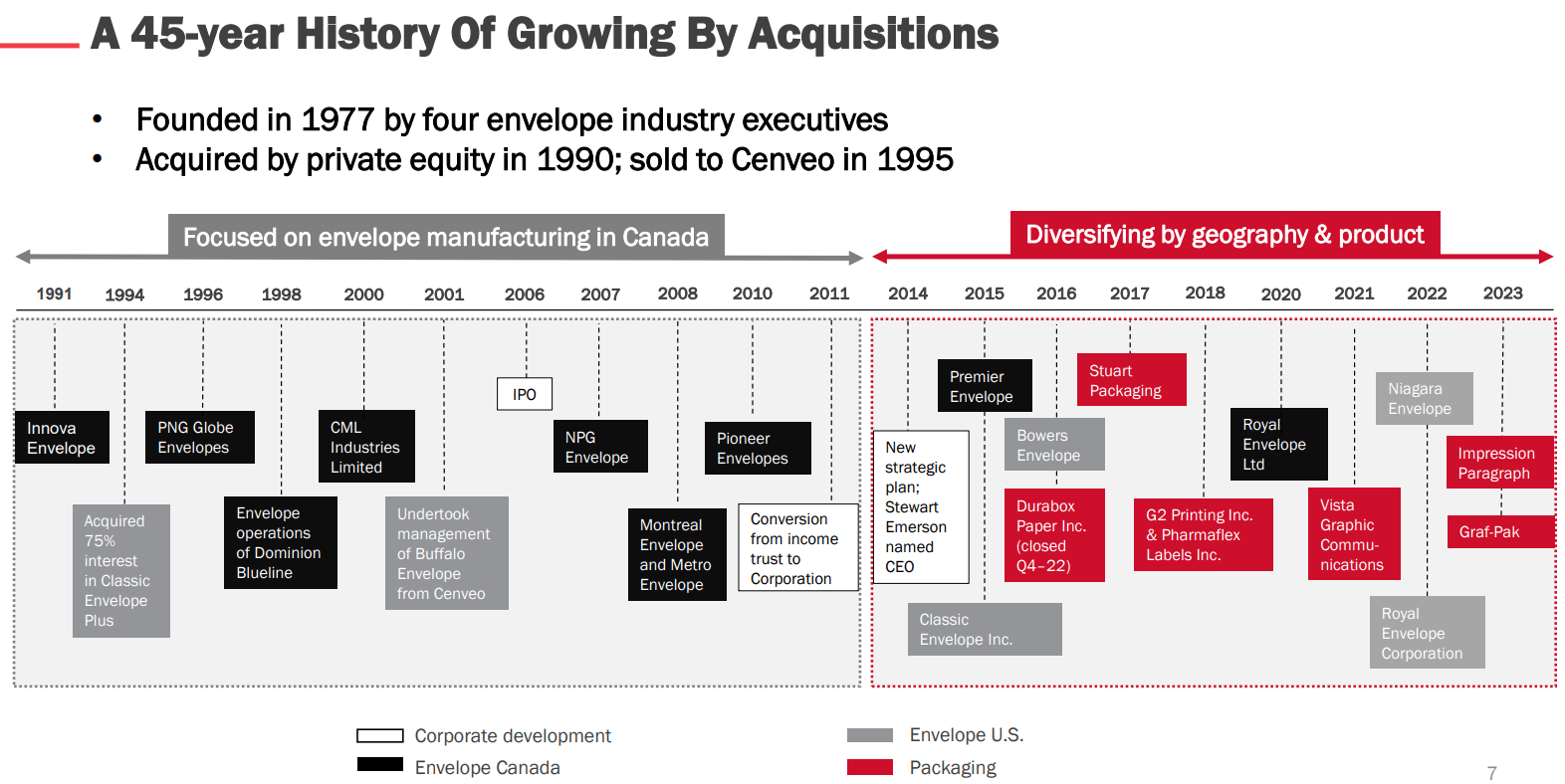

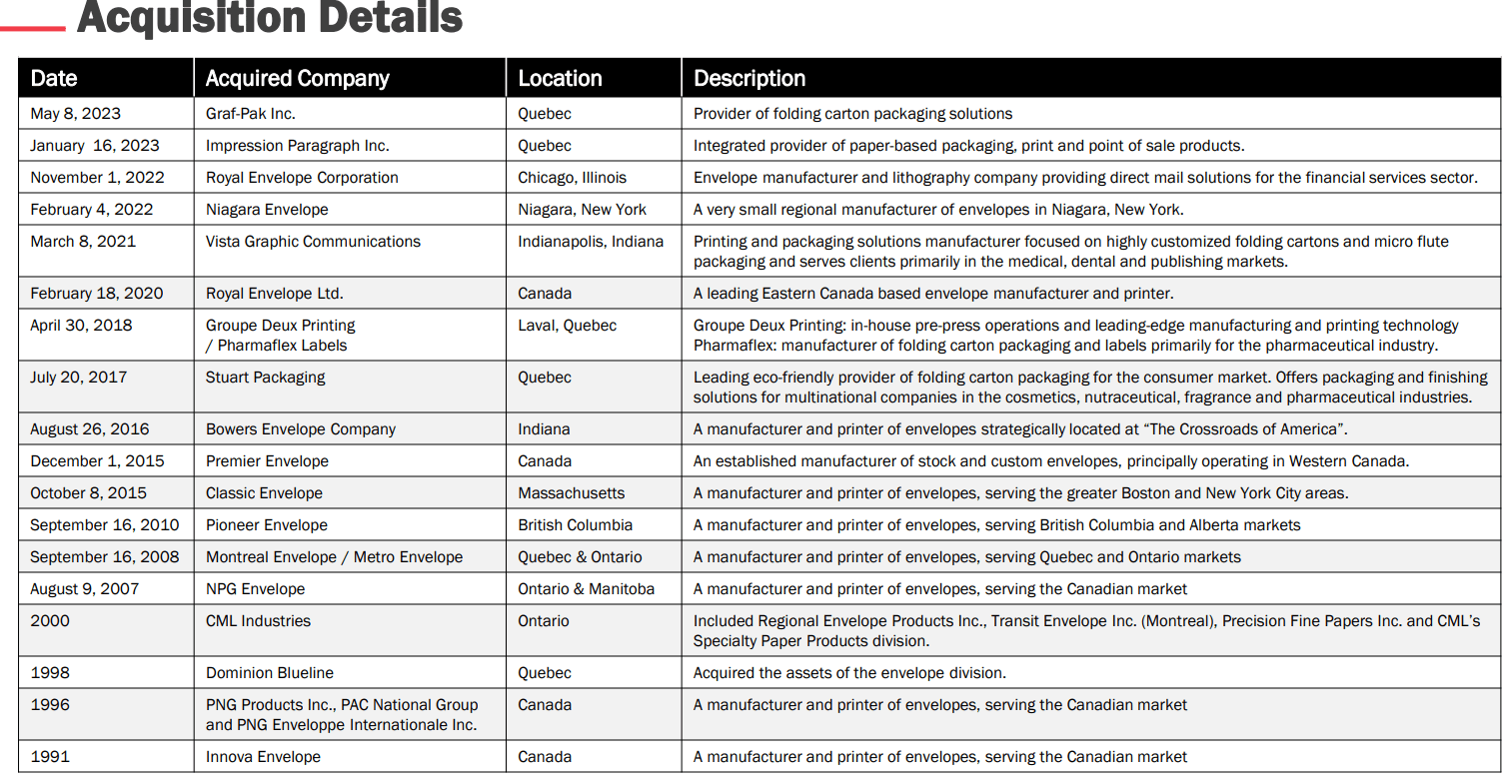

Under my best case scenario, I assumed that Supremex will successfully find new targets, and will be able to integrate them successfully. In my view, given the previous expertise in the M&A markets, Supremex does have the know-how necessary to grow inorganically. Founded in 1977, the company has grown significantly through acquisitions.

{kind=link}

{kind=link}

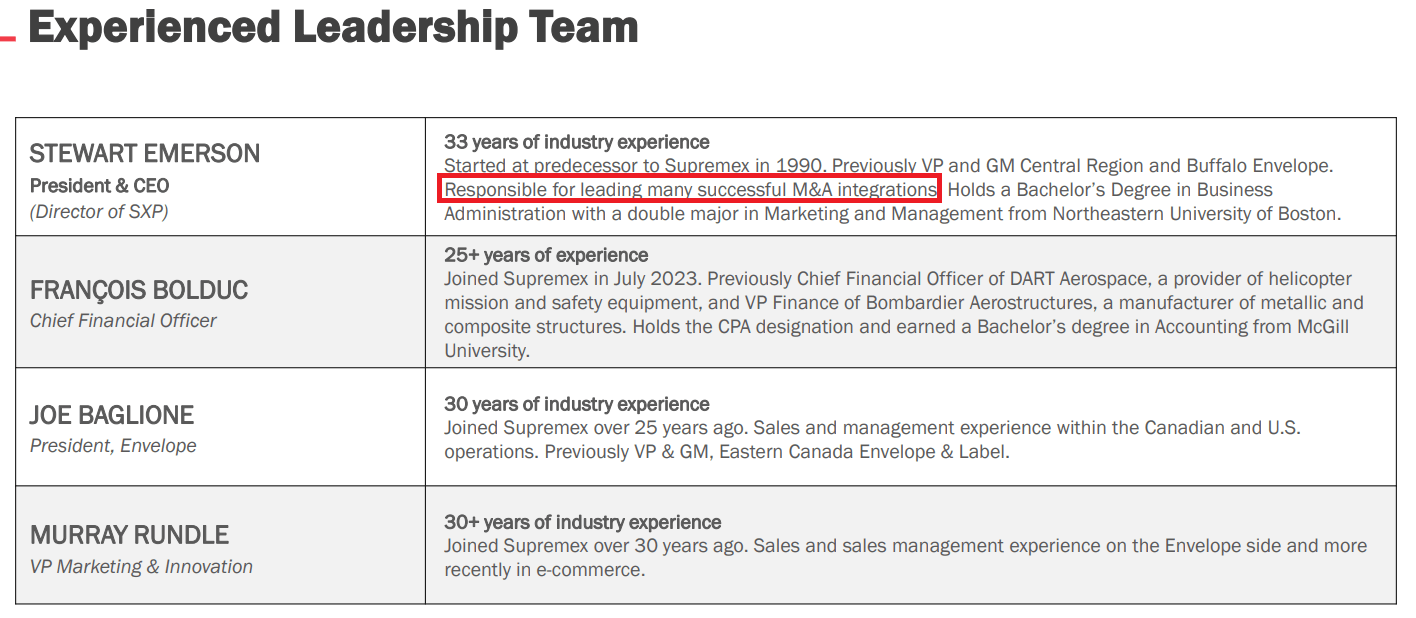

I also reviewed the team, which includes members with invaluable knowledge in the M&A markets. Specifically, I would point out the expertise of the CEO, who seems to have led a number of M&A integrations.

{kind=link}

Note that Supremex recently established a strategy based on acquisitions and organic growth in the packaging market, mainly in Canada. The emergence of new e-commerce markets is expected to bring significant growth to the packaging market, so I believe that the corporate move is smart.

{kind=link}

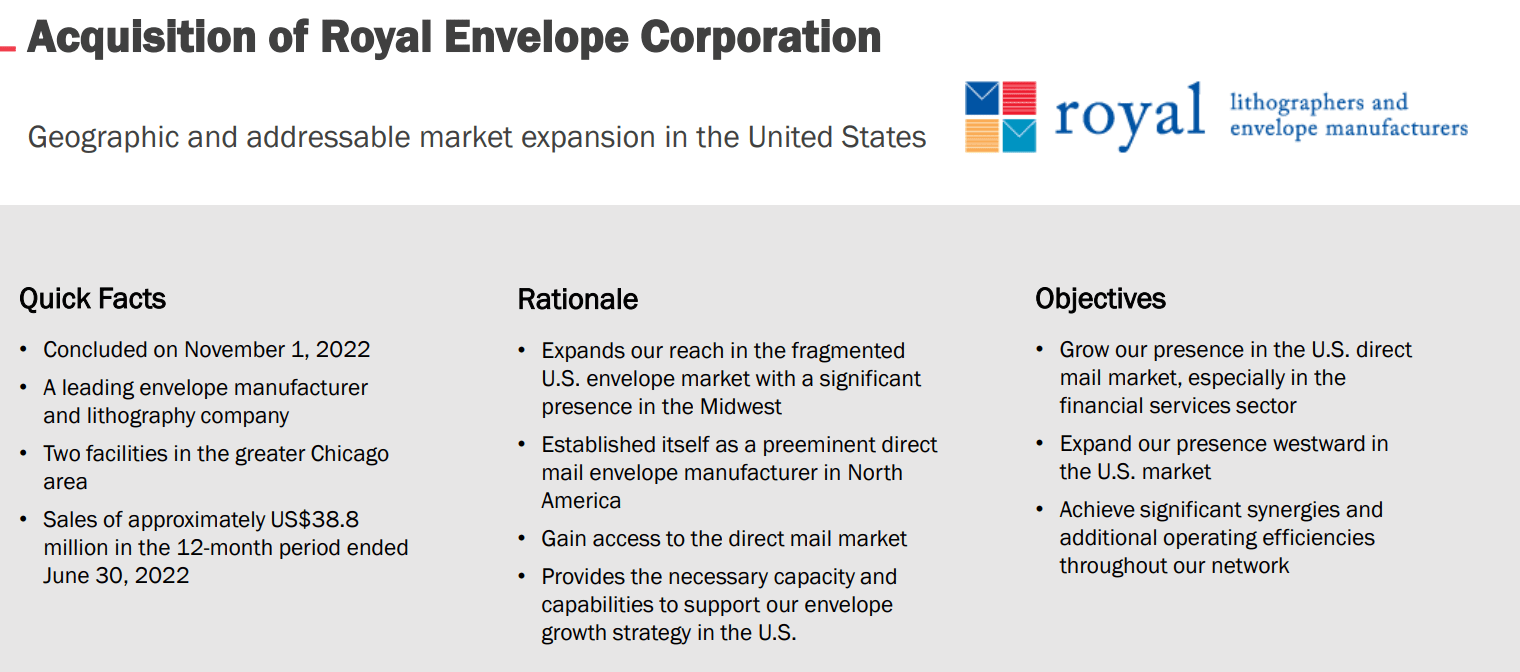

Under this scenario, I also assumed that the recent acquisition of Royal Envelope could bring significant new presence in the U.S. direct mail market, and bring synergies to be seen in 2023 and 2024.

{kind=link}

Additionally, I believe that the recent optimization initiatives in the packaging segment announced a few weeks ago may bring cost savings and FCF margin growth. In my view, as soon as other investors have a look at the announcement, demand for the stock could increase, which may lead to share price appreciation.

On October 17, 2023, the Company announced optimization initiatives in the packaging segment to enhance efficiency and yield synergies resulting in annual cost savings of CAD1.5 million once all measures are implemented. Source: SupremeX-Announces-Q3-Results

I also assumed that Supremex will continue to design product mixes and price increases that will successfully find demand in Canada and the U.S. Given the expertise of management in these matters, I do not think that I am thinking that out of the box. In the last quarterly report, the company noted that successful price increases mitigated cost inflation.

The increase is attributable to a CAD32.2 million contribution from Royal Envelope, an average selling price increase of 31.6% from last year primarily reflecting a more favourable customer and product mix in U.S. operations and price increases implemented throughout 2022 to mitigate input cost inflation, as well as a favourable currency conversion effect. These factors were partially offset by lower volume. Source: SupremeX-Announces-Q3-Results

Finally, I believe that the renewal of its NCIB program, which is expected to bring further stock repurchases, could accelerate the demand for the stock. As a result, we could see stock price increases.

The Company announced the renewal of its NCIB program. Under the new program, Supremex is authorized to purchase, for cancellation, up to 1,294,058 common shares, representing approximately 5.0% of issued and outstanding common shares of the Company as at August 18, 2023. Purchases will be made over a 12-month period ending on August 30, 2024. Under the previous program, Supremex repurchased 185,700 common shares at an average weighted price per share of CAD4.7963. Source: SupremeX-Announces-Q3-Results

Assuming a long term risk free rate of close to 2.9%, beta of 1.1, market risk premium of 5.7%, and cost of equity of 8.6%, I obtained an implied WACC close to 6.9%, which I think is quite conservative.

Source: DCF Model

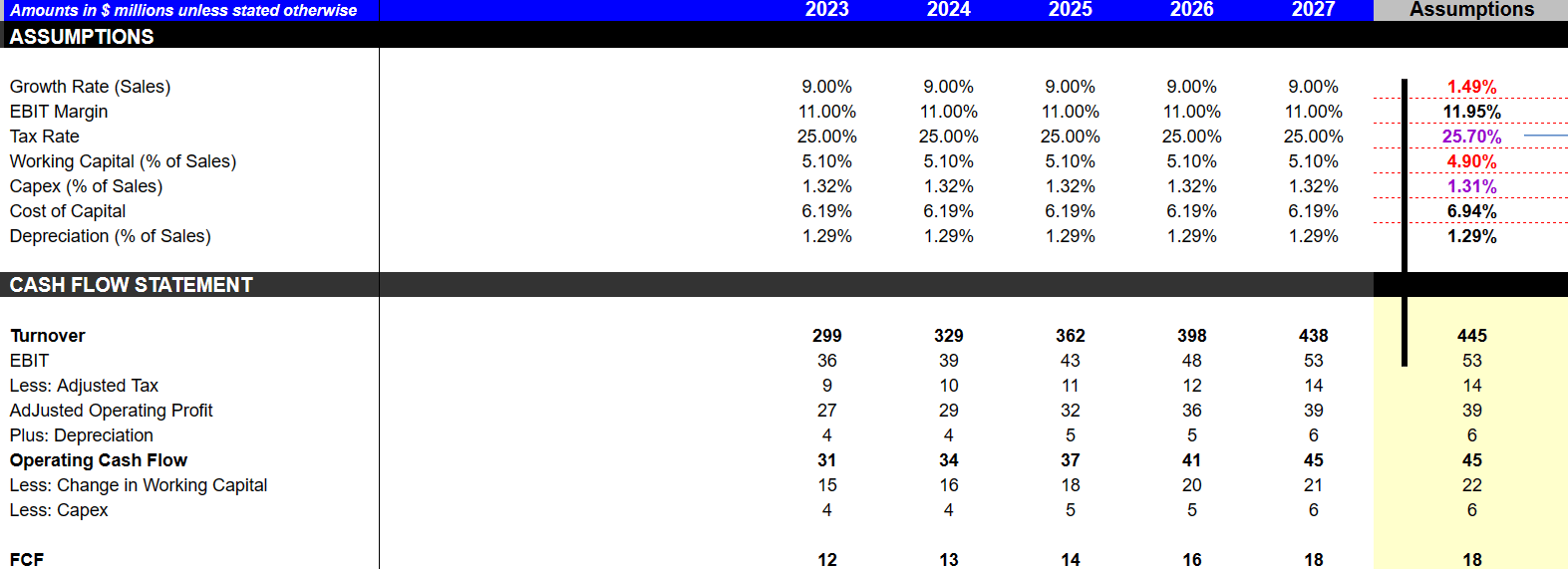

With a DCF model including FCF from 2023 to 2027, I used a net growth rate of 9%, EBIT margin close to 11%, working capital/sale of 5%, and capex/sales of 1.32%.

In addition, with depreciation/sales close to 1.29%, I obtained the following results for the year 2027. Net sales would stand at CAD438 million, with EBIT of CAD52 million, operating cash flow worth CAD44 million, changes in working capital of CAD21 million, and capex of CAD6 million. Finally, 2027 FCF would be close to CAD18 million. Using a Gordon Growth model, I also took into account very conservative long term assumptions, including net sales growth of 1.4% and an EBIT margin of 11.95%. The rest of the model is given below.

{kind=link}

The previous figures lead us to a present value of residual value close to CAD231 million, an equity value close to CAD225 million, and a fair price valuation of about CAD8.65 per share.

Source: DCF Model

{kind=link}

Bearish Case Scenario, And Major Risks

I believe that major risks include failed acquisitions or goodwill impairments derived from overpaying for targets. As a result, impairments could lower the book value per share, and lead to share price declines. In this regard, it is also worth noting that failed acquisitions may not be welcomed by investors. If they decide that Supremex does not know how to acquire targets, or select targets, the demand for the stock may lower.

It is also worth noting that the company may not be able to find suitable targets to acquire in the packaging market. Besides, Supremex could find acquisition targets, but at a price that is more expensive than what management requires. In this case scenario, less inorganic growth will most likely lead to lower stock capitalization.

Under this scenario, I also took into account that inflation may also harm Supremex in the long term. If clients decide to lower their orders, and are reluctant to accept price increases, in my view, Supremex could see lower EBIT and FCF margins. As a result, the implied stock valuation may lower, and stock price could decrease.

Under my bearish case scenario, I included a net sales growth rate of 3.5%, with an EBIT margin of 9%, tax rate close to 26%, and working capital/sales of about 5%. Besides, with capex/sales of 1.5%, I also took into account cost of capital close to 7.5% and depreciation/sales of 1.2%.

My results included 2027 net sales of CAD438 million, 2027 EBIT close to CAD52 million, 2027 adjusted operating profit worth CAD38 million, and 2027 operating cash flow worth CAD44 million. Finally, with changes in working capital of about CAD21 million and capex of CAD6 million, 2027 FCF would stand at close to CAD15 million. Like in the best case scenario, I used the Gordon Growth model with conservative assumptions about net sales growth, D&A, and other assumptions, which resulted in FCF of about CAD6 million.

Source: DCF Model

With the previous assumptions, I obtained an enterprise value close to CAD147 million, equity value of CAD79 million, and an implied forecast price of CAD3.05 per share.

Source: DCF Model Source: DCF Model

Competitors Seem To Be Trading A Bit More Expensive Than Supremex

I checked some of the companies competing with Supremex. My peer group trades at close to 2.2x EBITDA, and traded in the past between 5.9x and 4.8x. Median EV/Sales also stood at close to 0.7x and 1.4x.

{kind=link}

Given the trading multiples reported by Supremex, I would say that the company appears a bit undervalued as compared to the peer group. I think that other analysts out there may use different competitors in their peer group. With that, I believe that most would say that Supremex could be trading at a bit more expensively.

Source: Ycharts Source: Ycharts

Conclusion

Supremex did not deliver better than expected quarterly revenue in its last quarterly report, however management made several valuable commentaries that may move the stock price up. First, the company noted optimization initiatives in the packaging segment, which may not only bring new synergies, but also FCF margin improvements. I also believe that the balance sheet is well positioned to include the new promised acquisitions. Besides, I believe that the recent acquisition of Royal Envelope could bring further EPS momentum in the coming years. Yes, there are risks out there from inflation, failed price increases, or product mix offering. With that, I believe that Supremex could trade at a maximum price mark of $8-$9 per share. It does look a bit undervalued.

For further details see:

Supremex: Without A Q3 Earnings Surprise, Optimization Initiatives And M&A Imply Undervaluation