SGRY - Surgery Partners: Capital Intensity Without The Earnings (Rating Downgrade)

2023-09-15 23:14:55 ET

Summary

- Surgery Partners continues its financial performance throughout FY'23.

- SGRY operates 152 surgical facilities and has revised its projections for FY'23 to pre-tax earnings of $435mm.

- SGRY's asset-heavy business model and low earnings rate on capital raise concerns about shareholder value creation.

Investment briefing

Healthcare minors have rolled over into the backend of the year after catching a strong bid in early FY'23. Names like Surgery Partners, Inc. ( SGRY ) are still priced to perfection, despite lacking the economic rigor needed to sell at more pleasing valuations. Since the last SGRY publication, there's been multiple investment updates, that are discussed here.

As a reminder, SGRY books revenues from 2 channels: patient service revenues and 'other' service revenues. Patient service is broken into 2 sub-segments, 1) surgical facility services, and 2) ancillary services. This includes charges for procedures performed at surgical facilities, patient fees at physician practices, anesthesia services, pharmacy services, and diagnostic screens ordered by SGRY's physicians. Other service revenues are booked from management and administrative service fees from its non-consolidated facilities.

At the end of Q2, it operated a portfolio of 152 surgical facilities, located in 32 states, made up of 134 ambulatory surgical centers and 18 surgical hospitals. SGRY holds a majority ownership stake in 92 of these facilities, and 119 of them are consolidated under its winds.

Net-net, I'm revising my outlook on SGRY to a hold for the reasons discussed here today.

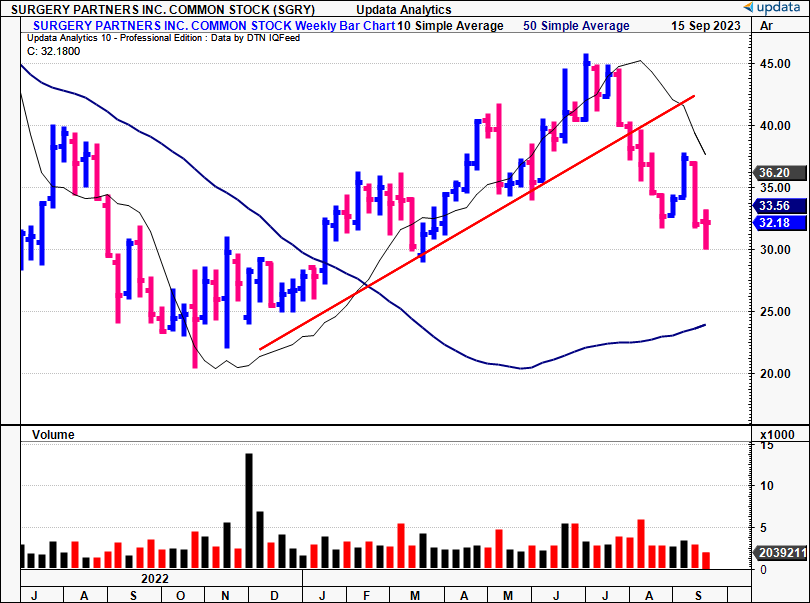

Figure 1. SGRY Breaking lower support line into H2, trading below 50DMA with descending volume.

{kind=link}

Critical investment facts to revised thesis

1. Analysis of latest developments

SGRY put up Q2 revenues of $667.6mm , up 8.5% YoY. Growth was underscored by 200–300bps of volume increase (demand) and rate changes (pricing) of 2%—3%. Acquisitions sported ~200–350bps of top-line growth, and remain a key revenue growth driver for the company. On a same-store basis, turnover was up ~8.3%. It pulled this t pre-tax earnings of $100.2mm, a 16.4% increase YoY, on net income of ~$19mm, up ~$28mm YoY.

Given the momentum this YTD, management revised its projections for FY'23, and now looks to pre-tax earnings of ~$435mm by yearend. Figure 2 shows the revenue + OCF walk YoY, along with the H1 FY'23 top-line breakdown. Cash flows backing revenues are flat at 8% of turnover, whilst its orthopaedic and pain management business remains the biggest segment on revenue terms.

Unit economics continue to ratchet higher. For example:

- Total case growth was up ~530bps YoY on a 4.8% growth in revenue per case. It performed around 26,000 orthopedic procedures were performed during the quarter. The growth was underlined by 73% procedural growth in total joint surgeries in its Ambulatory Surgical Centers ("ASCs"). The total number of surgical cases for Q2 came to 155,000, up 4.1% YoY, with same-facility cases growing in the 2–3% region.

- It deployed $60mm towards ownership interests in 3 surgical facilities during the quarter. It also bought a surgical facility currently in development. Each of the acquisitions was made at an average of 8x TTM earnings, bringing the total spend to $119mm on acquisitions this YTD. The firm is aiming to deploy at least $200mm annually, to we could expect ~$80mm or so in the back end of the year. In fact, management is projecting to bring 15 de novos online over the coming 18 months, which could be a tailwind if all goes well.

BIG Insights

2. Long-term economic performance—asset-heavy business, small earnings rate on capital

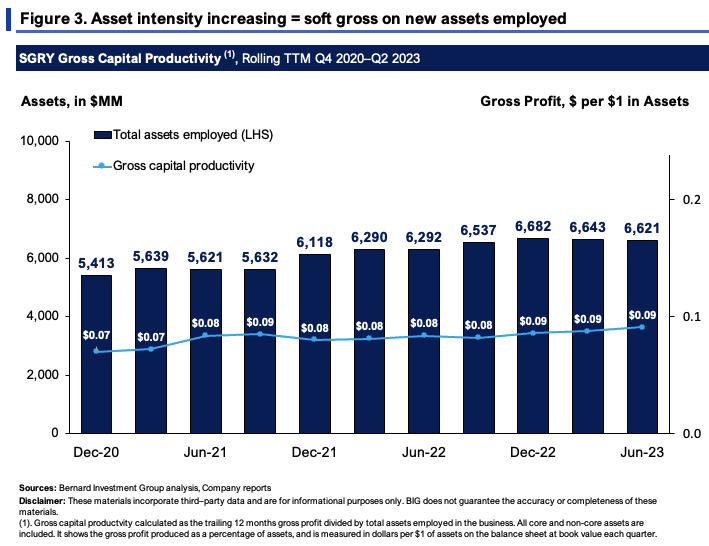

Deeper economic analysis of the investment facts pattern is revealing of a company failing to create shareholder value. I must admit it starts to make sense why the market has placed such a thin premium on assets employed into SRGY's business after scrolling through some of the numbers here.

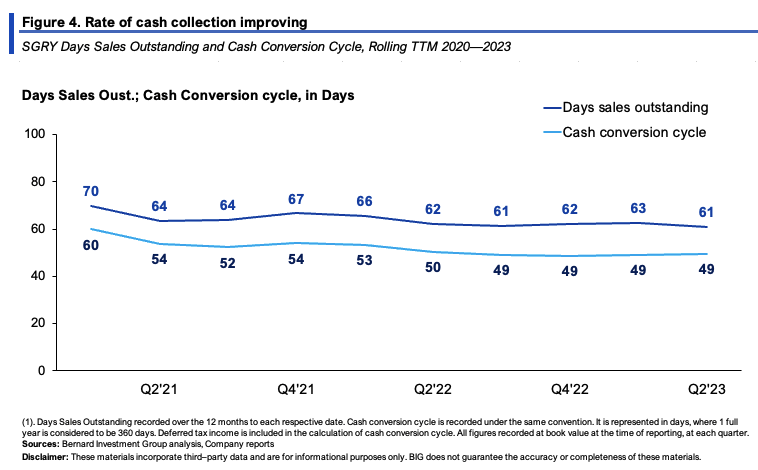

For one, the firm has $6.6Bn of assets employed on the balance sheet, up from $5.4Bn 2.5 years ago [see: Figure 3]. Most of this is in accounting goodwill secondary to its acquisition strategy. But these assets rotate back just $0.09 on the dollar in gross profit—simply unacceptable for the astute investor. That's every $1 of assets employed just $0.1 in gross profit. A figure >$0.3 is considered high, >$0.70 is extraordinary. Well, SGRY's numbers are extraordinarily low in my view. This, despite rates of cash collection improving by ~1 day YoY to every 49 days, as seen in Figure 4.

{kind=link}

{kind=link}

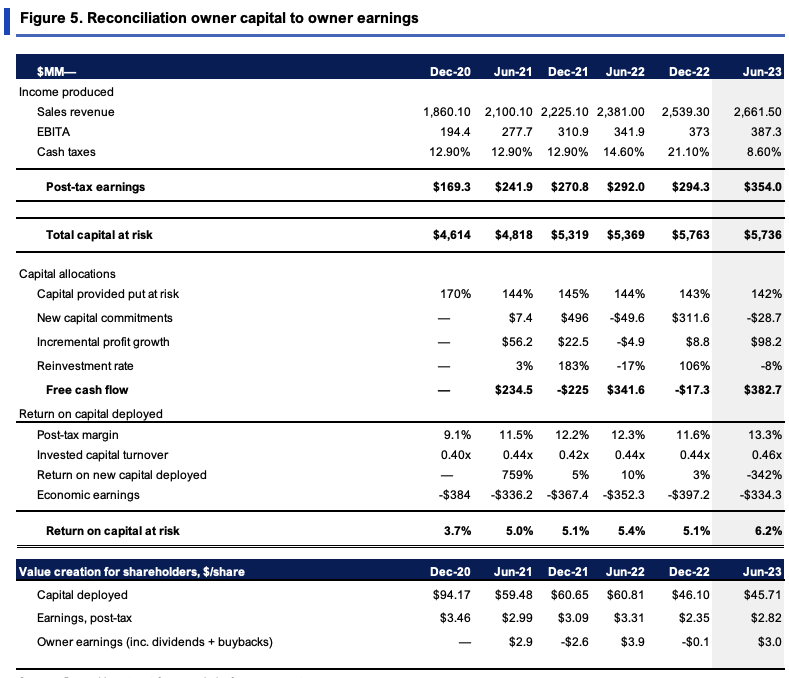

As to the capital put directly at risk in operations—$5.7Bn, or $45.70/share, ~140% of what's been provided by investors (debt, equity). The earnings rate on this is just $2.82/share, otherwise 6.2%. With $5.7Bn in capital returning just $2.82/share, $1 invested in the business is not worth more than $1 in the market—not when long-term market averages are ~12%, considered the hurdle rate here. The culprits? Anemic post-tax margins and tremendously inefficient capital turnover (13% and 0.46x, respectively). FCF has been lumpy, and relatively small. The capital isn't producing enough money in my view, plain and simple.

No different incrementally, either. Since 2020, SGRY has reinvested ~$1.12Bn directly into growing the business (~40% of cumulative NOPAT), to grow post-tax earnings $185mm, a 16.5% incremental rate of return.

{kind=link}

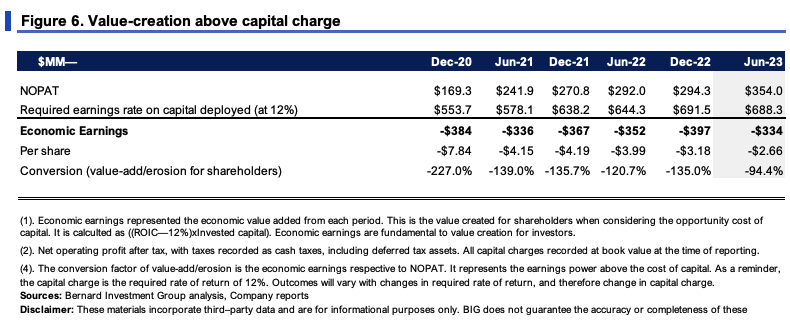

None of these investments have added intense value to the owners of the company's net worth. Figure 6 captures this well. It shows what SGRY needed to do in NOPAT to beat the 12% threshold, a key competency for our equity holdings. As you can see, the economic earnings we're after here are deep in the red. For example, it needed to do $688mm post-tax in Q2 FY'23 (TTM basis), but returned $354mm instead, resulting in a $334mm economic loss. We don't want economic losses—profits are the preference.

{kind=link}

3. Requirements, expectations going forward at steady-state

The value drivers underlining SGYR's business growth from the last 3 years are seen in Figure 7. Sales have grown at a rate of 4%, on an average 13.5% pre-tax margin. The economics from Figures 5 and 6 are so transparent here. Every new $1 in revenue required $0.13 in NWC and ~$0.30 in fixed capital. Almost 50% of every $1 in sales growth is sported by investing requirements. M&A added just 130bps of 'value'.

BIG Insights

Should it continue at this 'steady-state' of operations, you'd get something like what's presented in Figure 8:

- If it wanted to grow at 4% sales moving forward, quarterly investment requirements would be ~$50–$55mm ($200–$220mm annualized), most of this in fixed capital. This aligns with management's objectives outlined earlier. It would sport a $6Bn capital base by FY'24 in this instance.

- FCF of $267mm—$308mm, with quarterly post-tax margins of ~13.5% and capital turns of 0.5x, producing a rate of return of ~5-6% on capital at risk.

- Compounding intrinsic value at ~3.65% on average based on these stipulations.

Are these attractive numbers? Not in my opinion, not with so many other opportunities available that surpass these numbers.

BIG Insights

Valuation and conclusion

The stock sells at tremendously high earnings multiples, but is priced at a low premium to assets/capital. It sells at 36x forward earnings and ~20x forward EBIT, but just 1.4x EV/invested capital. You want a business that's priced appropriately relative to the earnings and assets in the business. That is, low earnings multiples, high multiples of capital.

Taking the numbers from Figure 5 and assumptions from Figure 8, and comparing it to the 1.4x multiple, SGYR's earnings power and asset factors look more than adequately priced in.

BIG Insights

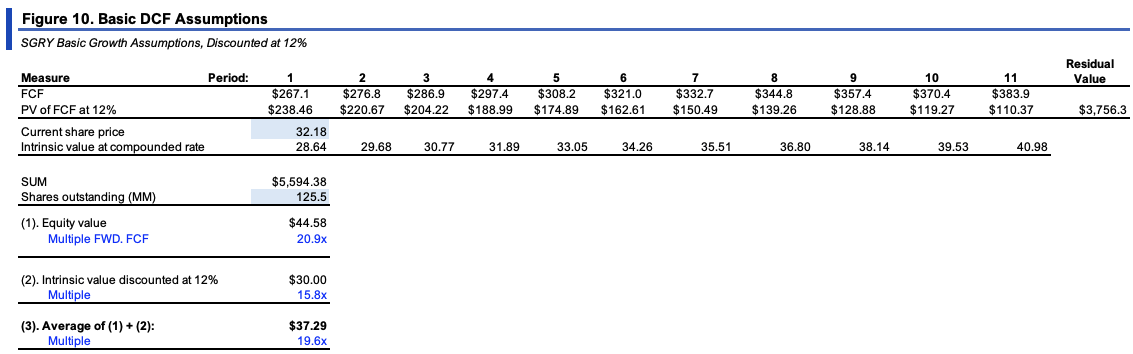

Figure 10 shows the calculus of 1) projecting the cash flows out to FY'28 under the same convention, and discounting at 12% (the hurdle rate used here), and 2) compounding SGRY's market value at ROIC and the reinvestment rates. Averaging the two gets you to $37/share, which supports a neutral view (SGRY sells at $32/share at the time of writing).

{kind=link}

In short, SGRY presents us with lots to think about. For one, it is embarking on an aggressive growth strategy, committing ~$200mm to investment each year to grow the business. Second, unit economics are stretching higher, in procedural volumes and same-store growth, but it stops there for me. All this investment and capital recycling isn't producing attractive business returns. The value of $1 is worth less in SGRY's hands than in the market's, based on long-term averages. Whilst the unit economics are good—the business economics aren't in my view, with thin post-tax margins and <0.5x capital turnover. Around $45.70 produced just $2.8/share in NOPAT, less in FCF/share, and the market isn't agnostic to this, pricing SGRY at 1.4x EV/IC. Net-net, revise to hold.

For further details see:

Surgery Partners: Capital Intensity Without The Earnings (Rating Downgrade)