SGRY - Surgery Partners: Exceptional Business Economics Trading Below Fair Value

2023-06-24 05:03:31 ET

Summary

- Surgery Partners comes with a set of attractive investment criteria.

- SGRY's economic characteristics, such as a consistent stream of 20% returns on existing capital, are standout features in the debate.

- A revised growth outlook and attractive valuation support a buy rating with a $62.50 price target.

Investment Debate In Summary

The realm of selective investment opportunities offering long-term capital gains within the financial markets never ceases to amaze me. I feel blessed to have my DNA woven within the market's epithelial layers, where a vantage point is gained in scrutinizing various companies positioned along the healthcare spectrum.

Case in point here is the recent deep dive I just completed on Surgery Partners, Inc. (SGRY) after noting its 6-month breakout. The stock now trades at 52-week highs and offers the investor a 5.5% forward post-tax earnings yield as I write. Further, the company's unit economics are ratcheting higher with more surgery volumes, and surgeons on its books. Orthopaedic surgery and the like aren't going anywhere and provide a steady stream of business growth, even during economic downturns. These trends are therefore encouraging and backed by a set of tremendously attractive business economics. These show SGRY stretched up the returns produced on its operating assets by 40% on a cumulative basis since 2017.

Prior to 2023, the company was trading well under the radar. However, things have changed, and there was never a deviation from the company's long-term prospects. Now, investors have cracked onto the economic credentials of the firm, thus supporting my buy rating. Net-net, rate buy at $62.50 price target.

Figure 1.

{kind=link}

Critical facts to SGRY buy thesis

After extensive review of all the moving parts, it is my view that the SGRY investment case is quite easy to explain. It boils down to a combination of fundamental, economic and valuation factors. Perhaps most critical to my own investment criteria is the exceptional economic characteristics SGRY has thrown off in recent times. Further, there is reason to expect these trends to continue, based on the evidence presented here.

1. Fundamental drivers of value

It was an impressive quarter for SGRY during Q1 in my view. It clipped quarterly sales of $666mm, a 12% growth, on adj. EBITDA of $90.1 million- up 17% YoY. It pulled an EBITDA margin of 13.5% on this which is a 60 basis points improvement YoY. Growth was underscored by a 12% gain in surgical cases performed, with ~176,000 cases completed during the quarter, averaging $3,784 in revenue per case.

There are notable takeouts from the latest numbers, which set a good stage to understand the company's business economics:

-

On key driver to the firm's income is individual surgery rates. As a positive, SGRY booked a tremendous upsurge in the number of joint replacements performed at its ambulatory surgical centres ("ASCs") in Q1. Volumes were up heavily with an 84% growth in numbers.

- In addition, the firm has demonstrated a keen focus on physician recruitment as a means of driving revenue growth. As evidence of its success here to date, Q1 saw the addition of ~150 new surgeons to the company's books. This adds to the tail of potential surgery volumes it can run through its centres, thereby adding to operating income. This recruitment effort was targeted at high-growth specialties that are critical to the company's operations, ensuring a robust pipeline of qualified physicians for its surgical facilities.

- I would also add that the returns produced on the firm's recruiting efforts are an attractive feature. The recruits from the FY'22 cohort contributed ~78% additional turnover compared to their marks last year. This is a good return and relates directly to points (1) and (2)- more surgeons, more sales, more earnings. Not a difficult cycle to comprehend.

- The firm committed an additional $60mm for strategic acquisitions in Q1, maintaining an average multiple of <8x earnings across each. I believe critically that SGRY's commitment of employing at least $200mm each year through acquisitions could be a bullish factor. I am not the biggest fan of an acquisition-led growth strategy, however, it is not as if SGRY has a lack of opportunities to deploy capital at high rates of return --quite the contrary, as you will see later-- but that acquisitions if done right can add strategic value to the company's portfolio.

Added to the above, SGRY divested 4 of its lower-performing facilities and expects to conclude another 4-6 divestitures by mid-year, so I'd expect a lighter capital base, and, a capital [cash] injection on the sales. This will free up the cash to allocate at more attractive avenues-- a feature that SGRY does well.

The main point I've gleaned from the company's unit economics is that key metrics are showing impressive change. Such momentum in the core revenue drivers, like patient volumes, surgery volumes, surgeon base, and total facilities, is conducive to the company's future. This wouldn't be surprising, given SGRY's long-term record:

Table 1.

Data: Author, SGRY SEC Filings

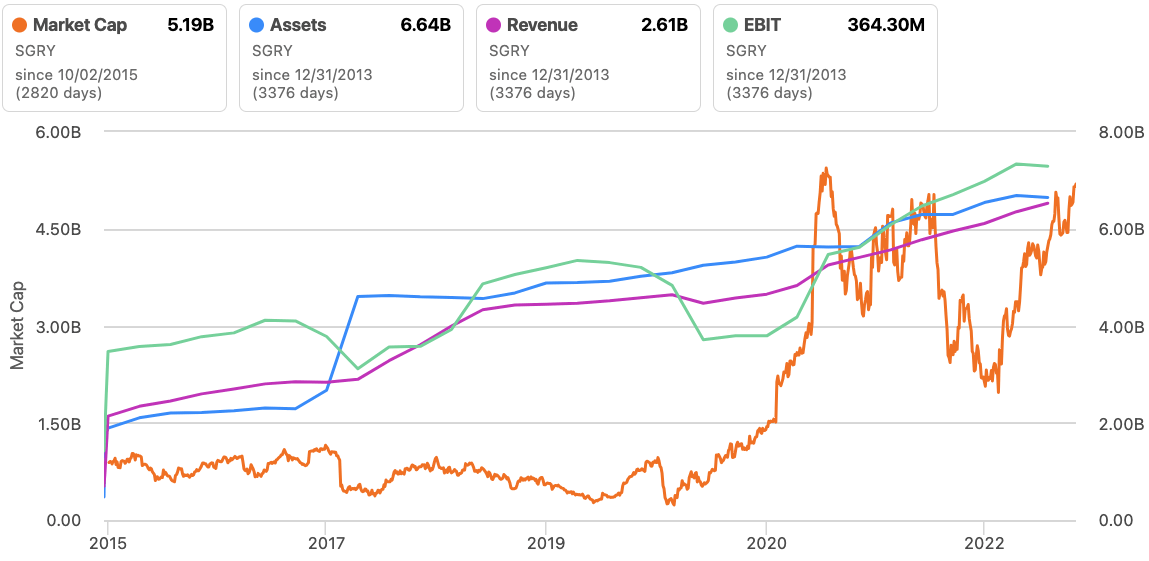

I would suggest this is important because the market has only now caught up with the company's long-term track record, in terms of sales, earnings power and asset factors. As you will see below, on a composite of these 3 factors:

- SGRY was "undervalued" for the good part of 5 years in my opinion.

- The Covid-19 rally was kind to the company, where it revalued from ~$466mm to >$5Bn. After a large drawdown period, spanning the good part of 3 years, we are back at that level once more.

The company expects $2.75Bn in revenue this year on adj. EBITDA of $430mm, or 13% YoY growth. My assumptions have the company doing $3.8Bn at the top-line this year, pulling this to $392mm in operating income [Appendix 1]. Note, my assumptions do not bake in the $100mm headwind management project from its divestitures this year. Should this be factored in, then I am in line with management. Hence, it would be more accurate to say that I am looking to a number $2.75-$2.85Bn for SGRY in FY'23.

Figure 2.

{kind=link}

2. Economic characteristics

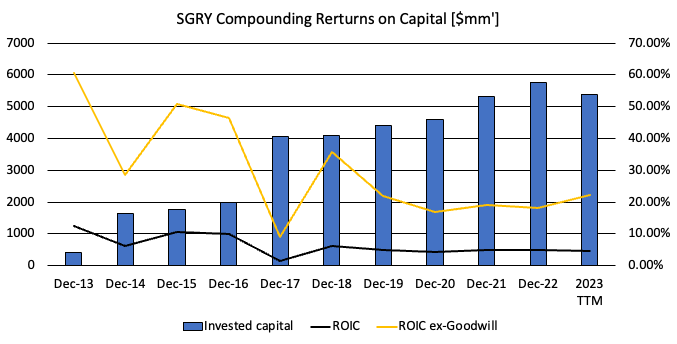

It is within this domain that I observe the greatest investment proposition for SGRY. The company has had no difficulty meeting its capital charges, and then some over its lifecycle. The returns it has generated on its investments have outpaced the market return in equal standing. By all means, I estimate these forces of capital appreciation to remain in situ.

It depends on how you define capital invested in this instance. If you include goodwill --a non-operating asset, that represents a premium paid above the assessed fair value of an asset-- the returns aren't as jazzy. You're talking 4-5% in the TTM, with no change on this since 2018. Goodwill also represents the transfer of shareholder wealth from the acquiring firm to the target firm. Arguably, therefore, it should be included.

On the other hand, goodwill is a non-operating, non-cash asset, that is subject to impairment (non-cash) charges. It is not amortizable and thus has no direct bearing on earnings. Arguably, it should not be included- it produces no operating income, directly speaking. There is, of course, economic goodwill, but this is not discussed here.

My assumptions on SGRY do not include goodwill in the calculus in this case, for the above reasons. The difference in ROIC with and without the goodwill charge is noted in Figure 4. It is a marked spread. To contrast- with it included, the returns are ~4-5% as mentioned. Looking at ex-goodwill, the company has produced a consistent stream of 20% return on existing capital per year since 2018.

These are tremendously attractive economics. At a 12% hurdle rate (long-term market average) you're looking at an 8% spread above the market return on capital, which, over 5 years, cumulates to 40%.

Figure 3.

{kind=link}

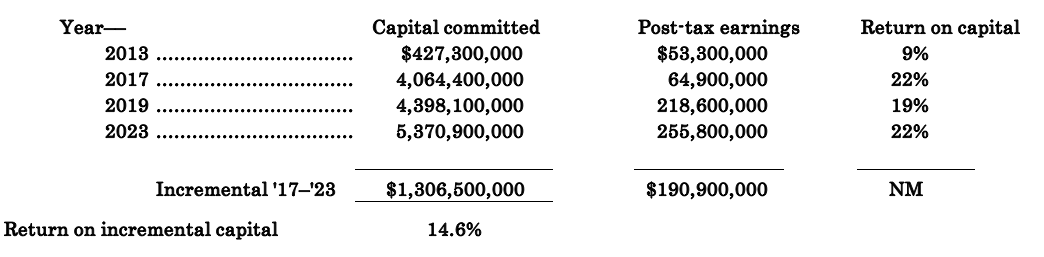

Just how attractive exactly is seen below. You can see the change in capital invested over the testing period. Note the following critical facts:

- Very important to my investment criteria is what we see in the "Return on capital" column. Note the general increase in capital productivity over time, with returns produced on its operating assets increasing from 9% in 2013, 19% in 2019, and 22.2% in the TTM.

- Since 2017, that equates to an additional $190.9mm in post-tax earnings, off of an incremental $1.3Bn investment.

- Therefore, in combination with the returns on existing capital outlined above, the company has produced an additional 14.6% gain in profitability from the capital its put to work since 2017.

Consequently, we are left with a company that invests at c.20% return on capital, whilst producing an extra 10-14 points of profit as it commits more investments to grow the business.

Table 2.

{kind=link}

Forward estimates and valuation

Of course, the investor of today is not paid for yesterday's successes. It is what lies ahead of SGRY that matters. Two things on this- First, my numbers are conducive to a period of growth going forward. I am calling for $2.8Bn at the top line in FY'23, stretching to $3Bn the year after [Appendix 1]. I would see it doing $392mm in pre-tax income, as mentioned earlier.

Furthermore, I wouldn't be surprised to see the company pushing forward with another $100-$290mm annual investment over the coming 3 years, especially with the planned divestments it has for this year and next. Should SGRY hit its trailing ROIC numbers of c.22%, it could grow post-tax earnings by another $22-$64mm. Hence, I believe it can do $356.6mm in after-tax profits this year or $2.84/share.

Figure 3. Note planned divestitures for FY'23

Data: Author

The stock is trading at 22.8x forward EBIT and this is ~35% premium to the sector. It is also catching 2.07x book value, again another premium. Hence, those tied to a mandate or comparing to a benchmark may not see the kind of value I do here. At 22x forward my FY'23 earnings estimates of $2.84 (earnings defined as post-tax operating earnings) this gets me to $62.48 per share in equity value, or 54% return potential on the current market price.

Discussion

A combination of fundamental drivers, attractive economic characteristics and potential valuation mispricing has me very constructive on SGRY. The company is a "slow grower", being that it has its roots entrenched as far back as 2004, or nearly 20 years ago now. But that doesn't mean the investment value doesn't grow. Au contraire, on an intrinsic valuation basis, SGRY has compounded earnings and asset factors for the last 5-years at least.

Given the multitude of factors discussed here, there is good reason to believe these trends can continue. For one, it will have a splash of cash from its planned divestitures this year. It can put this capital to work, where it has historically obtained 19-22% return on existing capital since 2017. Two, the company's unit economics are ratcheting higher in support of this. You see this evidenced in its Q1 numbers, with the surge in surgery volumes and new surgeons added to its books. Finally, SGRY has shown itself as an effective operator that can generate long-term shareholder value. That inspires confidence in my investment cortex, exuding a smile on the face of this happy investor. Net-net, rate buy at $62.50 price target.

Appendix 1. SGRY forward estimates

{kind=link}

For further details see:

Surgery Partners: Exceptional Business Economics, Trading Below Fair Value