USVM - Surging Interest Rates And Inflation Result In The Worst Year For Stocks And Bonds In Decades

Summary

- Stock and bond market returns were strongly negative in 2022.

- The S&P 500 Index fell 18%, its worst calendar year decline since 2008 and the 4th worst since 1945.

- Bond markets recorded some of the worst declines in history. Major benchmarks for both stocks and bonds declined together for the first time since the 1960s.

Stock and bond market returns were strongly negative in 2022. Multi-decade highs in inflation combined with historically aggressive Fed rate hikes and growing concerns about corporate earnings and a possible recession, pressured both stocks and bond market returns.

The S&P 500 Index fell 18%, its worst calendar year decline since 2008 and the 4th worst since 1945. Bond markets recorded some of the worst declines in history. Major benchmarks for both stocks and bonds declined together for the first time since the 1960s.

2022 Returns for Two Index Funds

Fortunately, longer-term returns are still positive.

According to the New York Times , “The year saw the end to an era of low interest rates that made borrowing cheap and encouraged investors to take risks — on the stocks of new tech companies, in cryptocurrencies and in debt markets — in the hunt for lucrative returns.”

Large technology stocks underperformed, a reversal from previous years.

Stock market declines were below-average for a Bear Market but bond market declines were unusually high. The most commonly used bond index, the Bloomberg U.S. Aggregate Bond Index:

- Suffered its worst decline in at least 40 years.

- The 2022 decline was more than four times higher than the previous worst decline in the last 34 years.

- 2021-2022 was the first time it declined in two consecutive years.

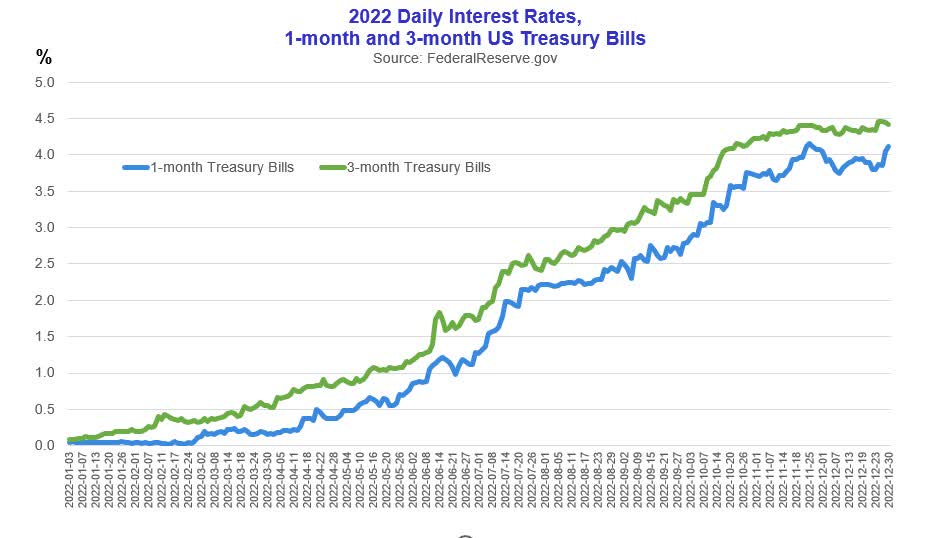

The major cause of the bond market decline in 2022 was the Federal Reserve’s campaign to increase interest rates to fight inflation. The resulting increase was the most rapid in history.

One month Treasury Bill rates were 0.05% at the beginning of the year and 4.1% at the end. Other bond yields also increased. Prices of existing bonds decrease when interest rates increase, which is why bond funds declined.

{kind=link}

How Declines Affect Investors

Stocks were down, bonds were down; so, investment accounts were down. The consequences for investors depended upon their need for investment income.

Retirees making withdrawals to supplement Social Security and pensions were negatively affected:

- The investments being sold to generate needed cash had declined in value.

- Selling low meant more shares had to be sold to generate the same dollar amount of income.

- Paper losses became real losses.

- The opportunity for those investments to recover and increase in value was lost.

For retirees who didn’t need investment withdrawals, the losses only existed on paper (ok, computer screens). They could afford to ignore the declines now, hoping for better future performance.

Those still investing benefited from the lower prices for funds (and individual bonds and stocks).

- They received more shares of funds for the same dollar amount invested.

- If the investments increase in value in the future, their rate of return will be higher.

- Most investment funds generate income from either interest or dividends and, potentially, capital gains. Usually, the income generated is reinvested in the same fund. When fund share prices decline, a dollar of generated income buys more shares at a lower price. There are then more shares to increase in value in the future.

Interest is the major source of return for bonds. The face values of individual bonds (with a few exceptions) do not increase over time. Bond values fluctuate after they are issued and until they mature. But when a bond matures, it is only worth its original face value. The profit from holding a bond primarily comes from the interest generated by the bond, as illustrated below.

According to Vanguard, “… it’s important to remain focused on the long-term benefits of higher rates. Bond total returns have two main components: price return and return from income. Changes to interest rates cause these two components to move in opposite directions. Medium- to long-term investors should care more about bond total returns instead of the negative short-term impact on bond prices. In fact, as we show in the chart, the long-term performance of bond investments has come mostly from income return, not price return.”

Tax Loss Harvesting

“Tax Loss Harvesting” in taxable accounts (Tax Loss Harvesting is not possible in IRAs) was another potential benefit from the 2022 market declines. The goal of Tax Loss Harvesting is to reduce taxable income by selling investments that declined in value. It is. That generates capital losses which may reduce net taxable capital gains. The result is a reduction in taxes on capital gains.

If long-term losses exceed long-term capital gains, up to $3000 can be used to reduce ordinary income on your tax return and any remaining long-term losses can be used in future tax years.

In addition, if sales are timed correctly, fund shares may be sold before end of year capital gains distributions from mutual funds or ETFs. Another tax saving.

Our clients did not invest with us to generate losses for tax purposes. They are looking for long-term gains. However, periods when stocks and/or bond investments lose value are a normal part of market cycles. When those losses occur, we look for opportunities to benefit investment clients and Tax Loss Harvesting is one of the potential opportunities.

This is a complex area of tax law. Please discuss with your tax advisor. We are not authorized to give legal or tax advice. Consult your tax advisor regarding any tax implications and your attorney for legal implications. Your unique circumstances must be considered before applying general investment strategies to personal finance.

What Now

Of course, holding stock investments during market declines only makes sense if we assume that prices will recover. That is not guaranteed. Past performance is no guarantee of future performance.

Historically, for investors who did not sell during a downturn, future performance was sufficient for investors in well-diversified and well-managed portfolios to come out ahead. Bear Markets (declines of 20% or more) were bad but Bull Markets (gains of 20% or more) were sufficiently high enough to offset the Bear Markets and reward patient investors.

Bull and Bear Markets, 1926-2022

Since 1926, for the S&P Dow Jones Indices of US stocks,

- The average decline during a Bear Market was 37% but the average increase during a Bull Market was 362%, almost ten times higher.

- The average length of a Bear Market was 1.2 years but the average length of a Bull Market was 6.7 years, five times longer.

That does not mean markets will recover in 2023; declines may last for years. But, historically, long-term investors were compensated for holding stock investments during market declines.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Surging Interest Rates And Inflation Result In The Worst Year For Stocks And Bonds In Decades