ABT - Surmodics: Regulatory Fundamental Catalysts Show 90% Upside Potential

2023-06-22 16:37:26 ET

Summary

- In November 2020, I rated Surmodics as "one for the future".

- The "future" has arrived, and there are now several catalysts driving SRDX's prospects higher, discussed in detail in this report.

- Based on the latest investment findings, I reiterate that SRDX is a buy, with a revised objective of $57 per share.

Investment Summary

The stage has been set for a potential re-rating of Surmodics ( SRDX ) stock, with three recent catalysts adding a fresh impulse to the investment debate. Two are centered around the conversion of its pipeline, confirming the monetization of its R&D investments in times gone by. Further, there are sentimental factors, with a number of revisions to the Street's targets by analysts in the last few months.

In November 2020, I rated SRDX as a buy, citing it as "one for the future", with a bunch of catalysts at the time. After a strong short-term rally, gains were clipped leading into the bear market of 2022.

This report will delve into the implications of each regulatory catalyst, and provide links to adjacent moving parts governing the SRDX investment debate. Based on the latest investment findings, I reiterate that SRDX is a buy, looking to a revised objective of $57 per share with the latest catalysts.

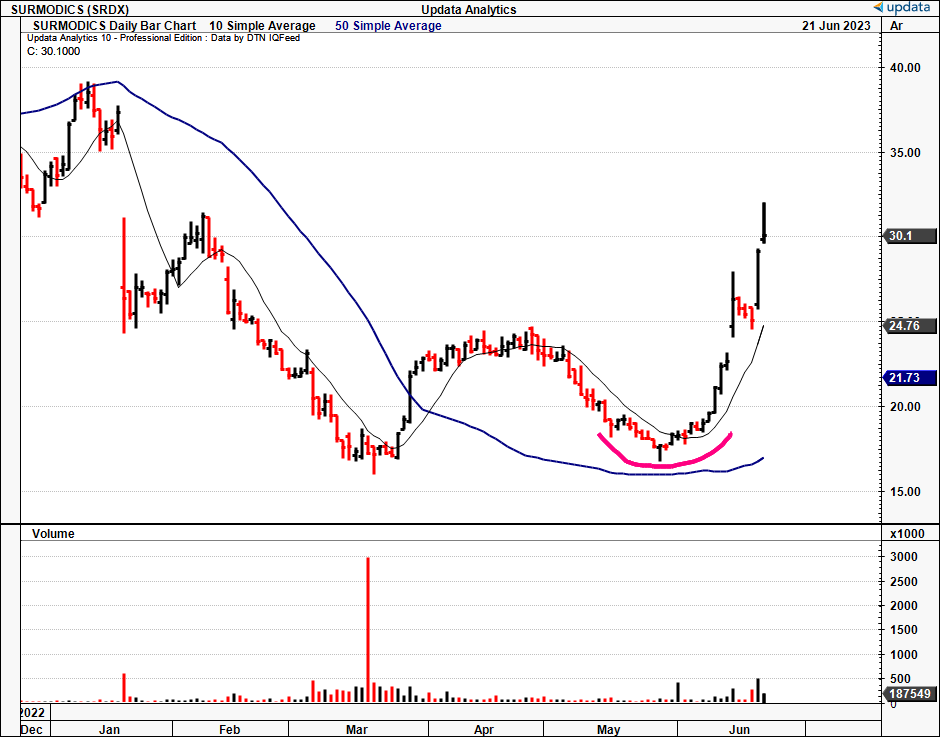

Figure 1.

{kind=link}

Critical facts underlining buy thesis

First, principles investing involves a rational discussion of what the drivers of equity value are, and then ranking these in order of importance, based on the individual circumstances at hand (industry, company, etc.). These ought to be grouped into fundamental, sentiment, and valuation-based factors, based on the aggregate of available drivers of market returns.

For SRDX, in my view, the order of importance matters - here we have a company with major updates to its investment view after the regulatory updates about to be discussed. It stands to reason, therefore, that the weighting would tilt towards the fundamental and sentiment categories in valuing SRDX.

Fundamental Factors

1. Regulatory momentum

SurVeil DCB U.S. approval

- Just this week, SRDX hit a major milestone in its growth journey. The FDA approved its SurVeil drug-coated balloon ("DCB"), which is a large tailwind in my view. This follows the firm's CE Mark approval in the EU in June 2020. As a result, physicians in the U.S. can now actively market and sell the SurVeil DCB for percutaneous transluminal angioplasty under certain patient/procedure criteria.

- Designed to treat peripheral artery disease ("PAD"), in my informed opinion, the SurVeil DCB is a direct representation of the advancement of medical technology we've achieved as a human race. Its standout feature is the "proprietary drug-excipient formulation", that ensures a durable balloon coating during the procedure.

Image 1. "The SurVeil™ drug-coated balloon"

Data: Surmodics TRANSCEND trial resources

- Moreover, the SurVeil DCB's manufacturing is centrally focused on enhancing coating uniformity, which seems to be an issue with these balloons according to my research. Further, SRDX isn't the only one at the DCB game. Competitors include TriReme Medical with its "Chocolate Touch" balloon catheter and Concept Medical with its MagicTouch ED and PTA lines. Concept has an extensive line of DCBs already in existence.

- Abbott ( ABT ) holds the exclusive global commercialization rights for the SurVeil DCB. This is terrific for SRDX in my view. The licensing deal allows ABT to do all of the heavy lifting for the company on the market, by leveraging its deep customer networks, and extensive marketing capabilities. Meanwhile, SRDX will manufacture the product and receive a profit share. This also includes a $27mm milestone payment. It is expected that Surmodics will recognize approximately $24-$24.5mm of revenue related to this milestone payment in its fiscal Q3 FY'23 (the upcoming quarter).

Pounce LP clearance

- Adding to the momentum, the firm announced it obtained regulatory clearance for its Pounce LP Thrombectomy system ("PLP"). The PLP is designed to remove thrombi and emboli (blood clots) from the peripheral arteries, with a major focus on below-knee clots. Here, it has shown capacity in the treatment of acute limb ischemia ("ALI"), which could be a differentiator in my opinion, because it is said that 16% of all case volume in vascular surgeons' books are related to this issue.

- ALI is a critical medical condition shown by a sudden and alarming decrease in arterial perfusion - blood flow - to a limb, typically the lower leg. The over-saturation of blood threatens limb survival, and therefore, it is considered a medical emergency.

- Typically, ALI is the downstream result of things like cardiac dysrhythmias or pre-existing peripheral artery disease. Disturbingly, ALI is associated with 30-day amputation rates as high as 30% and mortality rates of approximately 11.5%, the company says.

In my opinion, the FDA approval of SurVeil DCB and the clearance of the PLP mark significant breakthroughs in the firm's readiness to accelerate growth. The market has taken notice too and revised its expectations on the company (discussed later).

2. Financial results

The firm clipped its Q3 FY'23 numbers in April, giving us enough time to digest the market's appraisal of the results. Prior to the latest swing in SRDX's price (spurred on by the factors above), the stock was tacking at a fairly low range, suggesting pessimism in the fundamental outlook. It booked a 4% YoY increase in total revenue, printing $27.2mm for the quarter. Medical device sales deserve special mention in that regard, up 23% YoY and underlining the growth period. It was nice to see PLP contributing to this upside, along with the firm's Sublime Radial platforms.

Royalty and license revenue slipped back ~4% YoY to $9.4mm. Around 200bps of the decrease in royalty revenue was from a reduction in performance coatings. The other 200bps was from the high comps last year. Moreover, license fee revenue saw a decrease of ~ 9% due to the timing of revenues booked on the income statement under the SurVeil agreement with ABT.

Moving down the P&L:

- Gross margin decreased ~80bps from 63.4% in the prior year period to 62.6%. The margin was compressed by manufacturing inefficiencies as money was spent on ramping up the production of its new products.

- Looking to the operating line, the medical device business reported an operating loss of $7.1mm as it continued to invest in additional sales reps and other growth capital.

- The IVD business clipped an operating profit of $2.6mm, which is a decent gain on last year. The IVD business's contribution margin accounted for 49% of the IVD revenue in both Q3 this year and last. Hence, you would be best keeping a very close eye on both segments going forward (don't isolate one) as the revenue clip is evenly split between both.

Sentiment factors

As confirmation of the market's positive reception of these two fundamental drivers (regulatory momentum, financials), analysts have upwardly revised their forward revenue targets four times in the last three months, with no downward revisions. Consensus estimates indicate 17% YoY growth in revenue this year, with an 87% improvement in earnings (although still creating a loss). However, the fact that analysts are revising expectations higher is a bullish factor on the sentiment side of the risk-reward calculation.

Further, speculators are demonstrating their bullish positioning in SRDX with options demand on August contracts at a strike of $55. The majority of demand is centered around the $55 mark (aside from the $30 strike) and there is hedging activity on the other side of the ledger. If actual investors (not just commentators, as above) with skin in the game have actual positioning out to August at $55 - $25/share gain on current value - it would appear the market is overwhelmingly bullish, in my view.

Finally, the stock is trading above all moving averages on all the respective time frames (10, 50, 100, and 200-day averages, respectively). These are key "psychological levels" and the fact we've got SRDX above these is telling of the price investors are willing to pay to buy the company at the moment, "above the average" price over these periods. Collectively, this is bullish in my view.

Valuation factors

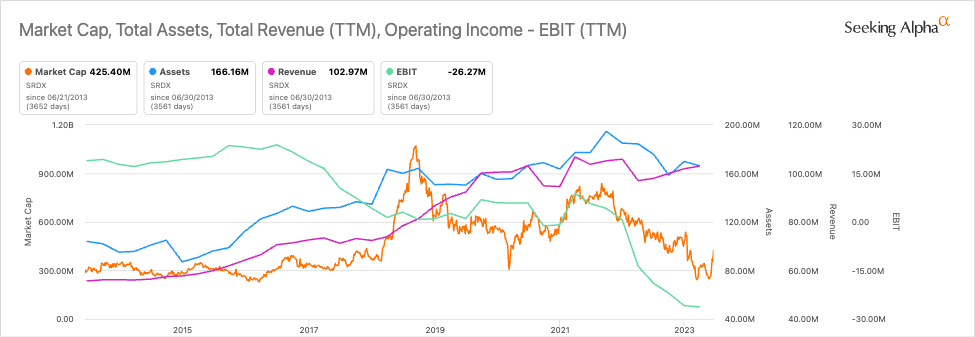

The stock is difficult to value on relative terms given the lack of earnings. It does trade at 3.6x forward sales and 4x book value, however. Further, the market looks to be valuing the company in terms of pre-tax earnings, versus asset or sales factors (Figure 2). Hence, the recent gains in market value imply the market expects a higher growth outlook for SRDX going forward.

At the current market cap of $411mm, assuming a 12% discount rate, the market expects ~$50mm in pre-tax earnings from the company, a major turnaround from its latest numbers and long-term ranges (49.35/0.12 = 411). Alas, the revision in market cap may bake in another $50mm in pre-tax earnings for the company over the coming 3-5 years. I believe this is bullish, and has scope to rate higher with the company's FY'22 numbers.

I believe SRDX deserves to at least trade in line with the sector given the revised prospects in the debate. That would call for a 16x forward multiple on the $50mm, valuing the company at $57 per share in equity value. Note, this is very similar to the options-based 'valuations' listed earlier, further supporting a buy rating.

Figure 2.

{kind=link}

In short

In my view, investors should consider maintaining a positive outlook on SRDX in the future. The updated expectations indicate significant growth potential, which the market anticipates. Based on my analysis, I estimate the company's value to be $57 per share. Recent regulatory and financial catalysts, as well as positive changes in sentiment, support the possibility of this valuation change and attracting significant investment. In conclusion, I still believe SRDX is "one for the future" as before. Reiterate buy.

For further details see:

Surmodics: Regulatory, Fundamental Catalysts Show 90% Upside Potential