SSSS - SuRo Capital: The Valuation May Provide Some Margin Of Safety

2023-08-11 14:58:35 ET

Summary

- SuRo Capital's portfolio has experienced a significant drop in valuation, causing the stock to trade at a 45% discount to its book value.

- The portfolio is concentrated in around 10 companies, mostly valued at EV/Sales multiples that are now well aligned with the market average/consensus.

- The upside potential lies in multiples expanding again due to the Fed cutting rates, with an estimated potential upside of 57% - 110% from the current price.

SuRo Capital ( SSSS ) has a portfolio of private and public tech and innovative companies that have been subject to a bloodbath of valuations contraction. In the last year, the company saw a drop of more than $100 million (roughly 50%) of the fair value of their investments. This is why the stock is down 35% in the last year and currently trades at roughly a 45% discount to its book value.

However, we believe that the current levels offer an interesting margin of safety given: (1) the reasonable multiples used for evaluating the portfolio companies, (2) the substantial amount of cash and treasuries, and (3) lower interest rates on the horizon.

Overview of their portfolio and the valuations

The bulk of SuRo’s portfolio is concentrated in around 10 companies, which represent around 60% of the total value of their investments. The biggest one is Learneo, an online course and education provider.

SuRo Portfolio Investments (SuRo 10-K)

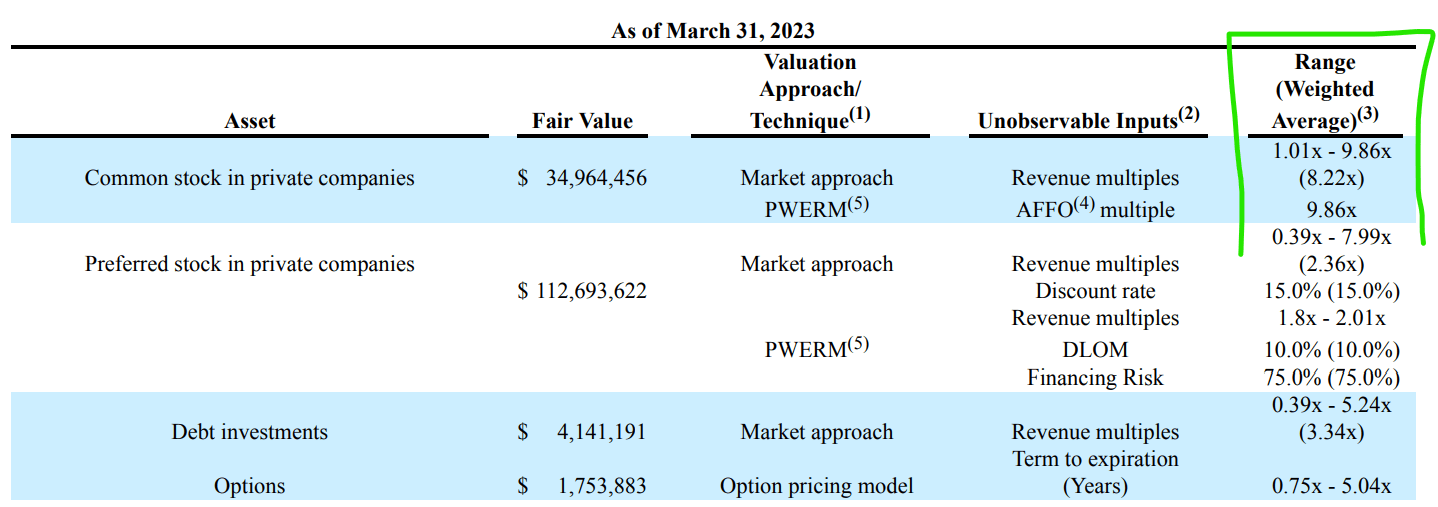

These investments are valued at “fair value”, and since there is no open market for the majority of these companies (very few are listed), there is a need for Level 2 and Level 3 assets value computation. This means using certain inputs and assumptions to calculate the fair value number. This is what SuRo’s assumptions look like:

{kind=link}

Valuation Methods (SuRo 10-Q)

The range gives us a perspective on where these stand on average across the overall portfolio. We are comparing these values with the total market average for software companies that have similar characteristics: private, growing fast, and usually unprofitable.

Valuation multiples (microcap.co)

According to microcap.co, the multiples across different companies' sizes are very close to SuRo’s inputs. We see a 2.6x multiple for a market cap between $100-200 million, which goes down to 2.3x for all the other companies. Comparing this to the 2.36x of SuRo’s preferred shares in private companies, we think that it is properly valued and subject to limited idiosyncratic risk. So while the systemic risk component is still high (rates going up forcing multiples to go down further), the specific risk of SuRo’s having overvalued assets in their book is limited.

The upside may lie in a simple scenario: multiples expanding again as a result of the F ed cutting rates and inflation cooling down. This is basically what the Nasdaq and the tech stocks valuations have been calling since January, and it may actually happen. The first benefits would actually be seen if SuRo’s PortCos are IPOed at generous valuations, allowing for a nice exit and some cash gains in their portfolio.

We think that the overall upside is represented by multiples going back to the 3-3.5 times sales range, which means cash gains greater than $50 million on their $112 million portfolio that is valued using EV/Sales.

A closer look at the risks and the (maximum) downside

To further put a number to fix the downside case for SuRo we want to provide a quick liquidation case analysis. We are going to take all cash and safe securities such as treasuries and subtract all cash liabilities. This is an overview of the analysis:

Liquidation Analysis (SuRo Filings - Author's analysis)

We can assume this as the lowest possible recoverable amount per share out of any distressed scenario. It represents a maximum downside of around 75% from the current price of $4 to reach the tangible liquidation value of $0.93. However, this is an apocalypse-like scenario and assigns zero value to all the other portfolio investments. We like to discount the other equity and credit investments down to 40% of the reported fair value by assigning very bad exit multiples that are well below market. For example, using the EV/Sales approach this means multiples below 1.5 times, which is very unlikely for a fast-growing and easily scalable company. This remaining discounted book is valued at around $50 million, or around another $1.80 per share, which brings the total estimated liquidation value to $2.73. If we compare this number to the current price of $4 we see that the overall downside is limited to just 30%.

Recent earnings: in line with estimates, confirming the thesis

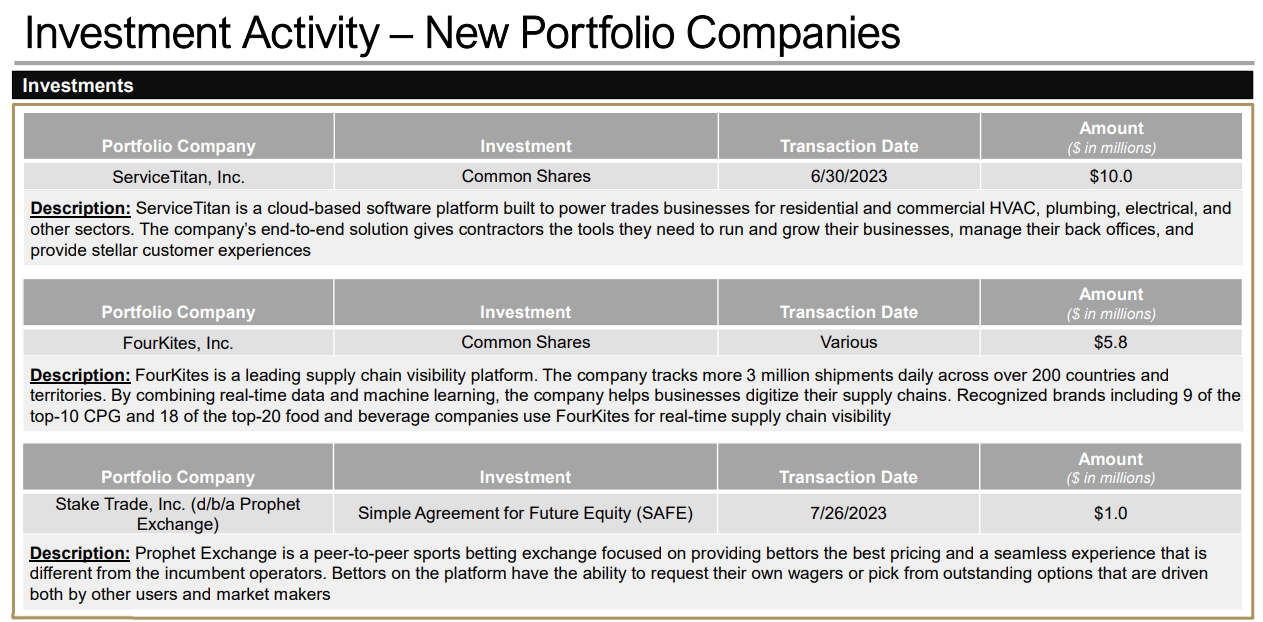

The data we used from the liquidation analysis is coming from the latest earnings. We saw results in line with the Street's expectations, and new investments that confirm that allocation of capital is happening at attractive valuations. We think this can spur the investment of the remaining $100 million of liquidity at much better returns and risk profiles than any previous period from 2018 and beyond.

{kind=link}

This table from their latest presentation shows the new allocation that took place between Q2 and the beginning of Q3. They allocated roughly $18 million and we believe that given the current state of the VC space, these deals took place at very conservative EV/Sales or EV/Adj EBITDA multiples.

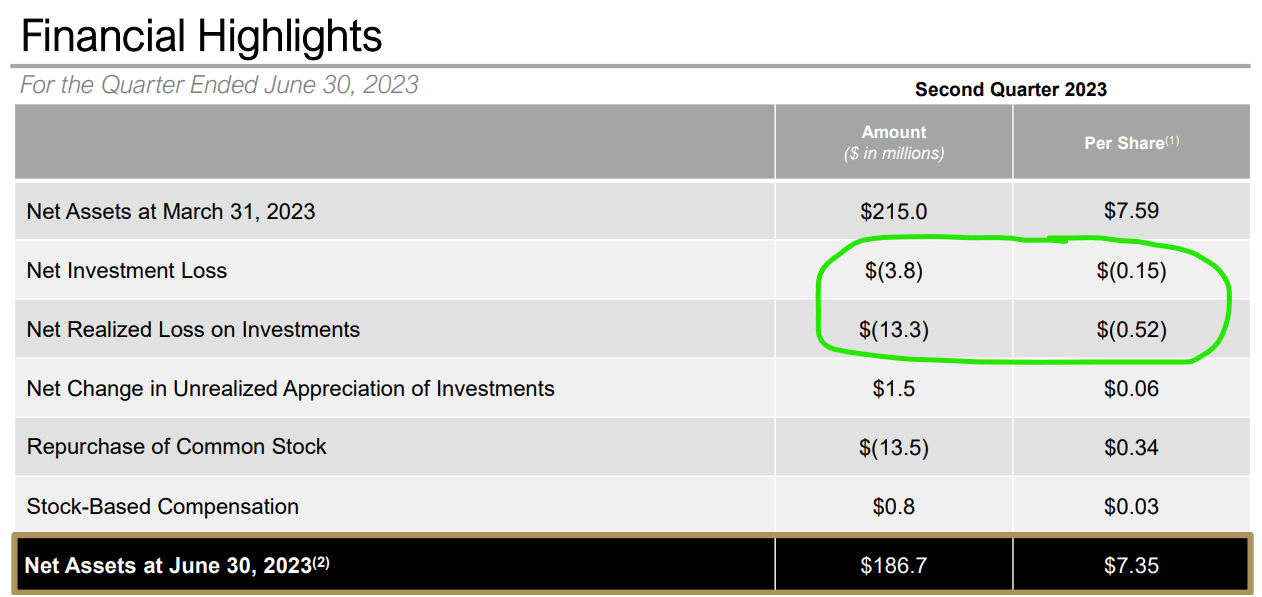

To give a look at the overall realized and unrealized gains and losses, we can see the following developments.

{kind=link}

The company is clearly continuing to write down investments and match the valuations in its portfolio with the overall market environment. This shows an incentive in remaining aligned and not trying to "pump" the value of their portfolio and NPV, increasing our confidence in the analysis.

Possible valuations and SuRo’s dynamic fair value assessment

As we have no magic sphere that looks into the future, we do not want to give a specific forecast on what the entire software industry EV/Sales multiple will look like in a year or two. However, we are also conscious that this weighs a lot on SuRo’s value and share price. We thus decided to present SSSS fair value as a function of a dynamic (changing) overall EV/sales multiple, which seems to be the single biggest factor affecting their portfolio’s fair value. It looks like this:

Valuation analysis (Author's estimates)

The fair value per share ranges between $3.70 with a multiple of 1x, and $11 with a very generous multiple of 5x, which is close to 2021 levels. We want to remain conservative and expect a median outcome between $6.30 and $8.44, which represents an upside of 57% - 110% from the current price. This will change based on the overall market environment but aligns well with the limited downside of around 30% based on the liquidation value assessment.

Conclusion

We believe that SuRo is an interesting opportunity because its portfolio is currently being deeply discounted by the market, and the liquidity provides an interesting limit to the downside. The inputs to the valuation models used to compute the fair value of their investments seem reasonable, and we think there is considerable upside to capture in the case of an overall re-rate of the market/sector.

For further details see:

SuRo Capital: The Valuation May Provide Some Margin Of Safety