SUZ - Suzano Still Benefiting From High Pulp Prices

Summary

- Pulp price increases in Q4 are ahead of cash cost increases, and with solid volumes that means profit growth continues for Suzano.

- This was not expected, especially since Chinese packaging demand fell due to COVID-zero throughout the year.

- It all comes down to supply still, and China's lockdowns do have to answer for that, as well as shifts from Russian timber.

- Pulp prices are coming off highs a little now, but not much. Still, it is sensible to expect further pressure as it is a commodity.

- Still, reopening of China flows back with some restored demand which is a positive, and no major capacity can come online until later next year.

Suzano ( SUZ ) continues to defy expectations thanks to very high pulp prices despite expected pressures. Supply is the main determinant of the price situation in pulp, and issues still remain, especially with the lockdowns in China having ended recently. There could still be problems with the Chinese reopening, but for the most part it is sensible to expect the cycle to come to an end as supply becomes more normalized, even though it is likely to come down less dramatically than it rose.

FY 2022 Results

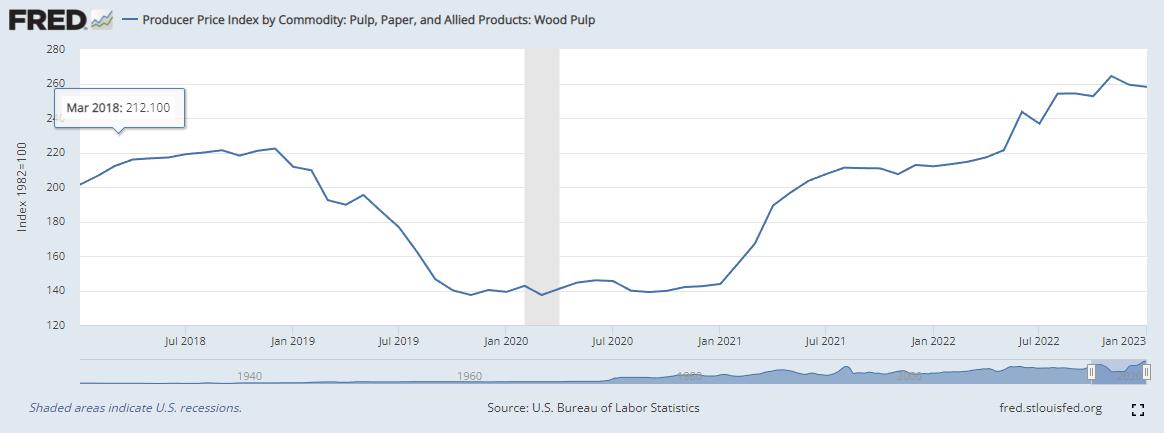

The price of pulp continued to rise even in Q4, which for most businesses came with some sort of slowdown. Prices have come off the highs towards the end of 2022, but they remain high even as of January figures. There are several reasons for the high 2022 prices, and several reasons why prices should come down in 2023 but probably quite slowly. 2024 and onwards is more concerning as new supply comes online.

- Supply chain disruptions from COVID-zero. While China is a major demand sink for pulp, especially as they had to prioritize virgin pulp due to limitations on recycled paper imports, things got stuck in logistics there and a lot of pulp was taken off the market as Chinese logistics couldn't finish off deliveries.

- Russia provides timber, and alternative imports have been prioritized including Suzano's Eucalyptus and Pine pulp.

- Finally, high prices have been permitted to an extent by customers in order to assure supply and be able to secure enough inputs.

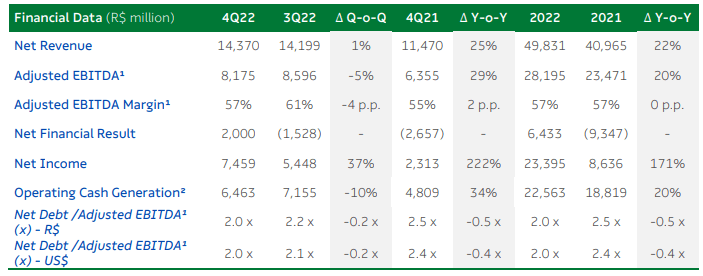

The results were phenomenal as a consequence:

{kind=link}

Cash costs were up almost 25%, but a ~35% increase in pulp price led to the EBITDA growth we see, as volumes were actually very flat.

Prices have come off slightly from highs, but not by much as of January 2023.

{kind=link}

We do expect prices to eventually fall, consistent with the market's commodity multiple view on the company.

- Demand in China has fallen, and this means that once logjams clear up there will be more supply free for Asian buyers, and therefore a negative price pressure.

- While we are getting a reopening in China, it will be slow to recovery to pre-2022 levels, since China is facing many more economic challenges this year and secular outlook deteriorating.

- Global demand in some key paper and packaging markets could become affected by the rate cycles happening in most western economies. Construction paper but also general levels of commerce are at risk of coming down. China, US, Italy, Netherlands and other European countries are all big export markets and are challenged this year due to inflation.

- Resolution of supply chain issues will increase availability and remove the 'hoarding premium' that appeared on some commodities this year due to conservative 2022 inventory management practices. In particular, there is still low inventory of containerboards among clients keeping prices in that important market high. Once this normalizes we could see more threat.

- After 2024, we'll start seeing more pronounced capacity increases, including Suzano's own Cerrado project, come online to bring down prices further.

Bottom Line

There are mitigating factors. Costs have come up for producers, and this means that they'll resist calls to pull down prices of pulp. However, this is only because lower prices actually threaten margins, and this isn't great.

While Suzano's multiple at a 2.4x FWD PE correctly reflects cyclicality in principle, the value appears very low. Suzano's assets are some of the lowest cost in the industry, and when the half-complete Cerrado projects is fully finished, the costs will continue to average down. Moreover, the conditions over the next year or two remain quite favourable, and the multiple isn't likely to rise on falling earnings by too much in that time. Payback periods are very low and achievable here.

However, we think the Lula win in Brazil poses a problem for the industry due to the issue around deforestation. A political discount is likely being placed on Suzano. Moreover, their deleveraging has stopped due to CAPEX on the Cerrado project, which was a great reason to invest in them before. Suzano claims its plantations are green but it's not for us to say or speculate how much the government will heed this. Negatives from regulators could come in even if not aimed at Suzano specifically, even if it is limits on timber harvest volumes and changes in deforestations thresholds.

For further details see:

Suzano Still Benefiting From High Pulp Prices