SI - SVB Financial Group Blowing Up Doesn't Change The Fed's Inflation Target

2023-03-13 04:56:26 ET

Summary

- Rates have been blowing out presumably because SVB Financial Group went down.

- It is perceived as a potential canary in the coal mine.

- The Fed would raise rates until “something breaks” and it looks like the banking system is breaking.

- A logical conclusion seems to be that the Fed will reverse course but I'll argue against that.

Markets broadly are figuring out the second-order effects of SVB Financial ( SIVB ) going down on Friday. The event is widely covered and discussed so I won't go into it. One second-order effect that I think is quite interesting is the rate move. Rates moved sharply higher on Friday on the short end as well as the long end.

Rates markets have traded consistently with the narrative that the Fed would raise rates until "something breaks". The 10-year and long bond have traded all along as if that event would come quite soon and it would force the Fed to reverse course.

Now it looks like the bond market has been precisely right; the banking system is breaking...

Ergo, the Fed will reverse course.

But the Fed has a 2% inflation target they have repeatedly said they will achieve. Should it stop hiking rates because a Silicon Valley bank puts many of its deposits on the long end of the curve, and its depositors are a homogenous group? Maybe banks should stop taking deposits if they can't safely and marginally profitably invest them.

Is the argument really that the entire country should accept 6% inflation because Silicon Valley can't meet payroll in time? I'm very skeptical that this will significantly hinder SIVB depositors. They'll get most of their money back quickly and reasonably quickly. I could see other entities providing capital against SIVB deposits as collateral. I'm skeptical that this, and the Silvergate ( SI ) blow-up (where I was long and wrong ), will stop the Fed.

The event could slow the Fed down; that's entirely probable. I believe this blow-up isn't necessarily an indication of a systemic problem. However, authorities need to establish the fact, leaving no doubts, that deposits are safe no matter where they're held. Otherwise, this opens up the possibility of running to the perceived safest balance sheet, which would again become unstable. In any case, no bank is secure if there are doubts about its safety.

Would the Fed contribute to the notion of a safe banking system by doing an emergency easing round or even pausing the next meeting? Effectively it would be saying; yeah, we're panicking because the banks are cracking. Your money is worthless because banks crack or because it is inflated away.

Let's say the Fed is going to pause the next meeting. Or, as some people are suddenly arguing, lowering rates and flooding markets with liquidity. Historically, that sends markets higher and bonds higher as well.

But this time, Remember the 6.41% inflation. It is 6.41% (down from much higher) after a year of the fastest series of rate hikes in history. If the Fed floods the market with liquidity and starts lowering interest rates AND inflation continues to recede… Then equities and bonds will be boosted again.

Inflation seems unlikely to continue to recede in this 6% environment where the real economy doesn't appear to be doing all that badly yet.

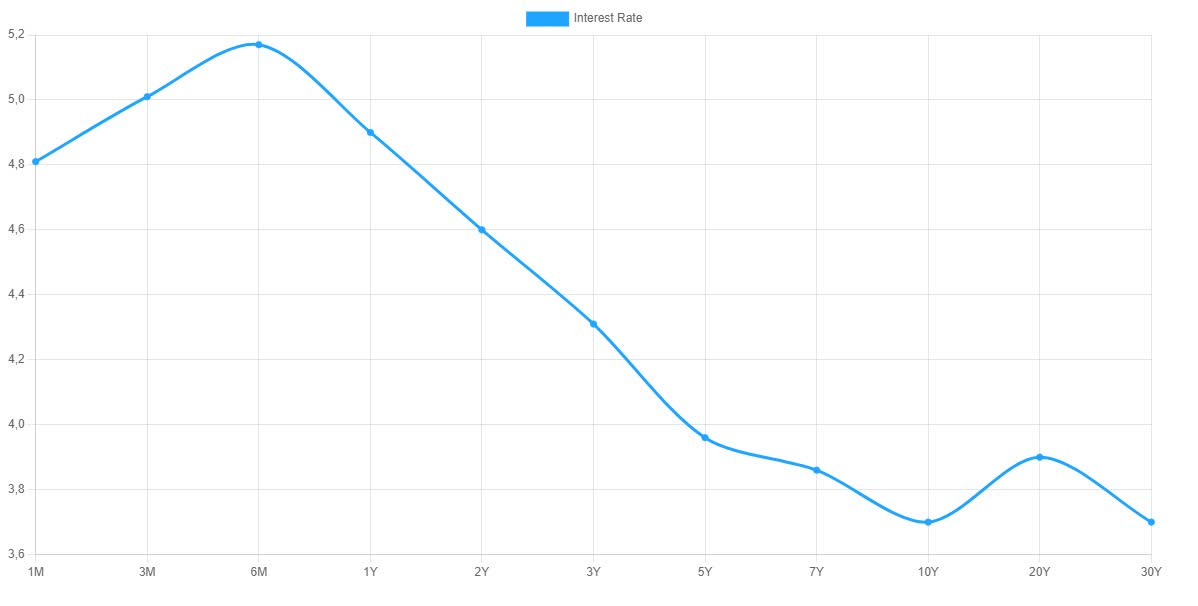

The yield curve looks like this:

U.S. Treasury Yield Curve (UStreasuryyieldcurve.com)

{kind=link}

It has been very flat, even inverted, for a while now. This has been explained (logically) as the market believing the Fed would get inflation under control by cooling down (or pushing into a recession) the economy and inflation would recede.

In this environment, I'm not so sure that the belief that A) The Fed can't hike any further anymore or needs to start lowering rates and B) this will be bullish for bonds make a lot of sense. Yes, it used to be like that when inflation didn't exist. But things have changed:

With inflation at 6% and the Fed (arguably) having to give up hikes, a long bond position looks very painful. An assured way to erode your purchasing power because inflation stays elevated for who knows how long... The alternative is that the Fed continues rate hikes, and long bonds don't do well either.

The only great path (for long bonds) is if the bank failure indicates a recession is here. The recession has to be disinflationary to the extent that rates can be lowered without igniting inflation.

The thing is that I don't see the failure of SIVB as a recessionary indicator. Without any further information, a bank failure is highly indicative of a being in a recession because bank failures often happen when defaults spike and banks take credit losses. But that's not what's happened at either Silvergate or SIVB. I'm painfully aware of how Silvergate failed. Due to 1) fast deposit withdrawals and 2) losses on the securities book. SIVB is a similar story. Both had a mobile and homogeneous deposit base. SIVB combined that with a risky securities book (not dangerous in credit exposure but in terms of interest rate sensitivity). No one forces a bank to take a lot of interest rate risk. The failures result from Fed hikes punishing one form of greed and are not indicative of overall credit risk.

In summary, the Fed can pause for a bit and ensure there's no systemic damage. But soon, the Fed will have to push on with inflation at 6%. Only if we're in a disinflationary recession can it start reversing. I don't think the SIVB failure indicates a recession because it (unusually) doesn't seem to have failed because of credit. The yield curve is inverted, and long bonds aren't yielding that much. Even if the Fed pauses because of systemic issues, but inflation doesn't recede fast, long bonds still look pretty bad. If you think a recession is now very likely, I think the long bond is still in a bad spot vs bills or even the 2-year. I think a short position in the iShares 7-10 Year Treasury Bond ETF ( IEF ) is attractive here. It can also work well with a long position in the iShares 1-3 Year Treasury Bond ETF ( SHY ). I've been short an array of bonds for a while, including the latter, but have been looking for a good time to switch to a long position on the front end of the curve. Many alternative instruments to express these bond positions will work as well. I used these as examples because they are very large and liquid and widely accessible. I wrote another idea for subscribers based on the somewhat indiscriminate fallout Friday. I continue to look for other ideas as there are often short-term opportunities when markets are in flux.

For further details see:

SVB Financial Group Blowing Up Doesn't Change The Fed's Inflation Target