SIVBP - SVB Financial Group Reached For Yield Failed Perhaps A Canary In The Coal Mine

2023-03-13 13:20:50 ET

Summary

- Silicon Valley Bank's failure marks the second biggest in U.S. banking history. The company's balance was so poorly invested, it is beyond words.

- The company, got caught reaching For yield, and a very poorly invested $86 billion of held-to-maturity securities portfolio, invested in long duration and low average yields sunk them.

- This big blow up is a good prompt for retirees, who are invested in high dividend yielding stocks, to re-examine the amount of risk they are taking.

This weekend, we were at a family party to celebrate my nephew's first birthday. Among the various topic discussed, questions surrounding the second biggest bank failure in U.S. history, notably, the failure of the parent company of Silicon Valley Bank, or SVB Financial Group ( SIVB ), were directed in my direction. Here is how I tried to explained it.

SIVB was a bank that catered to venture capitals, start-ups, and emerging technology companies, as well as mid-sized and publicly traded technology companies. The business and its deposits grew rapidly, amidst all of the money printing associated with Covid stimulus programs and the Federal Reserve's big policy errors (keeping rates way too low, for way too long). The vast majority of its funding was in the form of "demand deposits" to businesses. These types of deposits aren't sticky, like the tens of thousands (or hundreds of thousands) of retail deposits, which enjoy $250K FDIC protection. Again, some of these businesses were well-funded publicly traded technology companies and others were smaller and privately held businesses.

Fast forward to Sunday evening, March 12, 2023, and the U.S. government probably did the right thing here: they protected depositors. Yes, the CFOs and start up founders should have been smart enough not to had so much of their cash at SIVB. However, I think even Warren Buffett would agree that deposit holders weren't exactly taking risk (or at least they didn't think they were). They were banking their vital cash, at Silicon Valley Bank, in order to run their businesses, including meeting payroll, funding their working capital needs and investing in their businesses. From reading various WSJ articles, it also appears SIVB made it a requirement to move all of the startups or emerging technology companies assets over to the bank, in exchange for access to credit lines or various forms of debt financing.

Over the weekend, I spent a few hours looking at SIVB's 10-K , and it is simply shocking how inept this management team was. As an aside, I spent five years working, as a Senior Investment Associate, within a group that managed a $45 billion buy-side investment grade bond portfolio. This was for a large insurance company, and although the IG group far and away managed the vast majority of the assets and was the most vital group, within the context of the overall investment department, there were other segments, including a high yield group, a few private equity groups (so think fund of funds private equity investing), direct private equity energy investing (this group was highly success and a very early mover, since the 1990s - mostly in midstream energy infrastructure), a real estate group, a metals and mining group, and a small public equity group. As all members of the investment department got to attend the quarterly investment meetings, I saw first-hand how the senior portfolio managers, the Chief Risk Officer, and company's Chief Investment Officer, spent so much time on duration risk. This was one of the biggest topics and most important aspects of risk management, much more important than credit risks, as credit risk was fairly easy to define, track, and monitor.

Without getting lost in the weeds, as I'm just not sure how many readers will fully grasp all of the nuances here and jargon like Accumulated Other Comprehensive Income ((AOCI)), the risk management function was largely non-existent, at least in practice, at SIVB.

As I could write pages on SIVB, let me try and cut to the chase here and keep this as short as possible.

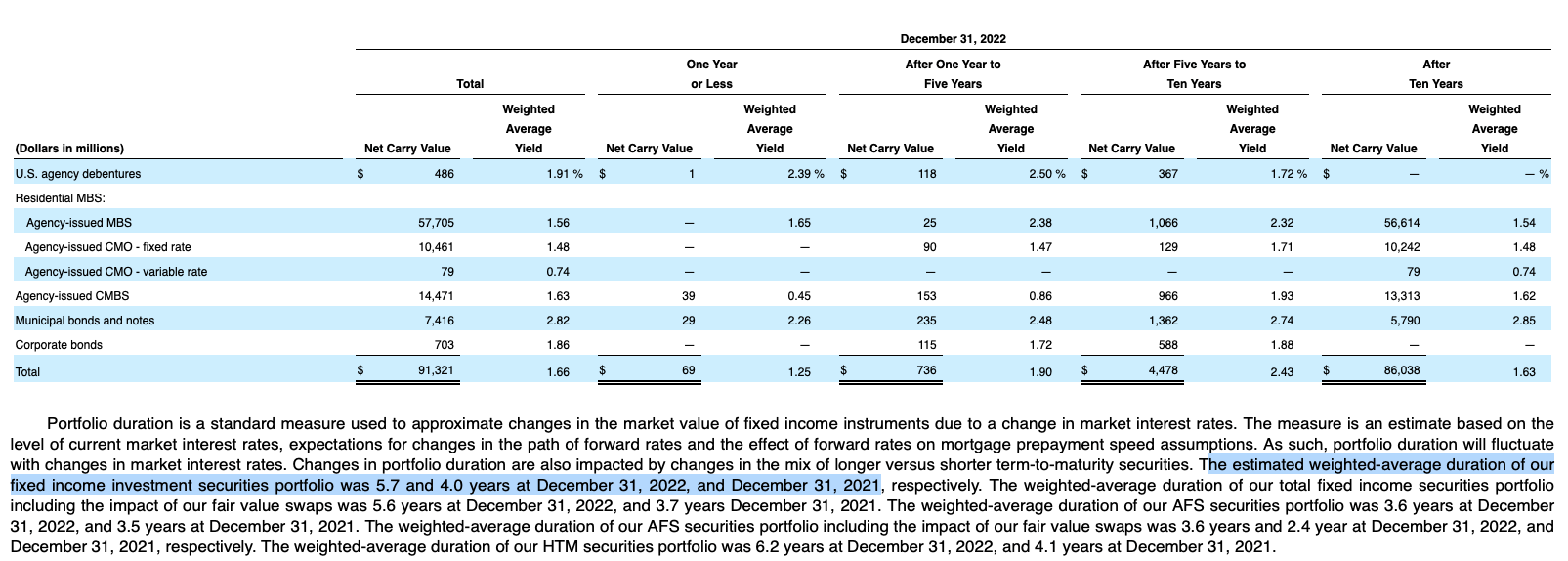

If you look at page 66 of SIVB's FY 2022 10-K, we can see the composition of its "Held-to-Maturity" ((HTM)) Securities portfolio.

Remarkably, $86 billion of the portfolio was invested in long duration securities, mostly Agency issued mortgage backed securities. Per the 10-K, the weighted average yield of these securities was 1.63%!!!

{kind=link}

It is utterly amazing how exceptionally poorly this portfolio was constructed and how utterly inept the management of it was here. During my five-year tenure in the IG bond group, I never got exposure or was tasked with focusing on CMBS, as there were a few really smart portfolio managers, in that group, but I do know principal pre-payment speeds dramatically slow in the face of the fastest Fed Funds Rate increases in history. In other words, of course, and sadly, divorce happens, people move, etc., so people pre-pay their mortgages, as they are forced sellers of their homes. However, when so many people are locked into very low absolute yields on their mortgages, they have no economic incentive to make pre-payments, or move, as new mortgage rates have dramatically increased. This, in turn, extends the true "estimated" and ultimately actual duration of these CMBS securities.

In the written section contained below SIVB's Held-to-Maturity Securities chart, I highlighted how the estimated weighted average duration of SIVB's investment securities portfolio spiked to 5.7 years at December 31, 2022 compared to only 4.0 years at December 31, 2021.

That dramatic jump, notably more so when we're talking about $86 billion here, also meant big mark to market losses. To save the banking system from systematic insolvency, back in 2008/09 the government allowed regional bank a hall pass from running the mark to market losses through their income statement, as long as the bonds/ loans were "held-to-maturity." This loophole remained opened, perhaps much too long and well in excess of its intended original purpose, and now we have the failure of Silicon Valley Bank.

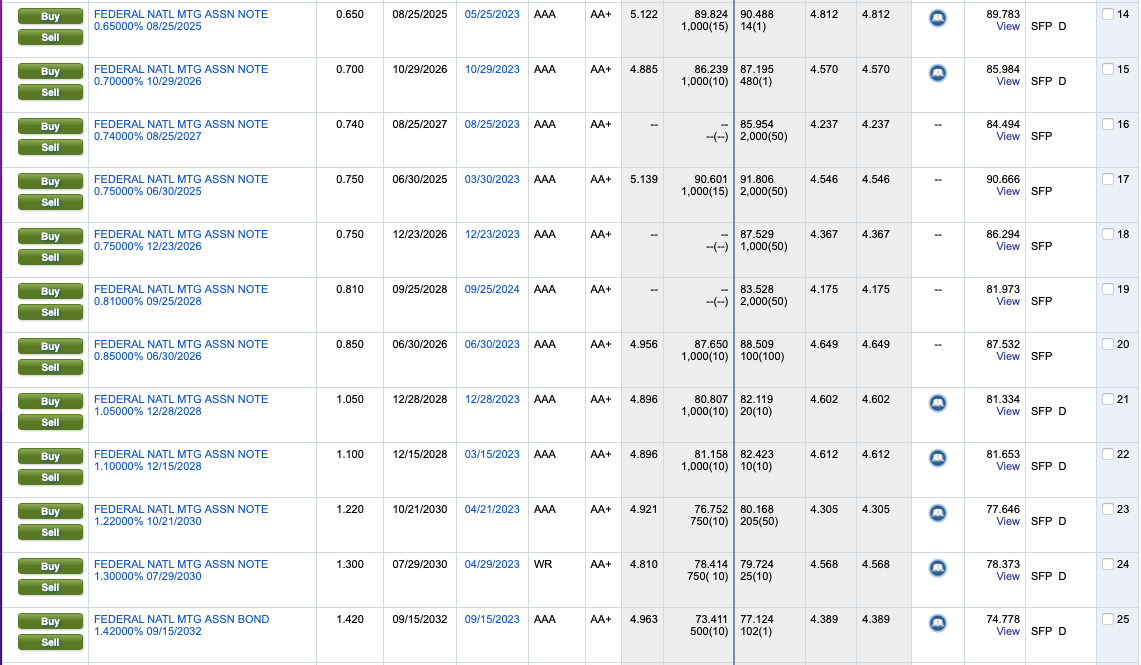

As a quick proxy to what some of these CMBS securities are currently worth, on a mark to market basis, enclosed below is a screenshot, from Fidelity's Agency CMBS inventory, as of Friday's close of business. Again, we don't have access to the composition of SIVB's held-to-maturity securities portfolio, so I just want to highlight, as a proxy, the mark to market losses and provide content.

As you can see, a lot of these low coupon agency CMBS bonds are trading at $0.75 to $0.90 on the dollar. So, using this, again as a rough proxy, if the mark to market value of the portfolio was $0.85 on the dollar, that is about a $13 billion of mark to market unrealized losses ($86.3 billion x 15%, which assumes the bonds were bought at par and are trading for $0.85).

{kind=link}

{kind=link}

So, last week, on March 8, 2023, when SIVB disclosed that the company sold $21 billion of its Available-for-Sale Securities, and crystallized $1.8 billion in losses, which triggered a need to raise equity capital, to replenish its tangible equity capital ratios, this triggered a run on the bank.

Candidly, we know now that the vast majority of market participants were asleep at the wheel here, including most of the sell side analysts, CFOs that banked with Silicon Valley, and notably the SIVB equity, preferred stock, and debt holders. The realization of the AFS losses and, ultimately, failed equity capital raise cast a spotlight on SIVB's 10-K, and the market quickly worked out, once awaken from its deep sleep, that the vast majority of SIVB's funding was "short" in the form of demand deposits, and that its held-to-maturity securities were severely upside down and under water.

Sir Warren Buffett was Right - The Efficient Market Hypothesis Isn't Accurate

It is utterly remarkable how inefficient markets are, and this proves Sir Warren Buffett of Berkshire Hathaway ( BRK.A , BRK.B ) correct, yet again, that capital markets are actually inefficient, whereas Efficient Market Hypothesis ((EHM)) Theory has been the gospel widely disseminated throughout the hallowed halls of so many business schools. SIVB's ticking time bomb of a balance sheet , so poorly constructed, with huge duration mis-match, and such bad common sense (locking in long dated duration at such low absolute yields), was hiding in plain sight. The fact that SIVB's equity was valued at north of $16 billion, just last Wednesday, or $268 per share, kind of proves Sir Warren was right that Efficient Market Hypothesis Theory is really just groupthink by a bunch of academics that have no skin in the game and who are unfamiliar with how markets actually work and move, during period of turbulence (outside of blue sky conditions).

As the damage is now done, SIVB's equity and preferred stock will get zeroed out, and arguably it bonds might only be worth $0.10 to $0.15, if that. As the recovery, in SIVB's bond, if there actually is any, is unknowable, at this point.

The Most Important Lesson For The Seeking Alpha Community - Don't Reach For Yield

As it is unlikely that many readers had any material exposure to SIVB's equity or preferred stock, the biggest lesson that readers might want to consider is "Don't Reach For Yield." Although the vast majority of my bandwidth and intellectual creativity is spent on small cap value and special situation equity investing (and with some calculated speculating sprinkled in), I do really worry about the type of advice retirees are getting. Retirees are a special group in that they can't go back to the workforce if there is some unforeseen financial reversal. By definition, and of course everyone's situation is different, this group has a fixed amount of saving /capital and they are charged with figuring out how not to outlive these assets.

This is a daunting task and something that keeps millions of actual retirees (or folks approaching retirement) up at night. The fear of outliving your money is a strong negative emotion. Lo and behold, and depending on your perspective, the financial industry is enterprising (at best) or has questionable motives (at worst). From a business perspective, there are tens of millions of baby boomers, who during their peak earning years, many of these baby boomers have ridden massive stock market gains and built substantial nest eggs. Most enjoyed massive real estate equity appreciation, and some might even have a pension. As group, this is a very wealthy demographic cohort. However, nonetheless, the fear of outliving their savings is real. Therefore, as a group, there are millions of retirees as potential customers. So whether companies are selling annuities, financial planning, wealth management, or newsletters, this is the largest captive audience and their needs are the most pressing. As a group, they have the ability and willingness to spend money on financial advice, in various forms, as described above.

However, I would argue there is a lot of bad advice out there. Advice that is designed to reassure retirees, but that isn't empirically proven. By appealing to a person's hopes and helping to allay their fears, it is a good way to sell financial products and services. As after all, people want to be told they are right and that everything will be fine.

Sadly, however, I would argue most of it is very unsuitable for most retirees and far more often than not, the risks are understated. Most of the arguments in favor are expressly designed to highlight the benefits and what can go right whereas the risks or what can go wrong tend to be hardly mentioned and glossed over.

As an aside, I personally love risk, as it is how part of how I create alpha, but it is so critical that the risks are well defined, presented and that only real risk takers are the ones actually taking the risks. In other words, people know and understand that amount of risk they are taking in order to attempt to realize higher yields are the ones who should be bearing it.

Well guess what? As of last Wednesday, SIVB shares closed at $267.63, or a $15.9 billion market capitalization. As of today, March 13, 2023, the equity value is zero.

A lot of leverage can and does kill

So as someone who has accumulated some real world fixed income knowledge, over a five year career period, and has a decent grasp of investment grade bonds, I'm shocked at the popularity of high yield dividend investing. I can't believe many retirees would ever even consider, let alone actually allocate more than 10% or 15% (maximum) of their portfolio in high yield dividend stocks.

High yield dividend investing is nothing like investing in Investment Grade bonds. Notwithstanding duration risk, when you are investing in investment grade bonds, you're higher up in the capital stack, so above the equity and preferred investors, and you're contractually obligated to get paid your interest via semi-annual coupons and principal, upon maturity, or the bond holders take over the company. Especially at the investment grade companies, as it takes years to build an investment grade quality business, the management teams get well compensated and a lot of really smart people tend to work at these businesses. Given that these are lucrative jobs, the management teams want to keep these jobs. Moreover, they have a strong incentive to perform, for the equity holders, as that his how they are measured and paid. As bond holders, sitting well above the equity class, you get the benefits and peace of mind knowing that your principal is highly, highly "money good." That said, and I learned this from having a front row seat to the financial crisis, from 2008/2009, as I sat on that $45 billion IG bond desk, I don't invest in financials. Certainly, not the equities, and only very selectively on the bond side. On the bond side, I only invest in the best in class companies, as we own JPMorgan Chase ( JPM ) and Bank of America ( BAC ) bonds.

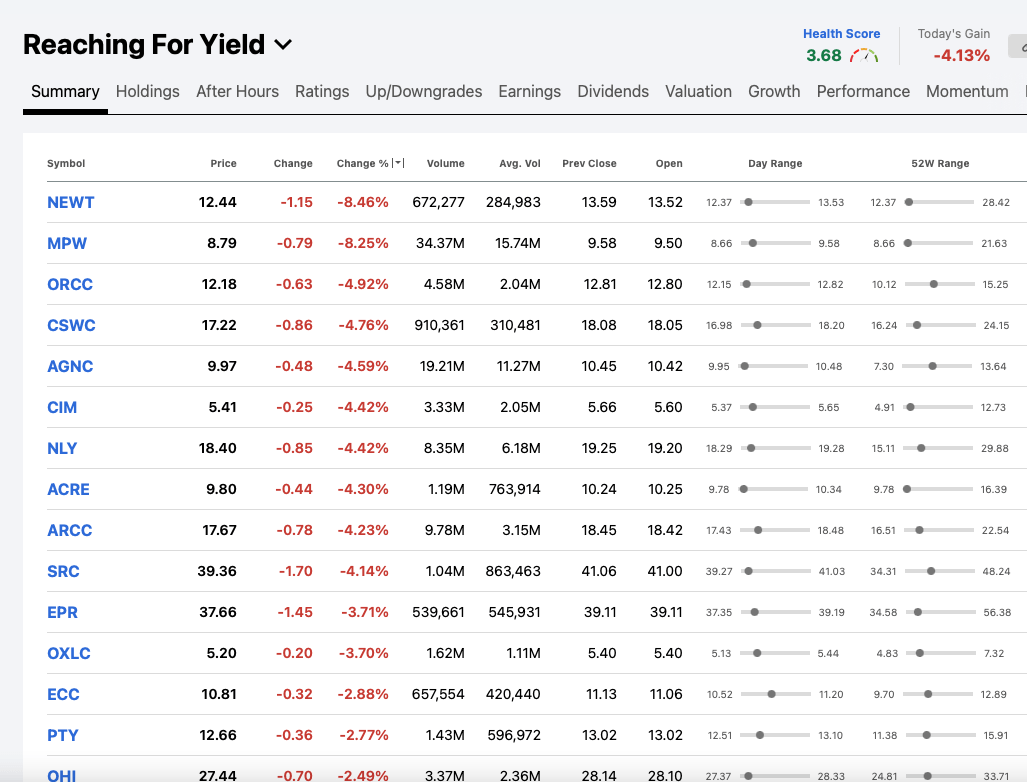

As a very small proxy for reaching for yield, enclosed below is a snapshot containing a small and hypothetical sample size of what I would consider reaching for yield. These stocks are extremely popular among the Seeking Alpha community, and articles about these stocks tend to generate hundreds of comments.

{kind=link}

Please note that number of these stock got beat up on Friday, given the heightened fear surrounding the Silicon Valley Bank failure and the risk of contagion.

Moreover, please note that NewtekOne Inc. ( NEWT ), Medical Properties Trust, Inc. ( MPW ), Owl Rock Capital Corporation ( ORCC ), Capital Southwest ( CSWC ), AGNC Investment Corp. ( AGNC ), Chimera Investment Corp. ( CIM ), and Annaly Capital Management, Inc. ( NLY ), Ares Commercial Real Estate ( ACRE ), Spirit Realty Capital, Inc. ( SRC ), EPR Properties ( EPR ), and Oxford Lane Capital ( OXLC ) were all down at least 3%, for the day.

And if you look at Friday's closing price, and compare that to their respective 52 week highs, on a percentage basis, and factoring in those juicy dividends, these stocks have lost material value.

And please don't tell me "Buy the Dip," when the high yield dividend portfolio strategy has described as be full invested. In other words, if people were following the strategy, to the letter, they don't actually have capital (or dry powder) to "buy the dip," in large quantities, outside of quarterly (or monthly) dividend reinvestment dollars.

Again, I can't say it enough, outside of severe market panics, like the 2008/09 crash or the March and April 2020 Covid-induced crash, where some really high quality dividend stocks were accident high yielders, at least for a very brief period of time, high yield dividend stocks aren't IG bond proxies. They sure as heck don't move like IG bonds, aren't even close to as safe, and probably aren't well suited for most retirees' portfolios, outside of perhaps a small and selectively allocation (at best).

If you actually look at the balance sheet leverage of many of these stocks and ETFs, you will quickly see many of them are highly leveraged. Now in future pieces, as this article is already on the longer side, and there is always the risk losing a person's attention span, I plan to discuss and highlight the leverage and risks of many of these high yield dividend stocks.

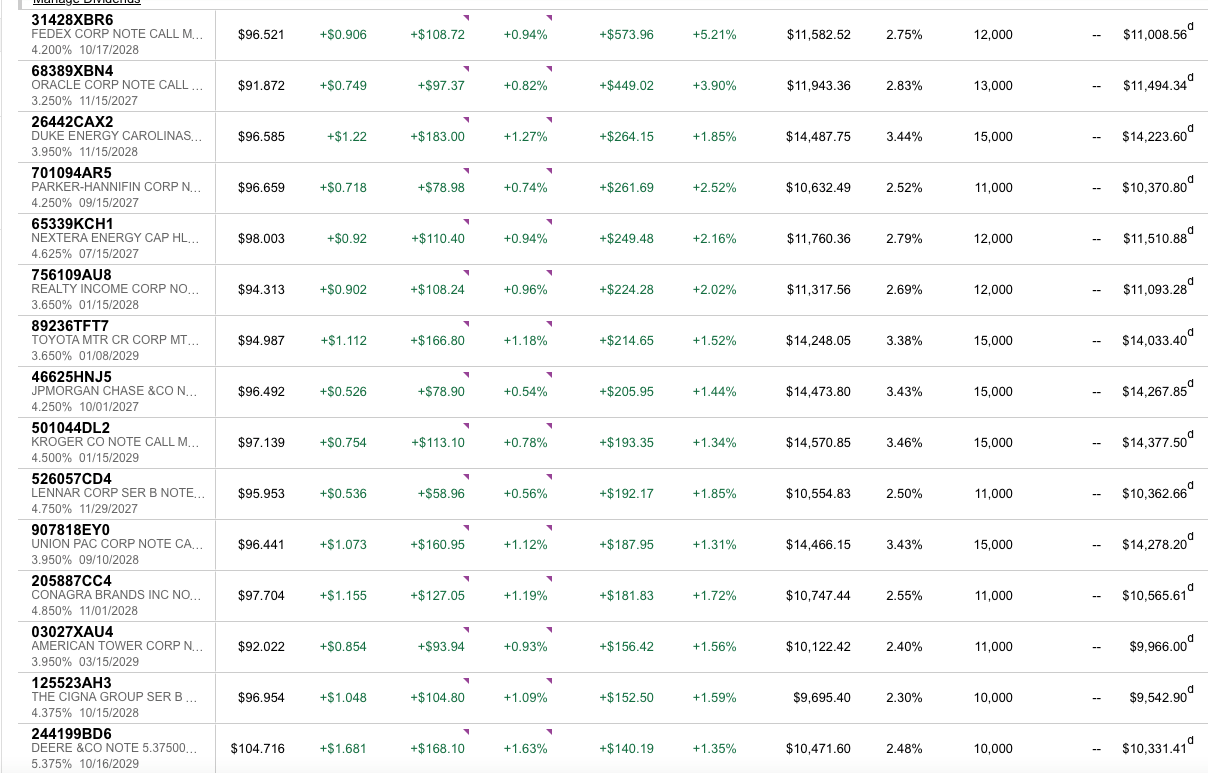

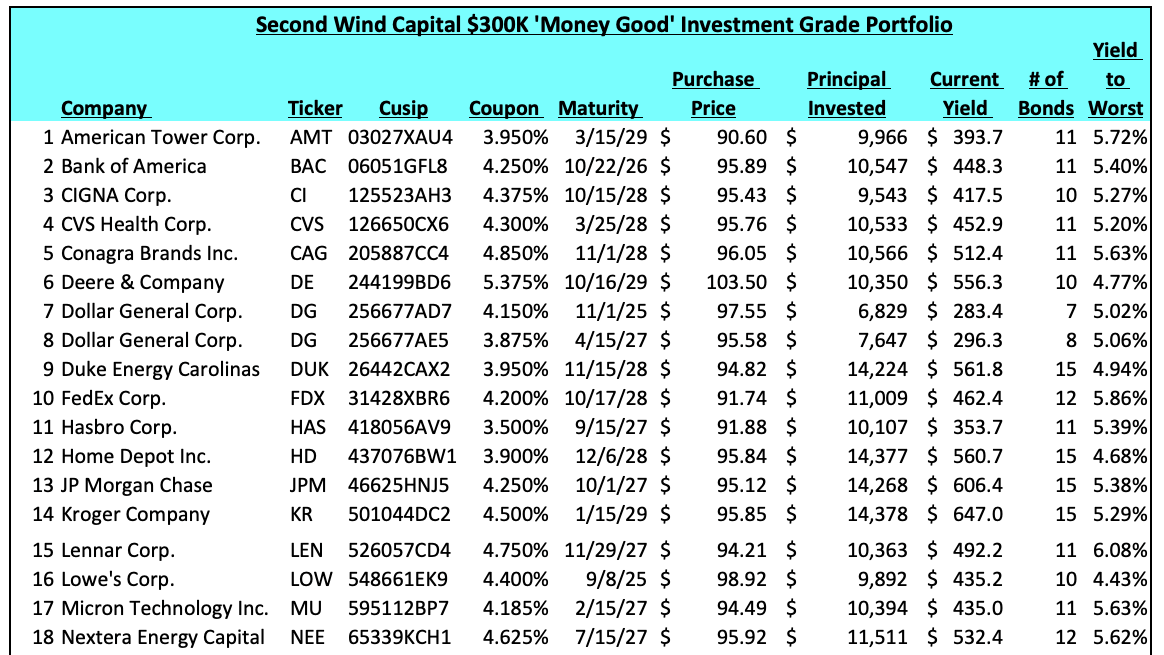

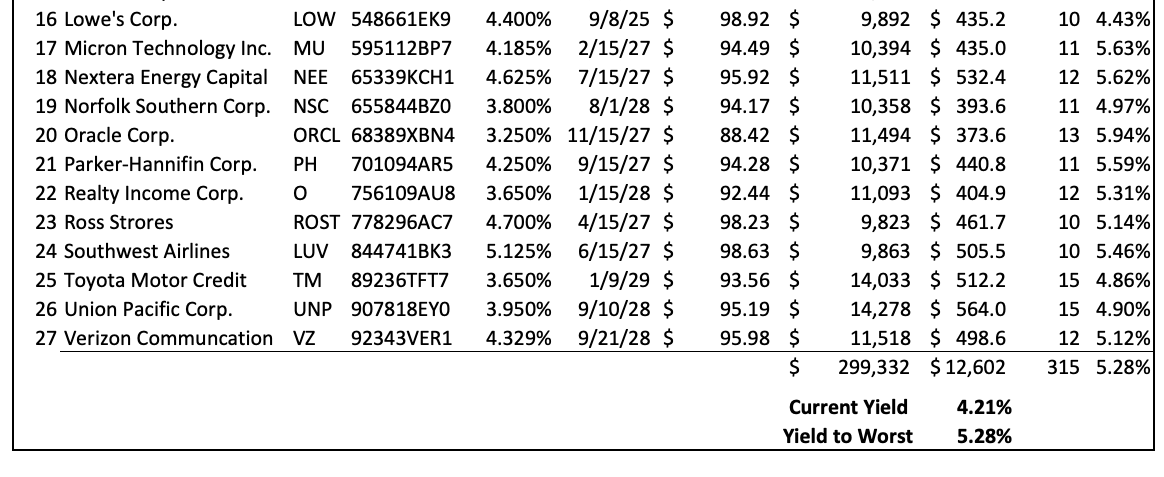

Alternatively, as it isn't enough to be against something without offering a different view, in late October 2022, I wrote "My Gift To Retirees: Sharing My Recently Constructed $300K Investment Grade SWAN Portfolio."

This is a pure Buy and Hold portfolio curated on behalf of my parents, age 72 and 74, as this is a significant portion of their taxable savings. They are fortunate to be in good financial shape, in that own their home, and cars outright, and have retirements accounts, but again, this portfolio is a meaningful piece of their net worth and the majority of their taxable savings. In other words, as a good steward, I had to be highly confident in its construction and in the underlying securities selection.

The money was invested in two tranches, $250K was deployed on October 5, 2022 and remaining $50K was invested on October 22, 2022.

Despite interest rates spiking, in 2023, notwithstanding Friday's big flight to safety, and rally in treasuries, this portfolio has held up very well.

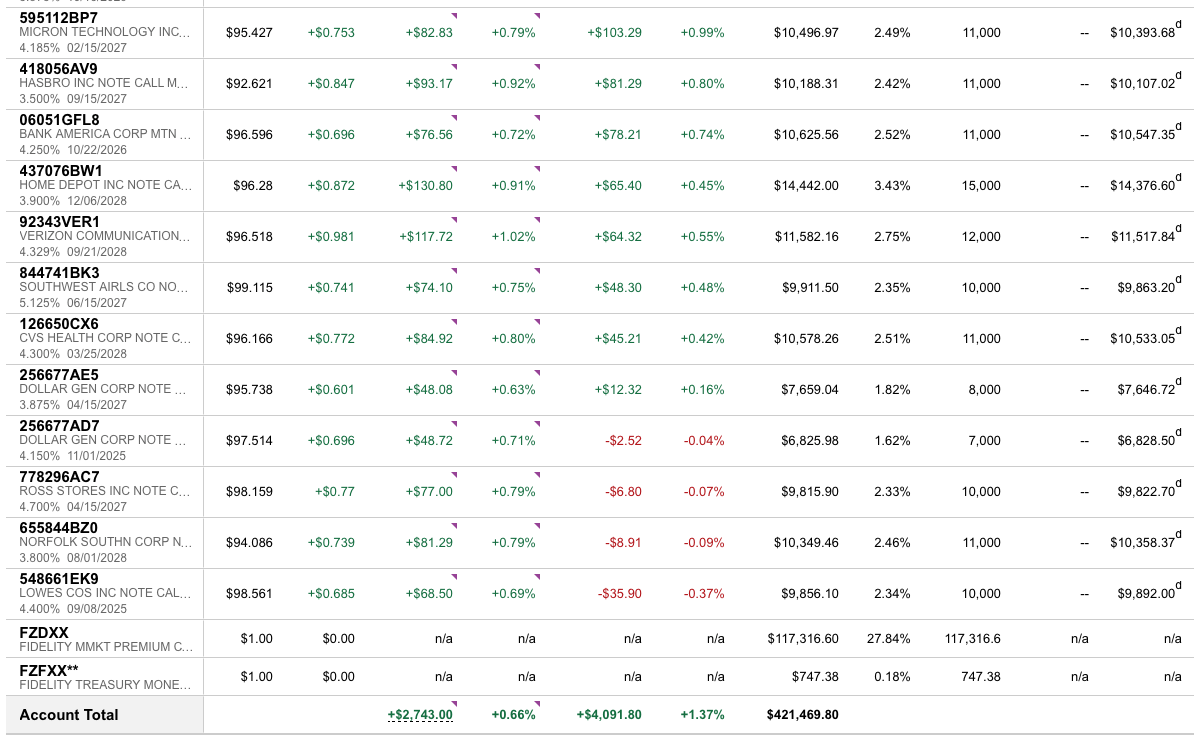

On a mark to market basis, so excluding all of the accrued and paid interest, in the form of semi-annual coupon, the overall portfolio has increased by $4,000.

{kind=link}

{kind=link}

{kind=link}

I'm showing the actual screenshots:

1) So you can see everything I do is with real money and not some excel spreadsheet or paper portfolios and 2) so you can see the cusps.

In terms of best performers:

- FedEx Corporation ( FDX ): +5.21%

- Oracle Corporation ( ORCL ): +3.90%

- Parker-Hannifin Corp ( PH ): +2.52%

- NextEra Energy ( NEE ): +2.2%

- Realty Income Corp. ( O ): +2%

- Duke Energy Carolinas ( DUK ): +1.85%

- Lennar Corp. ( LEN ): 1.85%

- Toyota Motor Credit ( TM ): +1.5%

- JP Morgan Chase ((JPM)): +1.4%

- Kroger Company ( KR ): 1.3%

Worst Performers:

- Lowe's Corp ( LOW ): -0.37%

- Norfolk Southern ( NSC ): -0.09%

- Ross Stores ( ROST ): -0.07%

- Dollar General Corp. ( DG ): -0.04%

- CVS Health ( CVS ):+0.42%

- Southwest Airlines ( LUV ):+0.48%

- Verizon Communications ( VZ ): +0.55%

And despite all of the scary headlines and its equity getting a bit dinged, as of late, the Bank of America bonds are still in the green. Also, even Norfolk Southern, which has also been in the news, and for all the wrong reasons, those bonds have helped up fine.

As long as you are buying these bonds at attractive yields to maturity, and now is a great time to be investing in investment grade bonds, you enjoy much less volatility than equities and sit comfortably higher up in the capital stack, where your principal is well guarded.

As many people, in prior articles, have said it is hard to read the small print, I included the large spreadsheet version, of the IG SWAN like portfolio, so people can more easily see the portfolio.

{kind=link}

{kind=link}

Putting It All Together

Silicon Valley Bank marks the second biggest failure in U.S. banking history. Incidentally, we learned that Signature Bank ( SBNY ), was also taken over, on Sunday, by New York Banking Regulators. This is the third largest failure in U.S. banking history. When I actually poring through SIVB's FY 2022 10-K, as I never invest in banking or financial stocks, so it would never have been on my radar, I was amazed how poorly constructed balance sheet was. The borrow short (and mostly via demand deposits) and lend long (and at terrible absolute rates) mis-match was beyond words. Once again, Sir Warren Buffett has been proven correct, this time, on the topic of Efficient Market Hypothesis. SIVB published a 10-K, on February 24, 2023, where it showed Mr. Market that the company was insolvent (or close to it). And yet, as of last Wednesday, March 8, 2023, SIVB shares were changing hands, in the $260s, with nearly a $16 billion market capitalization. Most of the money invested in SIVB was via ETFs, that just blindly tracking an index. Another important topic, well suited for another day.

As for the most important investor takeaway, for the Seeking Alpha audience, don't reach for yield . This most unfortunate event should be a catalyst that prompts retirees to re-examine how much risk they are taking.

Do retirees really understand how much risk they may (or may not) be taking?

Have retirees taken the time to truly understand how leveraged balance sheet of the underling companies are?, within their high yield dividend portfolios.

Lastly, are retirees comfortable with the amount of risk they are taking to reach for those yields?

For further details see:

SVB Financial Group Reached For Yield, Failed, Perhaps A Canary In The Coal Mine