SVOL - SVOL: Downgrade To Sell On Strategy Drift

2023-10-23 18:31:30 ET

Summary

- I decided to sell my entire position in the Simplify Volatility Premium ETF due to recent changes in its portfolio and strategy.

- SVOL has deviated from its core strategy by adding significant positions in the Simplify Aggregate Bond ETF and the iShares iBoxx $ Investment Grade Corporate Bond ETF.

- Furthermore, in the short-term, an escalating Israel/Hamas war risks causing volatility to spike. So caution is warranted.

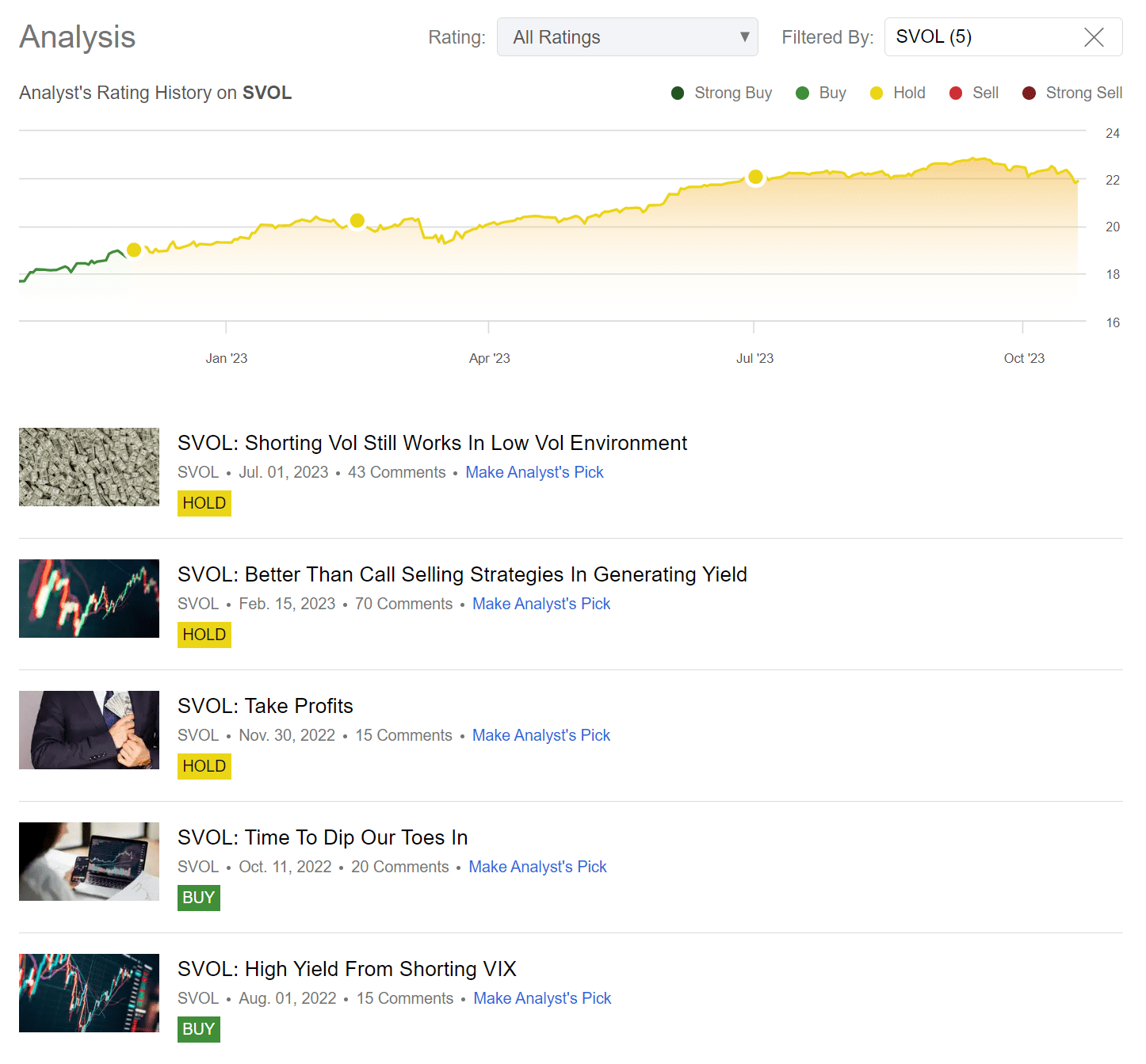

I have been an early advocate of the Simplify Volatility Premium ETF ( SVOL ), first covering the ETF in August 2022 when it was still a relatively unknown fund. Over the past year, I have written a total of 5 articles on the SVOL ETF, covering numerous topics such as risks to SVOL's strategy, comparison of SVOL to other high-yielding funds, and whether shorting volatility still works in a low-volatility environment (Figure 1).

Figure 1 - Overview of author's articles on SVOL (Seeking Alpha)

{kind=link}

In this article, I will go over some recent developments in SVOL's portfolio and why I have decided to sell my entire position in SVOL at this time.

Brief Fund Overview

First, for those new to the SVOL ETF, the Simplify Volatility Premium ETF seeks to provide investment returns that correspond to 0.2x to 0.3x the inverse of the S&P 500 VIX short-term futures index, while hedging tail risks for extreme moves in volatility with long volatility options.

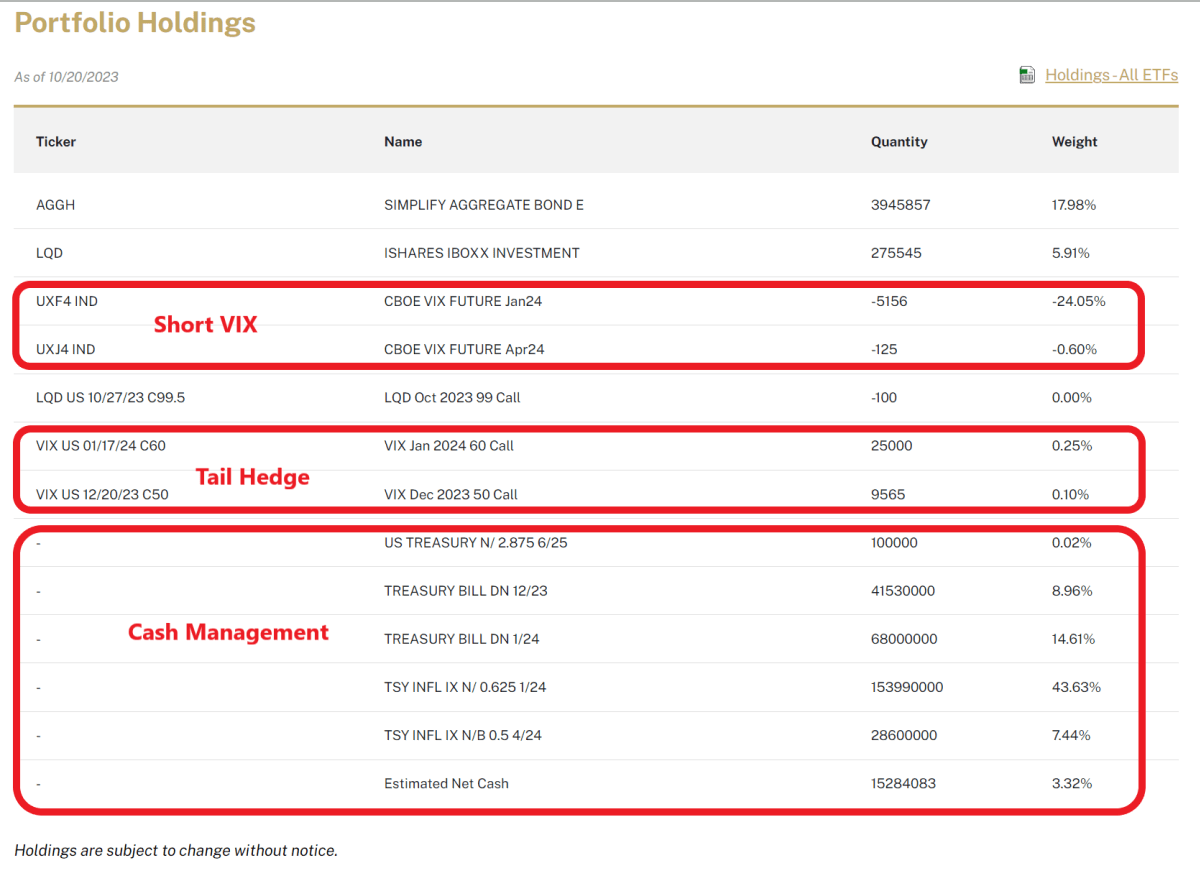

To understand SVOL, I have split its portfolio into 3 main buckets: the main short-VIX bucket that shorts 20-30% in short-term VIX futures, a tail hedge bucket that owns out of the money ("OTM") calls on VIX or similar products that protect against black swan events, and a cash management bucket that aims to generate additional yield on idle cash from treasury bills or other short-term bonds (Figure 2).

{kind=link}

However, in the last few months, I have noticed some changes to SVOL's portfolio that do not correspond to my historical understanding of the fund's strategy. Namely, we see the SVOL ETF has now branched out into an 18.0% weight in the Simplify Aggregate Bond ETF ( AGGH ), a 5.9% weight in the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ), and a small short of LQD calls.

Deviation From Core Strategy To Avoid Flat VIX Curve...

Furthermore, if we recall from my most recent article , I noted that SVOL's strategy was designed to short the 2nd or 3rd month VIX future and cover after a month or two when the future becomes the 1st month (Figure 3).

Figure 3 - Illustrative SVOL strategy (Screen capture from SVOL strategy video)

SVOL is basically a play on the historical contango spread between the near-month VIX futures and farther-dated VIX futures. As long as the VIX futures curve remains in contango, SVOL's strategy should be able to make money. However, if we look at Figure 2, we can see that SVOL is actually short January and April 2024 VIX futures, which are 3 and 6 month tenors. This is a deviation from the fund's stated strategy (for more background, please watch this video posted on SVOL's website where the fund manager describes SVOL's strategy).

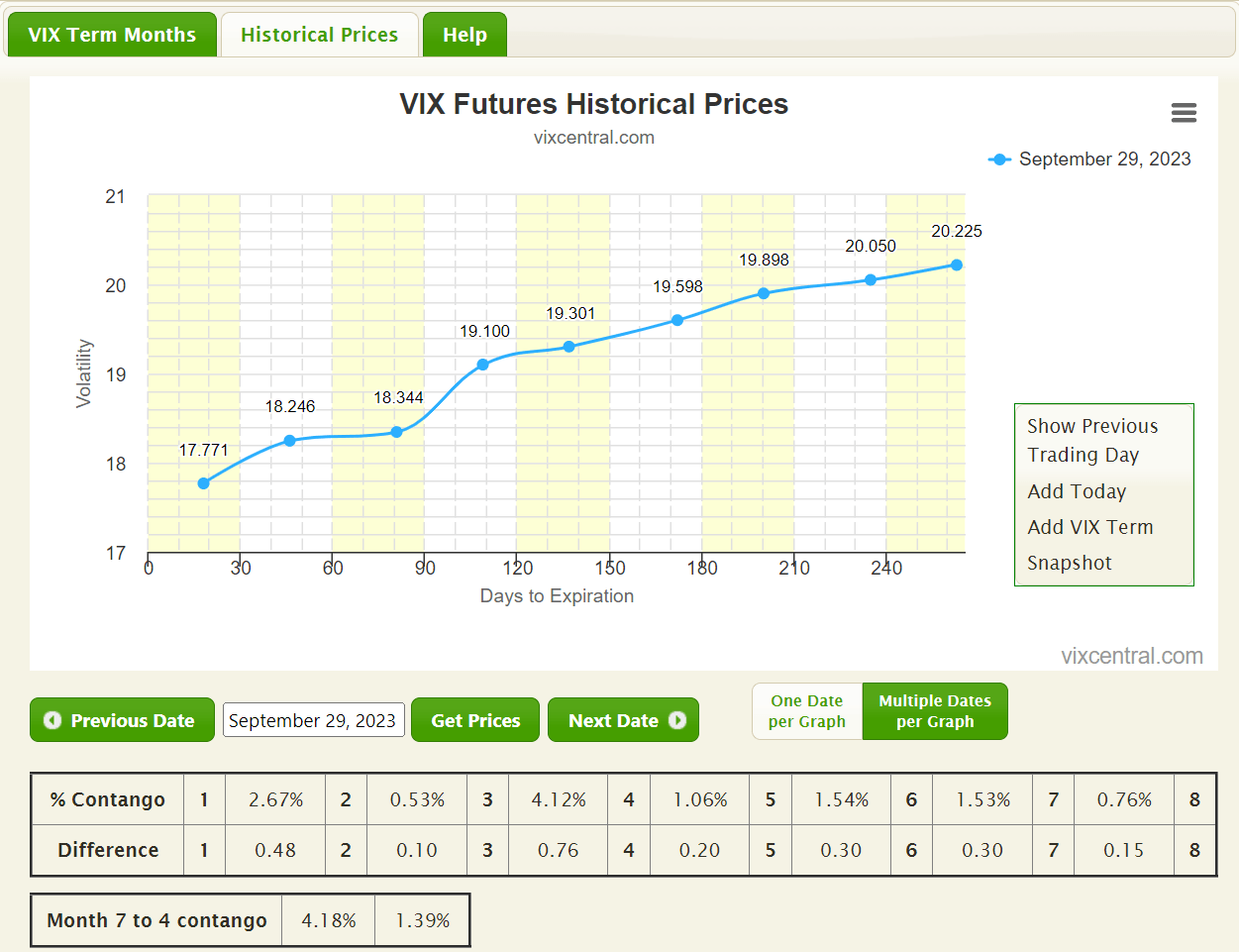

According to the fund's latest commentary , "SVOL has taken short positions in the intermediate part of the curve (as opposed to the front end) to have the potential to deliver positive returns even in a moderately rising VIX environment".

If we look at the VIX curve at the end of September (when the commentary was written), we can see that the VIX curve was very flat at the short end, whereas there was a notable jump to the 4th month (January 2024) and beyond (Figure 4).

Figure 4 - VIX futures curve, September 2023 (vixcentral.com)

{kind=link}

So SVOL's shift to shorting January 2024 and April 2024 futures does make sense, as the 2nd and 3rd month was very flat and did not provide an attractive spread opportunity.

Unlike some other strategies that mechanically performs the same function every month (i.e. XYLD), this flexibility by the manager to adapt to the market environment is what makes the SVOL ETF unique, and should be commended in my opinion.

... But Diversification Into Bonds Raises Concerns

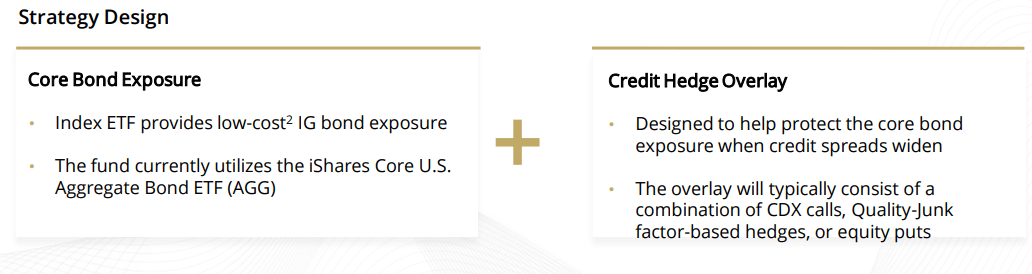

However, my main issue with the SVOL ETF is its deviation from a simple cash management function into sizeable positions in the AGGH and LQD ETFs. For those not familiar, AGGH is a marketed by Simplify as a core bond fund plus credit hedge overlay (Figure 5).

{kind=link}

However, as I discussed in a recent article , the AGGH ETF is an eclectic mix of fixed income ETFs and option positions that in aggregate, do not resemble its stated strategy in my view. In addition, one of the main strategies employed by the AGGH ETF is to sell interest rate and credit volatility in order to fund credit hedging costs. So in effect, by adding the AGGH ETF into SVOL's portfolio, the manager may be adding short-vol exposure to interest rate and credit markets that is not explicitly stated in SVOL's mandate.

To be upfront, I have a dim view of the AGGH ETF and this is the primary reason why my view on SVOL has soured. If I wanted to have exposure to the AGGH ETF, I would go out and buy shares of the ETF myself. I do not need or want the manager to make that cross-holding decision for me.

Investors should also note that with SVOL gaining in popularity and having $461 million in assets, an 18% position in the SVOL ETF equals $83 million, or more than 75% of the assets of the $108 million AGGH ETF!

Has SVOL Hit Theoretical Limits Of Returns?

The deviation in SVOL's strategy also ties back to a topic I have discussed in my prior articles, namely, what is the theoretical limit to SVOL's returns? From Figure 3 above, we can see SVOL's main strategy is to capture ~1 VIX pt between the 2nd and 1st VIX futures, or approximately 5% in monthly returns. With a 20-25% exposure to short VIX futures, this means SVOL can generate ~1.25% / month in returns or ~15% annualized. "SVOL can generate a 15% yield" is also what the manager has been quoted as saying, in the above-linked video (28-minute mark).

There may be some wiggle room with the SVOL's distribution yield, as treasury bills are now yielding more than 5%, which can supplement the yield generated from short VIX futures and offset the tail hedge budget of 2-4% per year.

Furthermore, the LQD and AGGH ETFs may pay a higher yield than treasury bills. So another way to think about the shift from holding treasury bills to higher-yielding LQD and AGGH ETFs may be the SVOL strategy hitting the limits of its short-vol strategy, and creatively trying to find other ways to maintain the yield it can pay to investors.

My hunch that SVOL has reached its theoretical maximum return is confirmed by analyzing the ETF's NAV, which has basically been flat since January (Figure 6). A flat NAV means that any returns generated by SVOL's strategy have been paid out to investors via its $0.32 / month distribution, which equates to a forward yield of 17.6%.

Figure 6 - SVOL's NAV has been flat since January (morningstar.com)

{kind=link}

In the past, I have advocated for the SVOL ETF to cut its distribution to an 8-10% yield and allow NAV to accumulate, as there will inevitably be periods when the VIX curve is less steep (like it was in early 2022 and currently), and the SVOL ETF will have to dip into NAV to fund its distribution. Long-term declining NAVs are problematic as it indicates there are less assets to support future distributions, making a fixed distribution rate harder and harder to sustain.

Instead, it appears the manager has chosen to add additional risks (AGGH and LQD) to the portfolio rather than cut the distribution rate.

Israel/Hamas War Could Be A Tail Event

Another reason I am less comfortable shorting volatility at the moment is the war between Israel and Hamas. Any escalation in the war risks devolving into a regional Middle East conflict that can cause oil and volatility to spike. For example, in 1990, during the first Gulf War, both oil and VIX doubled when the U.S. invaded Iraq to liberate Kuwait (Figure 7).

Figure 7 - Middle East wars can have large impacts to volatility (Author created with price chart from stockcharts.com)

I wrote more about this risk in a recent article on the ProShares VIX Short-Term Futures ETF ( VIXY ).

Risks To My Thesis

The major risk to my cautious view on the SVOL ETF is that seasonally, the year-end period has been weak for the VIX index, which should support short volatility strategies like SVOL (Figure 8).

Figure 8 - VIX Index seasonality (equityclock.com)

However, as we saw in Figure 4, subdued year-end volatility is well expected by the market, which has led to a flat VIX curve at the short-end and has pushed SVOL to short January and April 2024 futures instead.

Furthermore, since the SVOL ETF now has significant bond exposures via the AGGH and LQD ETF, if bond markets rally, then that could provide a boost to the SVOL ETF. But it is important to reiterate that long bond exposure is likely not what investors signed up for when they invested in the SVOL ETF.

Conclusion

The Simplify Volatility Premium ETF has been a solid performer in my portfolio, delivering 16% total returns since my first recommendation in August 2022, handily outperforming the S&P 500's 4.6% return over the same time frame (Figure 9).

Figure 9 - SVOL has outperformed S&P 500 since August (Seeking Alpha)

{kind=link}

However, recent changes to SVOL's portfolio and strategy have changed my view of the ETF. Specifically, I have a dim view of the SVOL ETF adding a significant position in the Simplify Aggregate Bond ETF, as it muddies SVOL's strategy, plus I have an unfavorable opinion of the AGGH ETF itself. Furthermore, I believe there is a significant risk that the recent Israel/Hamas war could cause a spike in volatility that would be detrimental to short-vol strategies like SVOL. Therefore, I have liquidated my holding on the SVOL ETF.

I may revisit the SVOL ETF in the future if the risk/reward to shorting volatility changes, however, I no longer view the SVOL ETF as a core portfolio holding due to the introduction of cross-holdings in other funds that complicates its strategy.

For further details see:

SVOL: Downgrade To Sell On Strategy Drift