CYA - SVOL: Downgrading Due To Concerning Trends

2023-11-20 12:02:06 ET

Summary

- Simplify Volatility Premium ETF has changed its dividend distribution to primarily return of capital distributions, indicating a struggle to meet consistent income targets.

- My rating has changed to hold over concerns of these RoC distributions continuing moving forward.

- SVOL has changed its hedging strategy to incorporate the Simplify Tail Risk Strategy ETF, which may introduce additional risks to the fund's strategy and prove as an inefficient hedge.

- Favorable positioning on the VIX term structure (curve) and ability to provide consistent income despite RoC provide a struggling bull case.

Introduction

About a month ago, I began coverage of the Simplify Volatility Premium ETF (SVOL) and gave it a buy recommendation based on changes in their underlying bond holding. That thesis has not changed, so please check that out if you want a deeper look into the fund's holdings. This article is a follow-up to address changes in dividends.

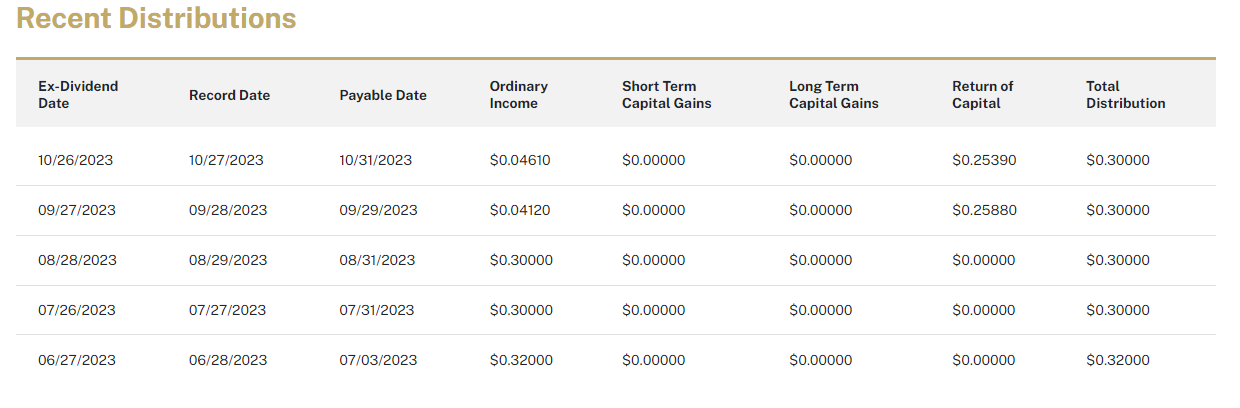

SVOL's downgrade comes as a response to the change in how Simplify is handling dividends. The last two dividends have been primarily return of capital (RoC) distributions. This is a signal that consistent income is not being met by the VIX carry strategy, and these returns were necessary to keep up the distribution target rate of 15%. While this may be temporary as holdings change, it is enough for me to give SVOL a downgrade to hold.

Return of Capital

For the first time since its inception two years ago, in September, SVOL had to return capital to shareholders instead of income. In the October distribution, SVOL again returned capital to shareholders in place of income.

This distribution does not create a taxable event, instead lowering the cost-basis on your initial investment. RoC distributions aren't necessarily a bad thing, but they aren't a good thing either.

In both distributions, SVOL distributed a mix of ordinary income and RoC. See Figure 1 for the breakdown.

{kind=link}

While I still believe in SVOL's potential to generate a consistent $0.30/share income moving forward, especially now that [[AGGH]] and [[LQD]] hold larger positions in the portfolio, this trend of returning capital is concerning and should give investors pause about enlarging their positions in SVOL.

This change in distributions comes at the same time as their change in core holdings, indicating that they are still tinkering with SVOL's core strategy and are trying to keep their income stream consistent. This consistency is commendable, and many income investors are still happy despite this change in the composition of distributions.

There is more to talk about in changes, but I started here since it is the primary reason for my downgrade.

Rolling January to April

From last month to this month, the short VIX positions have been consolidated. What used to be a short position in January has now moved out to April.

{kind=link}

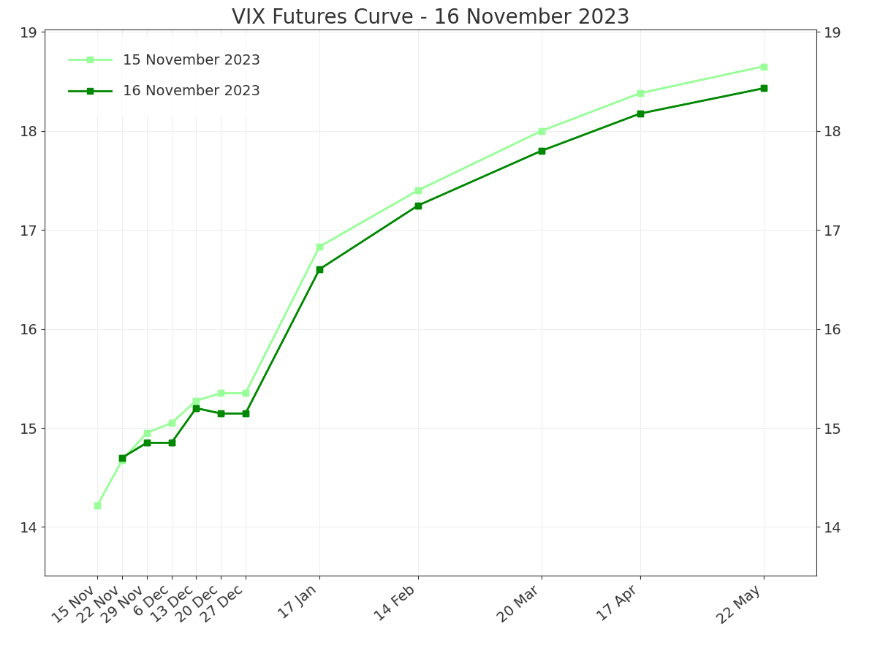

This extension may have been done for a few reasons, but primarily for convexity's sake. This is a welcome move from me, as I'm happiest when SVOL is positioned high on the VIX curve and can provide the most income.

{kind=link}

The move from January to April widens SVOL's exposure to VIX spikes, which may explain the changes in hedging strategy. This is a good move and I like the short exposure staying at 0.2x, since the VIX is relatively low.

If we see a larger move up, above 20, I would like to see SVOL position a little more aggressively with their shorts.

Change in Hedging Strategy

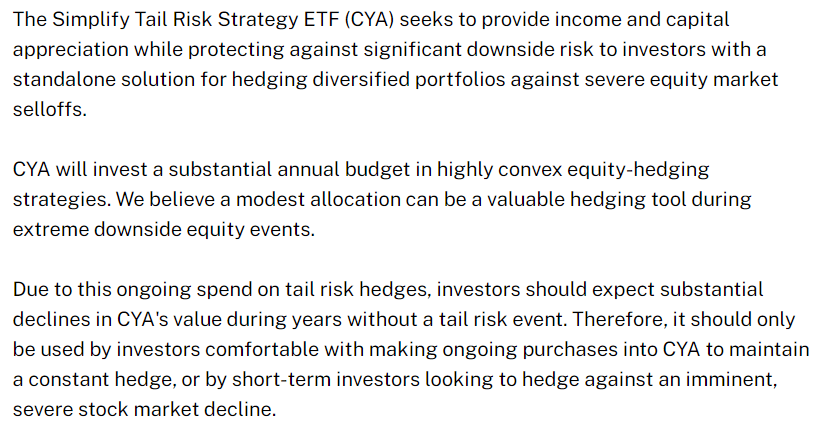

The last time I covered SVOL, its only hedges against an adverse move in the VIX were far OTM VIX calls. The current strategy has incorporated one of Simplify's other funds, the Simplify Tail Risk Strategy ETF ( CYA ).

I like the VIX call strategy, even though it hasn't been tested in a real black swan event, and I think that the managers have employed them responsibly so far. Simplify's Macro ETF ( FIG ), also employs VIX calls, though it buys short OTM call spreads instead of vanilla OTM calls.

I am not typically a fan of ETFs that have to warn investors upfront about their costs. Such is the necessary evil of hedging.

{kind=link}

The more capital-efficient approach would be to increase the position in OTM VIX calls, or create a ladder of calls to reduce some cost. SVOL could also employ the kind of call spreads used by CYA itself without needing to invest in CYA.

Currently, the position in CYA is small enough not to matter too much, but this change in hedging strategy is not what I wanted to see from the fund managers. CYA is a broader hedge against the market and not just the VIX itself, which is the primary risk with SVOL's strategy.

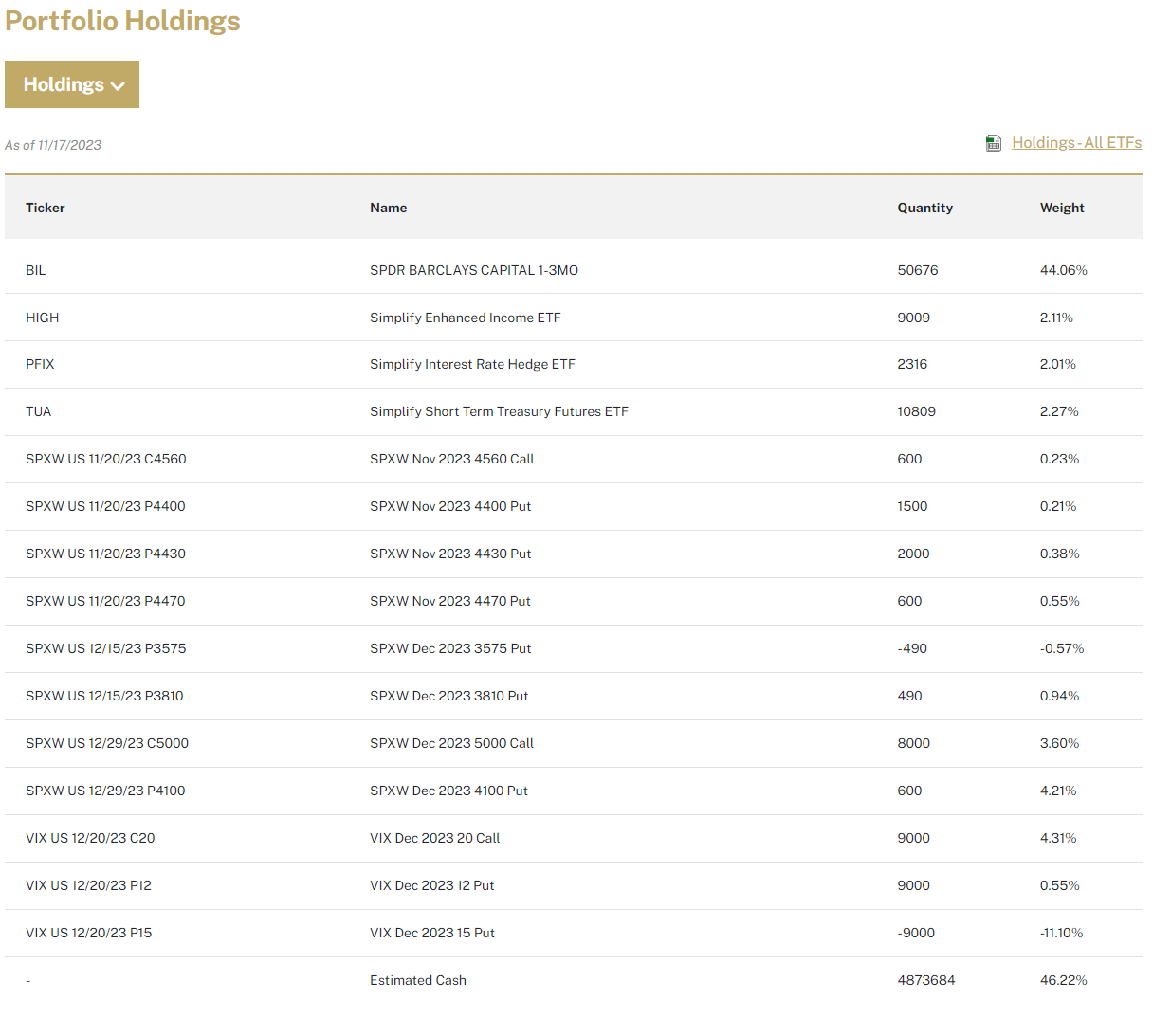

See CYA's holdings below. Notice that their primary hedging strategies are against the VIX and SPX and include a large allocation to T-bills, cash, and minimal positions in various Simplify income ETFs.

{kind=link}

VIX & Leverage Risks

The Simplify Volatility Premium ETF is a leveraged ETF providing -0.2 to -0.3x exposure to the VIX, reset daily. This means that there is risk of significant adverse moves in the VIX that could affect the fund.

SEC documents outline VIX Futures Risks :

VIX futures contracts can be highly volatile and the Fund may experience sudden and large losses when buying, selling or holding such instruments; you can lose all or a portion of your investment within a single day. Investments linked to equity market volatility, including VIX futures contracts, can be highly volatile and may experience sudden, large and unexpected losses. VIX futures contracts are unlike traditional futures contracts and are not based on a tradable reference asset. The Index is not directly investable, and the settlement price of a VIX futures contract is based on the calculation that determines the level of the VIX. As a result, the behaviour of a VIX futures contract may be different from a traditional futures contract whose settlement price is based on a specific tradable asset and may differ from an investor's expectations. The market for VIX futures contracts may fluctuate widely based on a variety of factors including changes in overall market movements, political and economic events and policies, wars, acts of terrorism, natural disasters (including disease, epidemics and pandemics), changes in interest rates or inflation rates. High volatility may have an adverse impact on the performance of the Fund. An investor in any of the Fund could potentially lose the full principal of his or her investment within a single day.

While this is not a fully leveraged fund that deals with value decay like ( SVIX ) or ( VIXY ), and SVOL has a positive expected return due to positive option convexity and a hedge against extreme VIX moves (as discussed earlier), there are still inherent risks.

Simplify explains better than I can, from the prospectus:

The option overlay is a strategic, persistent exposure meant to hedge against market moves and to add convexity to the Fund. If the market goes up, the Fund's returns may outperform the market because the adviser will sell or exercise the call options. If the market goes down, the Fund's returns may fall less than the market because the adviser will sell or exercise the put options. The adviser selects options based upon its evaluation of relative value based on cost, strike price (price that the option can be bought or sold by the option holder) and maturity (the last date the option contract is valid) and will exercise or close the options based on maturity or portfolio rebalancing requirements.

The Fund's returns are intended to possess convexity because the relationship between the Fund's returns and market returns is not designed to be linear. That is, if market returns go up and down in a linear fashion, the Fund's returns are expected to rise faster than the market in positive markets; while declining less than the market in negative markets. The value of the Fund's call options is expected to rise in proportion to the rise in value of the underlying assets, but the amount by which the Fund's options increase or decrease in value depends on how far the market has moved from the time the options position was initiated.

Investors need to be cautious about investing in any product they don't understand or are not prepared to take the associated risks with. While SVOL is on the safer side of these kinds of funds, since it is never more than 0.3x short, we cannot deny these risks still exist and must be understood.

Conclusion

I would not be rushing to sell your shares of SVOL. Changes in strategy may be welcome, and I am willing to wait and see how these play out. For now, I am not going to add any to my position in SVOL and advise that others do the same for now.

Due to the untested nature of SVOL's hedges in a real scenario, I like to play this position with caution.

For traders who want to be more aggressive, SVOL is still making the bull case that regardless of how dividends are paid, they are being paid consistently.

For further details see:

SVOL: Downgrading Due To Concerning Trends