SVOL - SVOL: Enhanced Version Of Short Volatility

2023-08-02 01:13:53 ET

Summary

- The Simplify Volatility Premium ETF has gained popularity among investors seeking current income and inversely correlated exposure to the VIX.

- The growth in AuM has been propelled by the recent outperformance of the S&P 500 and very attractive yield of 17%.

- SVOL offers income generation, tactical tools for negative correlation to the VIX, and asset class diversification through one instrument.

- The competitive advantage of SVOL is its unique characteristics, which differentiate it from other conventional short vol funds.

- SVOL avoids entering into extremely volatile front-end month VIX futures, but instead devises future, roll strategy by targeting longer dated contracts, and purchasing deep OTM calls to avoid losses from black swan events.

The Simplify Volatility Premium ETF (SVOL) is an actively managed ETF, which since its inception date back in mid-2021 has gained a lot of popularity among investors, who target attractive levels of current income and inversely correlated exposure to the VIX.

As of now, SVOL holds just over $370 million in the AuM and shows no signs of reversal in the growing AuM trend.

{kind=link}

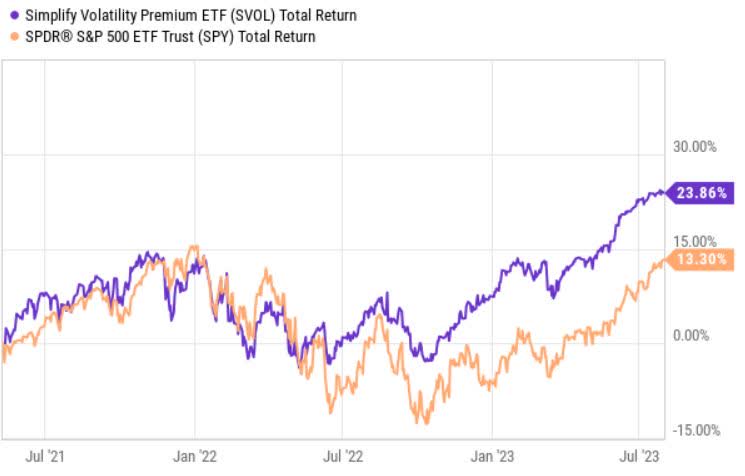

If we look at how SVOL has outperformed the S&P 500 and couple that with the current yield of ~17%, it quickly becomes clear why the AuM figure is trending upwards.

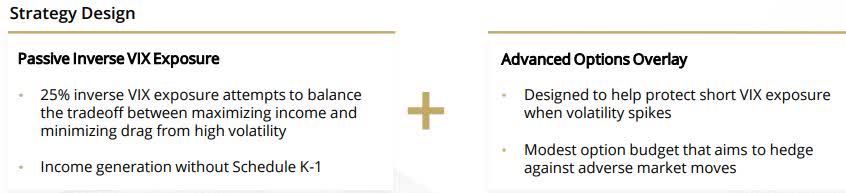

According to the Simplify - a firm managing SVOL - there are three portfolio applications that the SVOL offers:

- Income Generation : a differentiated approach for generating high yield that delivers attractive income when equity markets are range bound.

- Tactical Tool : allows to open negatively correlated exposure against VIX, profiting from declining volatility when most attractive.

- Asset Class Diversification : accesses a specific risk premium from equity, duration, and credit via one instrument.

Now, let's quickly break down the ETF and see how the strategy is structured.

{kind=link}

Effectively, SVOL combines the characteristics of passive ETF structures with relatively active option overlay tactics making the Fund semi-passive. Hence the gross expense ratio of 0.66%.

The strategy is based on 20 - 30% short VIX futures and deep OTM VIX call options seeking to provide low-cost protection against extreme VIX (or volatility) spikes.

To fund the short positions and OTM calls as well as to capture some additional yield, SVOL allocates a portion of its AuM into T-bills and/or short-term bonds.

Currently, 19% of the AuM is channeled towards short VIX positions and the remaining ~80% are allocated in risk averse bond positions (less than 1% is put into OTM VIX calls).

Investment thesis

There are two ways how one could assess SVOL and its potential to fit into investment portfolios. One is the wrong way without paying too much attention to detail and just focusing on, say, the short VIX exposure; and the second one is to delve into details untangling the underlying risk-reward dynamics.

So, if we assume the former approach, the conclusion would be biased towards avoiding SVOL.

{kind=link}

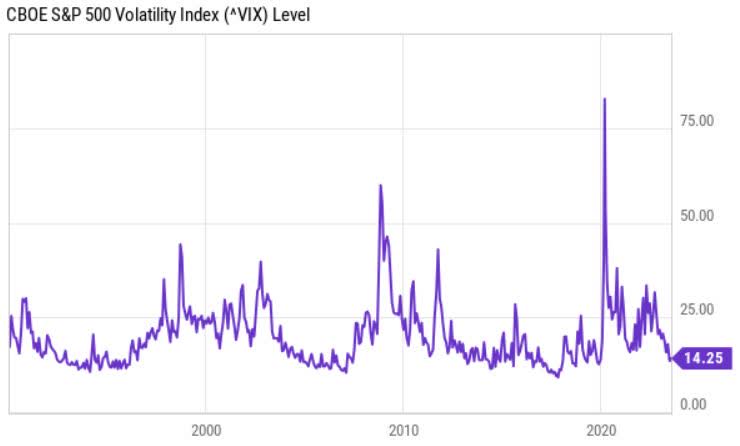

This is because the prevailing level of VIX is trading at relatively depressed levels, which inherently introduce a significant risk exposure to SVOL investors.

{kind=link}

The elevated risk stems primarily from the fact that VIX tends to trade at fairly stable levels, which after a while are abrupted by sudden spikes, whenever there is some serious catalyst for the market to become extremely fearful (or uncertain).

Currently, it seems that we have entered one of the 'stability periods', which quite naturally sooner or later will be interrupted by pessimistic data points.

Given that the SVOL is short VIX, the aforementioned dynamics seemingly do create some notable areas of concern, especially pertaining to an event in which VIX goes vertical once again.

Granted, for such tail-risk moments as we saw in early 2020 once the COVID-19 broke out, SVOL has incorporated exposure to OTM calls on VIX, thereby putting a cap on potentially catastrophic losses. However, we have to remember that these are deep out of money calls, which leave open (negative) exposure until certain threshold level (strike).

With that being said, I think that such analysis is only partially correct.

While it is true that SVOL's return profile is structurally linked in a negatively correlated manner with that of the VIX, the fact that SVOL's management team plays across the entire VIX term structure helps offset some of the key risks that are common for short vol strategies.

{kind=link}

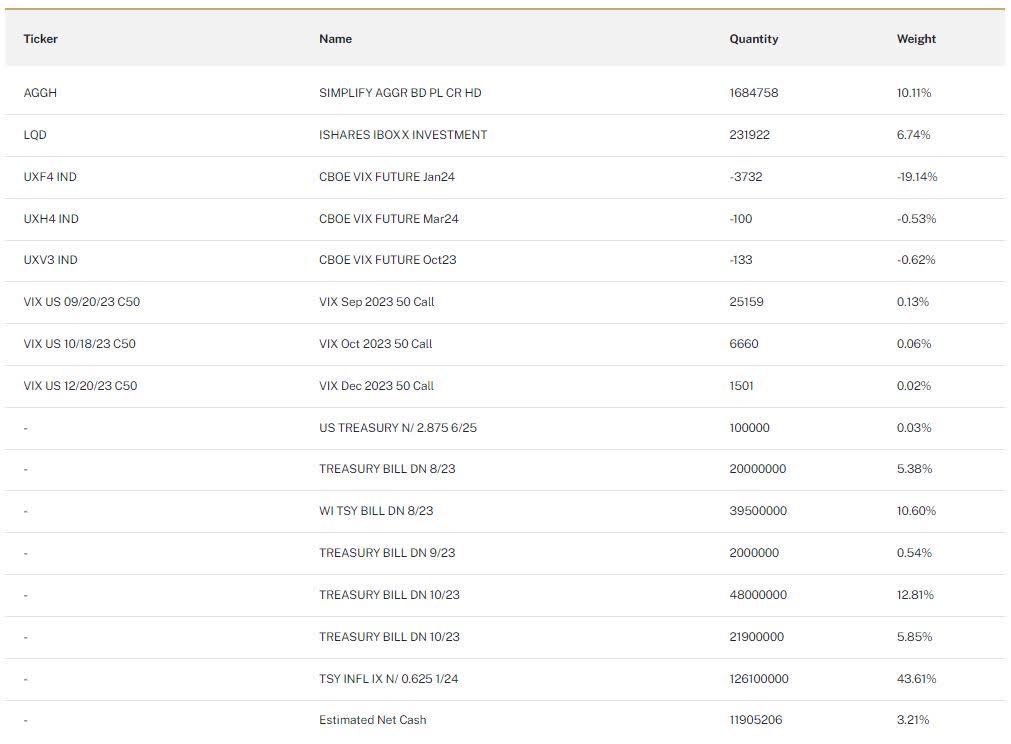

By looking at SVOL's end of July holdings, we can notice that there is no presence of front month contracts and that the management team has decided to obtain short VIX exposure via longer dated future contracts.

Plus, it is critically important to understand that SVOL does not apply 'buy and hold' type of strategy on short VIX contracts, but rather devises a future 'rollover' strategy by buying short dated and selling slightly longer dated VIX contracts.

As a result, this situation provides enhanced risk and reward dynamics. The are three underlying drivers for this.

First, there is no exposure to front end month of VIX, which historically has been the most volatile part of the entire VIX curve. Hence, SVOL is protected from very short-term market volatility spikes not only from the deep OTM calls, but also from the exposure to longer dated contracts.

Second, it allows to generate solid returns even if there are some temporary spikes in the VIX, where the roll yield or the avoidance of front-end month contracts offset the overall upward move in the VIX term structure.

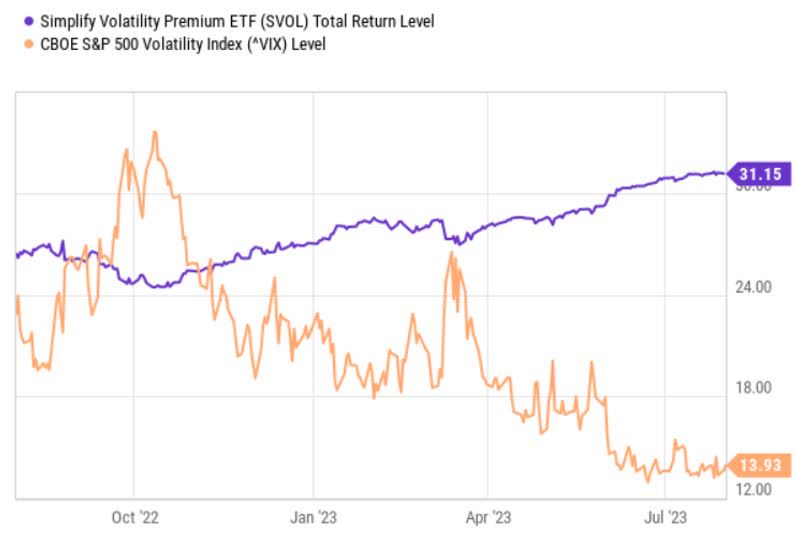

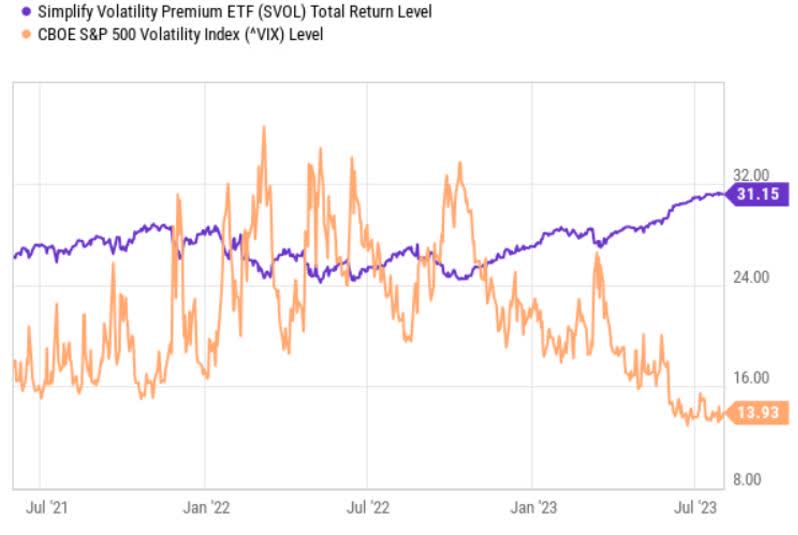

We can observe these dynamics in the chart below, where SVOL has trended upwards and/or remained stable, while VIX has fluctuated significantly.

{kind=link}

Third, the roll yield itself allows to register positive returns even if the VIX trades sideways for a longer period of time. Here the structural steepness or contango of VIX term structure comes in handy.

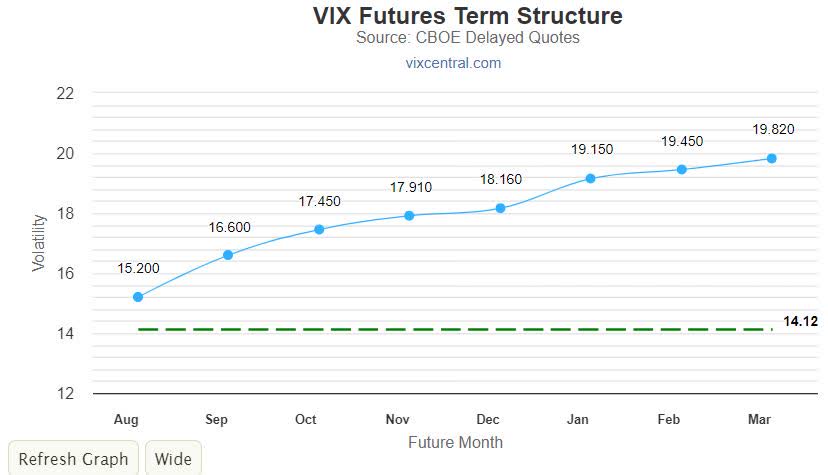

{kind=link}

The graph above depicts the current term structure of VIX, which is in contango as usual. The key drive for a structural steepness is the secular demand for front-end month futures by portfolio hedgers and speculators, who seek to profit from potential spikes in the VIX.

The term structure can transform to an inverse state, when the front-end month VIX goes ballistic such as in early 2022 of in the GFC. In this case SVOL would suffer from negative roll yield only in scenario, where the inversion remains unchanged for a relatively long period of time (e.g., more than a month).

Bottom line

In my humble opinion, SVOL deserves a place in an income-seeking portfolio as a diversifier to conventional high-yield and equity positions. The current yield of 17% is very attractive and should contribute to an enhanced level of income streams, while markets remain relatively calm or with temporarily elevated fear levels. In an upwards trending market, where the volatility remains relatively muted, SVOL embody great odds of continuing to register alpha performance.

For further details see:

SVOL: Enhanced Version Of Short Volatility