SVOL - SVOL: Unveiling The Strategy And Enhancing Investor Diversification With Income Potential

2023-08-16 10:57:19 ET

Summary

- The Simplify Volatility Premium ETF seeks to offer investment results that align with approximately -0.2x to -0.3x the inverse performance of the Cboe Volatility Index short-term futures index.

- SVOL stands out as the first ETF to combine inverse VIX exposure with a dynamic hedge.

- By leveraging the common occurrence of contango and the concept of mean reversion, SVOL offers investors an opportunity for enhanced yield, though not without inherent risks.

- SVOL uses deep out-of-the-money call options to hedge against volatile VIX movements, reducing the risk of substantial losses.

All figures are listed in unless otherwise noted.

SVOL Introduction & Mandate

The Simplify Volatility Premium ETF (SVOL) seeks to provide investment results, before fees and expenses, that correspond to approximately one-fifth to three-tenths (-0.2x to -0.3x) the inverse of the performance of the Cboe Volatility Index (VIX) short-term futures index while also seeking to mitigate extreme volatility.

Risk Level: Very High

Gross Expense Ratio: 0.66%

Investor Objective: SVOL aims to provide an attractive income stream and source of diversification while seeking to avoid risks inherent in other income-producing asset classes.

Fast Facts:

- SVOL is the first ETF providing inverse VIX exposure coupled with a dynamic hedge.

- Performance has been good as well earning 26.39% since inception (May 12th, 2021).

- The fund provides a good source of diversification within an equity portfolio as it has a 0.71 daily correlation with the S&P500.

How The VIX Works & What It Means

Before we dive into how SVOL works, we need to understand a few key terms.

Call Option: Imagine you really want to buy shares of a certain company, but you're afraid the price might go up in the next few months. You wish you could lock in the current price, but you're not sure if you'll actually buy the shares later. So, you buy something called a "call option". This option gives you the right (but not the obligation) to buy those shares at a specific price (let's say, ) anytime within a set time frame. You pay a fee for this option because having the ability to buy the shares at is valuable, especially if the price goes higher. It's like making a reservation to buy at a certain price, just in case the price goes up before your reservation expires.

Put Option: Now, let's say you own some shares of a company, and you're worried that the price might drop in the next few months. You wish you could lock in the current price you'd get for selling the shares, but you're not sure if you'll actually sell. So, you buy a "put option". This option gives you the right (but not the obligation) to sell your shares at a specific price (again, let's say ) within a certain period. Similar to the call option, you pay a fee for this put option because having the ability to sell at is valuable, especially if the price goes lower. It's like making a reservation to sell at a certain price, just in case the price goes down before your reservation expires.

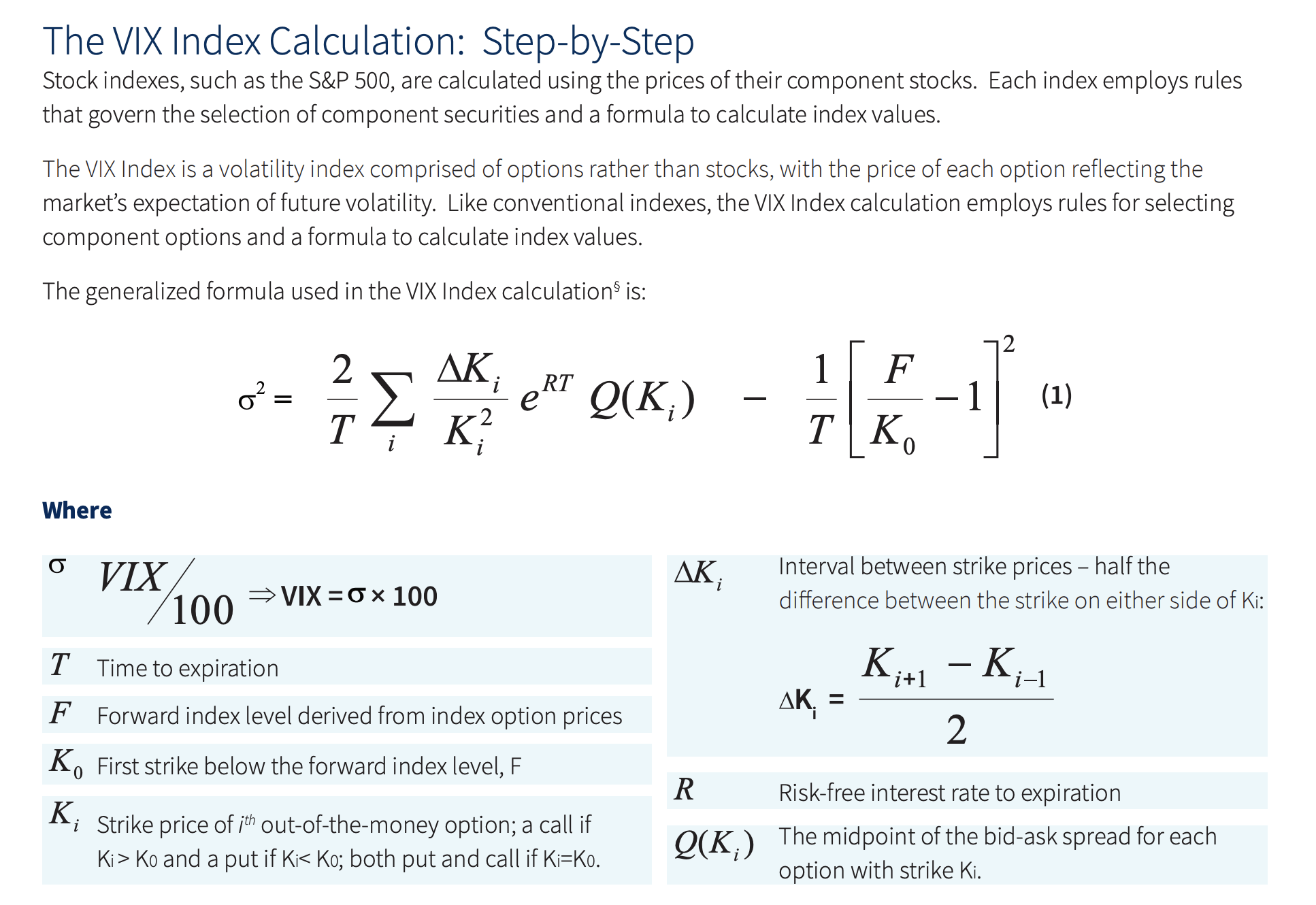

Now that we have a basic understanding of call and put options, we can work out what the VIX is. The VIX or volatility index, is a market index representing the market's implied expectations for volatility over the next 30 days. The volatility that we are calculating is based on the S&P 500 using near- and next-term put and call options with more than 23 days and less than 37 days to expiration. The VIX is calculated as:

VIX Formula (Cboe VIX White Papers)

{kind=link}

As a quantitative application, if VIX was trading at 20 it would imply that on average, the S&P 500 is expected to move up or down by about 20% (annually). Converting to monthly, the S&P 500 is on average expected to move up or down by 5.77%, and daily would be 1.265%. To get to the monthly expectation, we take 20% and divide it by the square root of 12. For daily, we take 20% and divide it by the square root of 252.

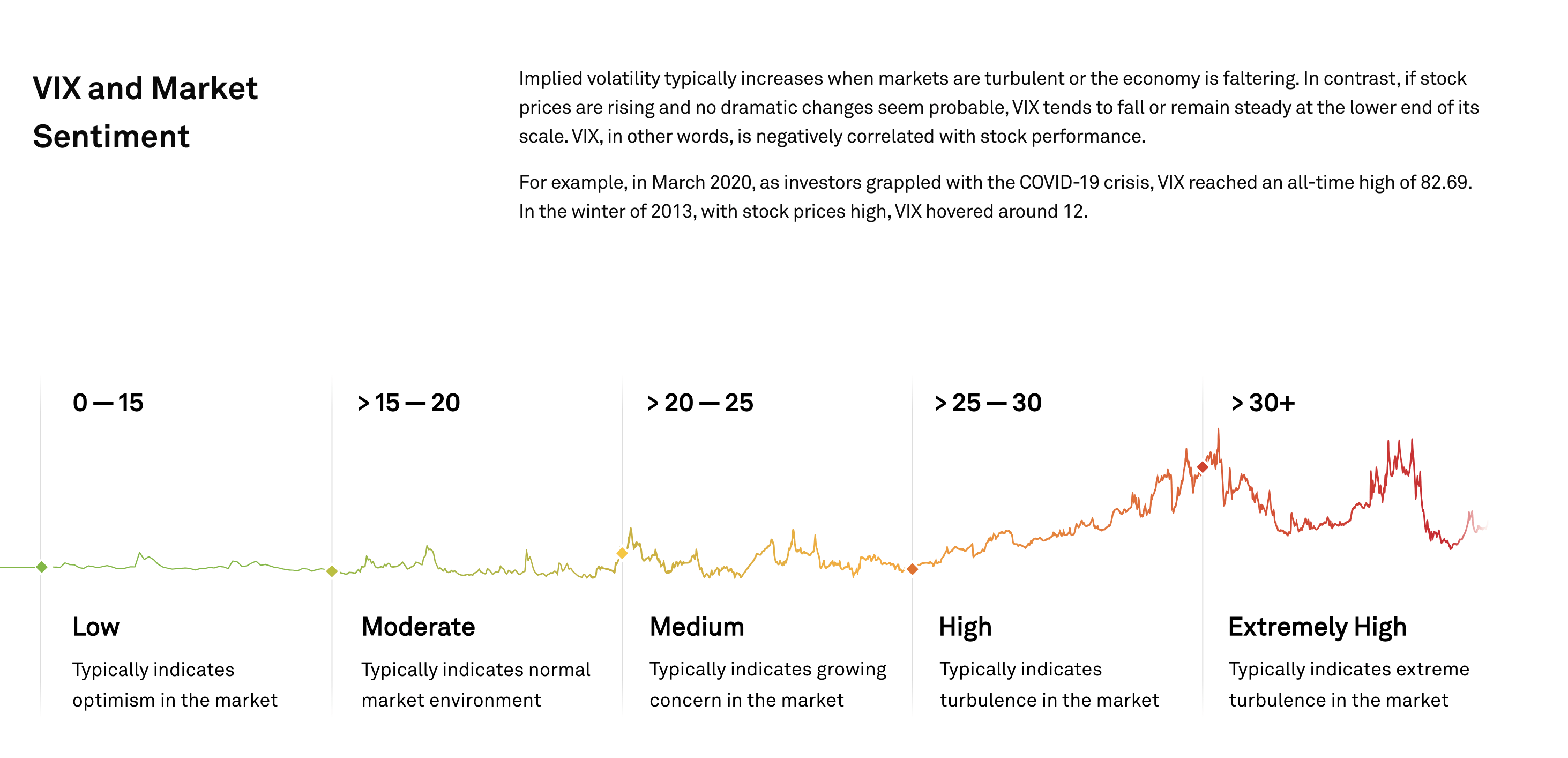

The higher the VIX is, the higher the expected volatility is. Typically, in these cases market turbulence is high.

VIX Level Meanings (S&P Dow Jones Indices)

{kind=link}

Now that we understand what the VIX is, it starts to become more clear on how one could make money using it.

For example, if you believe that realized volatility over the 30-day period will be higher than what is expected, you would buy a futures contract on the VIX. If you believe that realized volatility over the 30-day period will be lower than what is expected, you would sell a futures contract on the VIX.

How SVOL Works

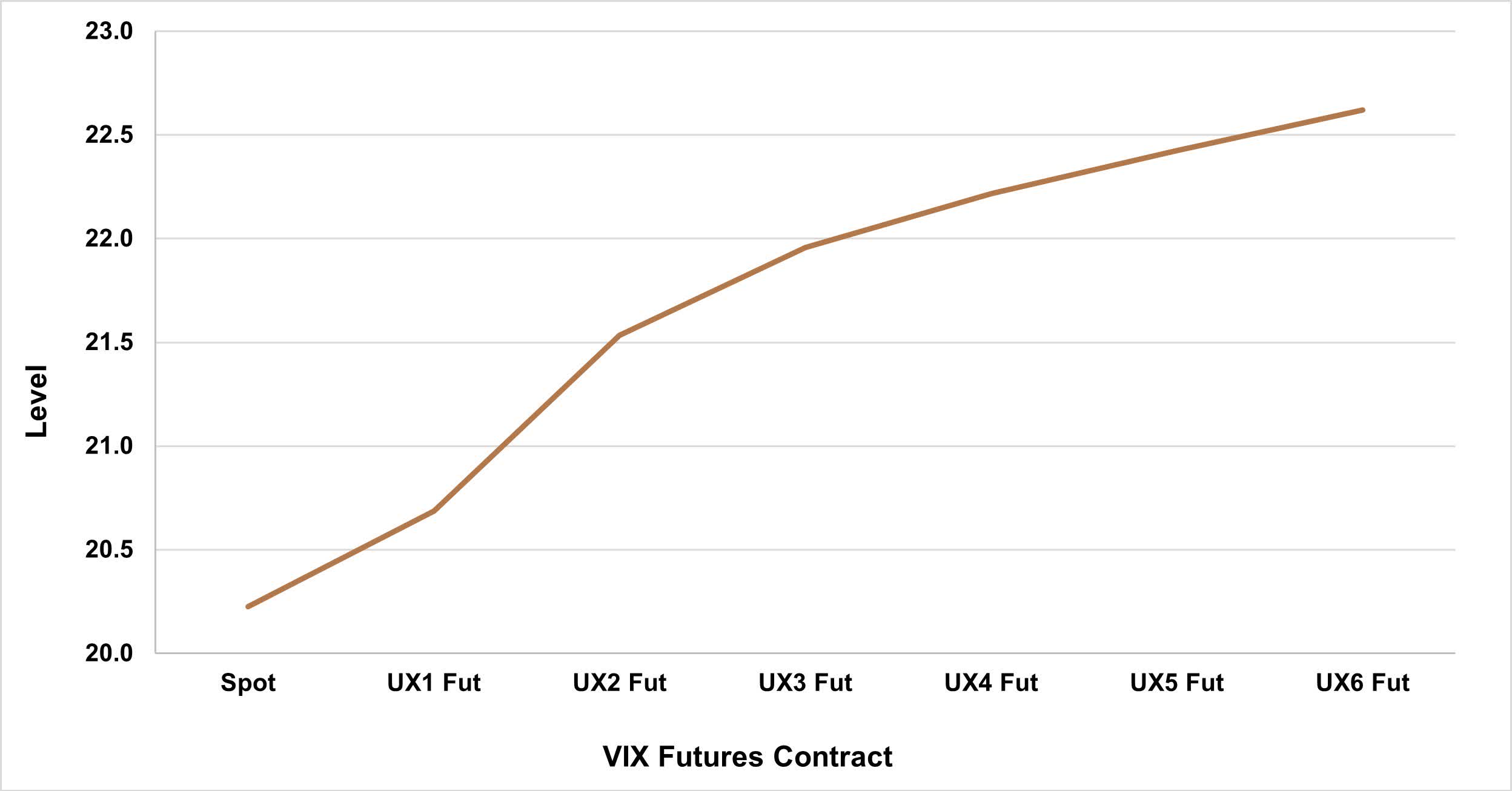

SVOL strategy involves taking a short position in VIX futures contracts. This means that SVOL benefits when the VIX futures market experiences contango (futures prices higher than the spot price). This is a common occurrence for VIX because of a mathematical property called mean reversion. Mean reversion is a theory used in finance that suggests that asset price volatility and historical returns eventually will revert to the long-run mean or average level of the entire dataset. The VIX has a long-run average of 21 and has historically shown to revert back to this level when it increases/decreases.

VIX Historic Term Structure (Bloomberg)

{kind=link}

This property of mean reversion means that a short seller can capture a 'premium' by selling higher-priced VIX futures and then replace those with lower-priced ones as the futures contract approaches expiration. This premium that the fund captures is what gets paid out to investors. The premium tends to be higher when the VIX is higher because the market often prices in a volatility premium. Note that SVOL is short futures contracts meaning they think expected volatility will be greater than real volatility.

VIX can be very volatile itself, when there are huge jumps in volatility it could lead to large losses for SVOL. SVOL counters this by employing a dynamic hedge through the purchase of deep out-of-the-money call options. Therefore, when the VIX spikes up, SVOL's call options on the VIX increase in value. This offsets the risk of a massive loss. This forms the basis for what the fund describes as a derivatives overlay.

They enhance their returns by using reverse repurchase agreements from the US Government. Reverse repurchase agreements are primarily used by the Fund as an indirect means of borrowing. Reverse repurchase agreements are contracts in which a seller of securities, for example, U.S. government securities or other money market instruments, agrees to buy the securities back at a specified time and price.

Trading Strategy Example

Suppose the current spot price of VIX is at 15 (this would be considered on the lower end of the 'moderate' category for VIX). Further, suppose that the VIX futures position expiring in one month is trading at $14 and the VIX futures position expiring in three months is trading at $16. This is representative of a futures market in contango.

- Spot VIX: 15

- Near-term VIX Futures Contract (1-month expiration): $14

- Longer-term VIX Futures Contract (3-month expiration): $16

Today, we would short the VIX futures at $16 with the intention of buying it back later at a lower price.

- Short VIX futures expiring in 3 months at $16.

Now there are two potential outcomes. In the first scenario, we assume that the VIX decreases over the next 3 months. In the second scenario, we assume that the VIX increases over the next 3 months:

- Scenario 1 - Decrease in VIX

- After 3 months, the longer-term contract price drops to $12 at which point you would buy back the contract to close your short position.

- This would earn $4 per contract ($16-$12).

- Scenario 2 - Increase in VIX

- After 3 months, the longer-term contract price increases to $18 at which point you would buy back the contract to close your short position.

- This would lose $2 per contract ($16-$18).

Note that there are other considerations in practice including but not limited to, transaction costs, margin requirements, and potential adjustments to the position as market conditions change. The strategy tends to do well because of the mean reversion of VIX.

The VIX is often in contango however, a similar strategy could be performed in a backwardation market which is less frequent.

Final Commentary

SVOL offers investors a low-cost MER fee for an actively managed, complex strategy. Simplify as an ETF provider has been growing with AUM now exceeding $2 billion . Investors of this fund should consider the size of SVOL and the ETF provider before making any investment decision.

By taking advantage of the VIX commonly being in contango and the mathematical property of mean reversion, SVOL is able to provide investors with a high yield. There are a variety of different risks inherent within the strategy and the return is not risk-free. For investors looking at a different source of equity income to add to their portfolio, SVOL may be an option.

For further details see:

SVOL: Unveiling The Strategy And Enhancing Investor Diversification With Income Potential