QSWN - SWAN's Deep Dive Likely Over

2023-10-24 20:28:12 ET

Summary

- Amplify’s SWAN was launched on November 6, 2018, meeting all expectations through the December 2018 market swoon, the market’s 2019 recovery, and withstanding the 2020 Covid-19 crash.

- As previously warned, the Achilles heel of SWAN is market declines due to high inflation/rising interest rates, which is exactly what occurred in 2022 through Oct. 2023.

- With 10-year Treasury yields of almost 5%, inflationary pressures seemingly receding, and reduced recessionary fears, SWAN appears poised to protect against large market drawdowns due to non-inflationary factors.

- The expected one-year return for SWAN, ISWN, and QSWN is 90% times the treasury return (4.9% yield) plus 40% times the underlying index return, S&P 500, EFA, or Nasdaq 100.

Amplify BlackSwan Growth & Treasury Core ETF (SWAN) invests 90% in a treasury ladder composed of approximately equal weights in 5 to 10-year Treasuries while investing 10% in 70 delta (on average 6.5% in-the-money) long-term call options (LEAPs) on the S&P 500. My previous article Singing Swan Amid The Covid-19 Crisis in May of 2020 outlined how SWAN was performing exactly to expectations by avoiding large losses during significant equity market declines while participating in market gains.

With 10-year Treasury yields at 0.7% in May of 2020, I outlined two major concerns. The first was there would be almost no additional return to treasuries over the following year and to quote myself on the second issue:

The biggest concern going forward is rampant inflation pushing yields up while the S&P 500 simultaneously declines. Both the option and treasury component of SWAN would experience losses.

Since SWAN tends to operate like a 40/90 stock/bond portfolio as opposed to the classic 60/40, my predictions over the next year were 40% of the market return and 90% of the treasury return (expected to be less than 1%). From June 2020 to Dec. 2020, the S&P 500 increased 23% while SWAN increased 9.8% despite a 1% loss in treasuries. 2021 saw similar figures, another 23% increase in the S&P, SWAN up 9.3%, treasuries down -2.5%. Both results slightly outperformed my 40/90 ex ante estimates.

What occurred next in 2022 met all the conditions of my biggest concern, rampant inflation, higher yields, and a significant decline in the S&P 500. Below is a brief synopsis of what SWAN is, what happened in 2022, and what is the outlook for SWAN going forward with 10-year Treasury rates close to 5%.

SWAN's Rationale

SWAN is not an actively managed fund. It holds approximately 90% in treasuries and 10% in long-term call options. However, SWAN's target bond holdings have changed in the last year from using a bond ladder to target the same duration as the 10-year Treasury to an intermediate target duration using a 5 through 10-year Treasury step ladder. This has moderately reduced SWAN's duration and by implication, interest rate risk.

SWAN rebalances its options only twice a year (5% in late May/early June and 5% in late November/early December), and only with the options coming due (third week of June or December) back to 5%, these exposures can vary. As of Oct. 20, 2023, the treasury/option exposure is approximately 91%/9%. Mid-covid crisis, the option exposure had fallen to 1.4% as an example of the fluctuations. Amplify has two similar funds, one for international markets ( ISWN ) and tech ( QSWN ).

Historically, these barbell-type portfolios have performed relatively well, especially in times of market turmoil when investors tend to rush to safety. Table 1 shows the returns during informative time periods for SWAN, the S&P 500 index, 10-year Treasury or IEF , ISWN, MSCI EFA index, QSWN, and Nasdaq 100, the latter indexes relevant to ISWN and QSWN. Although SWAN wasn’t introduced until 2018, (Trainor, Chhachhi, Brown , 2019) did extensive research on this strategy using data from 1990 through 2015. The first six rows show what occurred to the S&P 500, the 10-year T-note, and SWAN during periods of market turmoil.

Table 1: Return comparisons for SWAN, ISWN, and QSWN during market crashes and/or since inception.

{kind=link}

The main point to note is SWAN did not suffer the losses of the S&P 500 during the 2000/01 tech crash or the 2008 financial crisis as the 10-year treasury offset options losses. The only minor exception was the 11/30/2001 to 5/31/2002 where the 10-year was flat and the market fell just enough to whittle away a large percentage of the option value, SWAN -7.8% vs S&P 500 of -5.7%. By avoiding the major market losses with significant participation in gains, SWAN performed slightly better than the S&P 500 itself over this period, 10.9% to 10.4% although it was never meant or expected to be a 100% equity replacement and this was a very good period for 10-year Treasuries which had a geometric return of 6.8%.

Shortly after Amplify introduced SWAN in 2018, the market had a rather abrupt correction and lost -15.7% in less than 3 weeks. SWAN performed as expected and only lost -6.7%, thus mitigating losses during market corrections as touted. Admirably, in 2019 as the S&P 500 index increased 28.9%, SWAN participated substantially increasing 22%. Although the decrease in rates certainly helped over this time frame with iShares' IEF (7 to 10-year Treasury ETF used as a proxy for Amplify's bond holdings) increasing by 8% while the options component added another 14% to the total return of SWAN.

The COVID crash again validated SWAN’s underlying theory with the S&P 500 index falling almost 34% in a little over a month while SWAN only fell 7.7%, again helped by treasury returns as IEF’s 6.5% return over this period demonstrates. SWAN similarly did well for the rest of 2020 and in 2021, despite small treasury losses as the option gains more than made up for the treasury losses.

Sinking Swan

In a rare occurrence, both bond and equity markets swooned in 2022 eliminating any floor or offsetting losses that bonds usually provide when equity markets significantly decline. The 10-year Treasury yield increased more than 2% to approximately 4% by the end of 2022. This resulted in treasury losses of -16% in the calendar year 2022. Couple this with losses in all three indexes of 14% or more, the percentage loss in options was 90% or more adding another 10%+ in losses based on the option percentage in the portfolio at the beginning of the year. Option weights were 13.5%, 8.9%, and 14.1% for SWAN, ISWN, and QSWN respectively at the beginning of 2022.

Through October 17, 2023, rates have continued to rise to almost 5% causing another -3.6% (90% x -4%) in bond losses for these funds. The option gains have offset these losses, almost 4% for SWAN and more than 13% for QSWN while EFA option returns have been mostly flat. Thus, the option portion of these ETFs is indeed allowing participation in the upside and significantly so given they are only approximately 10% of the ETF. Unfortunately, the bond portion continues to be a drag.

It should be noted that 2022 was the worst year in history for a typical 60/40 stock/bond fund since at least the 1930s, -17%, ( Wallerson , Oct. 19, WSJ). Figure 1 shows the annual returns to the S&P 500 and the 10-year treasury since 1970 further enforcing the outlier nature of 2022.

Author

Not since 1977 to 1981 when rates increased from 7.5% to over 15% have rates increased so dramatically and even then, the high yields helped ameliorate the capital losses which were also smaller for any given increase in interest rates as the duration was smaller. The largest loss during this period was less than -9% (Feb/1977 to Feb/78). (Technical note: duration approaches maturity as yields approach zero, i.e., a zero-coupon bond has a duration equal to maturity. As a refresher, percentage change in bond price equals -duration * change in yield.)

Looking Ahead

If you know how the SWAN suite of funds works, then when 90% of the portfolio loses 16% and the market declines enough to virtually wipe out the option value, it is simple enough to add the two up to calculate losses. If the option percentage is even higher than the base 10% due to rising markets when you invest in or hold SWAN, ISWAN, or QSWAN, then exposure to option losses (or gains) is even greater. There are no mitigating losses using SWAN, 60/40, 40/60, or any other combination when both the bond and equity markets are experiencing significant losses.

Fortunately (I think…) we have moved from an environment that had less than a 1% yield on 10-year Treasuries with little to no room for large capital gains during flights to safety to almost 5% today with the bonus of a positive after inflation-adjusted real return. At this point, the SWAN group appears to be in a much better position to weather minor increases in yield and should have limited losses to large market crashes not induced or coincident with increasing interest rates.

Predicting yields a year from now is a bit safer than predicting where the stock market will be but be wary of any forecasts including this one. Historically, there is an 81% chance the 10-year yield will be +/- 0.8% from where it is today based on monthly data from 1871 to Oct. 2023, see Figure 2. There was only a 1% chance of the 2.4% increase in yield seen in 2022. It is not impossible for yields to increase another 2.4% over the next year, but highly unlikely, famous last words. Thus, my best guess for next year’s yield is what it is now, 4.9%, which is fairly close to the 150-year average of 4.5%. Even if rates increase another 0.8%, the interest earned should offset that capital loss.

Author

Return predictions for SWAN, ISWN, and QSWN over the next year are approximately 0.90 x 4.9% + 0.40 x the underlying index return, S&P 500, EFA, and QQQ respectively. The 40% of the index return for SWAN is based on an analysis of the 10% option position since 1990. The 40% equity participation rate for ISWN and QSWN does not have enough empirical history to validate the 90/40 bond/stock rule. However, Trainor, Cupkovic, Chhachhi, Brown (2020), albeit using a slightly different methodology than Amplify, found a higher equity participation rate using EFA and slightly smaller for QQQ.

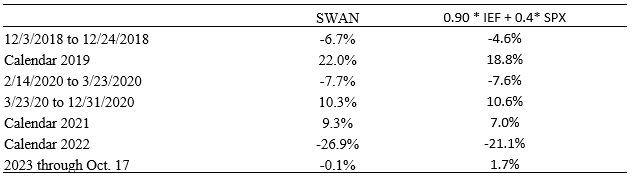

If considering or already invested in these ETFs, a rebalance of the options is approaching and will be made in late November/Early December. The options are held for 1 year and a day to qualify for the capital gains tax rate. As of Oct. 20, 2023, the percentage in options for the SWAN, ISWN, and QSWN are 9.2%, 7.2%, and 13.9% respectively. Table 2 shows the results using the 90/40 bond/stock idea for the time periods in Table 1. Except for 2022 when the 90/40 idea calculated -21.1% for SWAN (actual -26.9%), the calculation continues to be fairly accurate even with the fluctuating option percentages. As mentioned earlier, much of the actual loss in 2022 can be explained by the higher option percentage at the beginning of the year which was almost completely lost.

Table 2: Comparison of SWAN returns to an estimated 90/40 IEF/SPX portfolio.

{kind=link}

Conclusion

Amplify’s treasury/index option products clearly had their “feathers” ruffled in 2022, but this was the case for any bond fund. iShares' IEF (7 to 10-year Treasuries) lost 16% in 2022 and another -4.2% through Oct. 20, 2023. To the extent a 60/40 or 40/60 portfolio is no longer a valid idea due to one bad year, then neither should SWAN's 90/40 bond/stock "option" be discarded.

With a duration of approximately 7, the treasury portion of the SWAN suite will lose 7% for every 1% increase in rates. It can also gain 7% for a 100-basis point decrease in rates. In addition, unlike 2020/21 with 0.6 to 1.5% yields, there is now a 4.9% yield to help offset capital losses or add to gains. With the political uncertainty in the Middle East, Ukraine, Taiwan, etc. which may cause an increase in global uncertainty or some unexpected deep recession, SWAN is becoming an increasingly attractive alternative once again to defend against non-inflationary induced market declines while also participating in market gains.

For further details see:

SWAN's Deep Dive Likely Over