PPRUF - Swatch: A Luxury Outlier

2024-01-14 08:44:58 ET

Summary

- In line with the entire luxury sector, Swatch Group's stock has lost momentum over the past year. But it's due for recovery.

- Swatch's revenue growth accelerated and margins expanded in H1 2023. The company's outlook is encouraging too.

- While a further slowing down in the luxury market can't be overlooked, its muted market multiples still make a Buy case for the stock.

If there were any example of a stock losing momentum due to investor diffidence about the sector, it would be the Swatch Group (SWGNF) (SWGAY). In its last financial update for the first half of 2023 (H1 2023), the performance was robust and it had a positive outlook for the full year 2023 too, which I covered in my last article on it. It even saw its biggest single day gain of 8% in 2023 on release.

However, cut to now, and it's down by 21% over the past year (see chart below), having lost momentum soon after it saw the price spike. With its full-year results due in the next couple of weeks (the actual date isn’t known), here I take a look at what’s in store for Swatch in 2024.

Price Chart (Source: Seeking Alpha)

{kind=link}

The bigger picture

The luxury market is seeing a post-pandemic normalisation, most specifically noted in the US market, which saw a nosedive just when the China market reopened after its lockdowns. This is evident in their sales numbers and has also been reflected in their prices (see chart below).

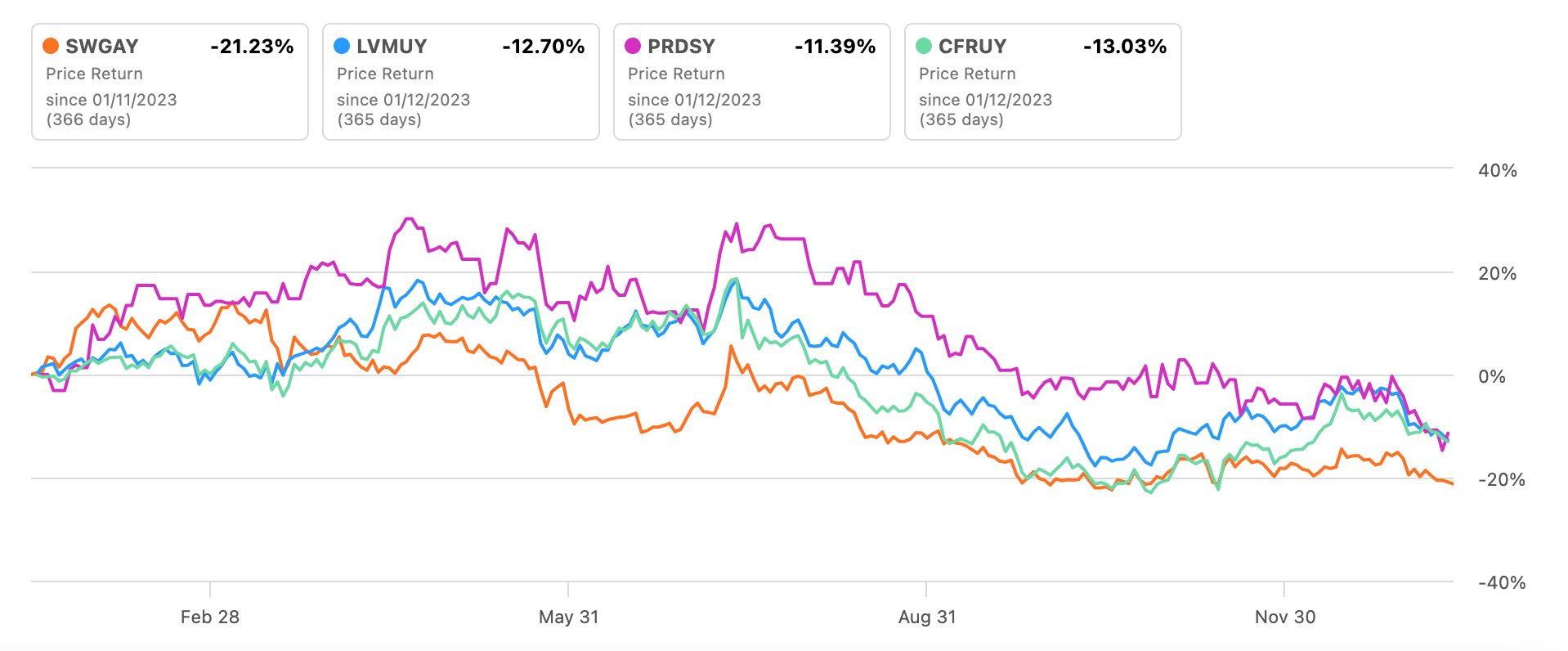

Price Returns for Key Luxury Stocks (Source: Seeking Alpha)

{kind=link}

Here, I’ve considered only LVMH (LVMUY), Richemont (CFRUY) and Prada (PRDSY), and left out the other two big luxury names Kering (PPRUY), which is facing a specific set of challenges and Hermès (HESAY), which is in its own league .

The key point to note in the price change comparison is that Swatch has seen the biggest price decline of the four. One reason for this could be its lower operating margins, which were at 15.5% in 2022. This compares to 18%+ margins for Prada and 25%+ for LVMH and Richemont.

Margins were particularly important in the recent past, as they were a good indication of a company’s ability to pass on higher costs to consumers in a time of elevated inflation. Also, unlike the peers considered, Swatch has relatively low-priced brands like its namesake brand, which could be more susceptible to margin contraction than premium luxury brands like Harry Winston and Omega.

However, with inflation subsiding, the margins are less of a worry now after inflation has subsided nearly to trend levels. Also, Swatch's own margins have inched up in H1 2023 to 17.1% anyway.

What to expect for the full year 2023

Sales slowdown or not?

Another reason for investor caution with the Swatch stock could be analysts' outlook. Analysts estimates put the annual sales growth at 15.5% in USD terms, which amounts to a 6.7% increase in Swatch’s home currency terms, the CHF. This is almost the same level of growth seen in 2022.

But the company’s own recent numbers and outlook indicate otherwise. Here’s how.

- Swatch has been an outlier among luxury companies in H1 2023, in that its sales growth accelerated to 18% year-on-year (YoY) in constant currency [CC] terms (H1 2022: 7.4%).

- While adverse foreign exchange movements lowered reported growth to 11.3% (H1 2022: 6.5%) (see table below), the growth was way ahead of last year despite a much bigger currency impact of 6.7 percentage points (pp), compared to the 0.9pp in H1 2022.

- H2 2023 sales will be on a favourable base since the company saw a 0.9% sales decline in H2 2022.

- In its outlook, Swatch expects “excellent growth opportunities in local currencies for the second half of 2023 in all regions and price segments.”

{kind=link}

In sum, considering the slowing down in the rest of the luxury companies, some cooling off in growth can be anticipated, but maybe not to the extent of last year’s levels.

Elevated margins can sustain

I believe that there’s also a good chance for margins to sustain irrespective of how much sales grow. And that’s down to one word. Inflation. The company’s cost of sales has been declining for the past two years, and going by the latest trends in producer prices, the trend could have continued.

The only risk to costs is accelerated operating expense growth, which was 68.8% of the revenues in H1 2023, and grew by a much higher 11.45% compared to a 5.1% rise in 2022.

Estimating 2023 earnings

To get an earnings estimate, I assume that the full-year revenue growth slows down to 9%, which is the average of analysts’ estimates in CHF terms and the company’s reported sales growth rate in H1 2023. This results in a slowing of 6.7% in sales growth in H2 2023. Assuming that the net profit margin remains unchanged at H1 2023’s level of 12.4%, the company would still see a 23.2% earnings growth, however.

Attractive market multiples

The expected earnings figure of USD 1.2 billion results in a forward price-to-earnings (P/E) ratio of 10.9x, which is lower than the 11.7x it was at the last I checked. This is significantly lower than those for LVMH at 21.5x and Richemont at 18.6x.

Even keeping in mind that it isn’t pure luxury like the two considered, the forward ratio is still lower than its own TTM P/E of 15.2x, which is trading even lower than that for the consumer discretionary sector at 17.9x.

If we add its 2.6% forward dividend yield to the equation and a history of consistently paying dividends for the last 13 years, the current price levels just don’t add up.

What next?

I’m tempted to for the first time in all my time of writing for Seeking Alpha to upgrade the rating to Strong Buy. But to stay cautious I’m retaining a Buy rating on the stock considering that there’s a possibility of a significant growth slowdown in its upcoming full-year result in 2023. Also, if the foreign exchange movements were even more adverse, as also pointed out as a risk factor by Swatch itself, sales could be impacted.

Even then, it’s expected to see earnings growth, which in turn means it can continue to pay dividends. Further, its P/E is also muted compared to both luxury stocks and the consumer discretionary sector, which indicates a potential for a price rise sooner rather than later.

For further details see:

Swatch: A Luxury Outlier