CFRHF - Swiss Helvetia Fund: A Pricey Play On A Region Poised For Near-Term Underperformance

Summary

- The performance of the Swiss Helvetia Fund hasn't been great in recent years despite the elevated expense ratio.

- Its defensive exposure could also underperform as we head into a risk-on market environment this year.

- While the fund trades at a NAV discount, I won't be buying anytime soon.

The Swiss Helvetia Fund (SWZ), a closed-end fund managed by Schroders (SHNWF) offering investors exposure to Swiss equities, has held up predictably well through last year's turbulence. The defensive characteristics of Swiss large caps, which the fund is particularly exposed to, make it a worthy portfolio addition during risk-off periods. More pertinently, heading into what has been a risk-on year so far, these equities tend to lag during risk-on periods. Adding to the headwinds is the fund's outsized expense ratio and underwhelming stock selection track record, which look likely to result in further underperformance vs. the benchmark Swiss Performance Index.

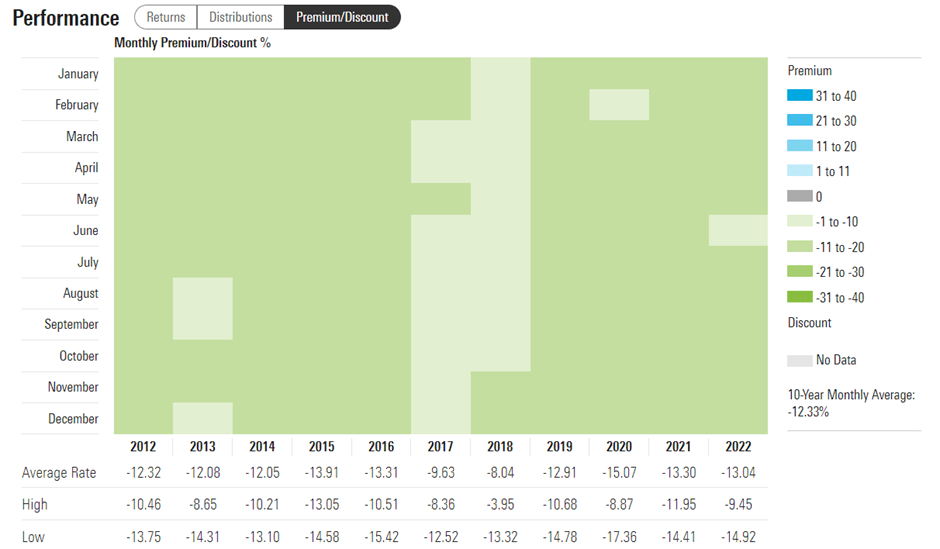

And while the Swiss economy has been resilient, monetary policy remains a key risk to valuations. Despite Switzerland's inflation coming in well below the rest of the Eurozone, the Swiss National Bank's ((SNB)) long-term inflation forecast remains pegged at >2% inflation through FY25, signaling a preference for policy tightening. Unlike the ECB, the central bank also hasn't yet announced a balance sheet reduction objective with regard to its stock and bond holdings, presenting another potential overhang on valuations. So while the Swiss Helvetia Fund currently trades at a mid-teens % discount to NAV and has a buyback in place for up to 250k common shares, I won't be adding this to my portfolio anytime soon.

{kind=link}

Fund Overview - A Pricey Vehicle for Exposure to Swiss Blue Chips

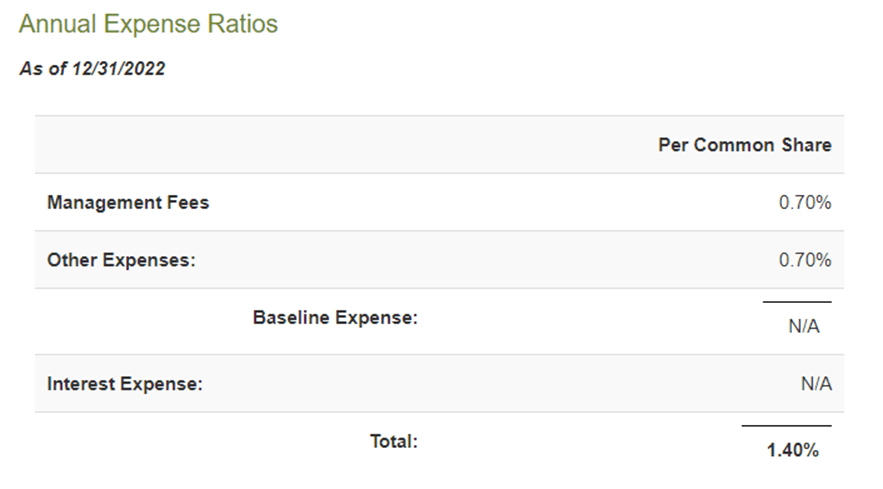

The Swiss Helvetia Fund is a closed-end investment fund listed on the New York Stock Exchange with the objective of achieving long-term capital appreciation through investments in Swiss equities traded on the Swiss stock exchange or other major European stock exchanges. The closed-end fund held ~$125m of net assets at the time of writing, well below the ~$152m in reported net assets in FY21. The fund maintains a 1.4% total expense ratio (as a % of average assets), with ~70bps going to management fees to Schroders, making it one of the more expensive options on the market for investors looking to access Swiss equities.

{kind=link}

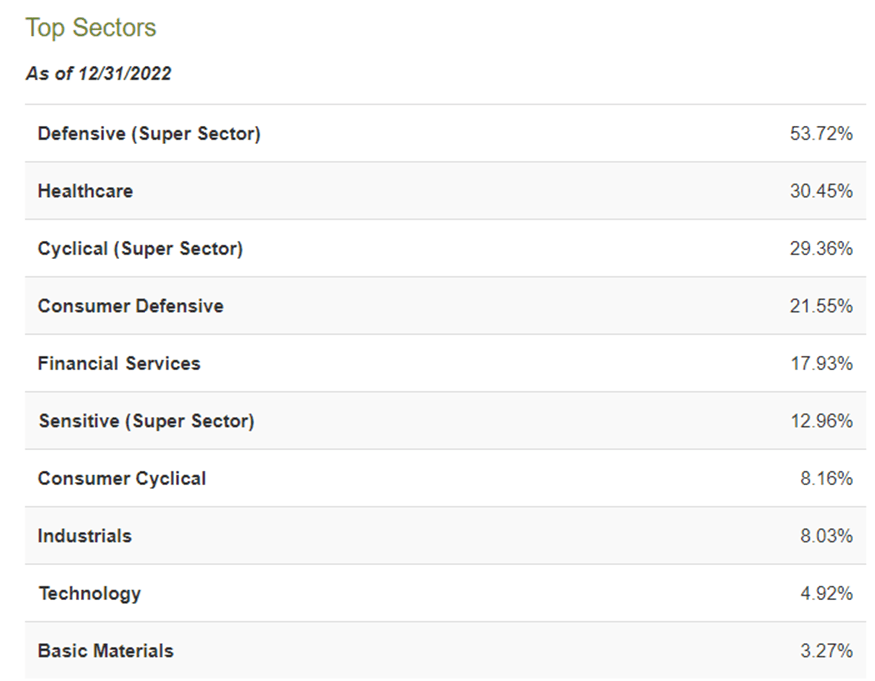

The fund's sector allocation skews toward the healthcare (30.5%), consumer staples (21.6%), and financial services (17.9%) sectors, which accounted for a combined ~70% of the total portfolio as of December 31, 2022. Broadly speaking, the allocation reflects a defensive stance, with 53.7% of the portfolio in defensive stocks; 29.4% and 13.0% are in cyclical stocks and more sensitive super-sectors, respectively. The manager has maintained a similar sector weight throughout the fund's operating history, largely tracking the composition of the benchmark Swiss Performance Index.

{kind=link}

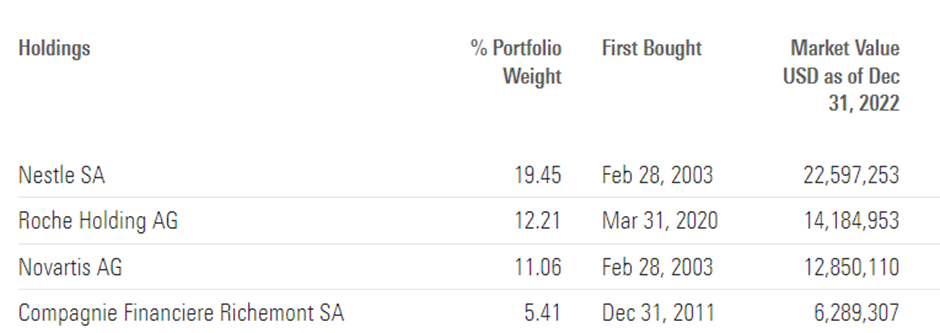

The fund's largest holdings are Swiss blue chips like Nestle SA ( NSRGY ) (19.5%), Roche Holding AG ( RHHBY ) (12.2%), Novartis AG ( NVS ) (11.1%), and Compagnie Financiere Richemont ( CFRHF ) (5.4%). The fund has generally maintained a similar composition of stock holdings over the years, as reflected by its low 11% portfolio turnover. All in all, the top ten holdings account for a cumulative ~64% of a 50-stock portfolio, so this is a fairly concentrated fund.

{kind=link}

Below Par Fund Performance; Acceptable Distribution Yield

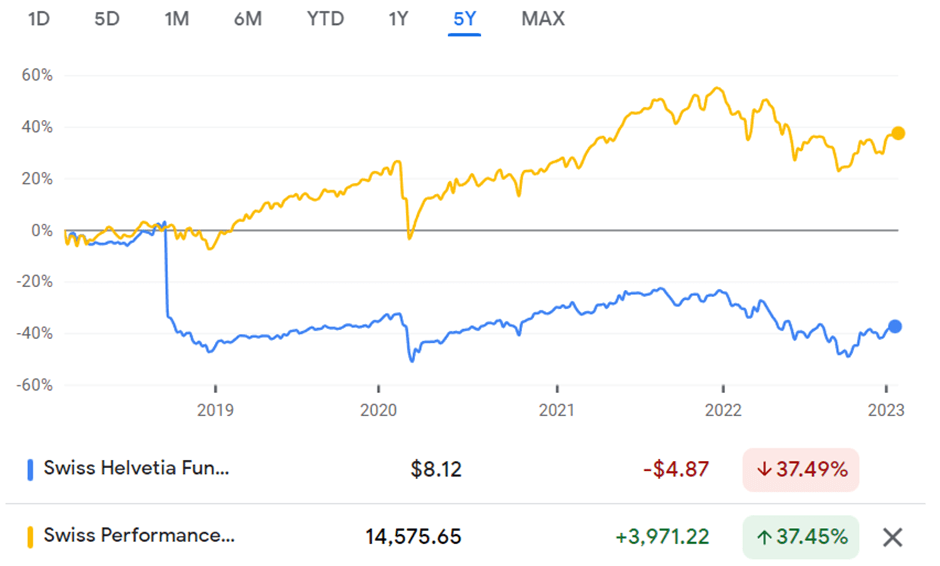

Since Schroders took over management of the fund in FY14, relative performance has been far from impressive. On a YTD basis, the fund's returns stand at 7.0% vs. 3.5% for the benchmark Swiss Performance Index but zooming out to a five-year timeline, the fund has underperformed the index by a wide margin despite the high expense ratio.

{kind=link}

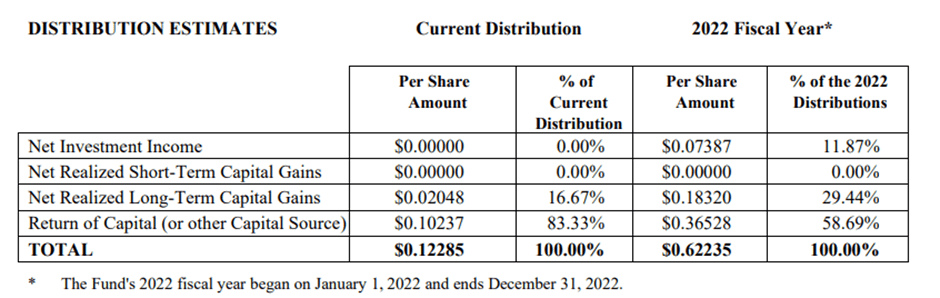

The fund does pay out good quarterly distributions through the cycles, however. Last year saw $0.62/share of distributions, implying a trailing yield of ~8%, despite equity market declines. Most of the payout (~59%) came from capital returns, in line with prior years, with the income portion typically coming in the first two quarters of the year.

{kind=link}

Switzerland - a 'Safe Haven' Set to Underperform

The defensive characteristics of the Swiss equity market are likely a key reason many investors include SWZ in their portfolios - many of the leading Swiss blue chips like Nestle and Richemont tend to generate strong cash flows regardless of the economic backdrop, allowing for outperformance when growth slows. While this was a great reason to own SWZ last year, the backdrop this year is much different. Recent data points from the Swiss economy point to a more resilient outcome this year (albeit with slower economic growth) on solid private consumption and a tighter labor market . Further, structural inflation is slowing as price regulation limits the impact of energy prices on households and a strong CHF continues to offset pressures from imported inflation. With a global recovery on the cards, risk-on assets are increasingly catching a bid, and thus, I suspect Swiss blue chips and, by extension, SWZ will lag the broader rebound.

The other key risk I see is the relative hawkishness of the Swiss central bank, the SNB. Having raised the policy rate in December by 0.5%pts to 1%, SNB commentary indicates it continues to see the policy as accommodative. This view is consistent with the SNB's long-term inflation forecast, which pegs inflation at >2% in 2025 (assuming an unchanged policy rate). Thus, there could still be more tightening on the horizon, either via more hikes or through a balance sheet reduction. In contrast to the European Central Bank, the SNB has not announced any balance sheet reduction objective despite still holding a sizeable securities portfolio. With the ECB already on track to reduce its securities holdings at a EUR15bn/month pace in March, the pressure could soon be on the SNB to follow suit. The risk of further tightening presents an incremental overhang on Swiss valuations, potentially driving relative underperformance ahead.

A Pricey Play on a Region Poised for Near-Term Underperformance

Swiss equities have traditionally earned a reputation as a 'safe haven' due to their defensive characteristics; the relative outperformance of the Swiss Helvetia Fund last year was a case in point. I would push back on owning SWZ at this juncture, though, particularly with FY23 shaping up to be a risk-on year (vs. risk-off when being defensive outperforms). Plus, the fund's expense ratio is very high at 1.4% in FY22, with ~70bps collected by Schroders despite a long track record of underperformance relative to the fund's benchmark. Finally, the more hawkish Swiss monetary policy stance poses a greater risk to valuations than many of its European peers - the SNB's long-term inflation forecast remains at >2% in FY25, while a balance sheet reduction plan (in line with the ECB) could emerge as a negative catalyst. So even at the current mid-teens % discount to NAV, I see an unattractive risk-reward to owning the fund here.

For further details see:

Swiss Helvetia Fund: A Pricey Play On A Region Poised For Near-Term Underperformance