SSREY - Swiss Re: Continued Growth In Premiums And Return On Equity

2023-12-19 18:47:56 ET

Summary

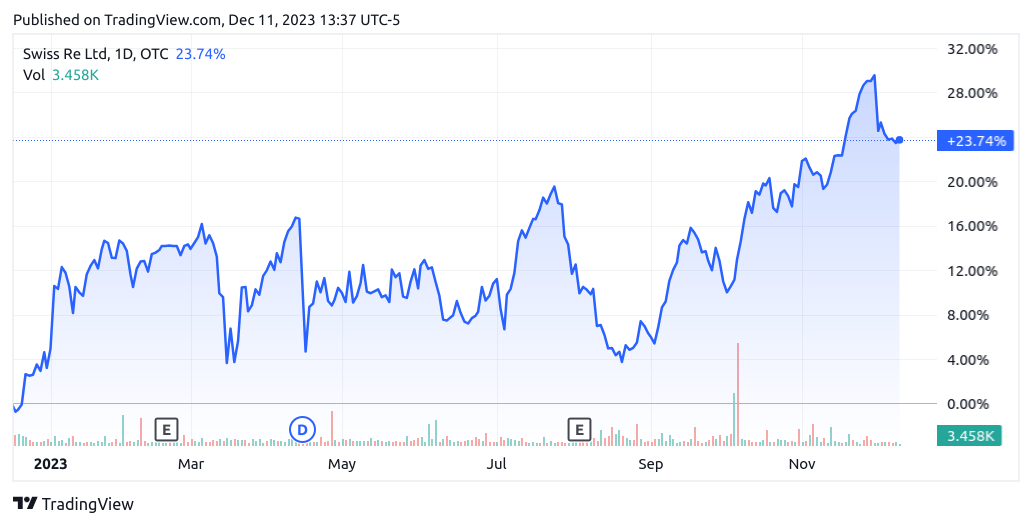

- Swiss Re has seen a 23.74% increase in stock price this year.

- Net premiums earned, and net income have both shown growth in the third quarter.

- The drop in the combined ratio indicates that premium growth is outpacing costs and expenses.

Investment Thesis: I continue to take a long-term bullish view on Swiss Re given strong premium growth and an upward trend in return on equity.

In a previous article back in October, I made the argument that Swiss Re AG ( OTCPK:SSREY ) has the potential to see further growth going forward, on the basis of continued premium growth and a drop in the combined ratio across the Property & Casualty segment.

Overall, the stock has ascended by 23.74% over the course of this year:

{kind=link}

The purpose of this article is to assess whether Swiss Re has the ability to see continued growth from here taking recent performance into consideration.

Performance

When looking at the nine-month earnings results of 2023 for Swiss Re (as released on November 3 2023), we can see that net premiums earned are up by over 4% on that of the prior year quarter, with net income having strongly rebounded into positive territory.

Swiss Re Press Release: 9M 2023

Net income growth was largely driven by underwriting performance due to successful renewals and rising investment income. Additionally, the combined ratio across P&C Reinsurance is down to 94.3 from 106.1 in the prior year quarter - which was particularly impressive considering that the company incurred USD 421 million worth of catastrophic losses in the third quarter - due to the earthquake in Morocco as well as severe weather events in Europe and wildfires on the Hawaiian Island of Maui.

Figures sourced from historical Swiss Re News Releases. Heatmap generated by author using Python's seaborn library.

In addition to the strong rebound that we saw across P&C Reinsurance, we can see that L&H (Life & Health) Reinsurance also saw significant growth - with net income up by 186% on that of the prior year's quarter.

Swiss Re Press Release: 9M 2023

Key Updates

The performance that we have seen for Swiss Re in the previous quarter continues to fit into my ongoing bullish thesis for the stock, given that:

- The combined ratio has continued to fall from the prior year's quarter in spite of ongoing catastrophic losses.

- Premium growth across both P&C and L&H has continued to rise significantly.

With that being said, it is also notable that large natural catastrophe claims for the first nine months of 2023 came in at USD 1.1 billion, as compared to USD 2.5 billion for the same period in 2022. In this regard, an increase in catastrophic losses could still stand to place upward pressure on the combined ratio going forward, and this may not be counteracted by continued premium growth.

Valuation

With regards to the company's price-to-book and return on equity metrics, we can see that the former is currently trading at a five year-high.

price-to-book

YCharts.com

When comparing this ratio to competitors Zurich Insurance Group AG ( OTCQX:ZURVY ) and Reinsurance Group of America, Incorporated ( RGA ), we can see that Swiss Re's price-to-book ratio still trades lower than that of competitor Zurich Insurance Group, yet significantly higher than that of Reinsurance Group of America.

YCharts.com

Additionally, we can see that return on equity has continued to rise and is currently at a five-year high - albeit lower than that of Zurich Insurance Group and Reinsurance Group of America.

Return on Equity

YCharts.com

From this standpoint, I take the view that Swiss Re has the capacity to continue to see upside from here, given that 1) its price-to-book ratio trades lower than that of competitor Zurich Insurance Group and 2) return on equity continues to see upside.

Up until last year, insurers had seen outperformance in general based on higher price-to-book values - this had largely been due to unrealized losses, which had caused significantly lower book values. However, ratings agency Fitch had recently expressed their view that unrealised losses on bonds would be captured in shareholder's equity over time as bonds approach par value leading up to maturity. Under this scenario, it is quite possible that we could see the price-to-book value for Swiss Re revert back near to 1 - having traded around this range for the period 2019-2022.

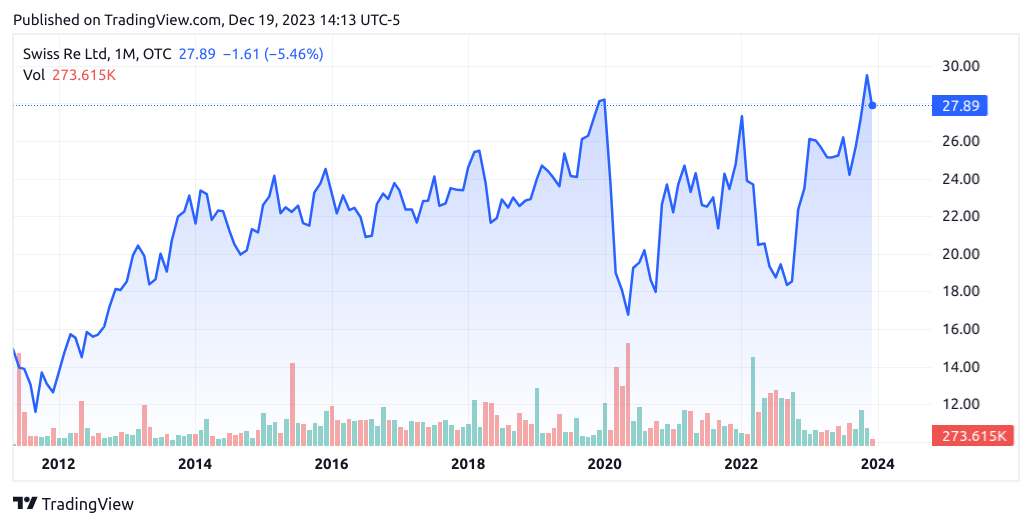

In this regard, I take the view that fair value for Swiss Re is reflected in the current price of $27.89 given a higher price-to-book ratio - the price of which is trading near a 10-year high.

{kind=link}

However, I take the view that the stock has room for longer-term upside if we see the price-to-book ratio start to moderate, and both premium growth and return on equity continue to climb.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the drop in the combined ratio for Swiss Re in the most recent quarter is quite impressive given that the company did see significant catastrophic losses in the third quarter. This indicates that premium growth is substantially outpacing costs and expenses associated with funding claims.

Going forward, I take the view that net premium growth across the Property & Casualty segment has the capacity to continue rising - and combined ratio performance to date has been impressive. Specifically, Swiss Re foresees that the underlying trends of increased urbanisation, inflation and extreme weather events - demand for property reinsurance is expected to remain high as exposures continue to increase.

In terms of the potential risks to Swiss Re at this time, we are seeing risks across the P&C sector, in that while we have seen the segment demonstrate vibrant premium growth of late - risks are also increasing across the sector due to increased catastrophic losses - and Swiss Re ultimately needs to ensure that the company can generate sufficient return to compensate for this increased risk.

Moreover, while recent performance across the segment has been encouraging and the first half of this year saw modest losses - recent performance does not make up for the five to six years of under-performance that Swiss Re ultimately saw across this segment. As retentions across the industry are set to increase and ultimately place more of the risk with the customer, this could place downward pressure on premium demand.

Conclusion

To conclude, Swiss Re has seen encouraging growth in premiums and net income across the P&C sector. While the P&C sector is likely to see risk exposure increase going forward, I take the view that the company has the capacity to continue premium growth to counteract this.

In this regard, I take the view that Swiss Re is currently trading at fair value given an elevated price-to-book ratio. However, I take the view that this is a temporary situation given the prior impact of unrealised losses and the company's financial performance remains strong. While a high price-to-book ratio may cause the stock to consolidate in the short-term, I continue to take a bullish view on Swiss Re and see capacity for further long-term growth given strong performance across premium growth and return on equity.

For further details see:

Swiss Re: Continued Growth In Premiums And Return On Equity