SSREY - Swiss Re: Strong Net Income Growth Despite Losses

2023-07-11 20:59:13 ET

Summary

- I revise my view on Swiss Re to bullish.

- Swiss Re is in a good position to meet its 95% combined ratio target by the end of this year.

- The company has demonstrated the ability to reduce its combined ratio and bolster net income in spite of higher catastrophic losses.

- Despite potential risks from inflationary pressures increasing the cost of claims, Swiss Re is seen as effectively managing this risk, with fixed income reinvestment remaining a valuable income source.

Investment Thesis: I revise my long-term view on Swiss Re to bullish, given strong net income growth in spite of higher catastrophic losses in Q1 2023, as well as continued strong performance for the company's fixed income allocation.

In a previous article back in March, I made the argument that Swiss Re ( SSREY ) may see limited upside in the short to medium-term, on the basis of an uncertain macroeconomic environment and a potential slowdown in fixed income growth if recessionary conditions warrant a slowing down of rate hikes.

Since then, the stock has ascended slightly to a price of $25.11 at the time of writing:

{kind=link}

In this article, I wish to make the argument that Swiss Re has the capacity to see further upside from here - by continuing to bolster premium and net income growth, along with being on track to meet its target of a combined ratio below 95% by the end of this year.

Performance

When looking at the most recent financial results for Swiss Re, we can see that the Property & Casualty segment has shown growth in both net premiums earned and net income - as well as a decrease in the combined ratio.

Swiss Re Press Release: Q1 2023

The reason I highlight performance across the Property & Casualty segment in particular is that this represents the largest portion of Swiss Re's business by net premiums earned - accounting for 53% of overall net premiums earned for Q1 2023, with L&H Reinsurance and Corporate Solutions accounting for 35% and 12% respectively. As a result, performance across this sector is likely to set the overall trajectory for Swiss Re's growth prospects going forward.

To get a broader overview of combined ratio fluctuations across Property & Casualty for Swiss Re - I decided to generate a heatmap of the combined ratio for the periods from 2019 to the present:

Figures sourced from historical Swiss Re News Releases. Heatmap generated by author using Python's seaborn library.

When looking at the above heatmap, we can see that the ratio is down significantly from 2021 onwards (the high combined ratios we saw in 2020 were largely due to the effects of COVID-19).

It is also noticeable that in the last two years - the combined ratio for the latter two periods of the year (9M and FY) have been higher than that of the former two periods (3M and 6M). According to Swiss Re, the business makes the majority of its natural catastrophe premiums in the second half of the year. Moreover, with risks to properties being higher in the winter months due to adverse weather conditions - we would expect to see a rise in the combined ratio in this regard.

With that being said, Swiss Re was able to increase net income to USD 369 million in Q1 2023 from USD 85 million in Q1 2022 in spite of large natural catastrophe claims as a result of the Turkey-Syria earthquake - for which the company recorded USD 426 million in net claims.

L&H Reinsurance and Corporate Solutions also continued to see growth - with net income for the former up from -$230 million in Q1 2022 to $174 million in Q1 2023, along with growth from $81 million to $168 million for the latter.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the fact that net income growth proved resilient to a higher degree of natural catastrophe claims for Q1 gives me more confidence that Swiss Re can contain an anticipated rise in the combined ratio for the second half of the year.

The company has a target of achieving a full-year combined ratio below 95%, and a combined ratio of 97.2% for this quarter is quite impressive taking into consideration a large degree of catastrophic claims in this quarter driven by the Turkey-Syria earthquake. The results for the half-year of 2023 will be a significant milestone in determining whether Swiss Re is on target to achieve its 95% target - but its performance in the most recent quarter looks quite impressive.

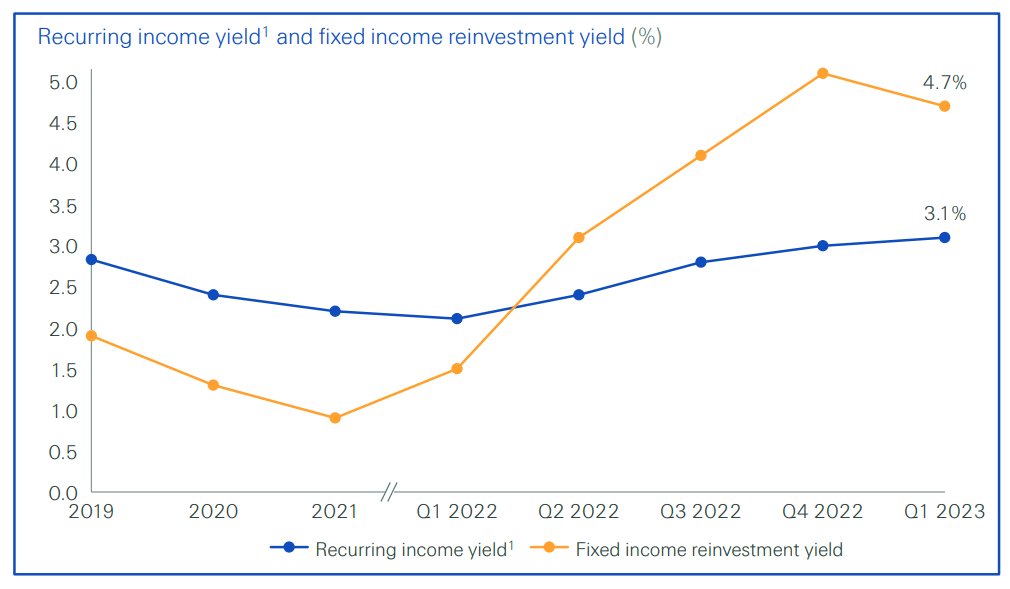

I would also like to address my prior assertion that Swiss Re could see limited upside in the short to medium-term as a result of an uncertain macroeconomic outlook and the potential for downward pressure on fixed income should recessionary conditions warrant a slowing down of rate hikes. While we have seen a slight slowdown from the last quarter - the fixed income reinvestment yield still remains substantially above levels seen in 2020 and 2021:

Swiss Re investor and analyst presentation: First Quarter 2023 Results

{kind=link}

In this regard, I take the view that the risk to fixed income reinvestment is minimal - and Swiss Re can continue to benefit from generating a sufficient degree of investment income from its fixed income sources.

Overall, the primary reason for my more bullish stance on Swiss Re is its resilient performance in Q1 in spite of large catastrophic claims. More broadly, demand for P&C Reinsurance has continued to remain vibrant. In spite of risks of a potential recession - inflationary pressures have meant that demand has continued to grow due to the higher degree of potential losses that would result from not having adequate P&C cover.

Risks

Going forward, my view on Swiss Re is broadly optimistic and I take the view that the company can continue to thrive in the current environment.

In terms of the potential risks to Swiss Re at this time, we are still seeing that inflationary pressures are pushing up the costs of claims across the P&C sector - with the Insurance Journal estimating that premium income would have needed to rise by 13% in 2022 to offset the costs of claims being driven by higher inflation.

In this regard, we could see a risk to further net income growth if premium demand starts to plateau but the cost of insuring claims continues to rise - which would be expected to place upward pressure on the combined ratio.

With that being said, I maintain the view that Swiss Re is managing this risk effectively to date.

Conclusion

To conclude, Swiss Re has seen a strong Q1 - with net income having seen growth in spite of elevated catastrophic losses. Moreover, the reinvestment yield on fixed income continues to remain at higher levels relative to previous years and is likely to continue proving a valuable source of reinvestment income.

In spite of macroeconomic risks - I am particularly impressed by the company's recent performance and take a bullish view going forward for this reason.

For further details see:

Swiss Re: Strong Net Income Growth Despite Losses