SO - Switching Horses On Valuation: Southern Company Vs. Dominion Energy

Summary

- Sometimes two good companies in the same investment sector find their respective share prices diverge for what appears to be no good reason.

- I uncovered what appears to be such an instance in regulated utilities Southern Company and Dominion Energy.

- This author decided it's time to change horses on valuation.

- Fresh horse or trojan horse? Read on and decide.

Sometimes two good companies in the same investment sector find their respective share prices diverge for what appears to be no good reason. In such cases, I take a look at the fundamentals. If there are no red flags evident, I may begin a process of switching horses: transferring capital from a tired stock to a fresh one.

Recently, I found myself in a situation whereby I believe this is the case: venerable Southern Company ( SO ) and Dominion Energy ( D ).

Both are fine utilities with significant operations in the southern United States; offering investors largely regulated business model, solid operating metrics, and good dividend yield.

Let's take a closer look.

Evaluating Utility Stocks

I contend evaluating fundamentals for regulated utility stocks is a bit different than for other sectors. While investors may elect myriad metrics to review, I offer several below that provide a good starting point for further due diligence:

-

operating margin

-

return-on-equity

-

operating cash flow-to-debt ratio

-

dividend coverage ratio

-

electric sales growth

My rationale for the foregoing is as follows:

Operating margin : an overall business profitability measure that sets aside non-operating net interest expense and taxation.

Return-on-equity : another profitability metric that focuses upon how efficiently management utilizes stockholders' investment.

Operating cash flow-to-debt ratio : a debt leverage check as a function of cash flow instead of profit.

Dividend coverage ratio : a traditional screening metric to evaluate whether earnings support the current dividend.

Electric sales growth : a measure validating if a company operates in markets with increasing electricity demand.

Let's Compare Southern Company and Dominion

To enable a more visual process, I've employed FAST Graphs to highlight the last several years' data. For 2022, I performed the calculations using data from the company's website and / or SEC filings.

Operating Margins

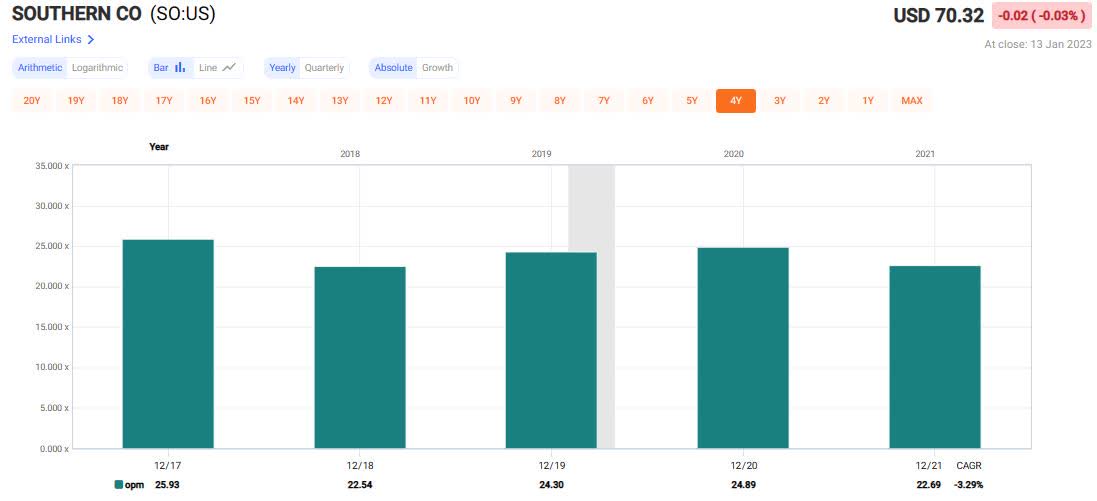

First, here's Southern Company :

{kind=link}

Over the last five full years, margins have run between 23 percent and 25 percent. Through the first three quarters of 2022, the operating margin is 24 percent.

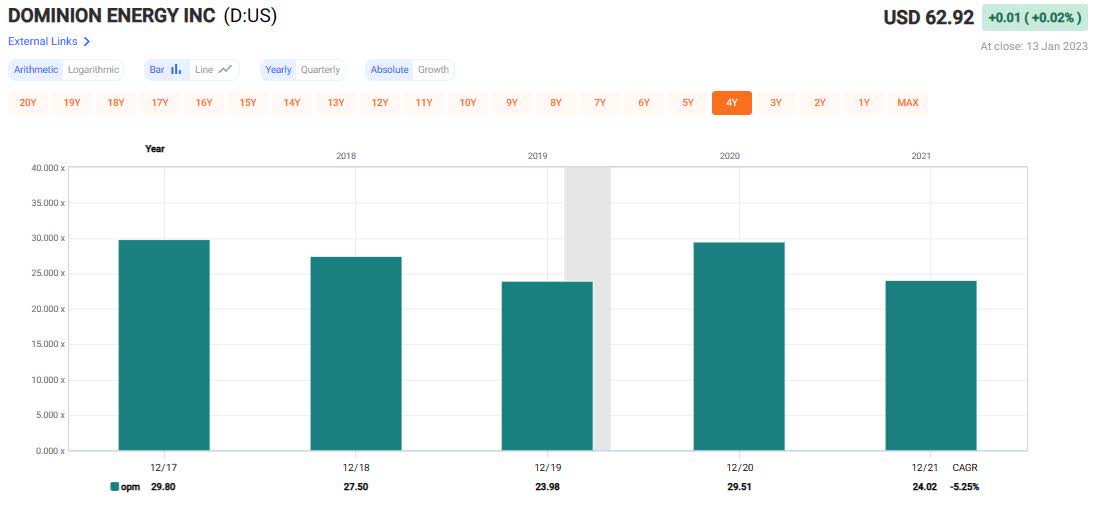

Dominion Energy:

{kind=link}

Margins ranged between 24 percent and 30 percent. Through 3Q2022, the operating margin is 29 percent after adjusting for net losses experienced via nuclear decommissioning, regulated asset retirements, and mark-to-market adjustments on hedging activities.

Bottom line: Dominion has somewhat better operating margins. Both Southern Company and Dominion Energy enjoy operating margins above the multi-utility segment average; 15 percent.

Return-on-Equity

Southern Company:

{kind=link}

Between 2017 and 2021, SO averaged ~9 percent RoE. Return-on-equity improved to 14 percent through the first three quarters of 2022. As the Vogtle nuclear project winds down, returns may improve.

Next, Dominion Energy:

{kind=link}

In recent years, D averaged 10 percent RoE. After adjustments, Dominion recorded a 9 percent return through 3Q 2022.

Bottom line: Return-on-equity is about equal and on par for the industry.

Current Operating Cash Flow-to-Debt Ratio

Southern Company – 11 percent

Dominion Energy – 8 percent

Note : Higher is better.

At year-end 2021, Dominion's cash flow-to-debt ratio was 10 percent. The reduced ratio through September 2022 was exacerbated by a $1 billion delta in deferred fuel and gas costs versus the year prior. Adjusting for this item (which should be recovered within a year) suggests the debt ratio would remain an even 10 percent.

Bottom line: Debt leverage on an absolute and relative basis is equitable for both utilities. Backstopping the data is the fact that both SO and D enjoy BBB+ credit ratings.

Dividend Coverage Ratio [through 3Q 2022]

Southern Company – 61 percent

Dominion Energy – 63 percent (after aforementioned decommissioning and asset retirement adjustments)

Bottom Line: no material differences / acceptable dividend coverage ratios.

Electric Sales Growth

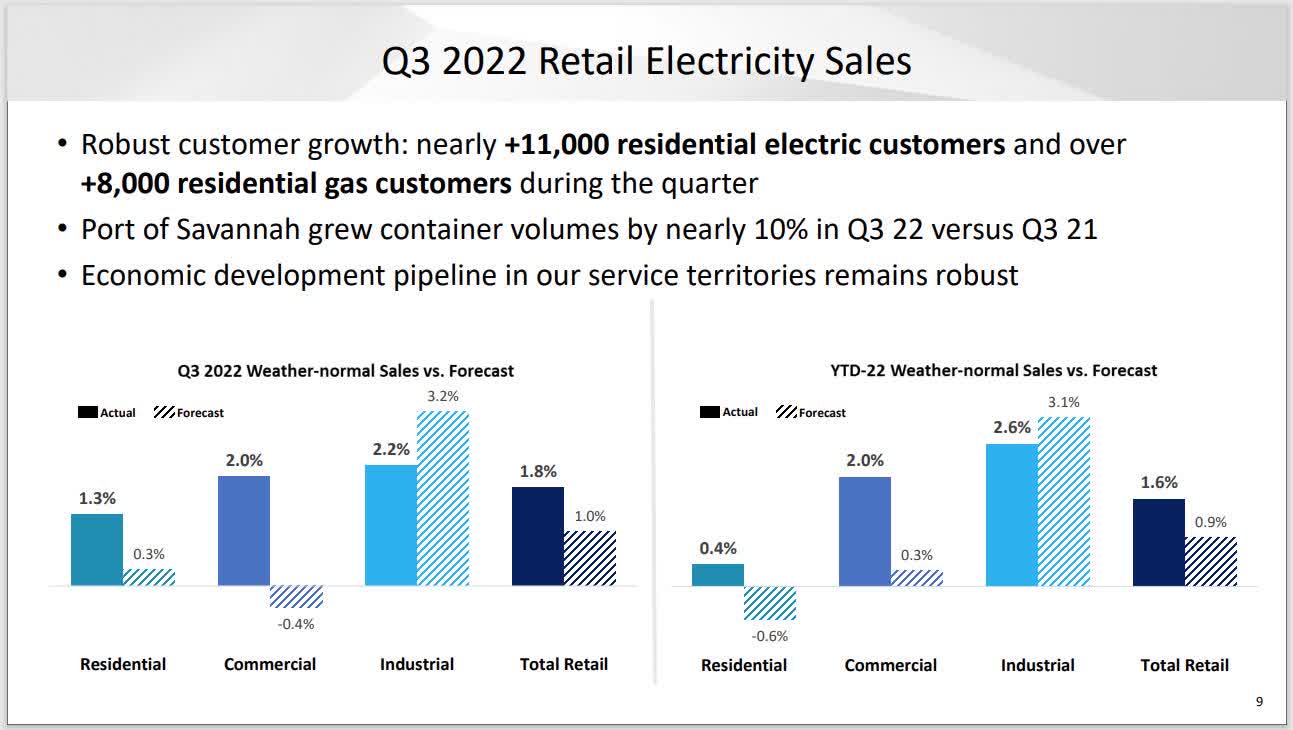

Southern Company

Southern Company 3Q22 earnings presentation

{kind=link}

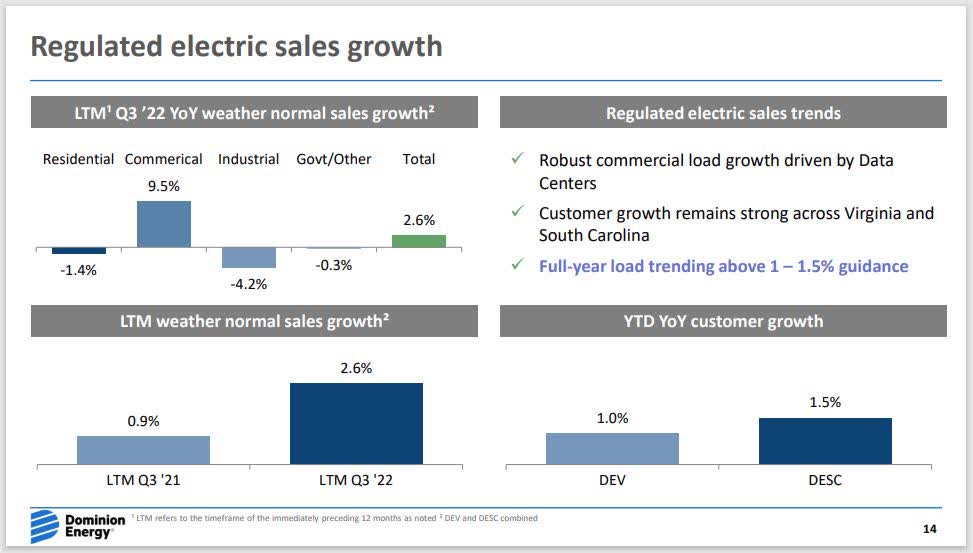

Dominion Energy

Dominion Energy 3Q22 earnings presentation

{kind=link}

Bottom Line: Within their service areas, Southern Company and Dominion Energy are enjoying weather-normal electric consumption growth. SO improvement is driven by increasing demand from the industrial segment. Dominion's commercial segment is underpinning the YoY increase.

Summing Up the Fundamentals

Based upon the metrics chosen, it appears Southern Company and Dominion Energy are experiencing:

-

above-average operating margins,

-

equitable / adequate return-on-equity,

-

reasonable debt leverage,

-

good dividend coverage, and

-

growing electricity demand

It's not evident there is a material separation between these two leading multi-utility companies.

How About a Backstory?

In addition to the fundamentals, investors may ask if recent news events or company narratives warrant concern.

Dominion Energy stock experienced a significant drawdown after 3Q earnings. The CEO announced he wanted to conduct a thorough business review in order to find opportunities to drive better performance. The message was somewhat puzzling and may have spooked the market.

Compounding matters, after the 3Q earnings report, some Street analysts revised downward forward EPS and dividend growth forecasts. Whether these developments warranted a 15 percent share price haircut is up for debate. Meanwhile, Dominion management's 3Q earnings presentation and conference call offered no obvious flags regarding future earnings power or dividend growth.

Southern Company's management indicated the business is on the downhill side of completing the Vogtle 3 and 4 nuclear reactors. For years, persistent cost overruns and delays plagued these projects. The overhang appears to have faded. Otherwise, management forward expectations forecast consistent improvement in profitability and dividends. No particular negative developments were cited.

On balance, Southern Company and Dominion Energy appear healthy, well-positioned, and well-capitalized regulated utility companies.

Valuation: A Case to Change Horses?

Now to the crux of the matter. Given the fundamental screening test is behind us, it's time to check the second benchmark:

Here are two FAST Graphs illustrating the valuation dislocation between SO and D stock.

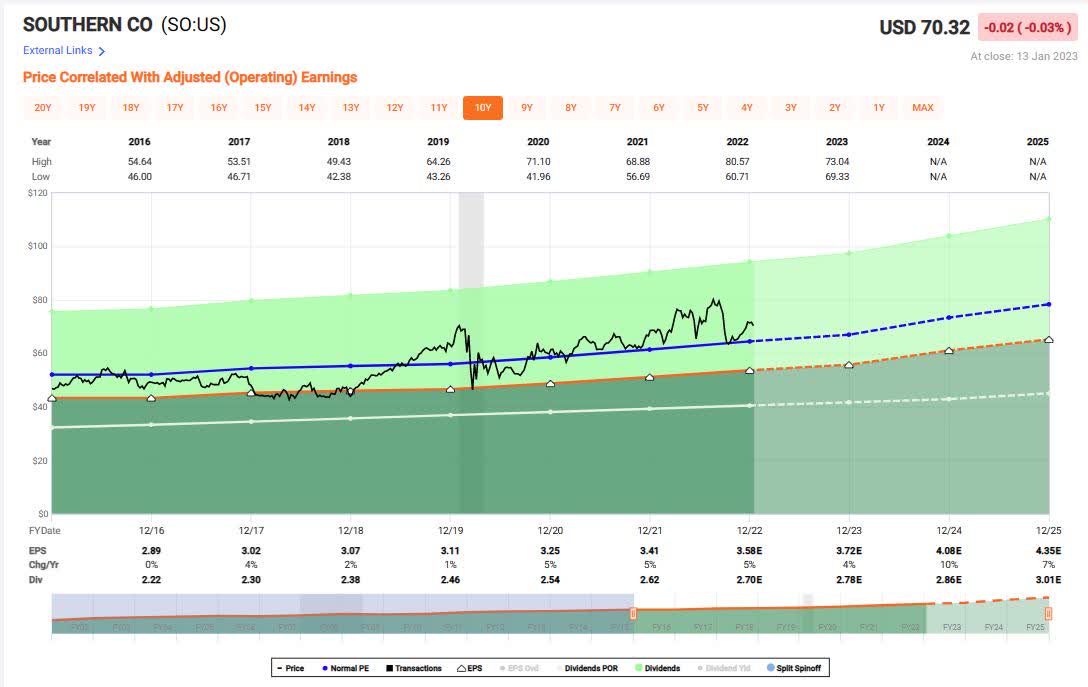

First up is Southern Company.

{kind=link}

The 10-year chart indicates SO stock is somewhat overvalued. The long-term PE is 18x and the current blended PE is nearly 20x. Over the next couple of years, Street analysts expect Southern Company to grow earnings about 7 percent a year, though 2023 is forecast to see a modest profit increase.

The current dividend yield is 3.9 percent.

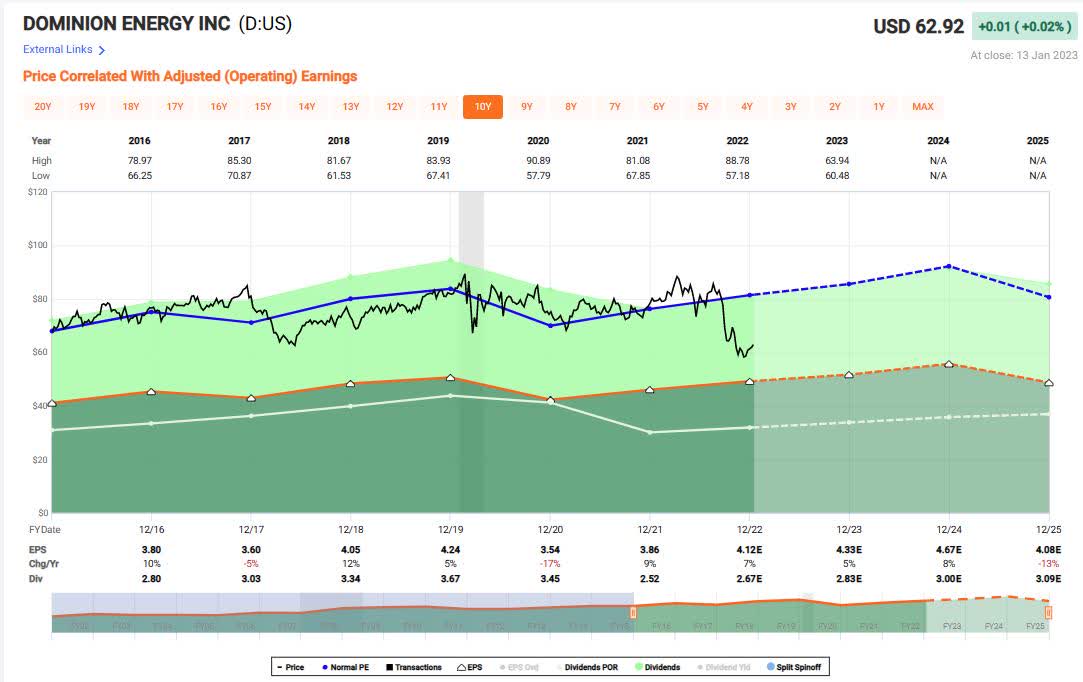

Now look at the Dominion Energy chart.

{kind=link}

Conversely, D stock appears materially undervalued. The long-term PE is nearly 20x, yet the stock now sports a 15x blended multiple. Despite stock prices tracking earnings reliably in prior years, during the summer of 2022 the shares took a header along with most Utility sector stocks. After rebounding a bit, the stock fell another 15 percent after 3Q 2022 earnings; whereby most large utility stocks did not follow suit. As pointed out earlier, there wasn't any particular news precipitating the fall other than the curious CEO announcement about wanting to conduct a full business review in order to improve operating and equity performance. That seems to have spooked some investors.

The current dividend yield is 4.3 percent.

A Brief Historical Excursion

In 2020, Dominion slashed its dividend in response to cancelling the Atlantic Coast gas pipeline and selling part of the business. At the time, I wrote about these developments in the Seeking Alpha article entitled , “ Southern Company: Safe, Solid Utility Stock for Income Investors. ”

I explained it was time to change horses; however, in 2020 it was to swap out of Dominion and buy into Southern Company. I opted to sell Dominion shares ~$80 and buy Southern shares in the low $50s.

Now the shoe is on the other foot.

Conclusion

SO is trading at or above Fair Value in the $70 to $75 range while D looks like a deal-on-the-cheap: accumulate in the low $60s range. I'm methodically distributing Southern Company shares and accumulating Dominion Energy.

Is Mr. Market offering a fresh horse to run, or a nasty surprise inside a trojan horse?

I welcome all relevant comments below.

Please do your own careful due diligence before making any investment decision. This article is not a recommendation to buy or sell any stock. Good luck with all your 2023 investments.

For further details see:

Switching Horses On Valuation: Southern Company Vs. Dominion Energy