TSLX - Switching Walk From Main Street Capital To Sixth Street Specialty Lending

2024-01-07 23:58:42 ET

Summary

- Sixth Street Specialty Lending and Main Street Capital are two of the largest BDCs in terms of NAV value and trade at a premium to the BDC sector.

- The notion of valuation premium is fully justified given the defensive characteristics of the underlying portfolios, excellent dividend coverage, and size advantage.

- While both BDCs are attractive, there are several aspects, which render TSLX a better choice.

- In this article, I compare these two names side by side, focusing on the key areas of difference.

In this article, I will assess and compare two BDCs that both fall into Top 10 list of the largest BDCs in terms of the NAV base:

- Sixth Street Specialty Lending ( TSLX ) with a NAV value of ~ $1.5 billion (10th largest BDC)

- Main Street Capital ( MAIN ) with a NAV value of ~ $2.3 billion (7th largest BDC)

There are really two reasons why I have cherry-picked this particular comparison.

First is the investors' overwhelming bias towards MAIN, which introduces an inherent inertia for favoring this BDC even though there are better opportunities out there. This is fully understandable given MAIN's size, stellar historical returns, and prudently structured portfolio, but it does not necessarily warrant alpha (at least relative to other selected BDCs) going forward.

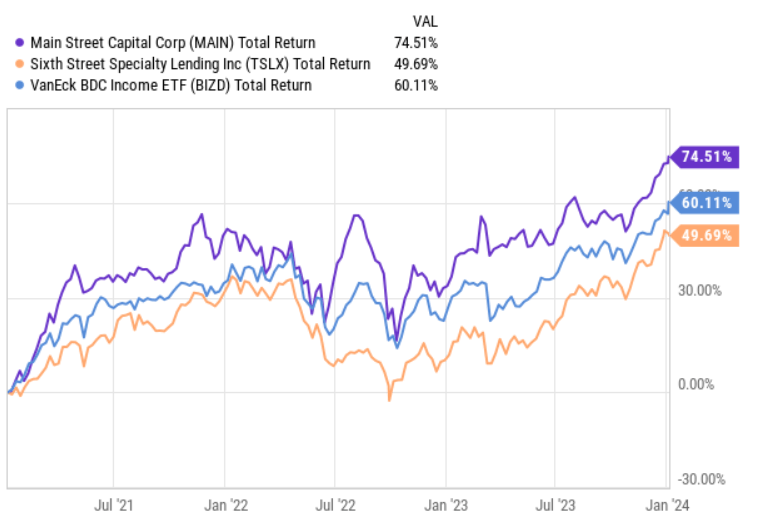

Second aspect, which makes this case interesting is the divergence between MAIN and TSLX's total returns, where over the past 3-year period MAIN has significantly more appreciated in value compared to TSLX, thus creating potentially attractive conditions for TSLX to catch up or, alternatively, MAIN to convergence back to mean.

{kind=link}

Granted, the fact that MAIN has managed to register greater returns than the market and TSLX does not automatically mean that this BDC is a worse investment, far from it. Yet, what it does is it just creates a reason to pay more careful attention to the valuations.

So, let's start with the multiple components of TSLX and MAIN and then dissect a couple of other nuances, which allow us to make better judgments in terms of which of these two BDCs embodies more appealing return prospects.

Both are expensive, but MAIN has gone too far

MAIN and TSLX both trade at a premium over the underlying NAV figure.

For MAIN the P/NAV currently stands at 1.52x, which could be easily ranked as the highest or most expensive multiple in the entire BDC universe. A P/NAV of 1.52x implies that investors entering MAIN at these levels are effectively paying 50% on top of the underlying value, while the BDC sector average stands at 0.96x.

In TSLX's case, we are also talking about a meaningful premium but not to a such drastic extent as for MAIN. Currently, TSLX carries a P/NAV of 1.26x.

If we look at the consensus EPS estimate for 2024, the implied P/E of MAIN lands at 11.1x, which again renders this BDC the most expensive one in the sector. For TSLX the corresponding multiple is at 9.3x, which is closer to the sector average and ~16% below MAIN level.

All in all, from the multiple (valuation) perspective it seems that MAIN will have to do a lot and generate truly remarkable returns to justify the premium. While for TSLX we could potentially factor in some incremental returns stemming from multiple expansion, in MAIN's case I do not see how this could happen given this "tough base".

TSLX is superior in the context of both portfolio and dividend yields

If we peel back the onion a bit and look at the portfolio yield levels across MAIN and TSLX investments, we will immediately recognize a notable spread that is in favor of TSLX.

As of the latest quarter , MAIN had a total debt portfolio yield of 12.9%, while for TSLX the relevant metric stood at 14.3% (i.e., ~140 basis points spread).

Considering the difference in portfolio yields and richer multiples for MAIN, the dividend yield (including TTM special dividends) of TSLX is 60 basis points higher, offering 9.9% via quarterly distributions.

Now, from the portfolio quality angle, both of these BDCs could be deemed safe carrying well-calibrated portfolios with several layers of extra protection, which are not that common in the overall BDC space.

For example, both MAIN and TSLX can enjoy the benefits of their size by not having to concentrate too much of their AuM in the single largest names or industries. Currently, the Top 10 investments account for less than 20% of their portfolio values (albeit for TSLX it is 23% if measured at FV basis). Similarly, no industry constitutes more than 15% of the total exposure. These statistics are truly not that common among other smaller-scale BDCs.

Now, one might argue that the reason for MAIN's premium and lower portfolio yield lies in the fact that it has better quality portfolio.

While we could say that MAIN has indeed some greater characteristics of its underlying portfolio, the delta though is relatively insignificant and insufficient to justify the lower yield and premium over TSLX.

We can take a look at two aspects here.

First, MAIN carries roughly 99% of its portfolio in first lien investments. For TSLX this category consumes 91% of portfolio (which per se is a very solid statistic). Then TSLX has allocated 7% into equity-type instruments, where many of them are attributable to resilient preferred shares, which entail very similar return factors to the bond-like investments (e.g., first lien). So, we are left with a part of 7% equity exposure and 2% second lien / subordinated investments that inject a bit higher risk in TSLX books.

TSLX Investor Relations

One of the key reasons why both MAIN and TSLX trade at premiums to their NAV levels is the combination of resilient portfolios and superb dividend coverage ratios.

{kind=link}

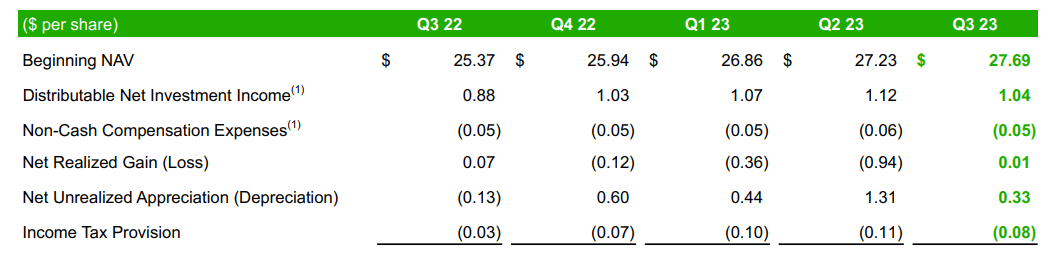

In fact, MAIN has one of the safest dividend coverage in the overall BDC market with ~150% of distributable investment income above the underlying dividend.

{kind=link}

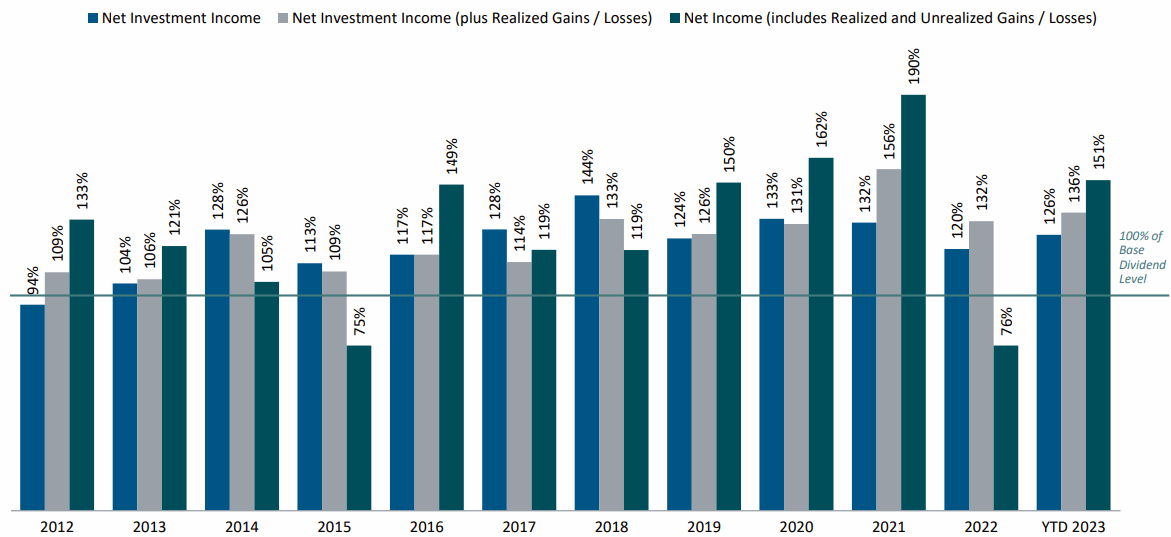

Looking at TSLX's ability to accommodate its quarterly dividends it is also very clear that the distributions are safely covered not only through net investment income but also via NAV appreciation component. While the net investment income is still significantly above the underlying dividend and could be easily categorized as also one of the safest in the sector, the overall coverage is not as strong as for MAIN. However, here we have to contextualize also the constant NAV appreciation, which together with net investment income sends the dividend coverage much higher from the already robust levels.

There are again differences between MAIN and TSLX portfolios, but nothing that I would consider material to justify the valuation gap.

The debt structure for MAIN is actually a potential problem

Before we assess the debt structures of MAIN and TSLX, we have to keep in mind the following aspects:

- 70% of MAIN’s debt investments bear interest at floating rates, which means that roughly one-third of the portfolio provides fixed interest rates.

- 98.9% of TSLX's debt investments are stipulated at a variable rate (i.e., SOFR), which almost completely neutralizes the potential mismatch between asset and external leverage yields.

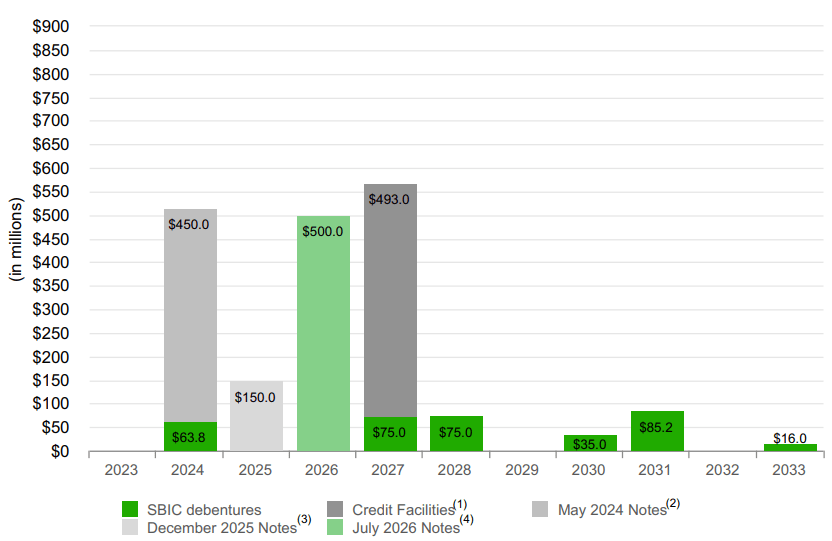

Now, an important factor, which helps MAIN generate rather attractive net investment income accommodating robust dividend coverage is the spread between its borrowing costs and the portfolio yield, which has to a large extent increased with SOFR with the previously assumed borrowings (a significant part of them) standing constant due to fixed rate nature.

{kind=link}

As we can see in the table above, MAIN will have to refinance meaningful parts of its external debt portfolio in the near future that will per definition increase the overall borrowing costs putting a downward pressure on the spread aspect (i.e., portfolio yield vs cost of debt). For example, 2024 SBIC Debentures and 2024 Notes Payable carry a fixed rate of 3% and 5.2%, respectively. This is clearly below the market level (implying incremental costs on the borrowing side once the refinancing is executed).

TSLX Investor Presentation

For TSLX, however, the debt maturity profile is more laddered with only one fixed rate debt maturity in 2024 allowing the BDC to avoid experiencing rising cost of capital in a less pronounced and more distant manner.

The bottom line

In my opinion, both MAIN and TSLX are great investments as they carry one of the highest quality portfolios and have one of the best dividend coverage ratios in the BDC market.

With that being said, considering the difference in multiples (more expensive MAIN), which is not sufficiently justified by the difference in the underlying fundamentals, TSLX seems more attractive BDC offering ~9% dividend yield that is underpinned by a resilient portfolio and cash flows.

For further details see:

Switching Walk From Main Street Capital To Sixth Street Specialty Lending