SLVM - Sylvamo: Asymmetrical Reward At 8x Earnings 53% Return On Equity

2024-01-05 23:22:46 ET

Summary

- The basic materials sector offers a compelling risk-reward calculus for top-down asset allocation and security selection.

- Within this domain, the paper production industry presents selective opportunities.

- Sylvamo stands out as a name with potential to trade at higher valuations based on asset factors and earnings power.

Investment Briefing

Top down strategic allocation

As far as top-down asset allocation and security selection goes, the basic materials sector offers the most compelling risk-reward calculus over the coming 12 months in our estimation.

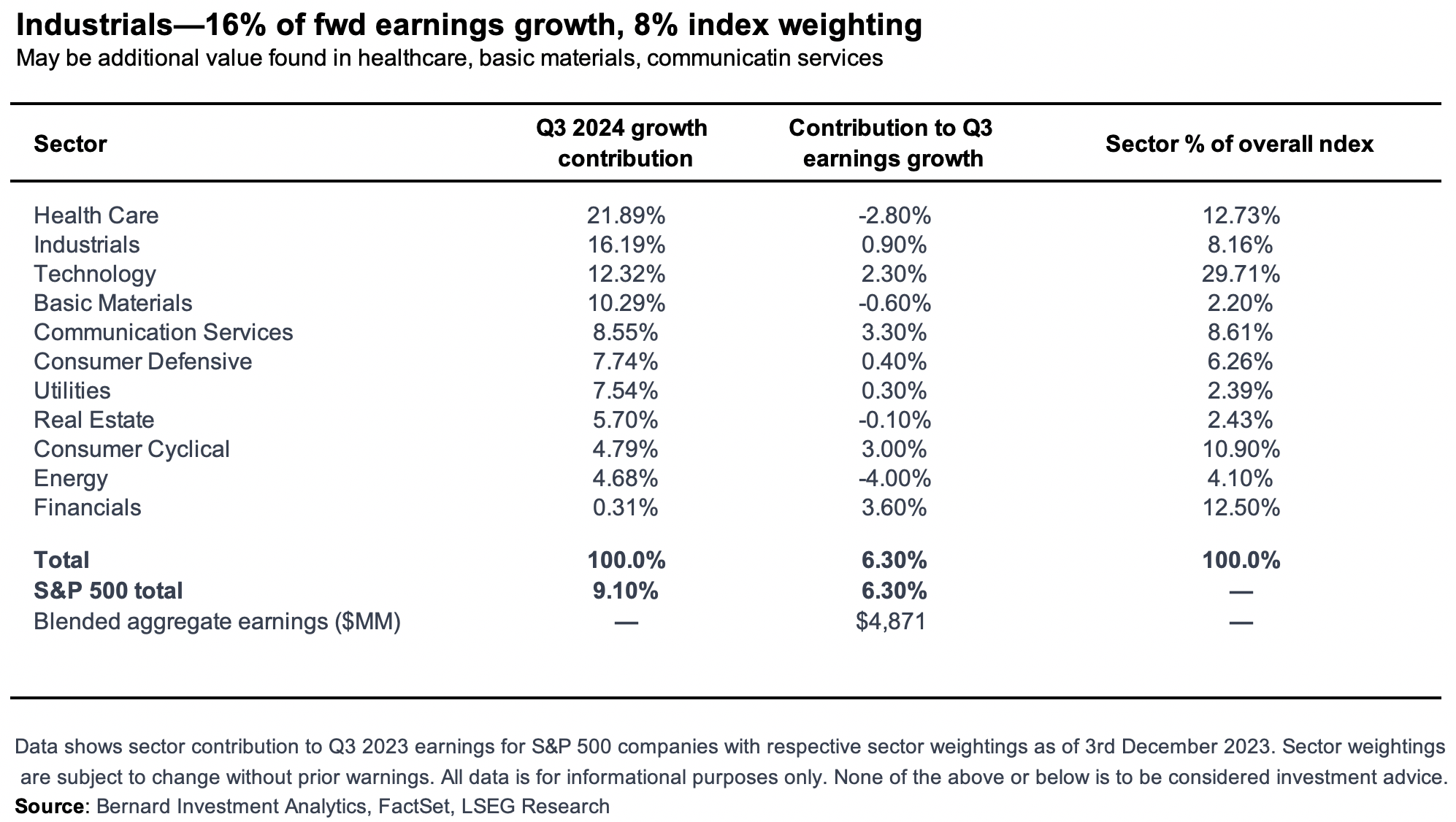

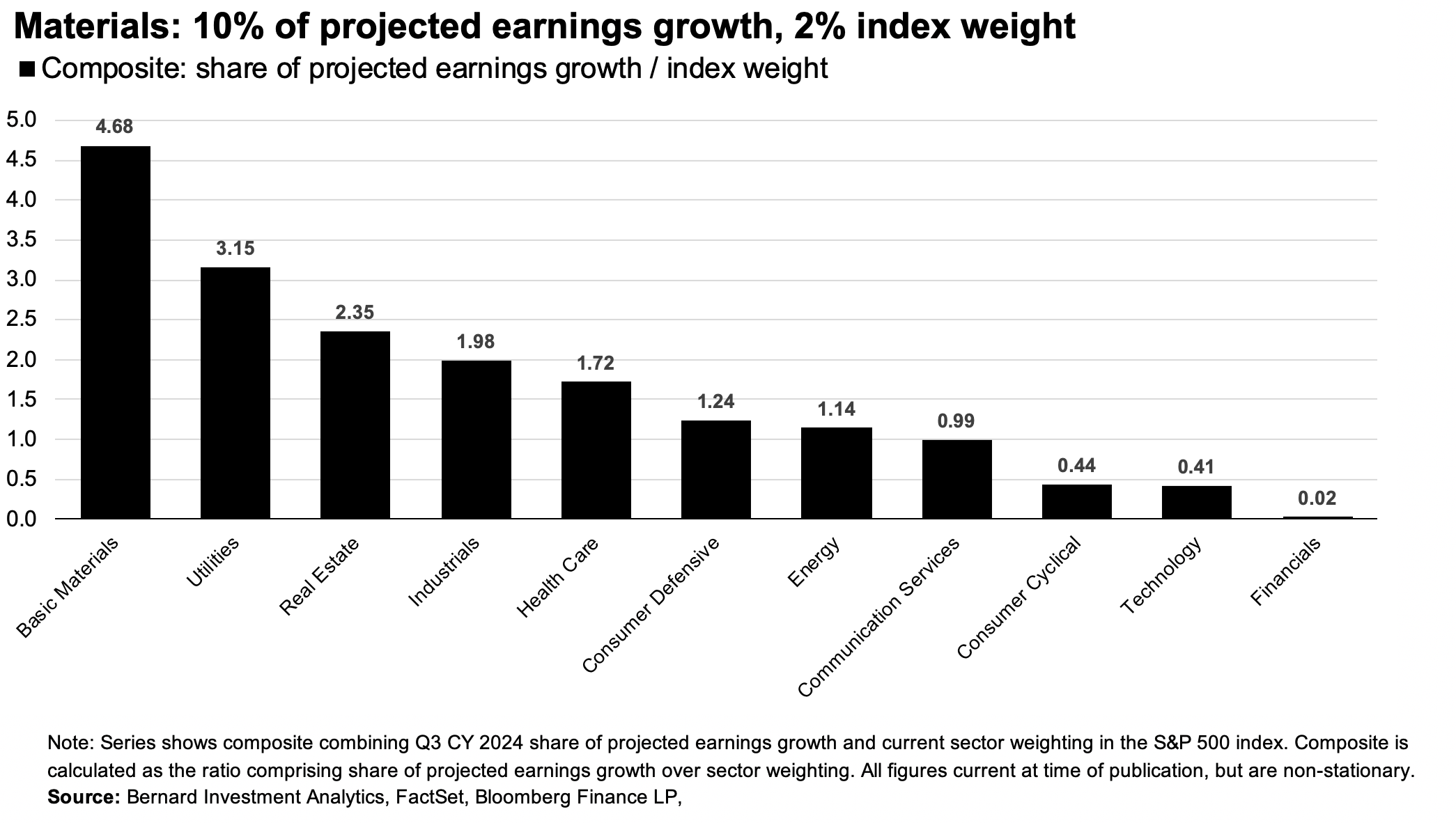

Critical findings from our analysis of Q3 FY 2023 earnings (Figure 1) showed that companies in the basic materials sector held just 2% notional value of the market capitalization weighted S&P 500 index at the end of Q3, but has 10.3% of the projected earnings growth for the next 12 months (Figure 2). As a growth/value composite, this makes companies within the basic materials sector—and their adjacent markets—tremendously attractive in our opinion.

Figure 1.

{kind=link}

Figure 2.

{kind=link}

Within the sector is the paper production industry, often overlooked in the digital age. This is precisely the kind of industry we are inclined to be searching through—the place where others aren't.

The landscape of paper production has reached a state of maturity, prompting a shift among paper producers from uncoated freesheet to packaging. This strategic shift is a response to the changing retail landscape, marked by the decline of traditional stores and the rise of online retail. Based on this information, there could be selective opportunities within the industry.

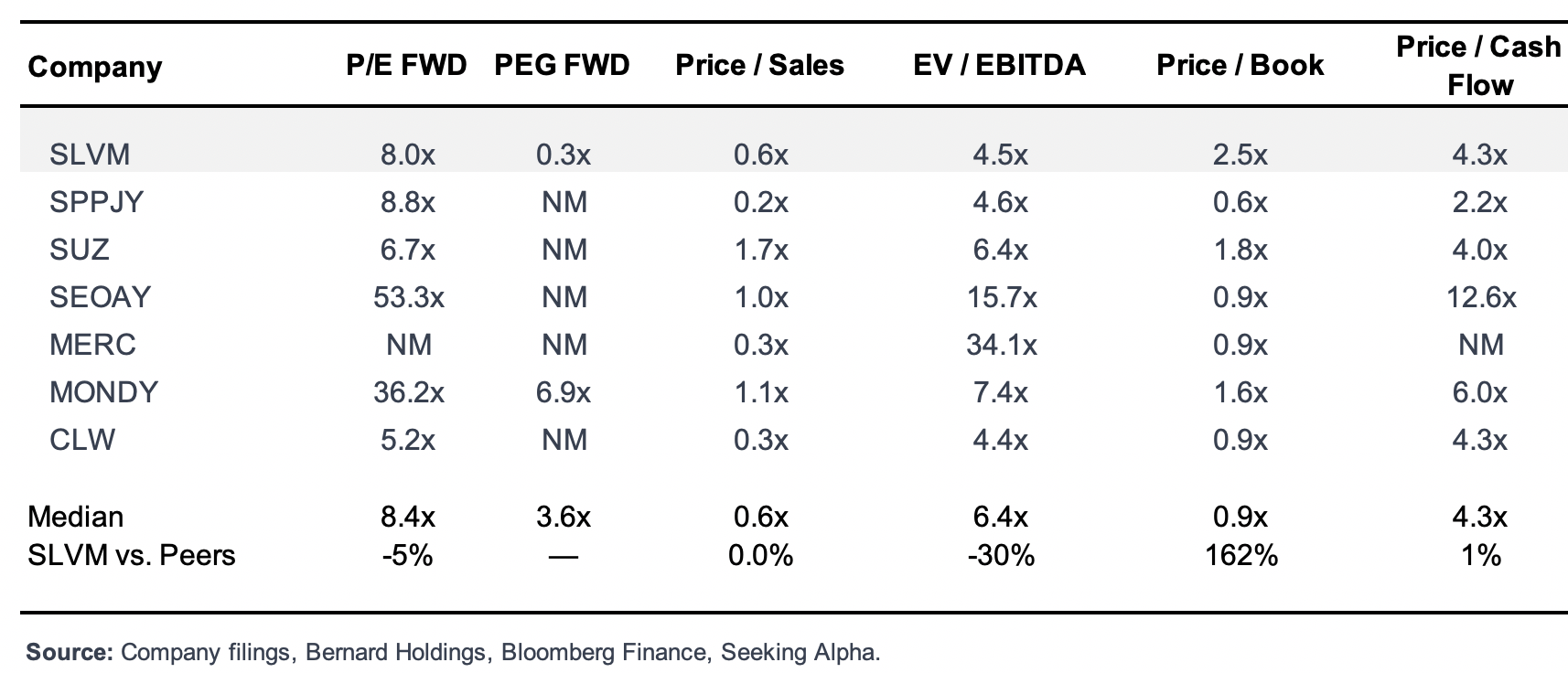

There are a handful of paper production companies trading on U.S. exchanges, seen in Figure 3. The industry trades at 8.4x forward earnings but has created little market value beyond the equity capital employed, priced at a median 0.9x multiple of market valuation to book value of equity.

Figure 3. Listed Paper Products Companies

{kind=link}

Opportunity

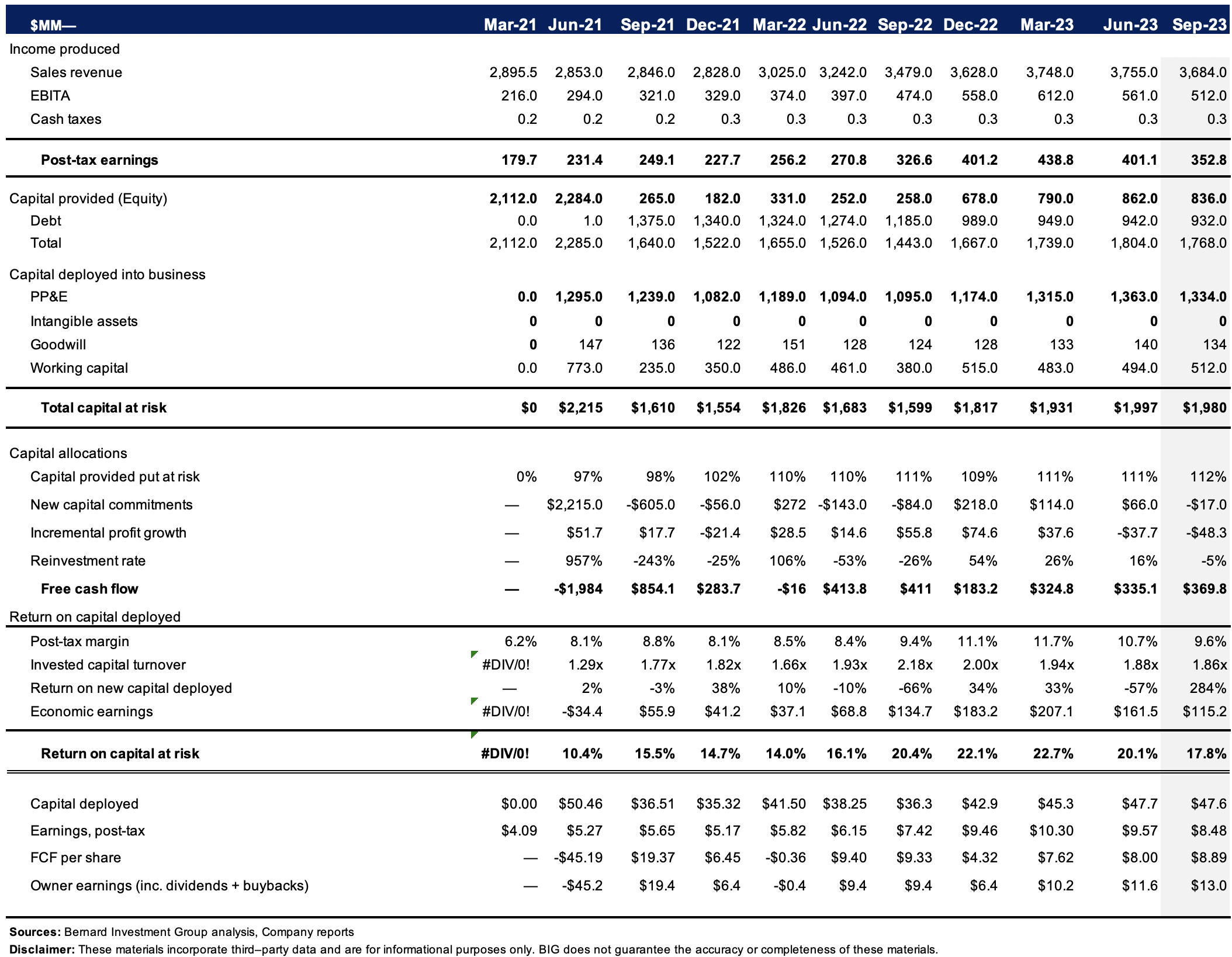

Within the group, Sylvamo ( SLVM ) presents as an outlier, trading at 2.5x its book value of equity and 8x forward earnings. To illustrate the dislocation in price to value, SLVM produced 53% return on this equity in the last 12 months, which concludes to 21% ROE for the investor when paying 2.5x book value to buy the company today. It has thrown off $8–$10/share in TTM FCF each period since Q1 2021 (see: Appendix 1), maintaining this trend since floating its shares later that year.

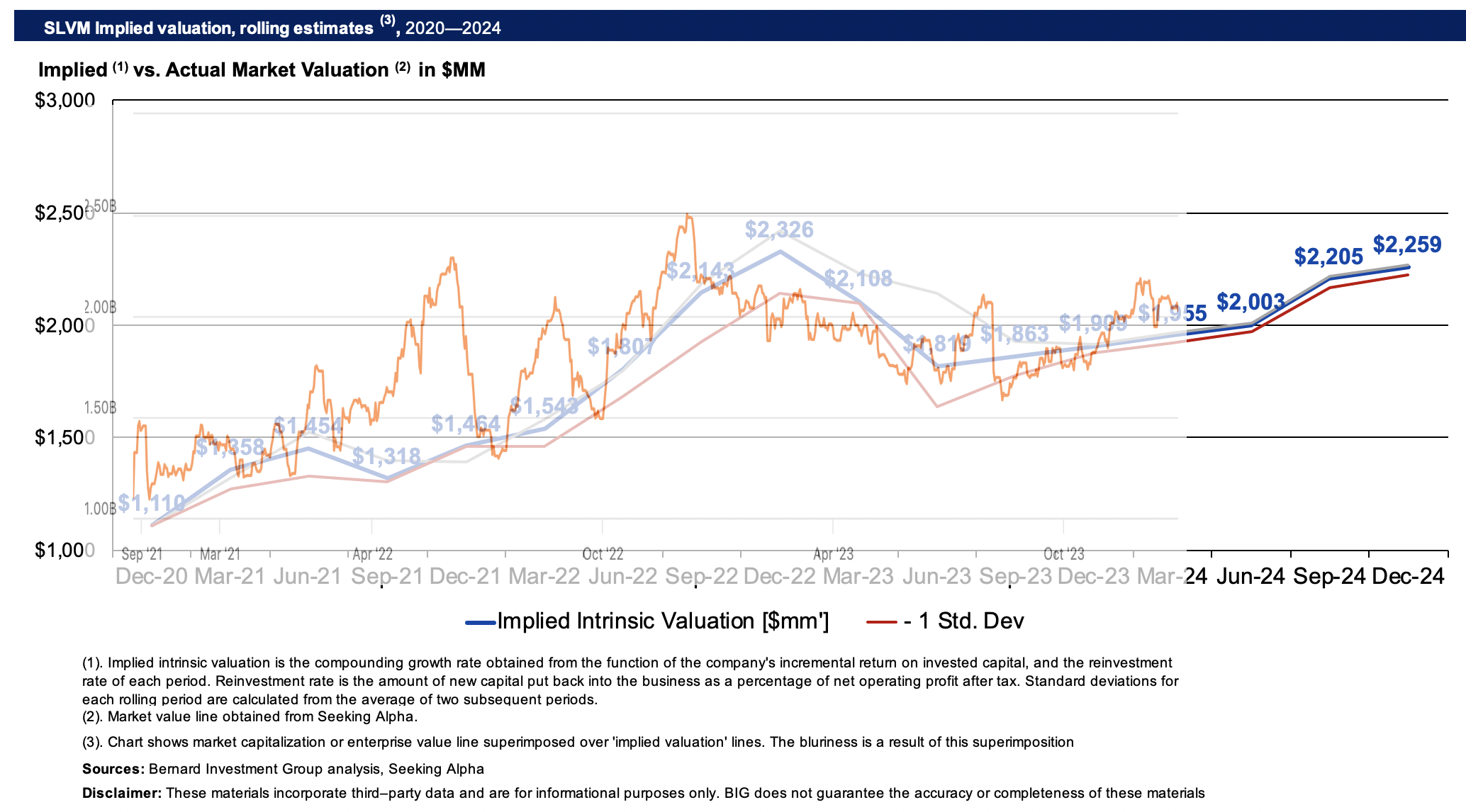

In our opinion, SLVM has scope to attract higher market valuations based on asset factors and earnings power. Our position is bolstered across all 3 investment horizons, with the stock trading below 10x earnings on >50% ROE with strategic use of leverage. The market has valued it accurately since listing and I am looking to a market value of $2.2Bn or $53-$55/share for the company over the coming 6 months, with catalysts from earnings and broad market strength. This report will succinctly demonstrate the additional reasons why.

Net-net, I rate SLVM a buy for the reasons outlined in this report.

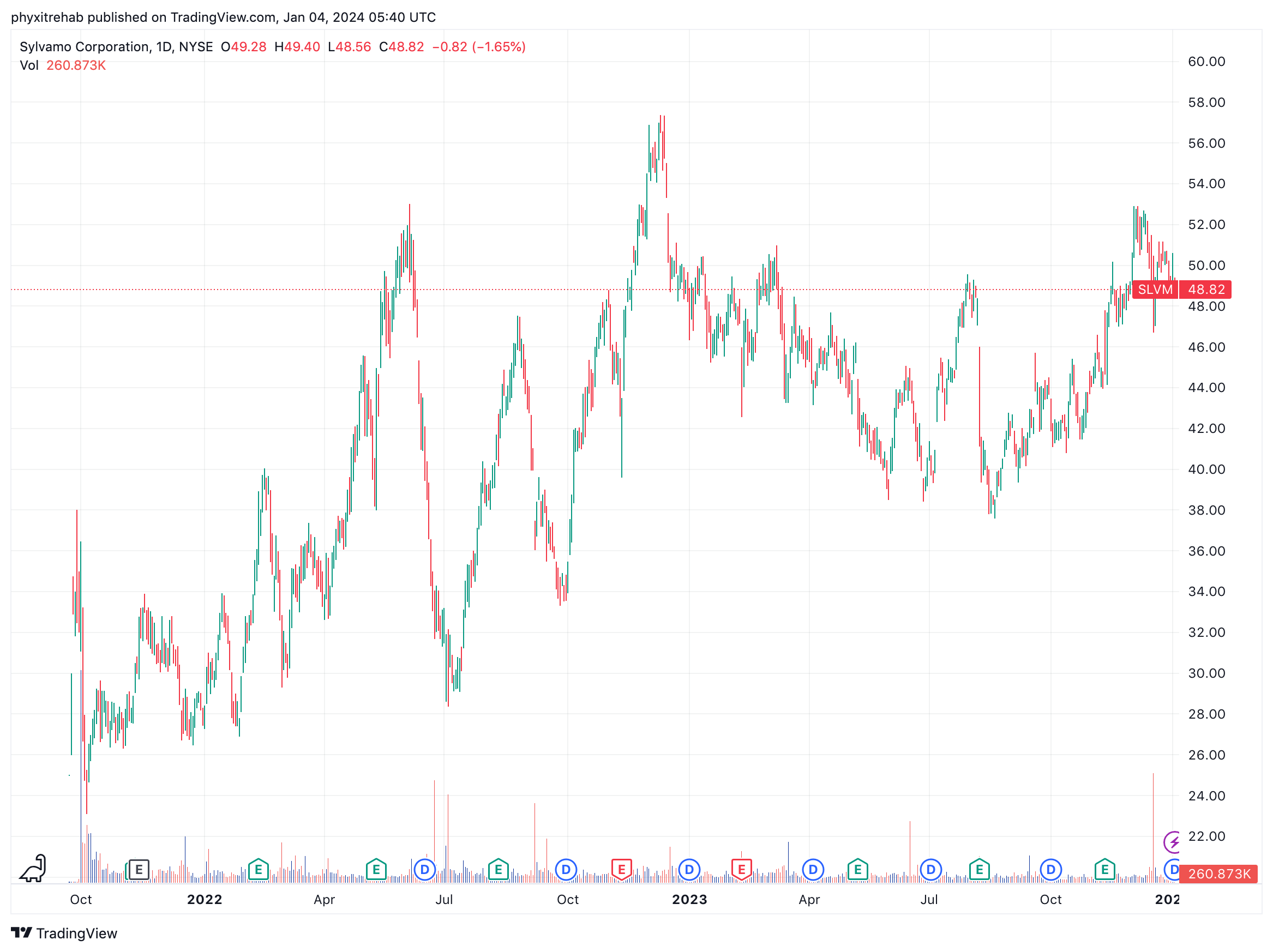

Figure 4. SLVM price evolution since listing

{kind=link}

Critical investment facts

A buy rating is supported across all 3 investment horizons in our opinion. The case for each selective holding period is outlined in the arguments below.

- Next 12 months returns

The case for asymmetrical returns for the next 12 months in buying SLVM today is bolstered in the fact it sells at 8x forward earnings , 53% below the entire sector and 5% below the industry. Investment returns for 12 months after purchase are heavily impacted by starting multiples, so this is statistically relevant.

This is also a statistical discount in our opinion for the following reasons:

(i) Adjusting for projected growth , the company sells at just 0.27x earnings,

(ii) It regularly earns >20% on capital employed which drives FCF per share growth and provides opportunities to redeploy or return cash (Appendix 1)

(iii) FCF yield of 18% as I write illustrating the immense value at these prices

Paying 8x earnings for a company projected to grow 8-10% and receive 18% FCF yield offers asymmetrical reward opportunities for the tactical investor because of how cheap the company is priced and what value is on offer.

- Investment returns 1–3 years and Q3 earnings insights

The company posted its Q3 '23 numbers on November 9th last year. SLVM put up Q3 revenues of $897mm, down 7.3% from a strong third quarter in the prior year. It pulled this to adj. EBITDA of $158mm and earnings of $58mm or $1.37 per share.

It also booked $197mm in OCF and converted $155mm if this to FCF as evidence of the company's capital-light operating model.

As to the operational highlights, critical findings include the following:

- Q3 revealed a $55mm decline in price and mix due to lower paper prices in Europe and Latin America. This was offset by a $6mm volume increase. Clearly the revenue downsides were demand-driven this quarter.

- OpEx was down $1mm, whilst planned maintenance outage expenses saw a notable $55mm decrease. I'd also note that costs for inputs were down $27mm YoY, driven by favorable fibre, chemical, and transportation costs.

Management called for adj. EBITDA of $90mm—$110mm for Q4, but also outlined several challenges. This includes a $20mm— $25mm decrease in price and mix, reflecting prior paper price decreases and an unfavorable sales distribution across its footprint. However, a corresponding $20mm—$25mm improvement in volume is also expected from its Latin America and North American markets.

Collectively, the performance was in line with the market's and internal expectations. Whilst investors may be positioning for a change in expectations, a la Mauboussin style, one thing to consider is that a continuation of expectations is also a bullish driver of stock prices as well. Such is the case for SLVM in our opinion.

Sales growth is forecast for 1-2% out to 2025, not unexpected for a company founded in 1898. You are buying SLVM for the value at these prices in my estimation, and growth is not part of the equation in my view. Even still, the outlook for 1-3 years is robust in our view.

Moreover, compounding the company's intrinsic value at the function of its return on capital and reinvestment rates, it appears the market has been an accurate judge of fair value since 2021 (Figure 3a). SLVM has exhibited mean-reversion activity around its implied fair value and continues to do so into 2024. My estimates are for a >$2.2Bn market value ($53/share) as the next price objective at current expectations, discounting the next 12 months projections back to the present.

Figure 3a.

{kind=link}

- Investment returns 3 years+

Returns from the next 3 years plus are bolstered by SLVM's ability to compound the rate of earnings produced on capital invested in the business.

Given the capital-intensive nature of the paper products industry, analysis of capital productivity and profitability is essential. The bulk of SLVM's investments (67%) are in fixed assets. The remainder is tied up in net working capital for operations.

As a reminder, capital is the cash provided by investors to finance assets or the means of production. When cash is used to finance assets–it is known as capital. It is in the form of debt or equity. Companies put this cash/capital at risk by investing it into assets of the business. These assets produce sales, cash flows and earnings.

As equity investors, we provide the cash for an economic benefit—return on investment. Our corporation produces this return through its business assets. The higher the earnings relative to capital employed, the higher the business returns, the higher the investor's returns. If all the cash provided has been put at risk, the corporation is therefore a conduit between our capital, where it has been placed, and the returns (cash flows/earnings) generated.

As it relates to the company:

- SLVM has increased capital at risk in the business from $35/share in 2021 to $47.60 per share as of Q3 '23. It has grown earnings from $5.20/share to $8.50/share in the same period—26% incremental return on investment (all earnings in TTM figures). It earned $8.50/share in NOPAT on $47.60/share invested last period, 18% trailing return on capital.

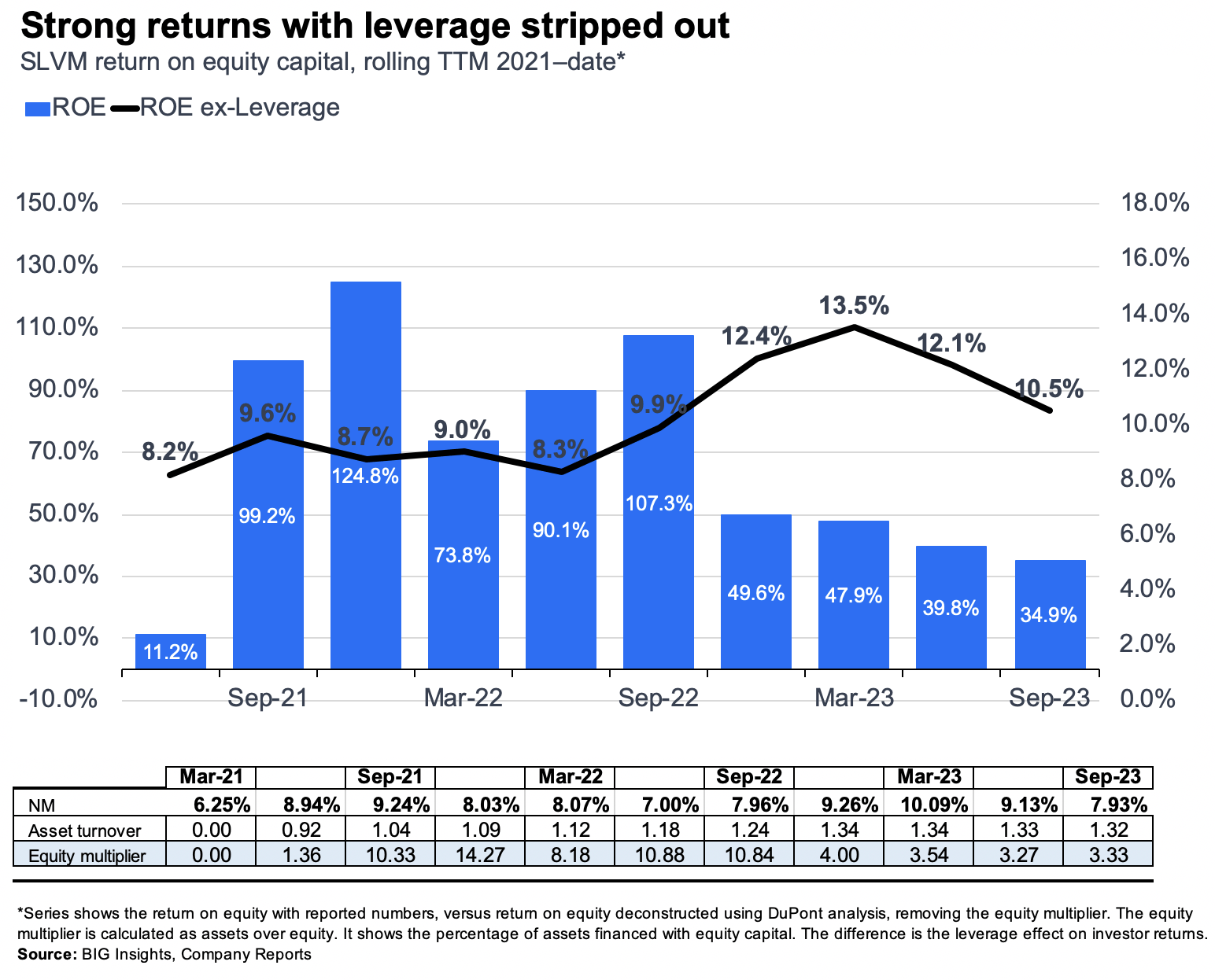

- Equally as robust are the returns for equity holders. SLVM has repeatedly demonstrated it can compound the rate of return earned on equity capital. As seen in Figure 4, investors have enjoyed double-digit returns on equity since the firm listed in '21. Even stripping leverage effects out, you're looking at 10–13% ROE across 2023, producing $28.30 in additional earnings on incremental equity of just $3.70/share over the same time.

Figure 4.

{kind=link}

The other fact is I've deemed SLVM's earnings economically valuable for the following reasons:

- Our opportunity cost is 12%, equal to long-term market averages. We believe this is achievable over a long-run. This is the market return on capital.

- Companies must beat this threshold margin in their business returns to create economic value in our portfolios. Otherwise, we'll buy the index.

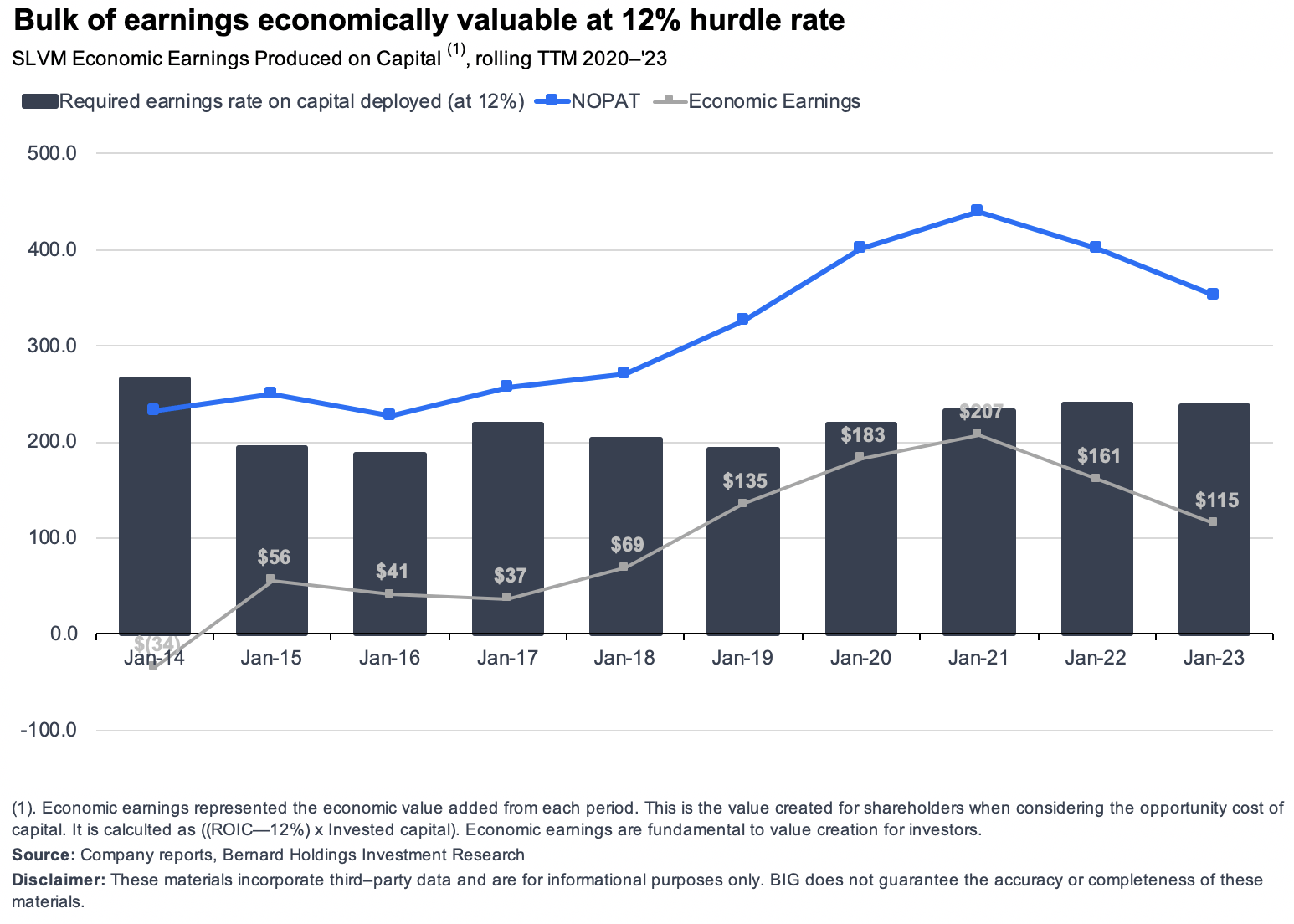

- SLVM has persistently beaten this watermark since 2021, as seen in Figure 5. The company routinely produces 20–22% as a rate of post-tax earnings against capital invested, equal to around 5% of sales on average, and 30-45% of NOPAT.

- As a result, at least 30% of SLVM's post-tax earnings are considered economically valuable to our equity budget.

- The company has produced $23.50 per share of economic earnings since Q3 2021 (excluding $1.875 dividends per share). Unsurprisingly, its market value has increased by exactly $23.99 at the time of writing, since its listing in September 2021.

Going forward, my estimation is that SLVM will continue along this trajectory, providing the bedrock for my bull thesis.

{kind=link}

Discussion summary

In short, there are multiple layers of evidence to support SLVM as a buy. This rating is supported across all 3 investment horizons, backed by valuation factors, business economics and the company's fundamentals. In our view, the company presents with the kind of equity premia that investors will continue to pay higher valuations for. As such, I initiate the company as a buy with $53-$55/share as the first objective.

Key risks to the thesis include:

1) Macroeconomic risks cannot be ignored, especially a second round of inflation. Risk appetite should reflect this.

2) SLVM may not hit the projections outlined here. If the variance is large, this could negatively impact the thesis.

3) Investors shouldn't ignore the potential impacts of being a relatively new issue and the liquidity considerations around this.

Investors must recognize these risks in full.

Appendix 1.

{kind=link}

For further details see:

Sylvamo: Asymmetrical Reward At 8x Earnings, 53% Return On Equity