SLVM - Sylvamo: Firing On All Cylinders But Capped By Tax Dispute

2023-03-21 13:22:08 ET

Summary

- Sylvamo made very smart transactions last year, with the acquisition of a modern Swedish paper mill and the sale of Russian assets, both at excellent valuations.

- Free cash flow in 2023 is expected to grow from $269 million to ~$315 million on stable demand, excellent cost controls, and debt management.

- Covenant language on the company's debt currently restricts its ability to return cash to shareholders due to a foreign tax dispute; patience may be required.

Sylvamo Corporation ( SLVM ) is a leading manufacturer and supplier of paper around the world, specifically the type of paper known as " uncoated freesheet " that is used for office paper, stationary, and in some cases, publishing. It was previously a part of the packaging giant International Paper ( IP ), but was spun out as a separate company in late 2021. With its first full year of operations now under its belt - and it was an eventful year - it is worth checking in to update my views based on what has transpired and evaluate the outlook.

Since my last review in September 2022, the shares have been on an overall upward trajectory, though backing well off the highs from December.

Review of 2022 Results

Sylvamo reported its Q4 and full year 2022 last month, and Q4 results in particular missed expectations for both revenues and non-GAAP earnings. The full year numbers, however, were encouraging, hurt primarily by charges taken for discontinued operations. Starting at the top line, revenue for 2022 came in at $3.6 billion, growth of $0.8 billion over 2021, or 28.5% year over year. Similarly, net income from continuing operations was well above 2021 levels, coming in at $336 million, versus $227 million, or 48% higher. The hit comes from the charge of $218 million for discontinued operations, versus the net contributions in prior years, including $104 million booked in 2021. The bottom line result was net income of $118 million for 2022, versus $331 million in 2021 due to the one-time impact of these charges.

Inflationary pressure on inputs - material and labor - was well managed in 2022, as gross margin in 2022 of 28% was some 300 bps better than 2021, although SG&A costs came in at 8% of revenue in 2022, not quite as efficient as the 7.3% in 2021.

What's In Store

Management is expecting a very strong 2023 in EBITDA and free cash flows, and for good reason. The one-time expenses from discontinued operations should be largely behind them, and the contributions from the acquisition of the operations in Nymölla, Sweden from Stora Enso (SEOJF) will begin showing up. This facility was picked up for €150 million, with the production capacity for 500,000 short tons of uncoated freesheet. To get a sense of how good the deal was for Sylvamo, the plant there included a recently complete upgrade in equipment in softwood pulp modernization that was worth $40 million alone.

Specifically, guidance for 2023 is for adjusted EBITDA of $760 - 840 million, and free cash flow of $300 - $330 million. For free cash flow, that compares to $269 million in for 2022, so a distinct improvement on that regard. The pathway to that free cash flow figure is the combination of capital allocation priorities and the payoff of prior investments starting to come to fruition. On the expense side, CapEx spending for 2023 is expected in the range of $210 million to $235 million (versus $149 million in 2022), with another $90 million expected for maintenance needs, including the impact of inflation. Additional investment of $35 million into the business is set aside for Brazilian forestry, which is needed to continue to supply Sylvamo with low-cost raw materials for its mills.

A variety of investments will start seeing a return that impacts the free cash flow. First and foremost is the addition of the Nymölla facility that just came on line for them at the start of 2023. It is already forecast to add $15 - $20 million EBITDA in the first quarter alone. Given that the total investment cost Sylvamo €150 million (around $160 million at current euro/dollar exchange rate), that's the start of a highly impressive return. Although it will clearly have ongoing costs, the trade-off between disposing of its Russian assets for net proceeds of $390 million and what it spent for Nymölla is clear win. I had been concerned that the Russian assets would be difficult to sell for a fair price, but Sylvamo seems to have managed that transaction much better than I was fearing.

The exit from Russia, however, is directly responsible for the second investment, paying down the company's debt. Although it is less interesting from an operational standpoint, it can be as critical from a cash flow perspective, and that benefit accrues nicely to free cash flow.

Sylvamo has vastly reduced its debt obligation over the course of the last year, and refinanced other debt at generally attractive terms, with the benefit that less cash has to go back to creditors, and the interest expense savings can be put to other uses instead. As of 12/31/22, Sylvamo's combined current portion of debt and long-term debt was just over $1.0 billion, which is some $366 million lower than one year earlier. The interest expense in 2022 came to $69 million, but will be meaningful lower in 2023, with no debt major maturities to stare down in the short term. In fact, entering 2022, Sylvamo had two term notes, one due in 2027 with a balance of $512 million and another due in 2028 with a balance of $401 million, along with $443 million in senior notes at 7%. The 2028 term note has been paid off in full now, with the 2027 term note down to a balance of $496 million. The 2027 term loan is floating rate (LIBOR + 1.75%), but due to the agricultural patronage credits that come from the company's involvement in the Farm Credit system, the real rate is measurably less, standing at 5.23% at 2022 year end.

Since the start of 2023, Sylvamo has been offering the holders of the senior secured notes to tender them, and the results as of March 8th press release was showing about an 80% response rate. This refinancing is replacing those senior 7% notes with borrowings largely from the company's existing credit agreement for incremental term loans, as well as a portion from its existing revolving credit line.

Valuation

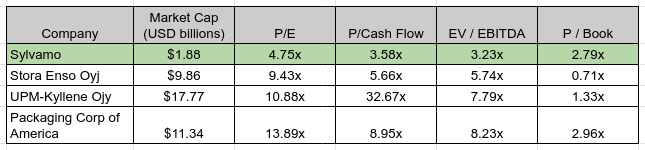

On a whole host of valuation metrics, Sylvamo screens well if looking for value, especially relative to its ability to generate operating cash flows.

Sylvamo Valuation Ratios with Peers (Author's spreadsheet; data from Seek Alpha)

{kind=link}

This really echoes what management was emphasizing in their comments last month. CFO John Sims put it this way in some of his remarks on the Q4 call in February:

We remain a cash flow story. We will leverage our strength to drive high returns on invested capital and generate free cash flow. And we will use that cash to increase shareowner value by maintaining a strong financial position, returning more cash to shareowners and reinvesting in our business.

I guess it cannot be put much more plainly than that, and the value relative to that cash flow remains attractive. Based on the solid management of the company's existing and new asset base and debt reduction priority in 2022, Sylvamo's shares relative to the free cash flow coming on line are almost absurdly cheap. A price/operating cash flow multiple of 6.0x (more in-line with Stora Enso and Packaging Corp of America ( PKG )) would impute a market cap of $3.15 billion, or share price of ~$75.00. Obviously at the current market price of $45, that's a significant upside of 66%. I am not setting a price target per se of $75, but rather to indicate that such a valuation is not unreasonable, and $45 is still quite a value in spite of the run-up since last fall.

Sylvamo has simultaneously managed to pay down debt, buy back shares, increase its dividend by more than double to currently yield 2.22%, acquire the high-quality assets in Sweden for an exceptional price, and close-up shop in Russia, and that's all in a matter of just over a 1 year time frame as a newly public company. The net results of those activities are superior operating results and the ability to concretely distribute cash back to shareholders, but not at the expense of failing to invest properly back into the business itself. Sylvamo seems to be a great example of hitting on all cylinders when it comes to what it might reasonably be able to do for creating value for its owners.

There is an important caveat here for investors. Currently (as of the Q4 earning call last month), Sylvamo did still have some financial covenants in place restricting how much could be returned to shareholders, at $90 million for the year. The 10-K notes to the financial statements elaborate slightly, as found in the note 14 on long-term debt that states (edited lightly for clarity):

The Company is subject to certain covenants limiting. . . the ability and the ability of most of its subsidiaries to. . . pay dividends on or make distributions in respect of the Company’s or its subsidiaries’ capital stock or make investments or other restricted payments . . . In the fourth quarter of 2022, the Company amended certain of its covenants and restrictions with respect to the Revolving Credit Facility and Term Loan. . . the amendment modified the limits on restricted payments that we may make prior to the resolution of the Brazil Tax Dispute, to be the same as the restricted payment limits set forth in our Notes Indenture. This results in an increase in the limit. . . from $75 million to $90 million if the pro-forma consolidated leverage ratio is less than 2.00 to 1.00.

Sylvamo was in a position to use the increased limit in 2022, distributing $10 million in dividends and $80 million in share buybacks, and there is ongoing effort with the board to come up with ways to be freer to make those otherwise restricted payments. The Brazil tax dispute mentioned goes back to tax matters related to International Paper's Brazilian subsidiary in which the Brazilian tax authority is challenging a tax treatment of goodwill from 2007 - 2015, and it is still being litigated. Sylvamo does have an arrangement with International Paper to split any final cost up to a certain limit, but it is in Sylvamo's interest and the shareholders' interests to get this cleared up and put it behind them. Brazil is a major market for the company, as well as a major source of forestry assets that the company maintains, so staying on good terms there is an important long-term priority.

Conclusion

The good news on the Brazilian tax dispute is that Sylvamo's exposure should be limited to $120 million, or 40% of any settlement up to $300 million total, with International Paper bearing the other 60% and 100% of any amount greater than $300 million. Of course, there is no guarantee that the tax authority wouldn't also pursue something at a later date for taxes since 2015, but for now the limit of the damage is reasonably well established. The downside is that until it gets resolved, Sylvamo either must continue to attempt to amend its credit facilities to be more generous, or shareholders have to be patient to live with the covenant restrictions.

Last fall, I moved to the sidelines somewhat prematurely in a cautious view with the uncertainty of what would happen with the company's Russian facility, and not knowing yet the central bank's commitments on interest rates. Now, with the clarity of full year results and the strength of the guidance, I find that the attractiveness of the cash flows Sylvamo is generating relative to the price of the equity is about as compelling as it gets for a value investor. In spite of the tax overhang, I am optimistic that there will be a market recognition of the value here in time, and I am willing to go back and restore a buy rating on Sylvamo.

For further details see:

Sylvamo: Firing On All Cylinders, But Capped By Tax Dispute