SLVM - Sylvamo: Things Are Starting To Move

2024-01-08 02:21:07 ET

Summary

- Sylvamo Corporation's stock price has grown slightly, outperforming the S&P 500, but lacks a catalyst for significant growth.

- The company operates in a low-growth market and needs to focus on margin retention and delivering shareholder value.

- SLVM has expanded globally and categorized its business segments into Europe, Latin America, and North America, adjusting its product offerings to remain competitive.

Investment Rundown

Since covering Sylvamo Corporation ( SLVM ) back in late July last year the stock price has grown slightly, up 6.07% compared to the S&P 500 4.53% growth, making it a slight outperformer. My rating then was a hold and I think that was the right decision looking back. My key point then was a lack of catalyst for the company as it is operating in a rather low-growth market where it needs to focus on margin retention and delivering shareholder value to stay relevant in the eyes of investors. With a 2.12% dividend yield, it's a decent value play still I would say.

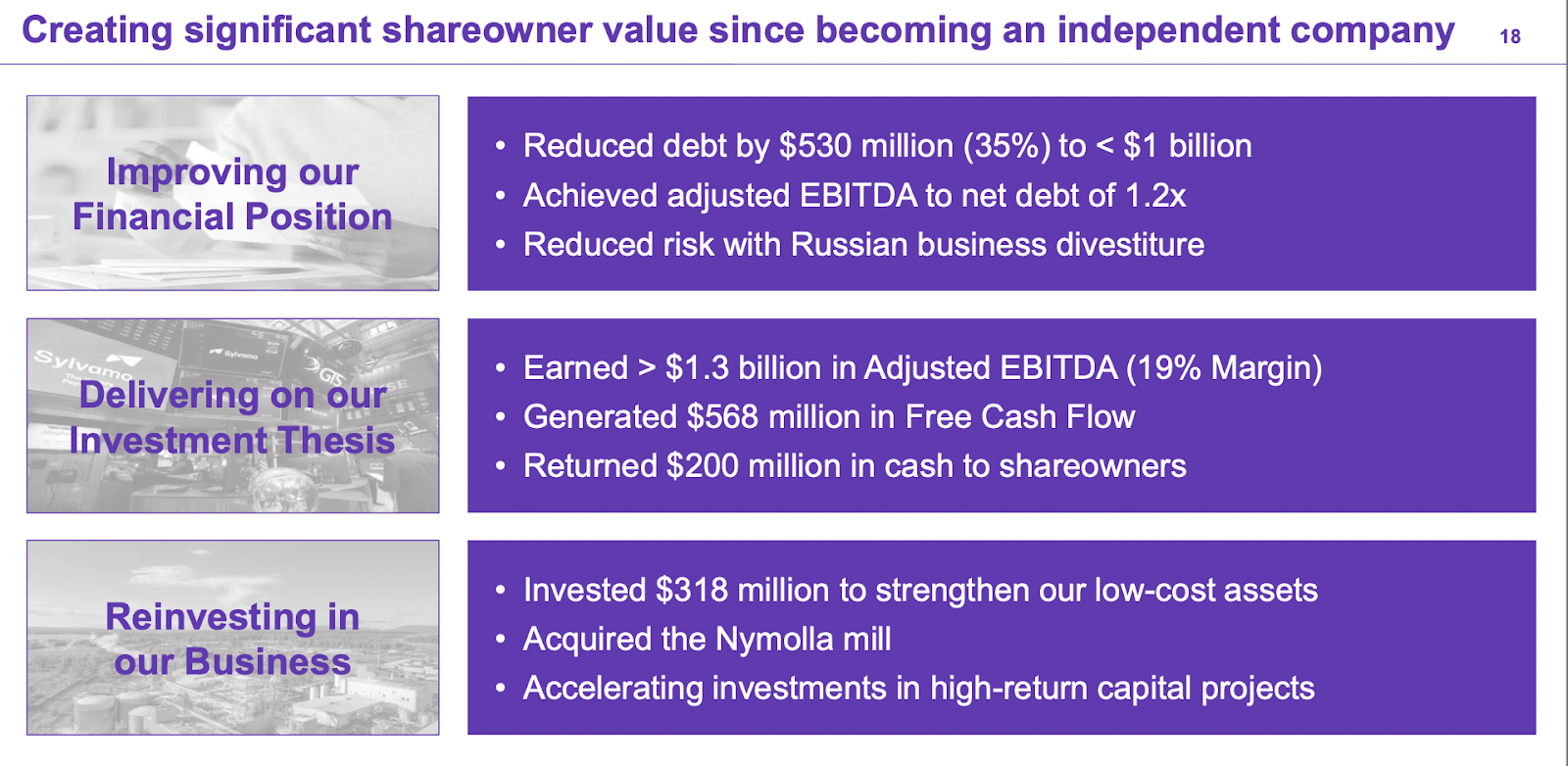

The low growth of the company means that the low valuation it trades at makes more sense. On a sequential basis, the company made some strong progress . The net income now sits at $58 million, up from $49 million in the second quarter of this year. The investment thesis that the company presents is that it can become a world paper company. It has low-cost mills in some very attractive regions right now. The company has a total capacity of 3.9 million short tons of uncoated freesheet and market pulp in total, putting it in a strong position both domestically but also globally as well. It seems there will continue to be a priority to maintain strong shareholder value through dividends and some buybacks. I think holding shares is still reasonable and I will continue having this rating for most likely the better part of 2024, depending of course if SLVM can raise the margins and production levels and there is a market for it too.

Company Segments

Established in 1898, SLVM has been dedicated to the production of paper products. The company has expanded its reach globally and categorizes its business segments into distinct regions, namely Europe, Latin America, and the North American segment. Despite its longstanding presence, SLVM encounters challenges in various markets, including issues such as destocking and fluctuating demand levels. Compounded by the phasing out of traditional paper products like offset paper and uncoated free sheets in favor of more cost-efficient digital solutions, SLVM is compelled to adjust its product offerings to remain competitive in the evolving market landscape.

{kind=link}

Each of SLVM's distinct segments is characterized by unique focus areas. In the European segment, the company specializes in the production of colored laser printing paper. Meanwhile, the Latin American segment serves as the location for the mills, contributing to the manufacturing processes. Additionally, within the North American segment, SLVM extends its offerings to include imaging and commercial printing solutions, showcasing a diverse range of capabilities across its operational regions.

Market Size (Statista)

What I have mentioned before is a lack of growth elements in many of the markets the company operates. Between 2022 and 2029 the market for paper and pulp is only expected to grow by 5% and be valued at $372 billion in total. I don't think the growth will be that impressive for SLVM during this period either. What could potentially fuel higher growth though is acquisitions, which would be an inorganic growth strategy to take on. In early 2023 the company acquired a company by the name of Nymolla Mill for €150 million. The transaction is setting SLVM up to be a strong competitor in the European paper market.

Earnings Highlights

{kind=link}

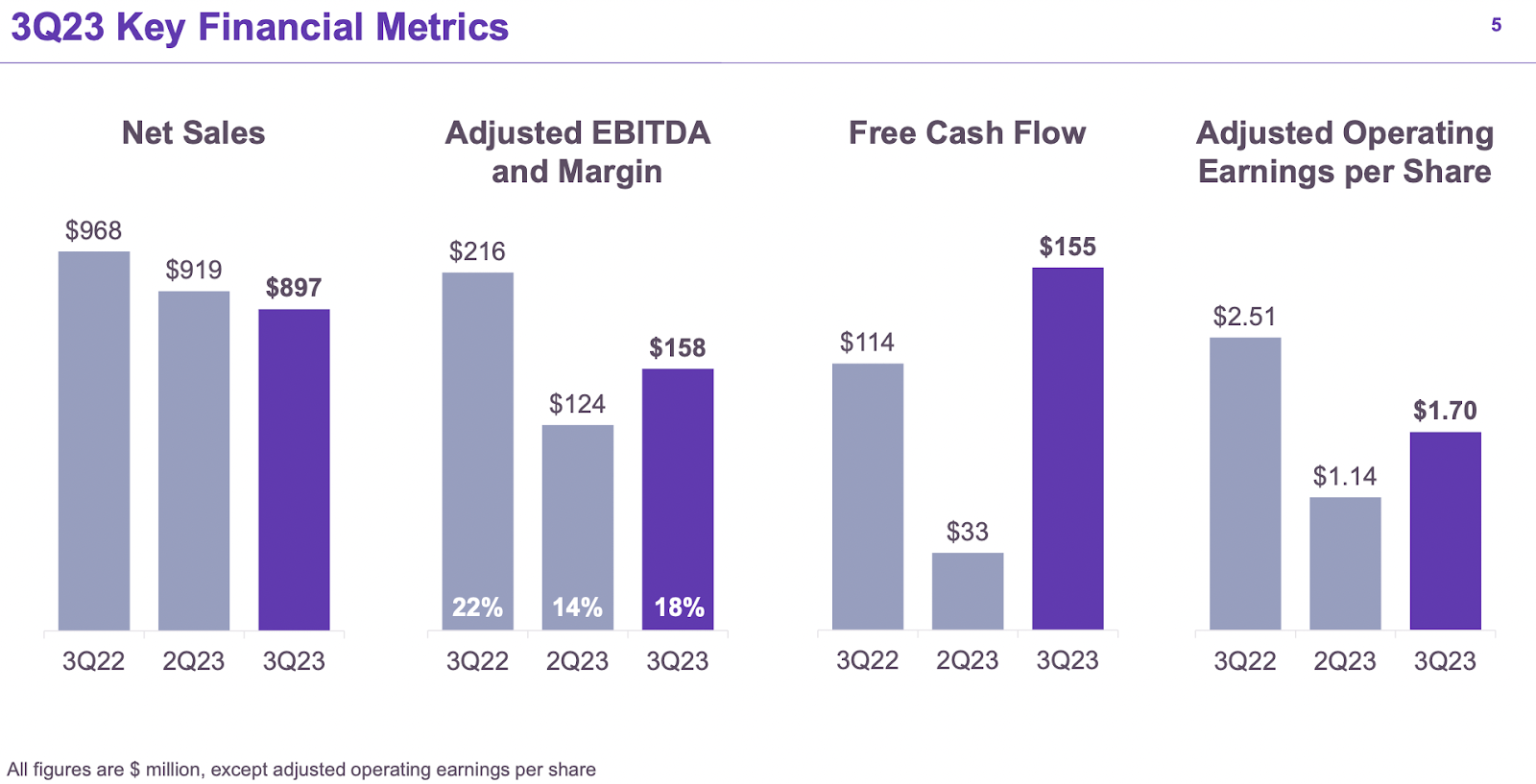

In the last quarter, the company saw a sight loss in sales but with strong margin growth was able to grow the EPS QoQ nonetheless. Sales came in at $897 million down from $968 million in Q3 FY222, largely due to softer prices for paper and pulp. Where my attention went the last quarter was the FCF for the business, now at $155 million in total. The TTM SLVM has repurchased shares for $133 million in total, a quite bullish sign, and perhaps a reason for the share price running up so quickly too.

{kind=link}

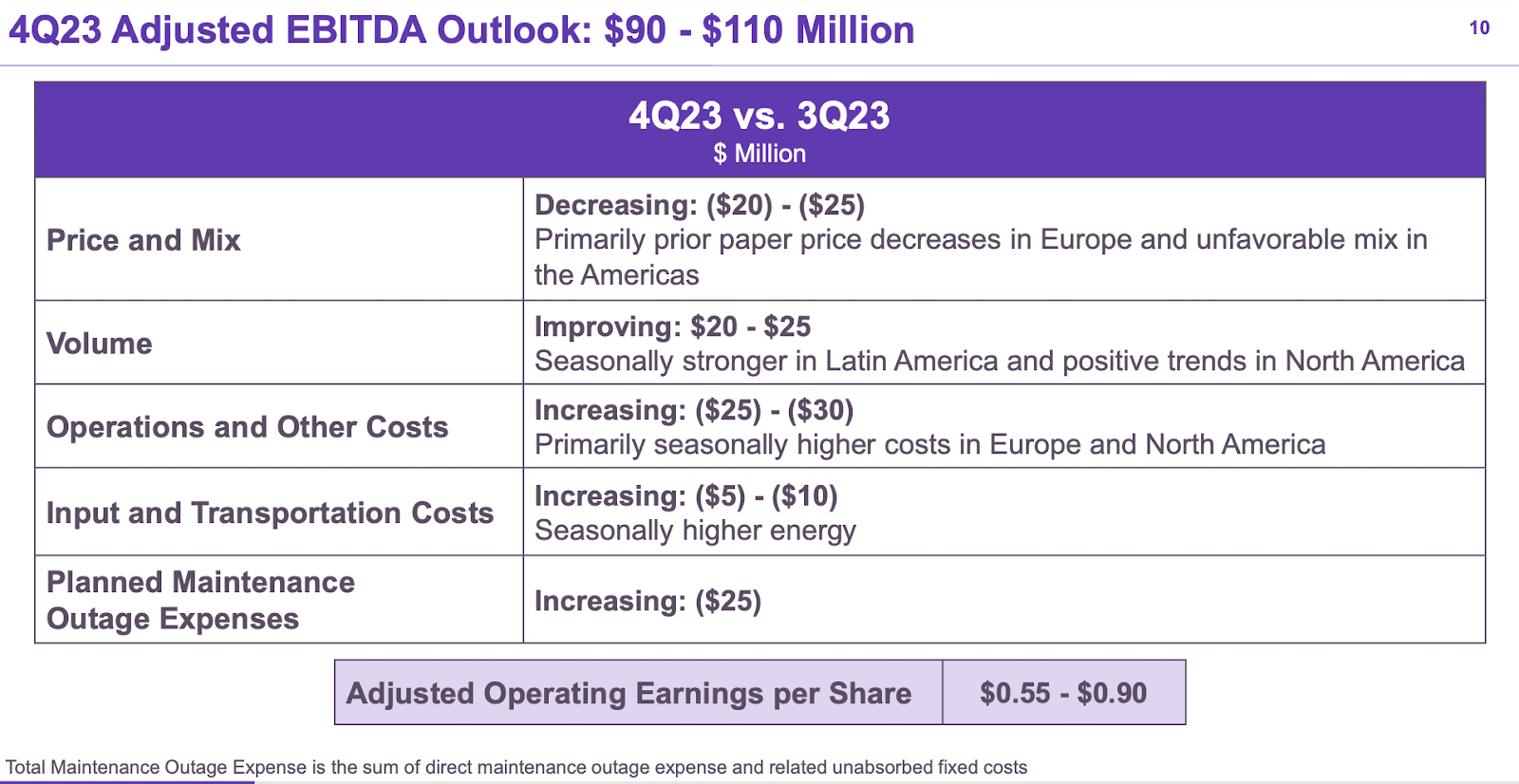

In the last earnings report, the management also provided some guidance for Q4 FY2023. Some trends seem to continue, like lower paper prices in Europe and an unfavorable mix in both North America and Latin America. This will likely impact the sales of the business so a key point to watch will be the margins instead. In 2024 we are set to start seeing some rate cuts, and that would help relieve SLVM from some of the earnings pressure it has had. Interest expenses are at $66 million now, and should rates come back to 2021 levels we might see something like $33 million in expenses instead. A nearly $30 million additional earnings would be a 10% increase, and perhaps a tailwind for the business and a reason for a higher multiple in the medium term if the company can continue its expansion strategy to become the world's paper company. My view on the company remains the same as the last article, a hold, I don't see a catalyst appearing, and growth will likely come from acquisitions in the coming decade. But I want to clarify that it's a rather positive hold and a buy would most likely come about if the stock price drops to undervalued territory, which I would consider being around 5x earnings, a 20% or so drop from today's multiple .

Risks

SLVM presently confronts a multitude of challenges that significantly impact its operational efficiency and financial outcomes. The combination of reduced seasonal volume and escalating seasonal costs exerts considerable pressure on the company's overall revenue and margins. With currencies fluctuating, I think SLVM has fared decently in the past quarters though, as the bottom line has expanded sequentially very well, without any severe currency impact. In terms of currency loss, SLVM did include a $78 million pre-tax charge related to its ceasing operations in Russia. This is a one-time charge and not something I think should weigh much on the business in the long term.

{kind=link}

I think there is quite a little downside right now to the company given the low valuation it already trades at. The company has like I said before, not posted that high growth numbers. It continues to be in the low single digits for the top line. The last few month's run-ups for the stock price have been quite rapid and I think there is a risk for some consolidation or potentially even an unproportionate downside risk should the markets correct in the coming quarters. Nonetheless, I don't think it's sufficient to warrant a sell here though.

{kind=link}

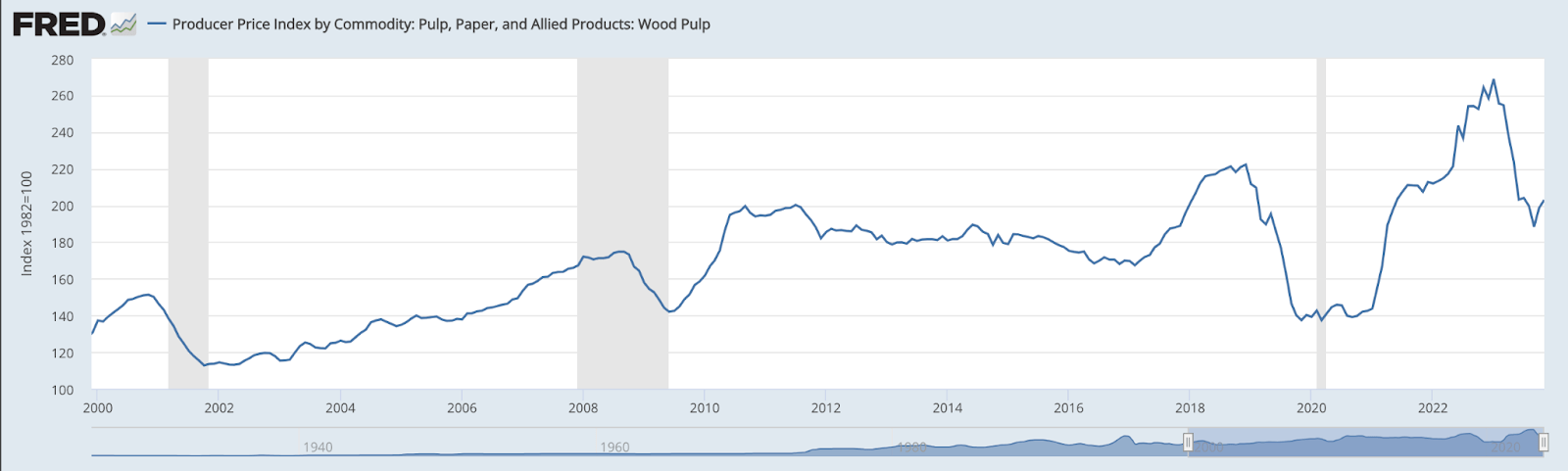

It is heavily dependent on positive market prices for paper and it has been quite volatile the last few years. In 2020 prices plummeted and SLVM saw revenues drop to $2.3 billion, down from $4 billion the year prior. Over the long term, revenues will organically grow through the appreciation of paper prices. The chart above showcases a steady level of growth since the early 2000s.

Final Words

I have covered SLVM before and I figured it was time for an update as we have now entered 2024. The company operates in what I think is a rather low-growth industry. Paper companies don't necessarily have the same growth prospects as semiconductor companies do. It's a commodity business where financial results are heavily tied to favorable prices of paper and pulp. What has made SLVM a decent bet here is the bottom-line improvements in the last few years, but it's not necessarily a catalyst enough to make it a buy this time around. I want to see more aggressive acquisition strategies as that is what I think would generate the best top and bottom-line percentage growth. With a priority to reward shareholders though I still consider the company a good hold with a dividend yield of 2% right now. My rating is the same as on July 27, a hold.

For further details see:

Sylvamo: Things Are Starting To Move