SYM - Symbotic: This Warehouse Transformer Has More Upside

2023-11-27 01:24:48 ET

Summary

- Symbotic's Q4 earnings beat expectations by $85 million, stock jumps 40%.

- The retail industry's labor and distribution challenges are driving demand for Symbotic's automated warehouse solutions.

- Symbotic has a comprehensive 5-pillar growth strategy in place to continue its strong growth trajectory.

- Although the company’s share price soared 40% after its earnings report, we believe that it is still undervalued according to our valuation metrics.

Symbotic Surpasses Expectations in Q4 Earnings and Soars 40%

On November 20, 2023, Symbotic ( SYM ) announced its Q4 results , which exceeded analysts’ forecasts. The company achieved its highest-ever revenue of $392 million, a 60% increase from the same period last year. The revenue growth was driven by continuing and new system installations and the completion of 2 systems. Symbotic reported a net loss of $45 million, an improvement from a net loss of $53 million last year. Adjusted EBITDA was $13 million, a turnaround from a loss of $20 million a year ago. This was the first time the company achieved a positive adjusted EBITDA, reflecting its strong operating efficiency and leverage.

For the fourth quarter of fiscal 2023, Symbotic guided above expectations. It expects revenue of $360 million (75% YoY), and an adjusted EBITDA of $11 million to $14 million. However, we think this guidance is conservative, as we will share our revenue forecasts in this article.

Also, we will look into the factors driving Symbotic’s remarkable growth, particularly in an industry experiencing an economic slowdown. Additionally, we will look at the market size, investigate the company’s growth strategy, and perform a valuation accordingly.

Retail Industry Challenges Driving Demand for Automated Warehouse Solutions

The retail industry is undergoing a transformation that creates a long-term secular demand for Symbotic solutions. The industry is facing several challenges that increase the costs and inflexibility of today's supply chains. To summarize these challenges:

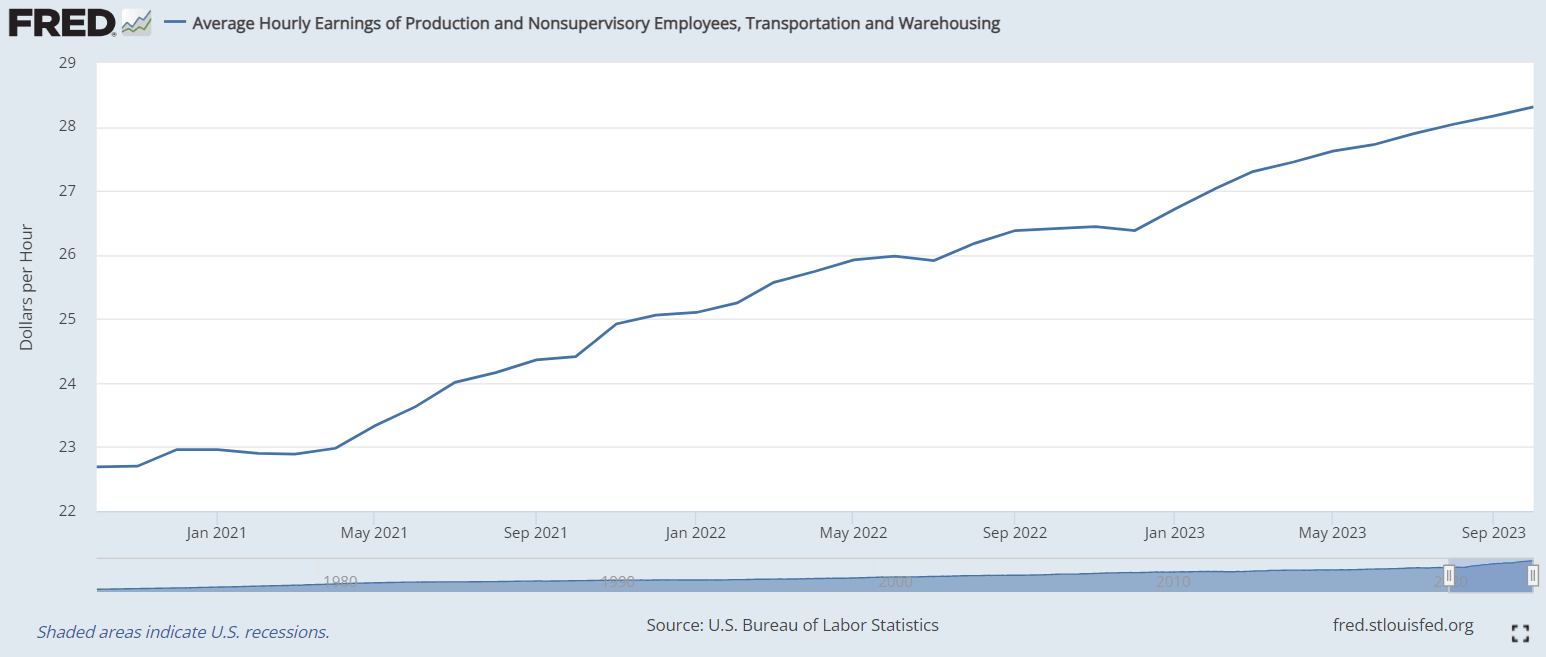

Labor Shortage and Cost —Warehouse labor is becoming harder to find and more expensive, as the workforce ages and becomes more educated. According to the US Bureau of Labor Statistics , warehouse staff wages rose by 25% from 2020 to 2023 (see below) and this trend is expected to continue. Warehouse workers also have a higher turnover rate than other workers, which creates additional replacement costs for employers.

Hourly Earnings of Nonsupervisory Employees, Transportation and Warehousing (Federal Reserve Bank of St. Louis)

{kind=link}

- Costly Omni-Channel Strategies —Online shopping is forcing brick-and-mortar retailers to support multiple distribution channels, such as traditional stores, online delivery, BOPIS (Buy Online Pick-up in Store), and reverse logistics. These channels add complexity to the distribution process, as they require delivering a diverse range of products to a wide range of locations, faster and in different ways.

- Growing Consumer Expectations and SKU Proliferation —The internet has given people access to more products, so they expect retailers to offer more product variety. At the same time, manufacturers are adopting personalization strategies, adding more SKUs, and changing them more frequently. These trends require retailers to store, handle, and make available more SKUs while managing seasonal variability. This requires either more specialized supply chain processes or more flexible existing processes.

All these factors are driving demand for highly automated warehouse solutions that can increase efficiency, accuracy, and speed of the retail distribution process. Existing warehouse automation systems are not designed to address these challenges or have outdated technologies that only automate low-value repetitive tasks.

Symbotic is aiming to resolve these problems and revolutionize the space with its AI-enabled robotics technology, designed to transform warehouse operations end-to-end.

$1 Trillion Market

One of the main reasons why we are optimistic about Symbotic is the huge market opportunity that they are pursuing. The company claims that its total addressable market ((TAM)) is nearly $1 trillion, which raises questions about its feasibility. When we check the warehouse automation market size, we see it's in the range of $50 billion . However, Symbotic is not a point solution like many of its competitors so it's not limited by this conventional market size. It offers an end-to-end platform that can transform any warehouse into a highly efficient autonomous fulfillment center. Also, by creating a new category of warehouse-as-a-service (WaaS), Symbotic is expanding its TAM to include not only existing tier-1 warehouse operators but also smaller or new ones who can benefit from its scalable and cost-effective platform.

{kind=link}

Considering its solution capabilities and its business model, we think that Symbotic’s comprehensive platform addresses the wider warehouse and storage industry, which is worth more than $1 trillion .

Symbotic Transforming Warehouse Operations

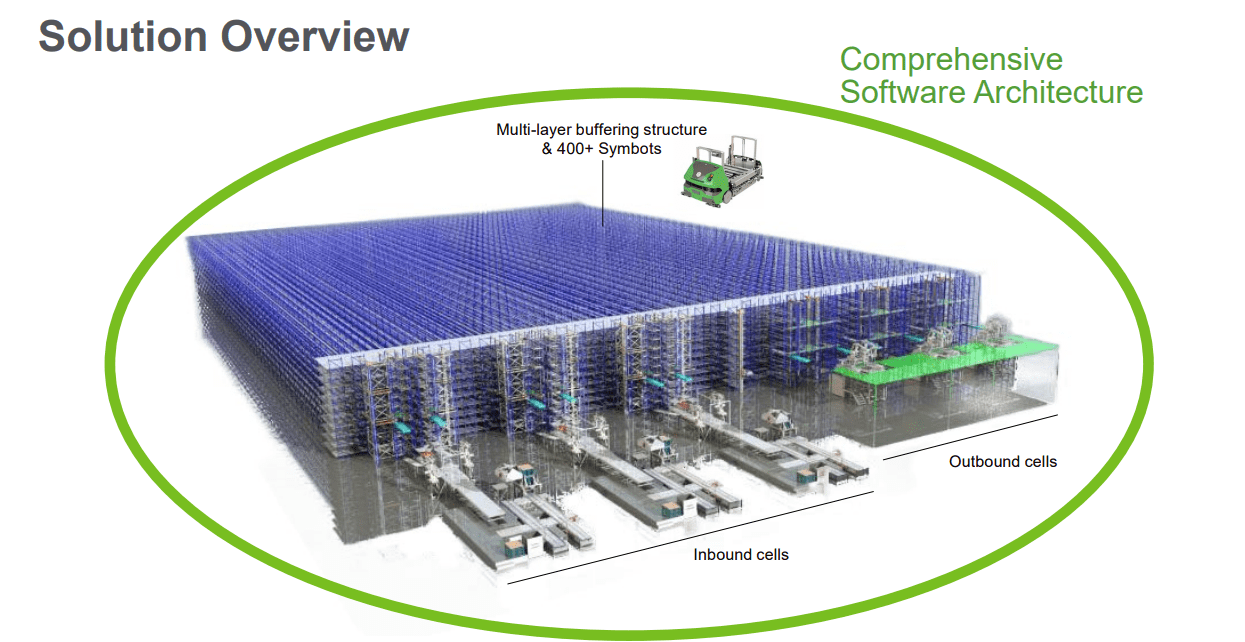

Symbotic was founded in 2007 by Richard B. Cohen. His vision is to reinvent warehouse management with a fully automated and high-density technology platform. The platform leverages AI, robotics, and software systems and enables customers to reduce supply chain labor costs, increase throughput, and improve inventory accuracy. We believe that the ROI for Symbotic systems is very high, and is a key factor contributing to the high demand for its products.

Symbotic Architecture (Symbotic)

{kind=link}

Symbotic 5-Pillar Growth Strategy

Symbotic wants to disrupt the supply chain industry with its innovative warehouse platform. We think that the company has the necessary vision and strategy in place to become a leader in this space. The company is successfully executing its strategic plan by expanding its customer base, improving its technology, and introducing new business models.

Symbotic's growth strategy is based on these five pillars:

- Deepen its relationships with existing customers : Symbotic works with tier-1 companies that have many stores and warehouses. Its customer base includes US largest retail companies, such as Walmart, Target, and Albertsons. The company has agreements with these tier-1 customers to transition some of their distribution centers to its platform. But its main goal is to secure all of its distribution centers, thereby strengthening its market presence and establishing deeper partnerships with these top-tier clients. For example, it has recently started the second wave of Walmart's five warehouse UNFI facilities deployment.

Walmart Delivery Truck (Symbotic)

{kind=link}

- Attract new customers in its current verticals : Symbotic has a lot of potential customers in the retail vertical. The company is actively looking for opportunities to onboard new clients within this vertical. A recent addition to their customer portfolio is Southern Glazer’s Wine & Spirits , the largest distributor of alcoholic beverages in the United States. Starting from 2025, Symbotic will implement its warehouse automation systems in Southern Glazer’s distribution centers.

Warehouse (Southern Glazers Wine & Spirits)

{kind=link}

- Enter new verticals: Symbotic believes that any vertical that involves moving goods through a distribution center can benefit from its platform. The company plans to expand to other verticals, such as non-food consumer packaged goods, auto parts, and third-party logistics. The company also plans to develop its refrigerated and frozen capabilities and enter the refrigerated and frozen food verticals.

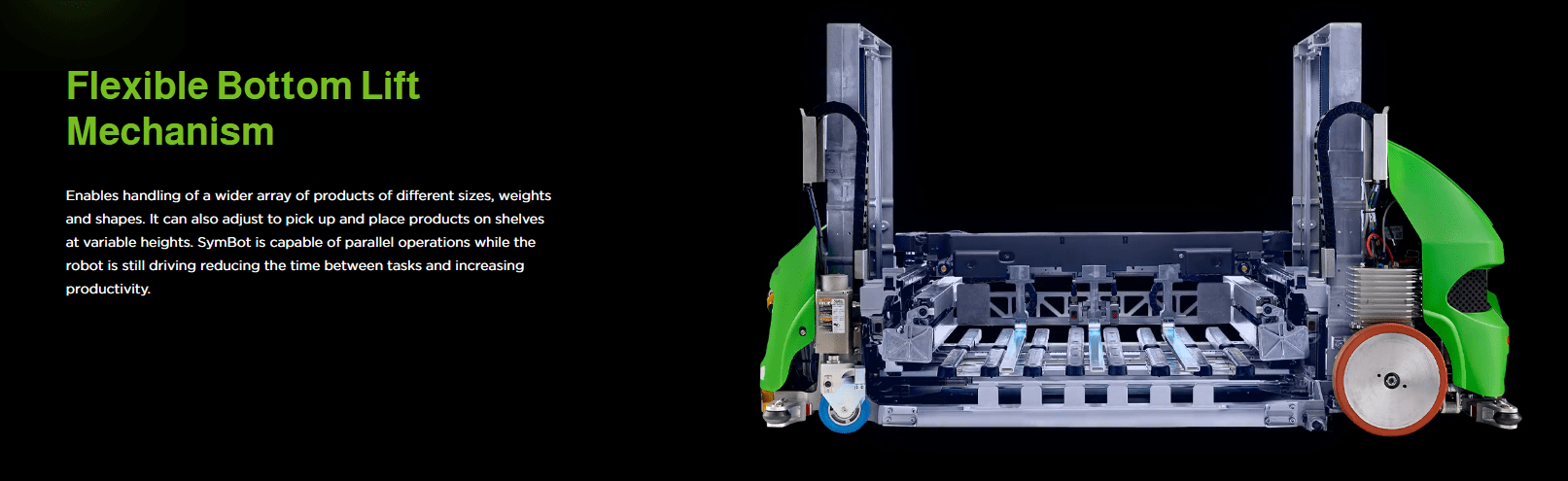

- Introduce new product offerings : Symbotic is continuously innovating in order to offer new products and services to its customers. For example, the company has released its newest autonomous robot, called SymBot , which is faster and has improved case handling. Another new product is the upcoming BreakPack system, designed to handle single items in addition to cases.

{kind=link}

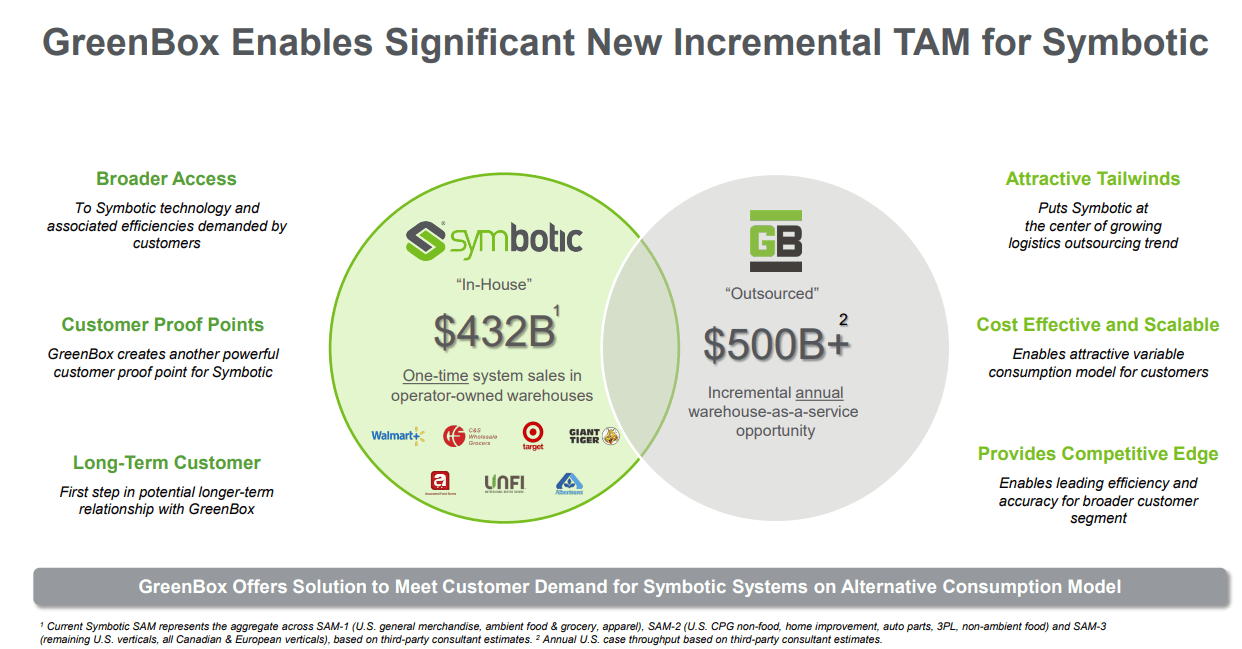

- New Business Models : The company is exploring new business models, such as reverse logistics and Warehouse-as-a-Service. Earlier this year, Symbotic announced Greenbox, a joint venture company that will provide Warehouse as a Service ((WAAS)) to customers who want to outsource their warehouse operations. Symbotic believes that GreenBox will add over $500 billion to its annual total addressable market. We view this joint venture agreement as a positive for Symbotic, as it not only doubles its TAM but also creates a recurring revenue model that is more sustainable.

- Expand geographically : The company is exploring potential markets in Europe, Latin America, and the Middle East, and has recently appointed a new VP for its European region.

Symbotic is a Founder-Led Company

We like founder-led companies and Symbotic is one of them, with Richard B. Cohen as the chairman and CEO. We believe that one of Symbotic’s greatest strengths lies in its founder-led structure, as companies led by their founders often have a unique market vision, commitment, and a long-term strategy that can drive innovation and growth. Cohen is also the chairman and CEO of C&S Wholesale Grocers , the largest wholesale grocery supply company in the US, which he has transformed from a regional family business to an industry leader. In a similar way, he envisions a long-term sustainable growth plan for Symbotic, invests heavily in R&D (R&D margin is 17% ), hires top talent, and partners with leading retailers across the country. We are impressed by Cohen’s vision and leadership, and we are confident that he will lead Symbotic to become a dominant player in the warehouse industry.

{kind=link}

Symbotic Revenue Trajectory

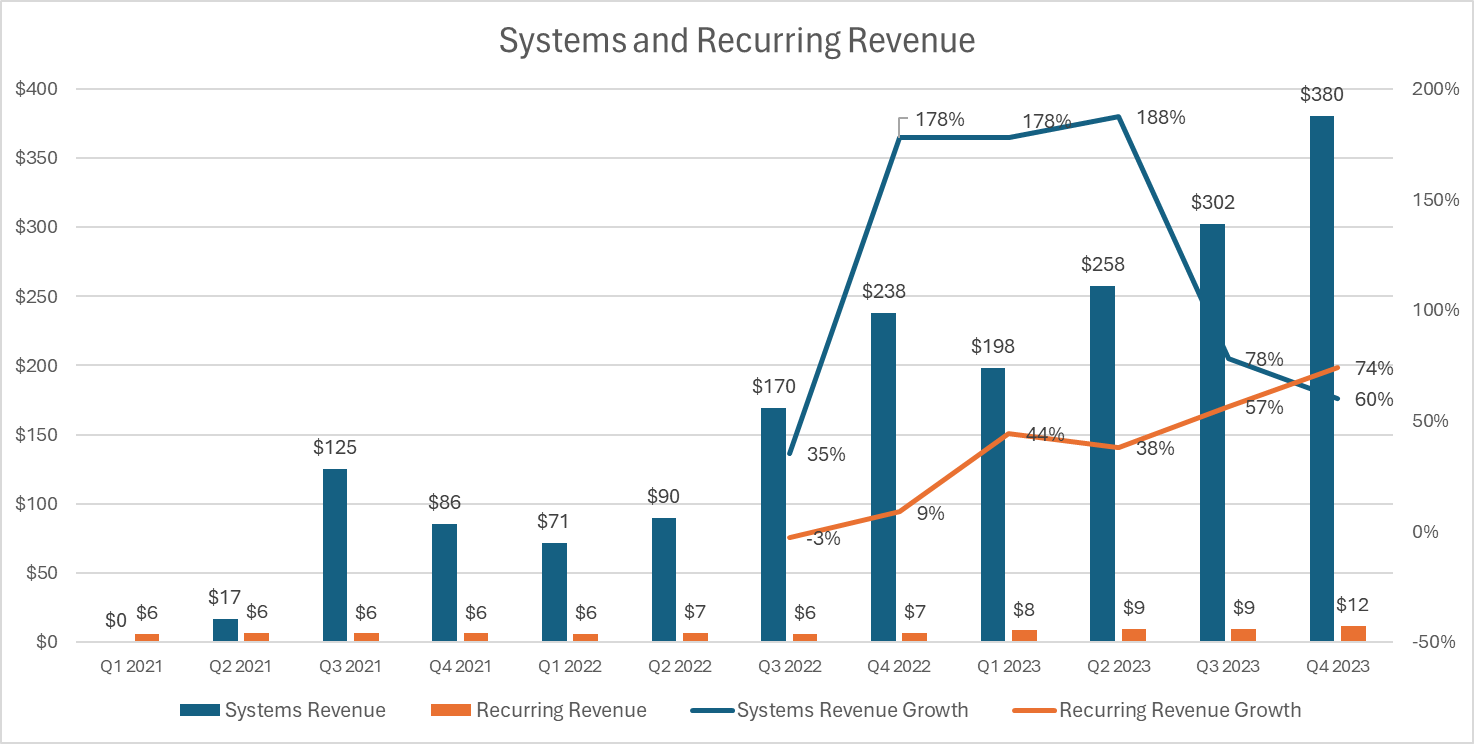

Here, we want to model Symbotic's future revenue trajectory. Symbotic Systems, the primary business segment of Symbotic, sells the autonomous robotic systems and has a non-recurring revenue model (depicted in blue in the chart below). The company’s other two segments, Operations, and Software Maintenance and Support generate recurring revenue streams once deployments finish and enter production (depicted in orange in the chart below). While the recurring revenue is currently relatively low compared to Systems revenue, it is gradually gaining momentum. Symbotic’s long-term goal is to shift to a mainly recurring revenue model, which can enable consistent growth and higher margins.

Symbotic Systems and Recurring Revenue (Author)

{kind=link}

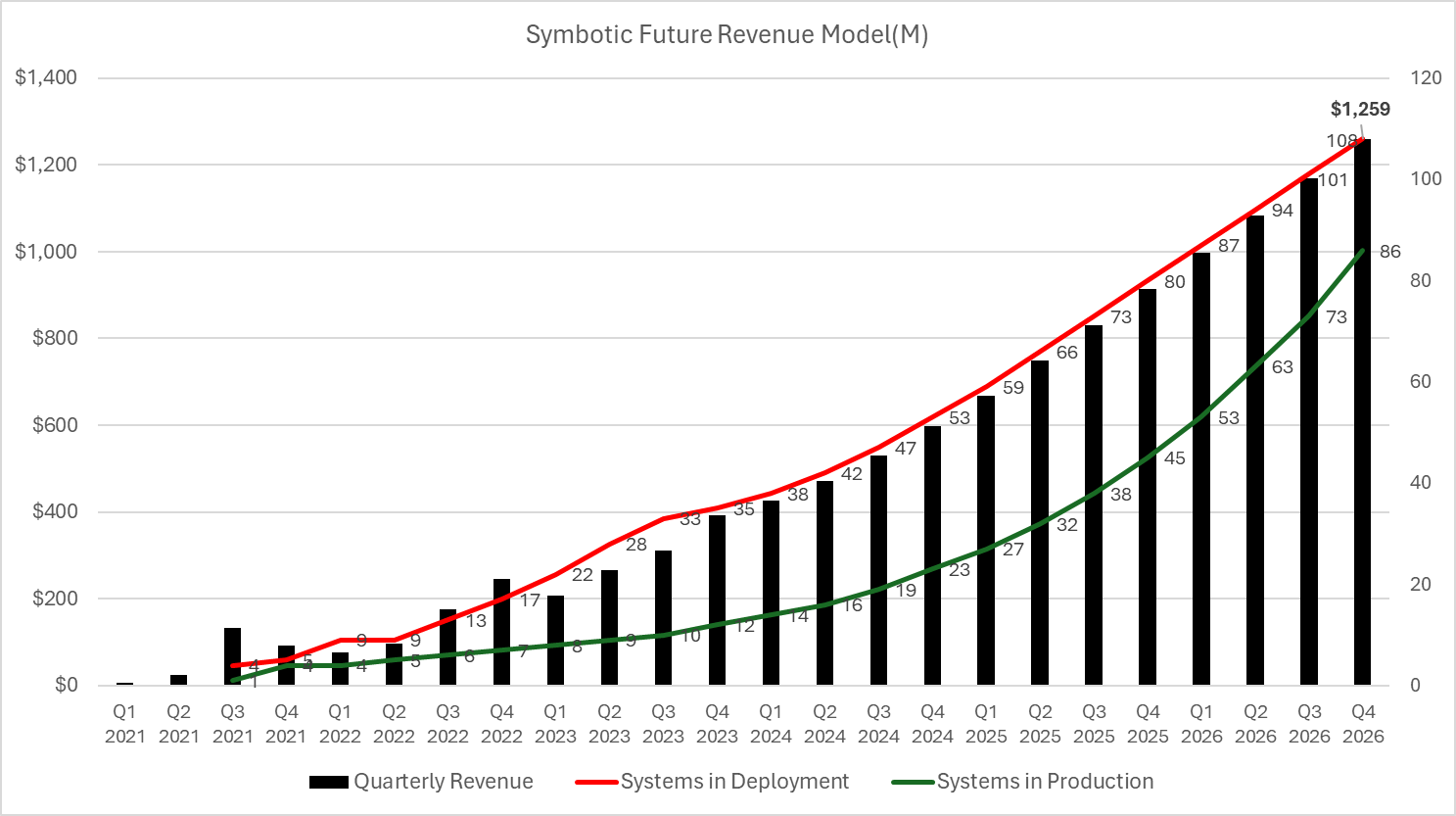

We did a 3-year future quarterly revenue projection for Symbotic until FY 2026 (see below) When we look at the chart, we can see that the current revenue momentum is very strong and is being driven by ongoing deployments (red line) and finished production systems (green line). Company doesn't have any revenue seasonality since it has a $12 billion backlog and is only constrained by deployment capacity. The company is expanding its deployments through outsourced partners, adding 4-5 new deployments every quarter. As of Q4, the company has 35 deployments and 12 production systems ongoing, up from 33 deployments and 10 productions in the previous quarter. Also, important to know is that there is a 2-year lag between the start of a deployment and production, however, the company is aiming to reduce this cycle to 6 months.

Quarterly Revenue Model (Author)

{kind=link}

Based on our growth model, we anticipate the total number of deployments to reach 108 and production systems to hit 86 in three years. Consequently, we project the total quarterly revenue to reach $1.26 billion by Q4, 2026, reflecting a CAGR of 57%.

Under these assumptions, our revenue forecast for FY2026 is $4.5 billion.

Valuation

Symbotic reported revenue of $1.18 billion for FY 2023 and its shares closed at $51 as of November 24, 2023, resulting in a market cap of $29 billion. Its P/S ratio jumped to 25x, which seems overvalued, but its forward multiples are converging towards 5x thanks to its high growth profile (see below)

SYM Price / Fwd Sales (Finbox)

{kind=link}

Based on our projections, we expect Symbotic to achieve a revenue of $4.5 billion in FY 2026, with a 3-yr CAGR of 57%. The company has a $12 billion backlog, so we see growth deceleration during the next 3 years as low risk. For a company with such a high growth rate, we believe that a 3-year forward P/S multiple of 15x is a reasonable valuation.

This implies a 3-year price target of $120, which represents 130% upside from the current price. Therefore, we think that Symbotic is still undervalued at these price levels.

Risks

Symbotic faces some risks that could affect its future performance and valuation. The main risks we see are:

- Walmart Concentration Risk : Symbotic’s revenue and growth depend largely on a few big customers, such as Walmart, Target, and Albertsons. Walmart alone accounted for 89% of its Q3 revenue, which creates a critical dependency. Although the company is diversifying its customer base with new accounts, any changes in the terms, conditions, or relations with Walmart could affect Symbotic’s business significantly.

- Competition: Symbotic's platform relies on advanced technologies, such as robotics, AI, and machine learning, that are constantly evolving and improving. Symbotic may face competition from other technology companies like Amazon that develop similar or superior technologies, or that offer lower prices.

Conclusion

A clear growth strategy, a new Warehouse-as-a-Service business model, continuous innovation of new products, and vertical and global expansion opportunities position Symbotic as a leader in the warehouse automation space.

Examining Symbotic's revenue trajectory also reveals a strong upward momentum. Although the company’s share price soared 40% after its earnings report, we believe that it is still undervalued according to our valuation metrics.

We rate Symbotic as a Buy.

For further details see:

Symbotic: This Warehouse Transformer Has More Upside