SYIEF - Symrise: Cheaper Than Before But Not A Bargain

Summary

- Symrise reported great results for the first half of 2022 and its trading update for the third quarter is also showing high growth rates.

- In the last two years, Symrise acquired several different companies and could grow its revenue by acquisitions.

- And when calculating with rather optimistic assumptions, Symrise might be undervalued - but I would be cautious.

In my last article about Symrise ( SYIEF ) I called the stock still overvalued (despite giving the stock a “Hold” rating). Since August 2021, when my last article was published the stock declined about 25% - however this decline is in U.S. dollars and Symrise as a German business is reporting in Euro. On August 20, 2021, Symrise was trading for €125.50 and now, at the time of writing, the stock can be bought for €104.50. This is resulting in a more modest decline of only 16.7% as FX effects also contributed to the 25% decline in U.S. dollar.

In the following article, I will provide an update about Symrise and try to answer the question if the decline was enough to not see Symrise as overvalued anymore.

Business Description

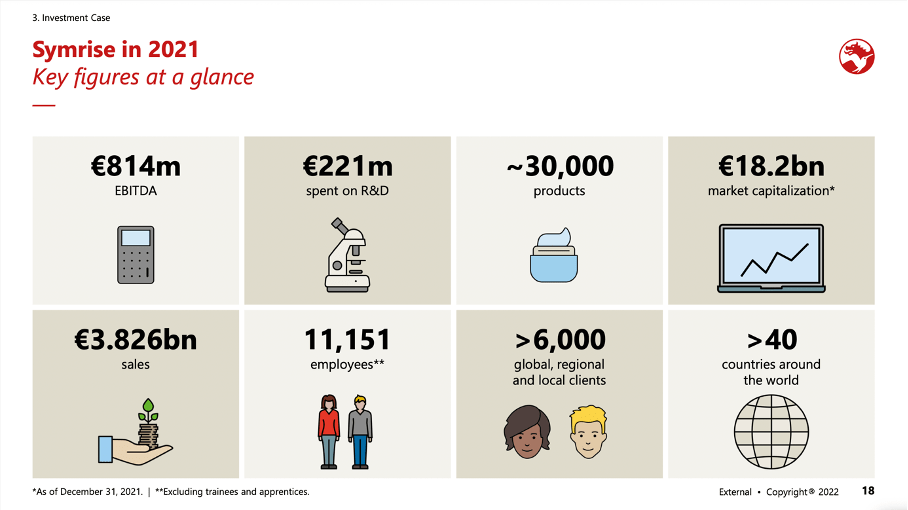

Symrise was founded in 2003 in Holzminden, Germany by the merger of Haarmann & Reimer, which was founded in 1874 and acquired by Bayer ( BAYZF ) in 1953 and Dragoco, which was founded in 1919. In 2021, Symrise generated €3,826 million in sales and the company has over 11,000 employees and over 30,000 different products.

{kind=link}

Symrise is providing flavor and fragrance experience for food production. It is offering products for different application areas – like food and pet food, beverages, dairy or snack food as well as hair care and oral care of cosmetic ingredients as well as consumer fragrances. The company claims that people interact with the products of Symrise about 20-30 times per day – from the toothpaste in the morning to the food one eats, the beverages one drinks, or the perfume used during the day. Symrise is reporting in two different segments – Scent & Care (which generated €1,491 million in sales – 39% of total sales) and Taste, Nutrition & Health (€2,335 million in sales – 61% of total sales). For more information about the business and the wide economic moat, see my article “ Hidden Stock Market Gems: Symrise "

Intrinsic Value Calculation I

The biggest issue I had with Symrise in my last article was the valuation of the stock. At the time of writing, Symrise was trading for 50 times earnings and despite the company having a wide economic moat around its business and growing with a solid pace, such a valuation multiple was not justified. When looking at the TTM earnings per share of €2.93 (H2/21 and H1/22 as the company does not report Q3/22 EPS) we get a P/E ratio of 36.

Although the price-earnings ratio is lower than about 1.5 years ago, I always get skeptical when stocks are trading for a valuation multiple above 30 as there are very rare instances when such a valuation multiple is justified. But let’s look at the business and the last results to determine if such a high valuation multiple could be justified for Symrise.

Results

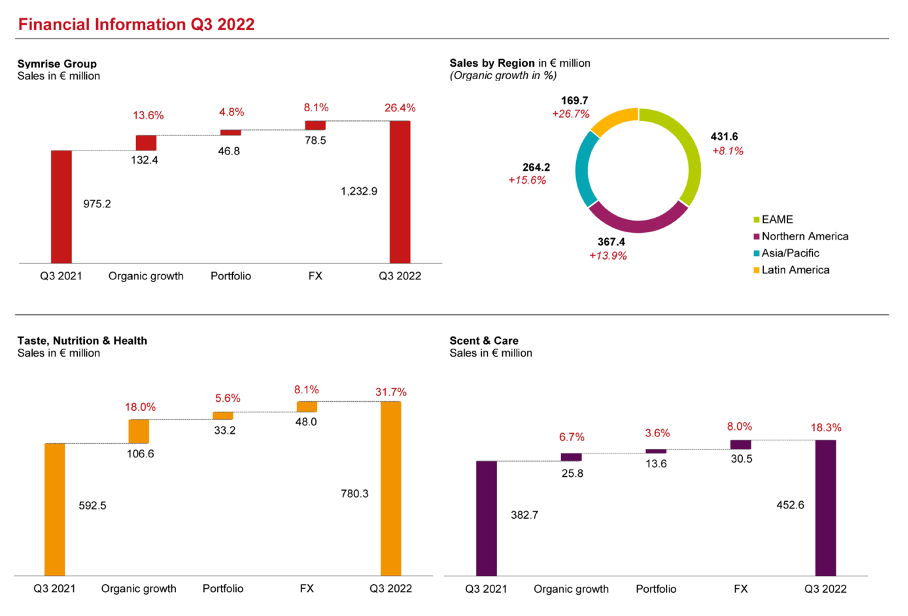

We can start by looking at the results for the third quarter of fiscal 2022, but like many other European companies Symrise is issuing only a “Trading Update” with limited financial information. Organic sales grew 26.4% year-over-year from €975.2 million in Q3/21 to €1,232.9 million in Q3/22. And while positive currency effects contributed to growth, organic sales growth was still 13.6%.

{kind=link}

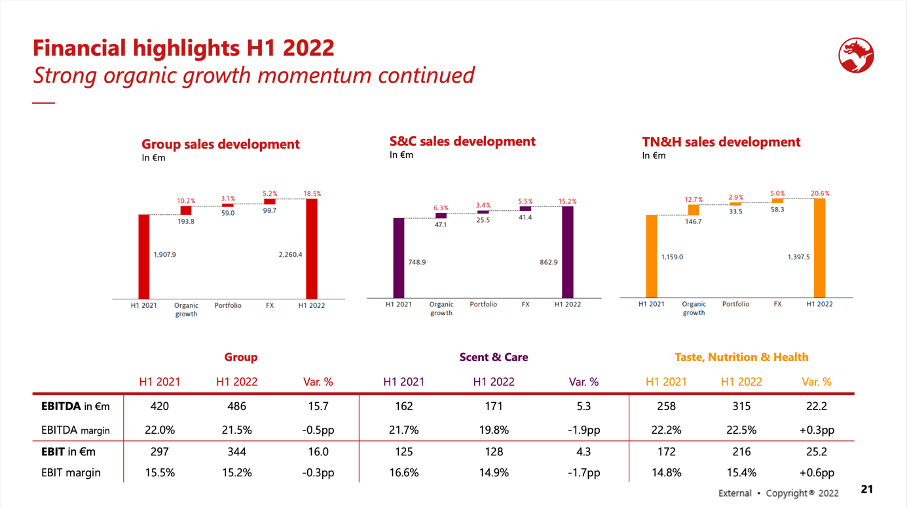

When looking at the results for the first half of fiscal 2022, sales for the Symrise Group increased from €1,908 million in H1/21 to €2,260 million in H1/22 – resulting in 18.5% year-over-year growth (with organic sales growth being 10.2%). EBIT also increased 16.0% year-over-year from €296.6 million in the first half of 2021 to €344.2 million in the first half of 2022. And finally, earnings per share increased from €1.45 to €1.64 – 13.1% year-over-year growth.

{kind=link}

When looking at the two different segments both contributed to growth. And while “Scent & Care” could grow “only” 15.2% (organic growth being 6.3%), “Taste, Nutrition & Health” increased 20.6% (with organic growth being 12.7%).

Symrise Investor Presentation September 2022

{kind=link}

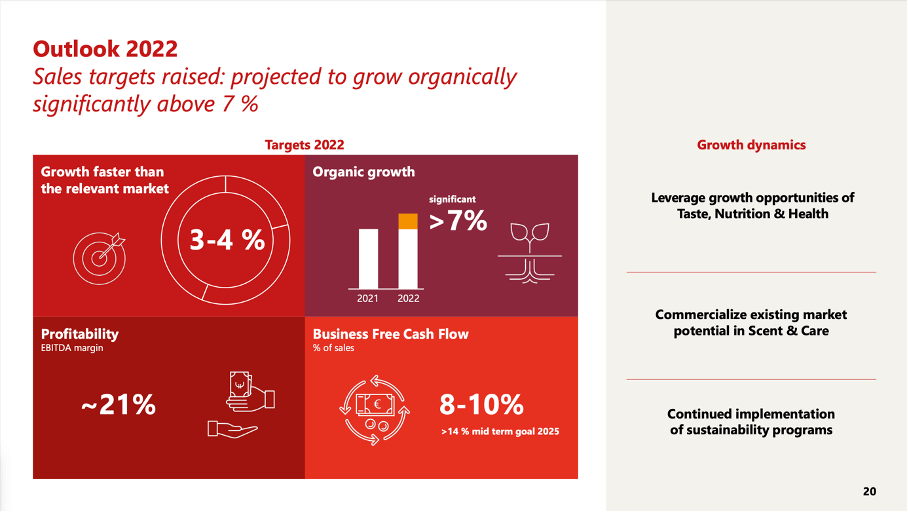

And for the full year of fiscal 2022, Symrise is expecting to clearly outgrow the market with organic growth being significant above its 7% growth target (we will get back to that).

{kind=link}

Growth By Acquisitions

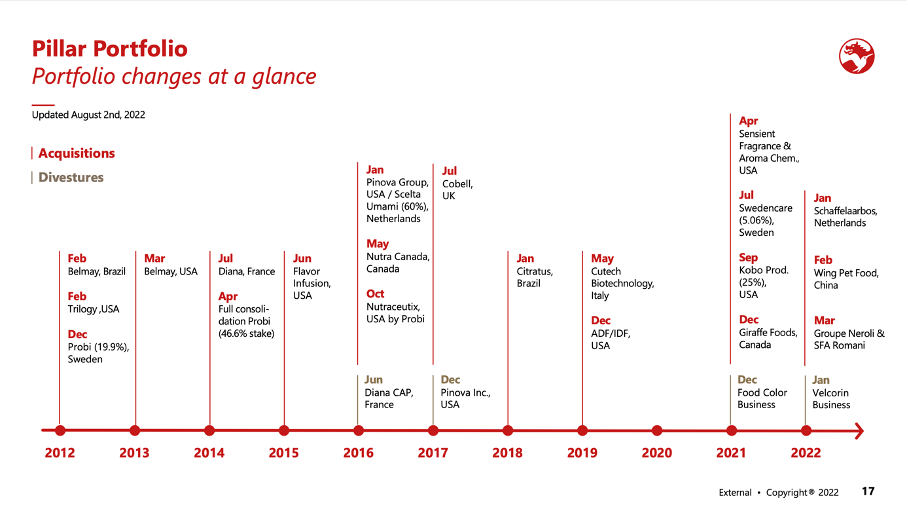

Since my last article was published in August 2021, Symrise made several acquisitions – which is one way to grow for the business. At the end of 2021, Symrise acquired the Canadian company Giraffe Foods Group, which is a producer of customized sauces, dips, dressings, syrups, and beverages for business-to-business customers in the home meal replacement, food service and retail markets. Final acquisition costs were €324.8 million.

In January 2022, Symrise acquired Schaffelaarbos B.V., which is a leading supplier of sustainably sourced proteins from eggs in the feed industry in the European Union. The company’s annual sales are around €25 million and total acquisition costs were €158.1 million. In April 2022, Symrise also acquired two French companies – Essence Ciel with its subsidiary SFA Romani as well as Neroli Invest DL. These two high-end fragrance companies will strengthen Symrise’s position in the area of luxury perfumes. Total payments were €127.6 million and combined annual sales of both companies exceed €40 million.

Additionally, Symrise invested in Swedencare AB – a supplier of premium, care, and health products for pets. Symrise spent a total amount of €318.2 million and the investment was made in the context of two capital increases by Swedencare.

Symrise Investor Presentation September 2022

{kind=link}

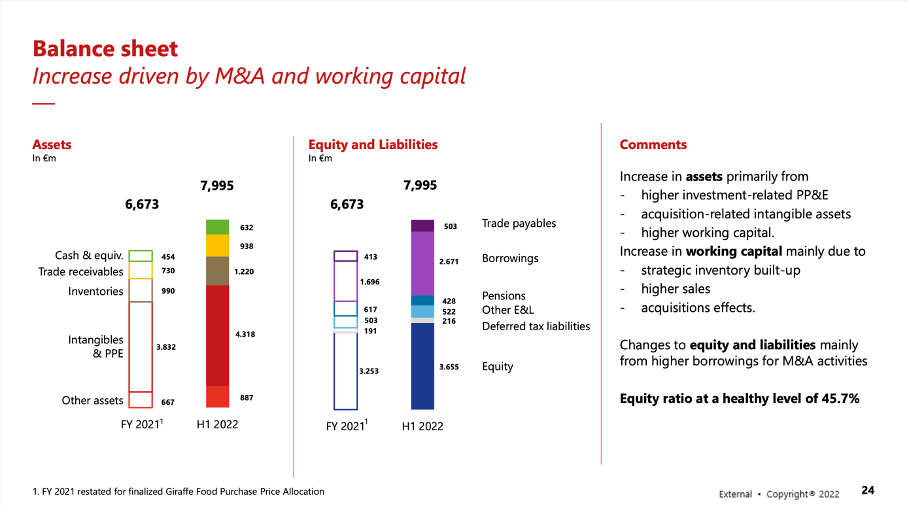

These acquisitions also had an impact on the balance sheet and led to higher debt levels. On June 30, 2022 – the latest data we have – the company has €285 million in short-term borrowings as well as €2,386 million in long-term borrowings. When comparing the total debt to the total equity of €3,655 million we get a still acceptable debt-equity ratio of 0.73. And when comparing the total debt to the EBIT of €559 million in fiscal 2021, it would take about 4.8 years to repay the outstanding debt – a rather long time. However, we should take into account that Symrise also has €632 million in cash and cash equivalents. When taking that amount to repay outstanding debt, it would take only about 3.6 times fiscal 2021 EBIT to repay outstanding debt.

Symrise Investor Presentation September 2022

{kind=link}

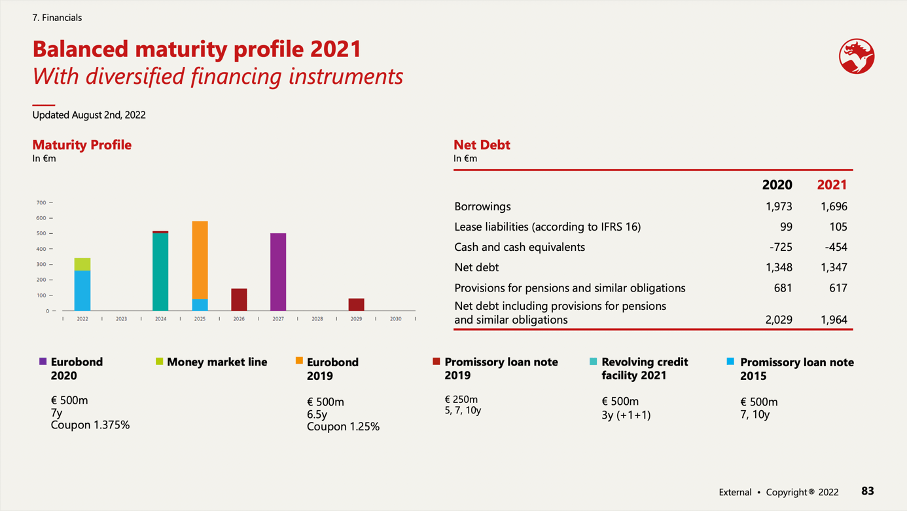

The balance sheet worsened a bit in the last few quarters, but there is still no reason to worry. Although debt levels are now higher, Symrise should be able to meet all its payments (according to the maturity profile).

{kind=link}

Growth

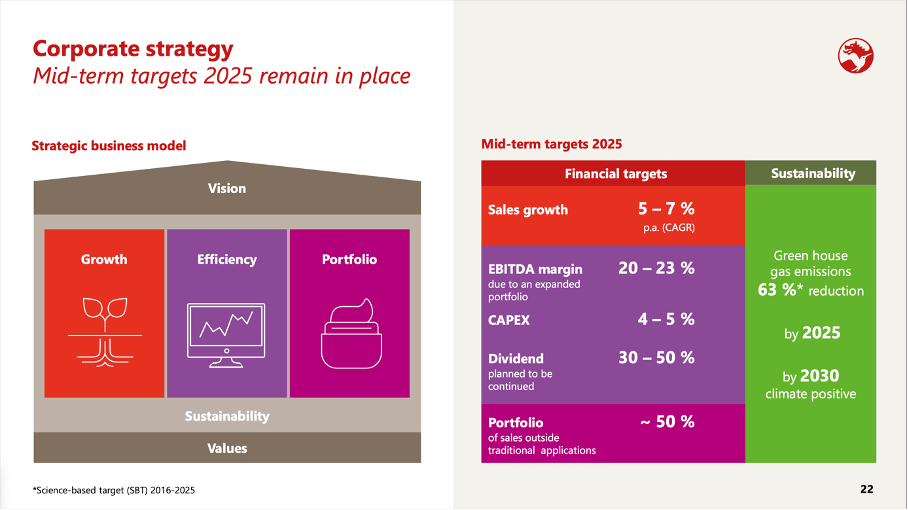

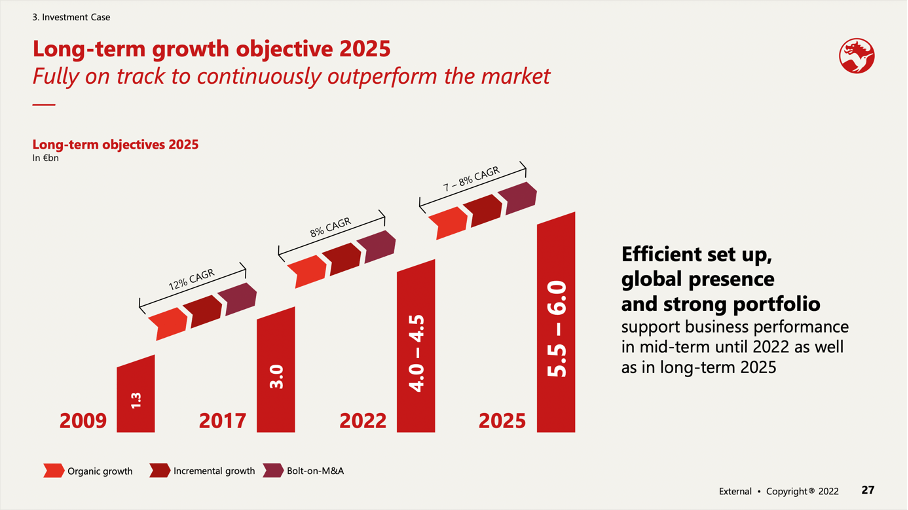

While acquisitions are one way to grow, Symrise is not just growing by acquisitions. Especially in the last few quarters, the company reported high organic growth rates and the business is confident sales will grow between 5% and 7% in the next few years and sales are expected to be between €5.5 billion and €6.0 billion in 2025.

{kind=link}

When looking at the growth potential of the underlying market, studies see the global perfume market growing with a CAGR of 5.9% until 2030. Other studies are seeing an annual growth rate of 5.0% until 2028. The food flavors market is also projected to grow with a CAGR of 4.64% until 2028. Other studies are seeing only 3.6% growth until 2030 for the global food flavor market while we can also find studies expecting the global demand for food flavors to increase with a CAGR of 6.2%. Overall, we can expect the underlying market to grow about 5% annually for the next few years and Symrise should be able to achieve its sales growth target of 5% to 7% in the next few years.

Intrinsic Value Calculation II

When only looking at the price-earnings ratio, Symrise seems to be overvalued and not a good investment. However, simple valuation metrics can often be misleading – instead a discount cash flow calculation should provide us with better insights and help us to decide if a stock can be bought or not.

{kind=link}

For 2025, let’s be optimistic and assume €6 billion in sales and Symrise being able to generate 14% of sales as free cash flow – this would result in a free cash flow of €840 million. For the years following 2025 we assume 7% annual growth – in line with the company’s mid-term financial targets – followed by 6% growth till perpetuity in 10 years from now. For 2023 we assume about €400 million in free cash flow as the company is right now only able to generate about 8% to 10% of sales as free cash flow. For fiscal 2024 we assume €620 million in free cash flow (midpoint between now and 2025). When calculating with these assumptions, a 10% discount rate and 139.77 million outstanding shares, we get an intrinsic value of €137.72 for Symrise and the stock would not be overvalued as the P/E ratio is suggesting but undervalued by almost 25%.

However, I see some problems with this optimistic calculation:

- These assumptions are not including a recession, which will most likely hit the world in 2023. And although Symrise is rather recession-resilient, it seems likely that Symrise won’t be able to increase margins in such a market environment and generate much higher free cash flow.

- Additionally, assuming 14% of sales enduing up as free cash flow is certainly achievable for Symrise but it can also be seen as an optimistic assumption. In the years since 2016 it was lower in most years.

- And when comparing net income to the free cash flow, it seems quite optimistic to assume €800 million in free cash flow in two years from now when net income was not higher than €375 million so far. In the last few years, it was mostly between €250 million and €300 million.

{kind=link}

So, I would be rather cautious if these assumptions are realistic for Symrise and if the stock is really undervalued.

Conclusion

In my opinion, Symrise is still a “Hold” and while I would not sell the stock as shareholder, I also won’t buy the stock right now. For me, the stock is still a bit too expensive and certainly not a bargain.

For further details see:

Symrise: Cheaper Than Before But Not A Bargain