SYIEF - Symrise: Market Seems To Have Already Priced In Near Term And Regulatory Risks

2023-03-13 03:28:24 ET

Summary

- Symrise is facing several negative factors, including the risk of customer destocking, slower end-market demand, and a regulatory investigation overhang.

- Despite these risks, the market seems to have already priced in some of the impacts, and management's guidance for FY23 is encouraging.

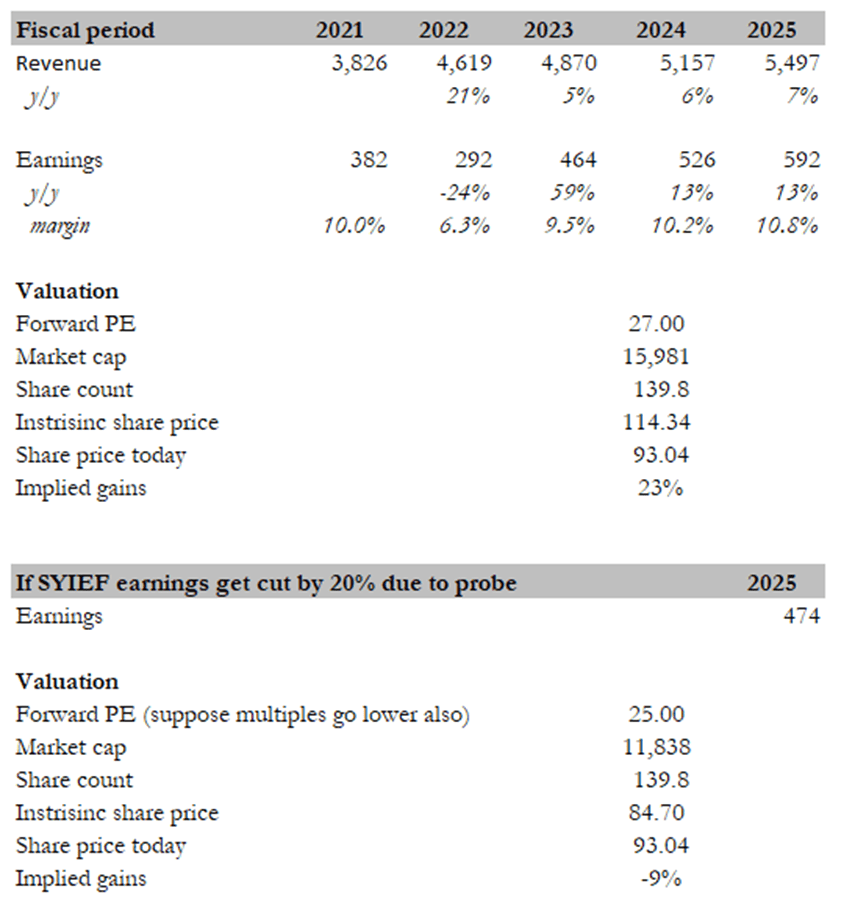

- Based on scenario analysis, the risk/reward ratio for investing in the company appears to be favorable, with a potential 23% upside to a 10% downside.

Overview

Symrise ( SYIEF ) has a lot of negative things going for it. There is a risk of customer destocking, slower end-market demand, and the obvious impact of higher energy and labor costs. Furthermore, there is a regulatory overhang for FY23 that is equivalent to holding a gun to SYIEF's head. However, based on my scenario analysis (shown below), it appears that investors have already priced in the risk of a regulatory investigation. If SYIEF can meet consensus estimates, the risk/reward ratio appears to be favorable. I recommend purchasing a small position that will provide exposure to this appealing risk/reward situation while also being small enough to have no impact on the overall portfolio if things go wrong.

FY22 results

Following the release of preliminary results in January, the SYIEF reported FY22 earnings, which failed to meet the consensus in terms of EBITDA and profits. However, there was a positive 11.5% growth in the fourth quarter of 2022, which exceeded expectations due to a strong performance in Taste and Nutrition, but Scent & Care was well below expectations. The EBITDA margin was also anticipated to fall below the consensus, as per the January release. Looking ahead to FY23, the guidance suggests that there will be 5-7% growth on a like-for-like basis and an unchanged EBITDA margin. This is broadly in line with expectations.

Regulation overhang

For those of you who are unaware, regulators are looking into a possible violation of cartel law in the production of fragrances and fragrance ingredients. I anticipate this to be a lengthy investigation, the results of which could result in fines that significantly impact European sales (maximum of 10% of global turnover). Based on the news, I anticipate a significant impact on SYIEF due to the fund's 37% exposure to Europe. Since this probe is expected to last several years, I do not anticipate the cloud of uncertainty surrounding the stock to dissipate anytime soon. That said, as I discussed below, the market seems to have already priced in a fair bit of impact from this news.

Guidance

Management has restated its mid-term goals, which include growing sales organically by 5-7% annually and increasing the EBITDA margin to 20-23% by the end of FY25. As for FY23, management guided organic growth of 5-7%, with an EBITDA margin of 20% and a FCF margin of 12%.

Since the miss was already known as per the Jan release, I believe most attention was focused on guidance, which turned out to be in-line with what consensus are expecting. That said, the guidance for normalized 5-7% organic sales growth in FY23, driven equally by volume and pricing, was definitely encouraging, as was the management's commentary on the 1Q's improvement so far compared to the 4Q. From what I can tell, management is taking a more cautious approach with this guide by factoring in only a moderate increase in commodity prices and a much larger increase in personnel costs compared to previous years. The ultimate impact from these two factors may be less than management expects, leading to a beat in guidance, because they depend on the development of the macro economy. In addition, management seems to be hinting at a brighter volume growth outlook than its main competitor Givaudan ( GVDNY ). based on my math.

Valuation

I created a simple model to depict two scenarios. First, suppose the investigation found no fault and management reached consensus figures (which is largely a function of guidance anyway). Using consensus figures, SYIEF should generate EUR5.5 billion in revenue and EUR592 million in earnings in FY25; at its current multiple, it would be worth EUR16 billion in market cap, equating to EUR114 per share or a 23% upside.

The second scenario assumes SYIEF was found guilty as a result of the investigation. While we don't know the exact impact on earnings and multiples, I made the simple assumption that earnings could be impacted by 20% (10% of maximum global turnover could result in a much higher earnings impact due to difference in margin) and multiples could be reduced by 2x to account for any short-term volatility. The result appears to be a 10% drop from the current price.

Put together, the risk/reward appears to be 23% upside to 10% downside, which appears to be a pretty good deal (2:1 ratio). And if the downside from the probe is less than I anticipated, the risk/reward ratio will be much better.

{kind=link}

Conclusion

While there are several negative factors impacting SYIEF, including the risk of customer destocking, slower end-market demand, and the regulatory investigation overhang, my scenario analysis suggests that the market has already priced in these risks to a certain extend. Moreover, management's guidance for FY23 is encouraging, with a normalized 5-7% organic sales growth and a cautious approach to factoring in commodity and personnel costs. Overall, I recommend purchasing a small position in SYIEF to take advantage of this appealing risk/reward situation, while also being small enough to have no impact on the overall portfolio if things go wrong.

For further details see:

Symrise: Market Seems To Have Already Priced In Near Term And Regulatory Risks