SYNA - Synaptics Incorporated: Battling Inventory Issues But Efficiently

2023-07-16 06:45:54 ET

Summary

- Synaptics Incorporated has generated around 72% of its total revenues from the IoT market in 2023, with the IoT market expected to generate a 26.1% CAGR between 2023 and 2030.

- The company has a strong portfolio of offerings, including ConnectSmart, DisplayLink, and VideoSmart, and is expanding into more smart solutions like fingerprint ID and efficient interaction solutions with devices.

- Synaptics has a massive share buyback plan, with $977 million still available for use, there is a lot of potential value for investors to get here.

Investment Rundown

Facing some short-term headwinds like inventory difficulties for their largest revenue stream seems to be easing and more momentum will commence. For 2023 so far Synaptics Incorporated ( SYNA ) has generated around 72% of the total revenues from the IoT market, one that is experiencing very strong growth and momentum right now, a trend which is expected to continue. In fact, between 2023 and 2030 the IoT market is predicted to generate a 26.1% CAGR.

As SYNA focuses on developing and marketing semiconductor product solutions they have built up a strong portfolio of offerings. ConnectSmart for example helps high-speed video/audio/data connectivity. We aren't far off until the next earnings report from SYNA, on August 3 2023 they are reporting their fourth quarter and full fiscal year 2023 results. I am optimistic about the performance and will be rating SYNA a buy right now.

Company Segments

Synaptics has since its founding back in 1986 built up a very broad and diverse set of products in its portfolio. But they continue to expand on this every so often to stay at the top of their game. Most recently they announced the expansion of their industry-leading MiS fingerprint authentication portfolio with the addition of a biometric security sensor.

{kind=link}

Serving many niche parts of the IoT market, SYNA has experienced steady revenue growth over the last 10 years, at a CAGR of 10.8%. Some of the notable products that SYNA has under its umbrella are ConnectSmart, DisplayLink, and VideoSmart. Besides that SYNA is also expanding into more smart solutions like fingerprint id and more efficient interaction solutions with devices. TouchPad for example senses the location and movement of one or more fingers on its surface.

Seeing as having a wide set of product offerings is what has gotten SYNA into its current position, ensuring they continue putting out new technology is key. Because of this the R&D expenses I think will remain the largest portion of the operating expenses. But it's the scalability of new products that will be a growth factor for the EPS at the end of the day. R&D Expenses/Revenue for 2022 was 0.21 and in 2019 it was 0.23. Not a major difference, but seeing margins trending higher and with the momentum the IoT industry is expected to have I think a sound prediction is that we will see revenues grow much quicker in the years ahead.

Massive Buyback Plan

The margins for SYNA are a highlight in my opinion when evaluating the company. The FCF margin is nearly 20% and I think a higher p/fcf 10 is fair. Given the sound growth they have had, without seeing any significant downturns as a result of the pandemic in 2020 a p/fcf of 15 should be applied. This leaves strong upside potential, leading to my current buy rating for SYNA.

But, the strong cash flows have also meant that SYNA is starting to aggressively buy back shares. In the last report, the company announced authorizing another $500 million to the share buyback plans previously committed. That $500 million could reduce the number of outstanding shares by around 13% given today's market cap. In total SYNA has accumulated a share buyback plan of $2.3 billion, right now there is $977 million still left available for usage. That would reduce the outstanding shares by over 25%. In my view, this is one of the strengths of going with SYNA. The priority of returning value to shareholders is very strong for the management. With a broader product portfolio, I think we might have an opportunity here that can, in the long run, yield larger returns than investing in a regular index fund.

Upcoming Report

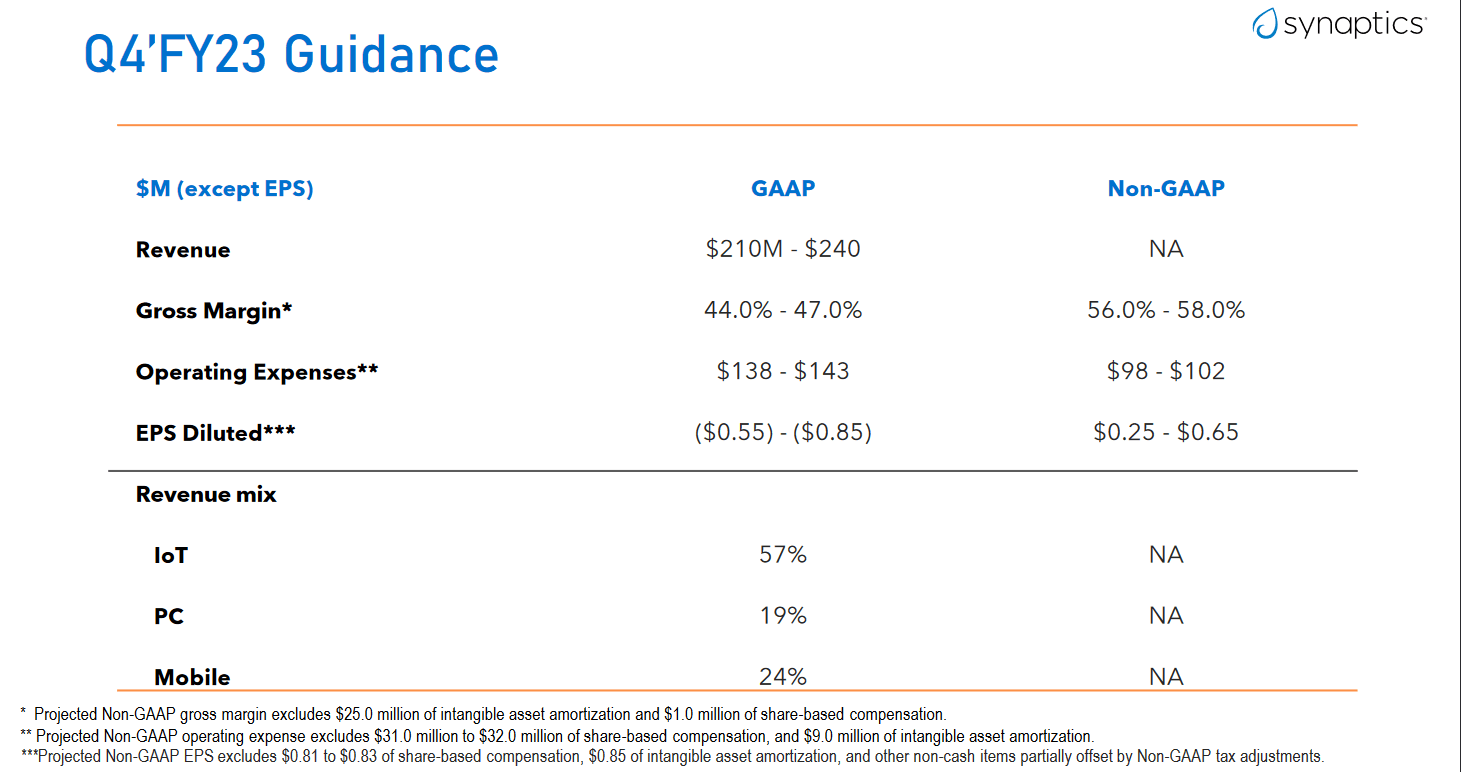

As I mentioned earlier, on August 3 SYNA is releasing its Q4 FY2023 report and the guidance they previously provided suggests that IoT is still going to make up a significant part of the revenues, around 57%.

{kind=link}

Revenues are to land at $210 - $240 million and the non-GAAP EPS is estimated to be between $0.25 and $0.65. That's quite a broad spectrum for them but I think given the announcement and momentum they are building on right now, I believe they can achieve the upper end of that guidance.

In the previous report, the company made some mentions of the inventory issues as they quite rapidly built them up but it didn't translate to stronger revenue growth per se. However, inventories are depleting and this should free up the position that SYNA is in right now. In the coming quarter seeing a lower inventory level would be comforting and a QoQ growth in revenues proof that the future still looks very bright for SYNA:

Risks

The impact of supply chain shortages has been significant, leading to a period of slower economic growth. This has prompted a substantial inventory correction that has not only affected the company's revenue and earnings growth but has also exceeded initial expectations. The challenges posed by disrupted supply chains have resulted in a more pronounced downturn in performance.

Furthermore, the slowdown in the economy has created additional headwinds for the company. As consumer demand weakened and market conditions shifted, the company faced increased pressure to adjust its operations and navigate the evolving landscape. This has required strategic decision-making and careful management of resources to mitigate the effects of the slower economy.

Final Words

The valuation right now for SYNA seems quite low given the market and industry they are operating in. Looking back at the revenues they don’t look that cyclical, but rather quite resilient and consistent. I still think there is much growth to be had for the company and with strategic product offerings they should be able to capture that as well.

The risks with inventory and slowdown in economic activity seem to weigh on the valuation and the p/e right now on a forward basis is just 11. I find a more reasonable valuation somewhere between 14 - 16. With EPS estimates for 2023 being $8.06 that leaves us with a price target of $120, far above the current price of around $90 per share. I am comfortable with the management team and I think inventory issues will deplete and we will return to a higher p/e multiple. Rating SYNA a buy.

For further details see:

Synaptics Incorporated: Battling Inventory Issues But Efficiently