SYNA - Synaptics Incorporated: Showing Why Its A Winner As Positive FCF Continues

2023-11-13 23:42:20 ET

Summary

- Synaptics Incorporated has seen its stock price increase while the S&P 500 declined, thanks to positive earnings and strong cash flows.

- SYNA offers investors exposure to the rapidly growing IoT market, with expectations of strong net income growth and a fair price for entry.

- The company has a diverse product portfolio and is focused on innovation, positioning itself for sustained success in the market.

Investment Rundown

Since my last coverage of Synaptics Incorporated ( SYNA ), the price has moved around 8 - 9% higher whilst the S&P 500 has declined by roughly 2%. This seems to have been largely due to the company's positive performance in the last earnings report as was very recently revealed. In the Q1 FY2024 report , SYNA continued to generate positive cash flows and efficiently managed the inventory levels. The outlook remains positive as margins continue to trend higher.

The IoT market is massive and one that is also growing very quickly. Right now I think that SYNA continues to offer investors with one of the better ways to gain exposure to this market. The company trades at a high FWD p/e of nearly 40, but given the rapid momentum the company is expected to experience that isn't a major concern. As inventory issues start to ease further I do expect SYNA to once again post strong YoY net income growth. Estimates suggest right now that in 2026 the EPS of the company will be $7.49, putting SYNA at an FWD p/e of 13. For a business that's operating in a market that is expected to grow over 26% annually up until 2030, I think that is a very fair price to get in at. Over the next decade, I see SYNA potentially yielding a very strong return as we will dive deeper into below. I was bullish a few months ago on the business and the recent earnings report has solidified that further as I continue to have the stock as a buy.

Company Segments

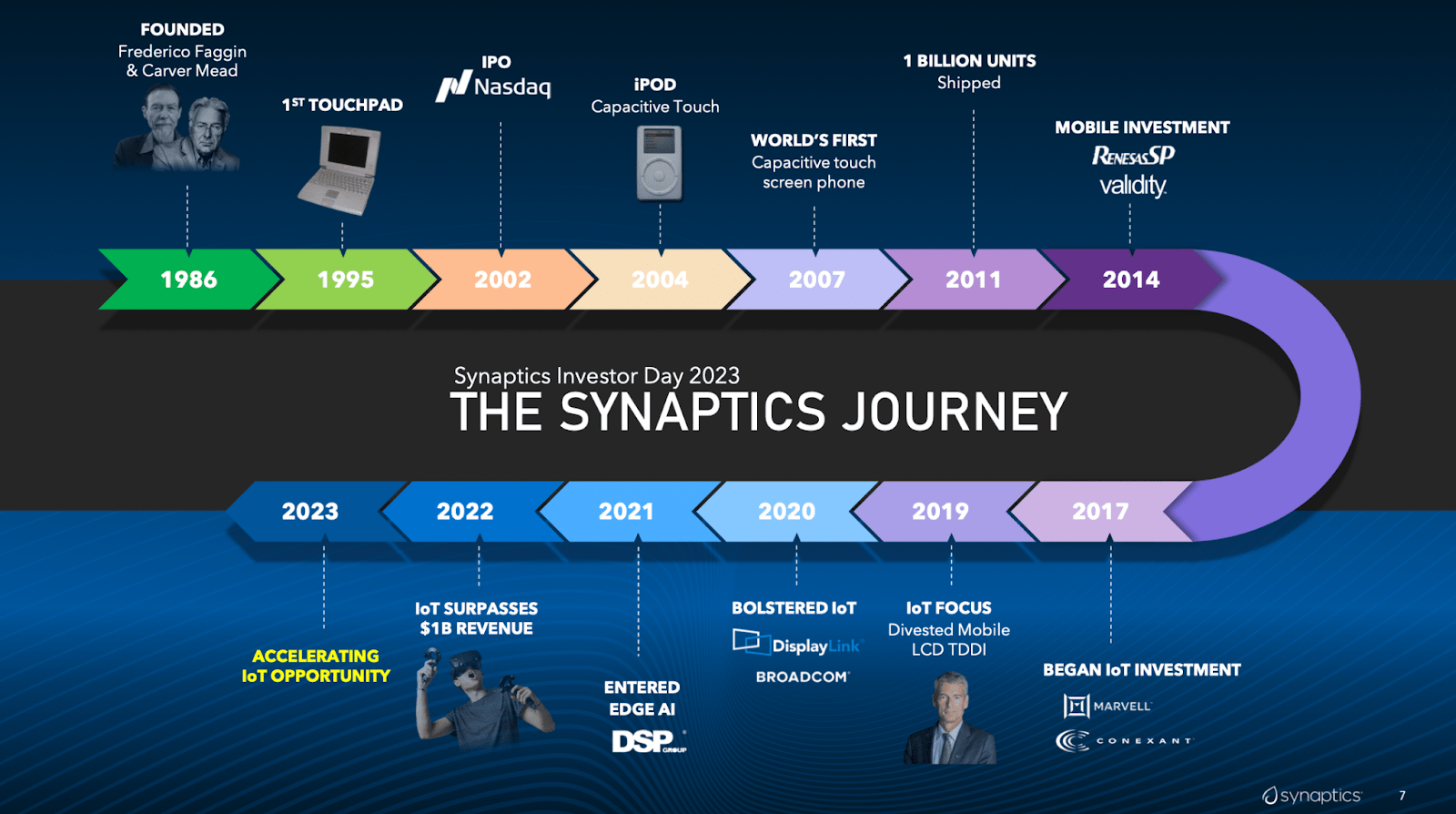

Since its establishment in 1986, SYNA has cultivated a comprehensive and diverse product portfolio. The company's commitment to innovation remains unwavering, as evidenced by its continuous efforts to expand and enhance its offerings. In its latest strategic move, SYNA proudly unveiled an extension to its industry-leading MiS fingerprint authentication portfolio - a noteworthy addition in the form of a cutting-edge biometric security sensor.

{kind=link}

SYNA has consistently demonstrated robust revenue growth, boasting an impressive CAGR of 10.8% over the past decade. The company has strategically positioned itself in various segments of the IoT market, catering to niche needs. Among its notable products are ConnectSmart, DisplayLink, and VideoSmart. SYNA's product portfolio extends beyond traditional offerings, venturing into cutting-edge solutions such as fingerprint identification and enhanced interaction capabilities with devices. The TouchPad, for instance, adeptly senses the location and movement of one or more fingers on its surface.

{kind=link}

With a keen focus on scalability, SYNA aims to drive EPS growth. Despite a modest difference in the R&D Expenses/Revenue ratio between 2022 (0.21) and 2019 (0.23), the upward trend in margins and the anticipated momentum in the IoT industry suggest accelerated revenue growth in the foreseeable future. As SYNA navigates the landscape of IoT , its emphasis on innovation positions the company for sustained success and prominence in the market.

{kind=link}

Looking at the TTM numbers for the R&D expenses and revenues we get 0.304 right now, an increase from previous levels indicating lower profitability. I have touted though that I think over the long term SYNA can raise the margins efficiently and get back to previous levels. The challenges of managing inventory levels have taken a toll on revenues as was visible in the last 4 quarters, and lower selling prices and volumes also caused the decline from the $1.7 billion record in 2022. I do think that SYNA can see at least 12 - 14% revenue growth in the next several years. By 2027 the revenues would be at $1.9 billion and as I think SYNA can efficiently scale during that time I think the R&D expenses would be around $380 million. That is a ratio to the revenues of 0.2, a return towards stronger margins .

Buybacks Are Still An Appealing Endeavour

The continued strong cash flows for the business have meant that the management has seen it fit to continue its spree of buying back shares, ultimately benefiting shareholders very much. Earlier this year the company announced that an additional $500 million the buyback program would be receiving, efficiently making the company capable of reducing total shares outstanding by over 13%. This sort of potential makes SYNA an appealing buy right now for investors in my opinion.

{kind=link}

As seen the tempo of buying back shares is increasing and I think this is a very bullish sign as the company sees the business as undervalued against where it might be in the future, meaning that once growth sets in, these price levels might not be seen again.

SYNA has amassed a $2.3 billion share buyback plan, with $977 million currently untapped. This initiative, if fully executed, would retire over 25% of outstanding shares. I consider this a notable strength of SYNA - an indication of robust shareholder value prioritization by management. The commitment to returning value to shareholders aligns with the company's broader product portfolio, presenting an enticing long-term prospect that could potentially outperform conventional index fund investments.

As for where I see the price of SYNA going, I have said before that I see strong 12 - 14 top-line growth annually until 2030 at least. By that point, the revenues would be over $2.8 billion, close to where the market cap is right now. But with growth like that, I think a p/s of around 3 is justified given that SYNA is a growth company. That puts a valuation of around $8.4 billion on the business. That is 119% higher than the current valuation or market cap and indicates a 17% CAGR between now and 2030. With a 10% discount rate, we get a CAGR of 15.3% which is still penalty enough for me to be rating the business a buy. When SYNA wouldn't be a buy is over $120 per share, at that point the long-term CAGR of an investment would be so low that you might be better off buying into an index fund instead and seeing similar results. Since SYNA is trading a fair bit below that right now though I will be continuing to rate the business a buy and a fantastic way to get exposure to the IoT market.

Risks

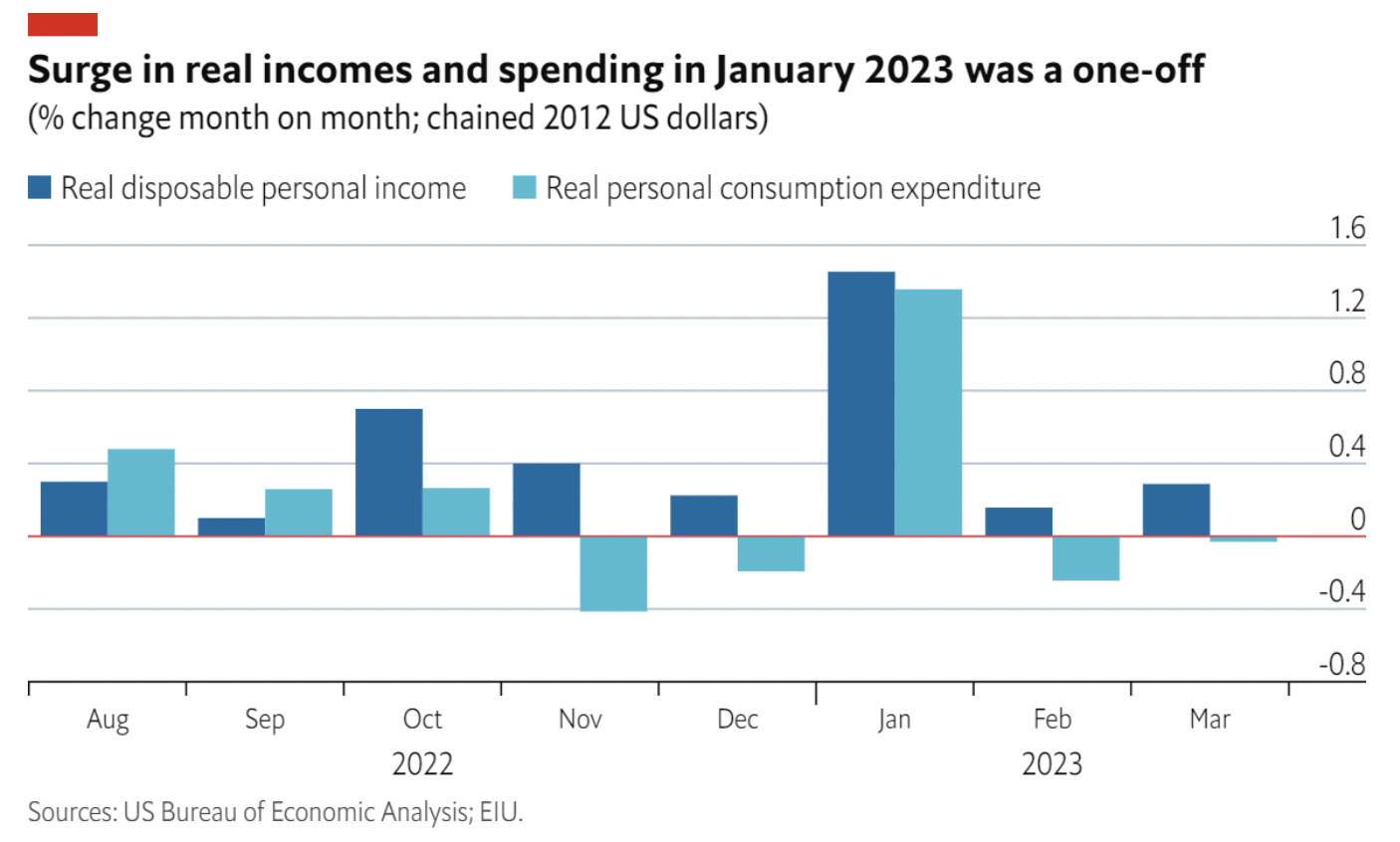

The repercussions of supply chain shortages have reverberated significantly, ushering in a phase of decelerated economic growth. This has instigated a substantial inventory correction, surpassing initial projections and casting a shadow on both revenue and earnings growth for the company. The disruptions in the supply chains have exacerbated the downturn in performance, presenting formidable challenges. As seen in the picture below, there was a surge in spending across the US but it seems to have been one and now consumption expenditures are trending lower again, indicating potentially a softer economic environment that could hurt the growth of SYNA, posing a risk to future results.

{kind=link}

In tandem with the supply chain disruptions, the broader economic slowdown has introduced additional challenges for the company. Weakened consumer demand and shifting market conditions have intensified the pressure on the company to recalibrate its operations amidst the evolving landscape. Navigating these challenges has necessitated strategic decision-making and prudent resource management to effectively counter the impacts of the sluggish economy. As the company adapts to these headwinds, the emphasis on careful navigation and proactive decision-making remains crucial to mitigate the effects of the economic deceleration.

Final Words

I have covered SYNA before as I said in the earlier parts of the article. I had the company as a buy then partly because of the massive opportunity for growth the IoT market presents, but also the fact the company has announced several buyback plans in recent quarters. FCF remained very strong and positive and this has driven the short price higher in the last few weeks I think. The guidance for Q2 FY2024 is that revenues will see flat growth QoQ, and margins will largely stay the same. I think however as the inventory issues and challenges clear up we will see a more rapid growth rate for both the top and bottom line, ultimately leading to my continued buy rating of the business.

For further details see:

Synaptics Incorporated: Showing Why Its A Winner As Positive FCF Continues