SYNA - Synaptics Interrupted IoT Wave Will Resume

Summary

- The company has made a terrific transformation now being an IoT company with a much higher TAM, higher growth and higher margins.

- That transformation is far advanced, so gross margins are topping but the larger TAM and higher secular growth remain.

- The company will shrink revenue in the coming quarters on a cyclical downturn, but management expects a recovery in H2/23.

- So one could be too early in buying the shares, we advise accumulating on dips.

Synaptics ( SYNA ) is well advanced in what can only be described as a very impressive transformation. Where it used to specialize in display drivers for PC and mobile handsets it now has a broad portfolio of leading tech solutions serving the IoT market:

{kind=link}

This transformation has:

- Greatly increased the TAM

- Accelerated revenue growth

- Improved gross margins to 60%+, which is really quite impressive for hardware.

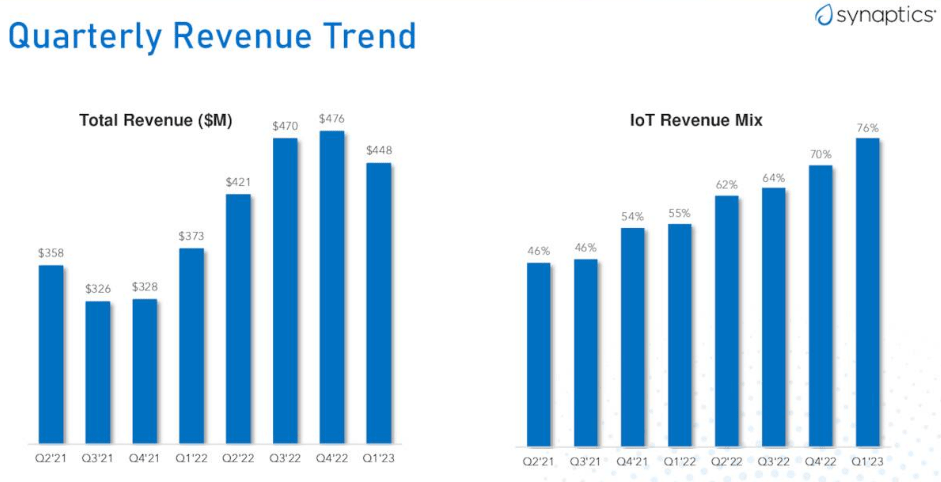

IoT revenue increased from 46% of revenue in Q2/21 to 76% in Q1/23, which is a huge change in a short space of time, just 8 quarters.

{kind=link}

Much of this was hidden from view as a result of the pandemic, but the last four to five quarters delivered excellent results and the share price responded setting a 52-week high of nearly $300.

FinViz

Q1/23 still delivered excellent results, but macro headwinds already appeared as revenue growth slowed:

There was still a y/y growth of 20% but sequential growth was -6% and in IoT growth slowed down to just 3% (while it was a whopping 67% y/y). This growth will likely turn negative in the current quarter to the tune of -19% (midpoint) for overall revenue and -18% for IoT.

This is due to consumer-facing segments like VR headsets where there is a sudden downturn in demand and inventories have been bloated by supply chain worries.

These inventories will have to be worked through and the company is in talks with its major customers to optimize this. Unless there is another bout of deterioration in the macro environment, management expects this inventory correction to play out by calendar H2/23 and growth to resume.

There are still products and segments that are strong and expected to remain strong, like automotive where the company has a string of design wins for its center info display with dollar content rising significantly.

Their recent acquisition Emza with its presence detection system will move from PC to automotive (and the smart home). There is also strength in docking stations (the soft PC market is more than compensated by higher attach rates), and video interface products.

The company has a very strong position in wireless with its WiFi 6 and 6E products and Bluetooth combination solutions with the likes of Amazon (AMZN) and Google (GOOGL) (GOOG) as customers.

Then there are newer products like networked displays, smart monitors, and conferencing systems, as well as wireless security products with new wins with Verisure, Vivint, and others.

There are cross-selling opportunities as well. Management sees PC demand stabilizing next year but is less optimistic about the mobile market apart from the new models that will launch in Q4. Mobile is now a segment in the single digits for the company so not that important anymore.

Finances

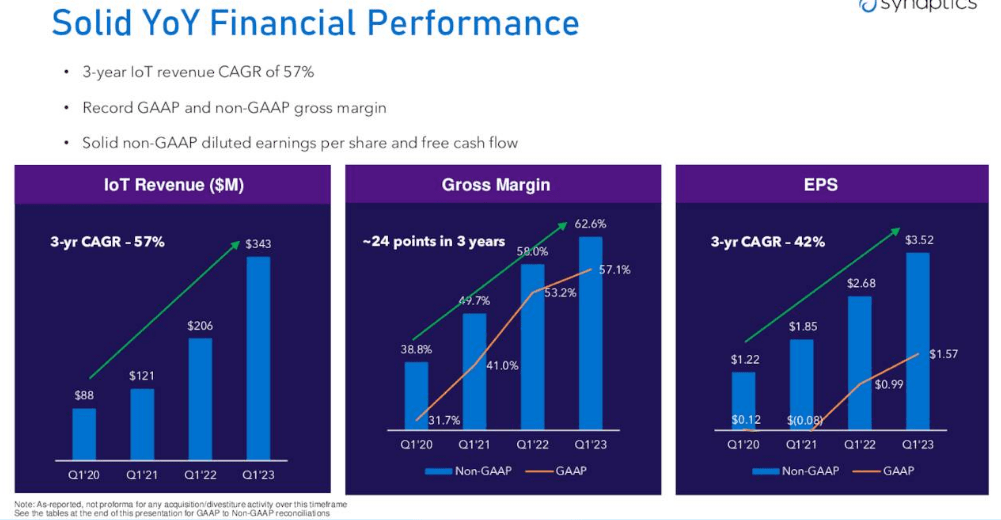

Some revenue data:

- Segment revenue IoT (76%), PC (15%), and Mobile (9%).

- IoT revenue + 67% y/y +3% q/q

- PC revenue -26% y/y and -20% q/q

- Mobile revenue -49% y/y and - 36% q/q

{kind=link}

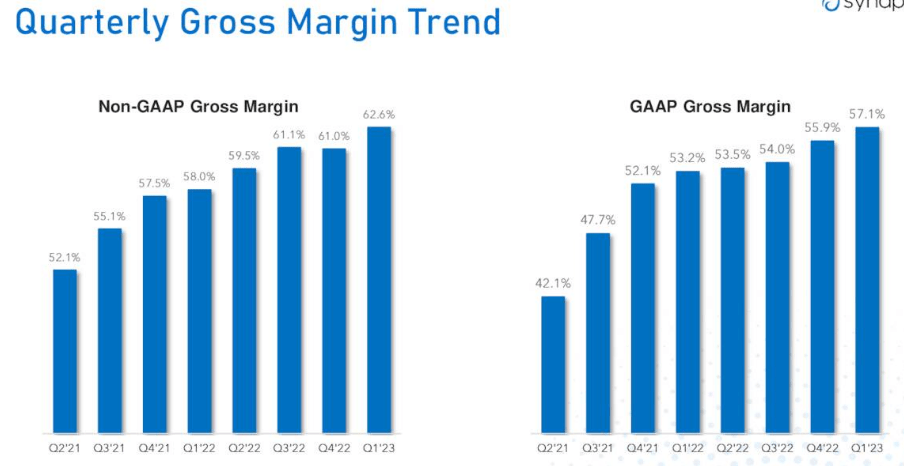

Margins

This is quite a picture:

{kind=link}

But we are probably at the top due to various factors:

- Favorable pricing played a considerable role in producing these high. margins (apart from an ongoing favorable shift in product mix).

- More difficult market circumstances will increase price competition and reduce pricing power.

- Revenues are likely to shrink considerably in the coming quarters (management predicts -19% for the current Q2/23 quarter) which inevitably leads to some diseconomies on fixed costs.

Management argues that the normal range for gross margins is high 50s, low 60s but they don't expect any dramatic decline, which is positive in itself. 100bp of the 62.6% record set in Q1/23 was also due to a one-time benefit.

There is still considerable operational leverage:

How much of that remains when revenues decline as they will in Q2 and probably a couple of additional quarters remains to be seen. The graph below is of course a beauty:

In just two years, the company managed to triple its cash flow. We probably get some downdraft on that in the coming quarters but nearly $500M of operational cash flow TTM for a company selling $1.8B of hardware TTM is very impressive. What did they do with all that cash?

- CapEx ($6.2M in Q1/23)

- They paid down debt (just $900K in Q1/23 with $974.8M left)

- They buy back shares (120K shares for $13M with $564M still available)

- The acquisition of Emza (terms not disclosed).

There is $907.8M of cash and equivalents left so the net debt is just $67M.

There are 40.5M shares fully diluted.

Risk

- Soft consumer markets persist longer and deeper

- Pricing pressure

These risks are actually one risk as the second would be a likely consequence of the first.

Valuation

With 39.8M shares and 0.9M options, there are 40.7M shares outstanding fully diluted which gives a market cap of $4.47B ($110 per share) and an EV of $5.14B for an EV/S of just under 3.4x.

FY23 EPS is estimated to be $9.94, which gives the shares a P/E ratio in the single digits (only just though). FY23 ends in June 2023, and FY24 EPS is estimated at $10.34, if management is right that H2 calendar 2023 will produce a recovery we think there is an upside to that.

In any case, the shares are already cheap.

Conclusion

There are many things to like:

- The tremendous transformation towards IoT which has accelerated growth, increased TAM and margins still has legs simply because IoT is growing much faster than the mature PC and mobile markets.

- The margin expansion and cash generation are especially impressive, although the gross margin isn't likely to expand much further, if any.

- The company has a solid balance sheet and generates substantial amounts of cash with which it buys back shares and reduces debt.

- The present cyclical downturn offers a very good opportunity to get on board, as growth will resume at some point (H2/23 according to management).

- The shares are really quite cheap already.

- The risk is a further downside in the coming quarters if economic circumstances deteriorate, which could also increase pricing pressures.

For further details see:

Synaptics Interrupted IoT Wave Will Resume