SYNH - Syneos: Further Contraction Imminent In FY2023 Reiterate Hold

Summary

- Flat Q4 and full-year top-line growth, offset by reasonable upsides in the commercial solutions segment.

- The company hasn't delivered a return on invested capital above the WACC hurdle, limiting value creation for shareholders.

- Guidance points to further contraction in earnings.

- Net-net, reiterate hold.

Investment Summary

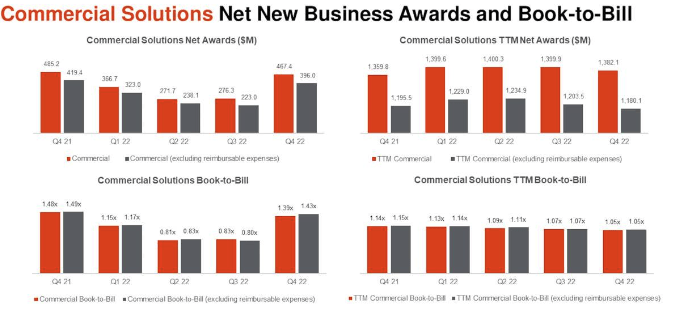

Syneos Health, Inc ( SYNH ) posted its Q4 and FY22 numbers last week with upsides versus consensus at the top and bottom lines. In November last year we released our last SYNH publication titled "Nothing's changed after Q3 earnings" it was clear the stock had broken its pre-pandemic lows and price action subsequent to its Q4 FY22 results has been flat, suggesting investors were expecting more from the company in its final quarter. It landed at a book:bill ratio of ~0.4x at the end of the year, however the commercial segment recognized a 1.43x book:bill ratio after the division recorded its "second highest quarter of net awards in [SYNH's] history" to use CEO Michelle Keefe's language from the earnings call . Valuations look reasonably priced on face value, however, after a sluggish period of growth, the firm guides to a 7% further pullback in top-line growth in FY23, leading us to believe the low multiples may be justified. Here I'll run through the major moving parts in the SYNH investment debate for the benefit of investor reasoning. On the culmination of these points raised in this deep dive, we reiterate SYNH stock as a hold.

Fig. (1)

{kind=link}

Data: SYNH Investor Presentation

SYNH Q4 analytics

Looking to the reported numbers, the company clipped total revenue of $1.36Bn , representing a 100bps YoY decrease on a reported basis. Moving down the P&L, quarterly adj. EBITDA also contracted by 11.8% YoY to ~$209mm, a margin of 15.4% that compressed 190 basis points YoY. Looking at this in greater detail, the tighter margin chiefly resulted from less favourable revenue mix, discussed below. Noteworthy, reimbursable expenses were higher than expected in Q4, due to the ramping of 2 expense-heavy projects, one each in the in the clinical and commercial segments respectively. We'd note that SYNH expects the burden of these projects to continue into H2. It pulled this down to quarterly adj. EPS of $1.23, a 16.9% YoY decline. Contrasting this to the its FY22 adj. earnings, it clipped a 580bps YoY gain to $4.72.

Turning to the operational highlights, important takeaways for investors are as follows:

- Quarterly top-line growth for the clinical solutions segment compressed by ~210bps YoY to $1.02Bn, and contributed ~75% to the top-line. This reflects the less favourable sales mixed outlined above. The downsides were underscored by lower net awards and backlog conversion delays. Looking at the total backlog, it totalled $10.13Bn at the end of FY22, down from $11.4Bn, meaning it worked through ~$1.27Bn in revenue conversion from the backlog over the year. Further, its clinical solutions segment was partially supported by an 80bps tailwind from the higher reimbursable expenses mentioned earlier. Expanding the analysis to the full-year, clinical revenues came in flat to $4Bn, on operating income of $689.5mm, or 12.8% of total sales..

- Meanwhile, the commercial solutions segment clipped revenue of $336.6mm in Q4, a 250bps YoY. Growth was underlined by a strong contribution from the company's Syneos One portfolio; however, the segment also realized a strong 450bps tailwind from reimbursable expenditures. Backing out this tailwind, the commercial franchise grew by just ~50bps. Moreover, only 25% of the top-line is attributed to this segment, and it booked $1.32Bn in revenues for the entirety of FY22. Moving down the P&L, this came to commercial solutions operating income of $159mm, a 2.9% operating margin.

- The company finished the year with $427mm in CFFO amounting to a $5.5mm gain in cash after a $2Bn debt repayment, issuing $1.8Bn in additional notes payable, and $93.5mm in CapEx. This pulled to $343mm in FCF to the firm. It also repurchased $180mm in stock throughout the year. Looking at its credit summary, short-term obligations are covered >1.1x from liquid assets, interest payment is covered 8.5x from pre-tax earnings and equity holders have a good claim in the capital structure, with a debt ratio of just 21%. Notably, however, is that ~61% of the company's asset base is comprised of goodwill, meaning it has a negative tangible book value of $2Bn, or negative $20.24 TBV per share. Further, an additional 21% of the firm's assets are made from receivables, and just 5% as tangible assets. Hence, the ROA of 3.25% is even less attractive as a chunk of this is a return on goodwill, the premium paid above fair value for the cost of its acquisitions.

Fig. (2)

Data: Author, adapted from SYNH FY22 10-K

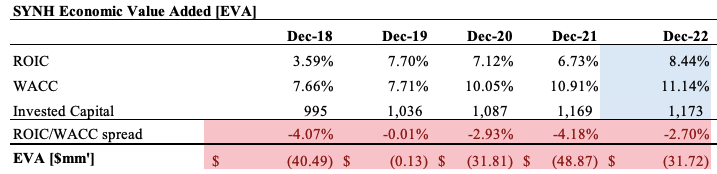

Moreover, even though SYNH is profitable, taking a longer-term view, we extrapolate further critical insights from its performance over the 5-years to date. I'd remind readers that a firm creates future value for its shareholders with a multi-pronged strategy involving growth and return on capital. We can immediately assess the firm's success of this by examining 1) high return on invested capital that exceeds the cost of capita l; 2) growth in post-tax earnings; 3) what percentage of earnings it reinvests for future growth; and 4) what percentage of earnings is leftover as residual cash flows distributable to equity holders, after the reinvestment for future growth. Key to the entire continuum, is that the ROIC exceeds the cost of capital [otherwise known as an economic profit]. If it doesn't, then growth destroys value, per Mauboussin (2020) . This is an essential component to grasp because it help us tie together the concept of valuation from an investors perspective, helping provide a better understanding of the cash flows to be received into the future. Alas, not all growth is created equally, and growth comes at a cost to shareholders – so we need to understand what this cost is, and if future growth is going to actually accretive to value for SYNH. Doing so, we can make detailed inferences about its future value, and what kind of growth profile we can expect to see over a long-term horizon. Looking to Figure 3, we see that SYNH has been profitable over the 5-years to date, with annual ROIC lifting from 3.6% to 8.4%. It's grown NOPAT by $323mm by investing an additional $595mm in capital for future growth, a 54% cumulative 5-year return on investment. With the $2Bn in cumulative NOPAT generated, it has reinvested ~30% of this to achieve that return. Subsequently, the growth rate is recorded at 15.8% over this time. These are reasonable growth percentages.

Fig. (3)

{kind=link}

Data: Author, using data from SYNH SEC Filings

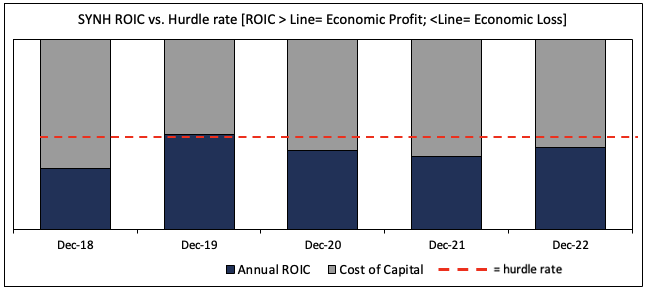

There's more to it than this, however. SYNH's annual ROIC hasn't beaten the annual cost of capital from FY18–22', as seen in Figure and Figure 5. Consequently, from an investors perspective, the company's growth rate hasn't been accretive to value [as outlined earlier when the ROIC<hurdle rate]. Why is this of importance to the investment debate for SYNH? To quote Mauboussin (2020) directly,

"the fundamental principle is that growth only adds value when the company earns a return on its investment that is above its cost of capital. The higher the return, the more sensitive the business is to growth. Growth is of no economic significance if a company’s returns are equivalent to the firm’s cost of capital. As a consequence, companies should focus not on growth per se but on value-creating growth"

Subsequently, this creates a valuable tool for us to evaluate SYNH by in terms of valuation and what it needs to do looking ahead in order to drive value-creating growth for shareholders. We need to see the company generating a higher return on its investments for one, and see it exceed the WACC hurdle in order to see the stock trade a higher multiple, by estimation. This is quintessential, and, if it can't invest at return that exceeds its WACC hurdle, then we estimate that investors will continue to shun the stock for more selective opportunities that do offer this kind of profile. We will benchmark SYNH against these numbers moving into the future.

Fig. (4)

{kind=link}

Data: Author, using data from SYNH SEC Filings

Fig. (5)

{kind=link}

Data: Author, using data from SYNH SEC Filings

Forward guidance points to further contraction

Moving on to the 2023 guidance, SYNH expects another pullback in a turnover to a range of $4.98Bn–$5.18Bn, calling for a decline of 4–7.8%. It bakes in a FX headwind of $10mm on this. Curiously, it also incorporates a projected headwind of 100bps from reimbursable expenses. It also projects adj. EBITDA to $725mm at the upper end of range, calling for a margin of 14% – another 100bps FY22. It hopes to pull this down to non-GAAP EPS between $3.26–$3.53, a c.31% decrease at the upper bound. Looking to the near-term, the company expects Q1 revenue of ~$1.31Bn on adj. EBITDA of $148mm at the upper end. Again, looking at Q1 FY11, this calls for a revenue decline of 2–5.7% to 2% and adj. EBITDA pullback of 15–21.7%. The wind-back in earnings supports additional findings on the company's profitability and economic profit discussed above. The problem being, that for investors, this means a lower claim on free cash flows and potential restrictions to valuation upside, again supportive of a neutral view.

Valuation and conclusion

On face value the stock trading at a discount to peers at 7.8x trailing non-GAAP earnings is attractive, however we'd point out that this is also a 57% discount to SYNH's 5-year average. Importantly, SYNH isn't the same company it was 5-years ago, and we have discussed earlier the impacts of its ROIC not beating the hurdle rate, and how this has potentially eroded shareholder value. Alas, the 58% discount to the industry P/E may be justified. Further, it trades at 1.08x book value, but the bulk of its book value of equity is comprised of goodwill, as mentioned. Looking at forward multiples, we think the 7.8x multiple is justified, as mentioned, and assigning this to the firm's call for $3.53 in EPS derives a price target of $27. This is supportive of a hold rating on SYNH.

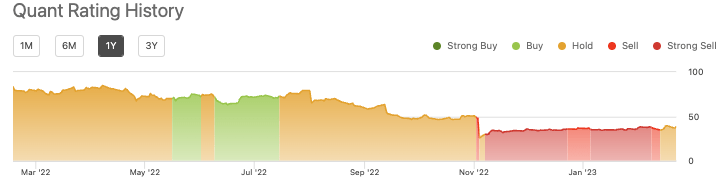

In short, SYNH has faced headwinds to creating value to shareholders, based on the blend of flat sales growth, ROIC that hasn't beaten the cost of capital, and contracted forward guidance for FY23. Each of these factors are supportive of a neutral viewpoint. In that vein, we rate the stock a hold, and look forward to seeing SYNH generate a higher rate of return on its investments, and drive free cash flows higher into the future. The hold rating is also supported by the quant rating system , adding further weight to this call.

Fig. (6)

{kind=link}

Data: Seeking Alpha, SYNH, see: "ratings"

For further details see:

Syneos: Further Contraction Imminent In FY2023, Reiterate Hold