IQV - Syneos Health: Rumors Of Private Equity Circling Potential 40% Upside

2023-04-12 17:19:34 ET

Summary

- Dealreporter article says that multiple PE firms are bidding for the company and even named advisors the company has hired.

- Private equity math works given relatively low current leverage and high cash generation.

- Even though the stock is decently off the lows, it's still about 60% off its high and probably 40% below its take-out price.

- High quality business as a standalone and likely recovers further even without a buyout.

- Announcing my new Investment Group launch, Catalyst Hedge Investing, coming April 27th!

Reported private equity interest in Syneos Health

On Monday (April 10th), Dealreporter put out an article that at least four parties are in the second round of a sale process initiated by Syneos Health ( SYNH ) in February. SA Editor Josh Fineman did a great job summarizing the situation on Monday .

I had looked at Syneos casually in the past. The business is extremely high quality. It is a CRO (clinical research organization). They provide outsourced services to pharma companies taking drugs through clinical trials. It also provides commercial consulting services (marketing, product launch, advertising etc). Clinical is about 3x the size of commercial construction in terms of revenue and both are about the same mid-teens EBITDA margin.

{kind=link}

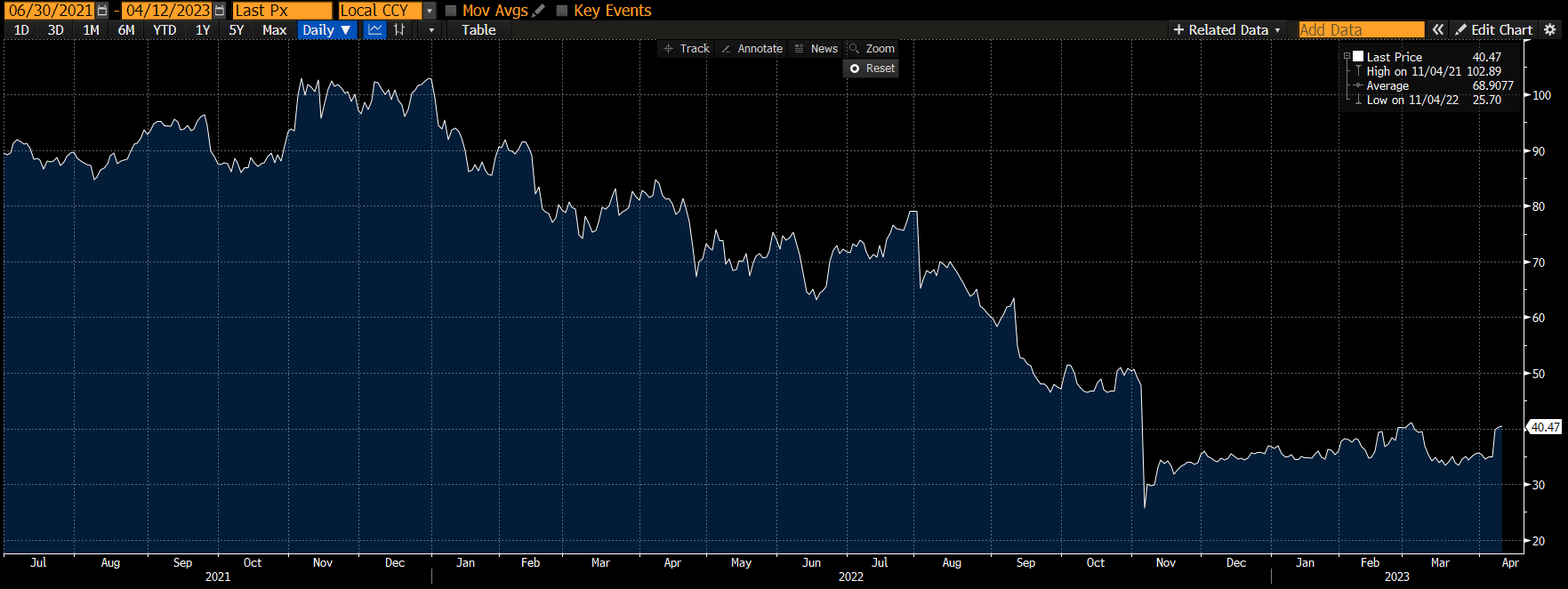

I never got involved in SYNH previously due to valuation. I'm just not the kind of investor that buys things at 20x EBITDA unless it's a really unusual situation. Like many growth stories, this stock started breaking down in the beginning of 2022.

{kind=link}

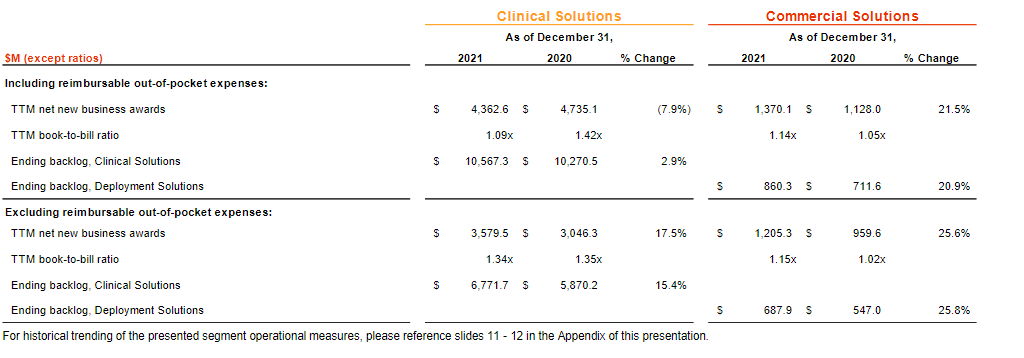

This is a contracted business, so the street focuses on book-to-bill ratios. Traditionally, book-to-bill for both clinical and commercial have been over 1.0, meaning good flow of new business and a growing backlog. The company historically ran well above book-to-bill of 1.0 in both businesses.

{kind=link}

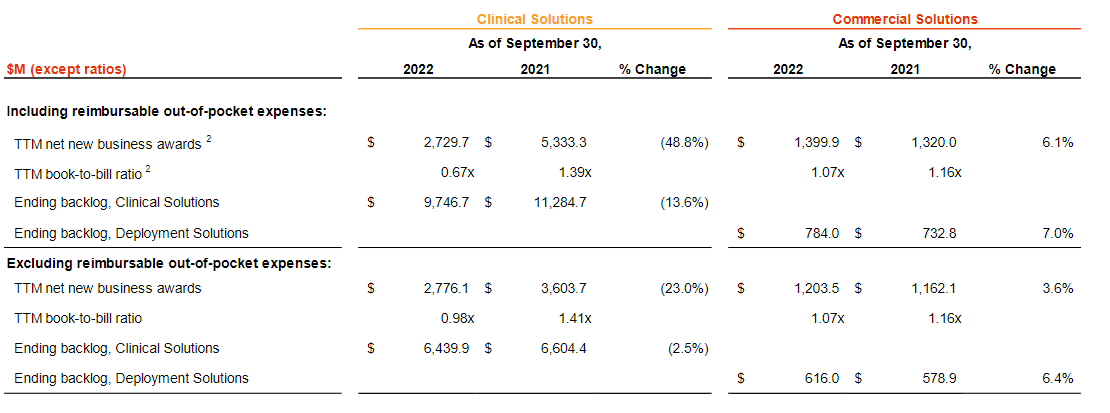

The wheels came off in Q3, particularly in the clinical business which experienced a 0.30 book-to-bill that quarter. That reduced the ratio to well below 1.0 for clinical as of September 30.

{kind=link}

The company tried explaining the miss with:

Our core issues with clinical net new business and revenue growth are primarily with small to mid-sized biotech customers, where we historically maintained a leading position, while demand from these customers has been impacted by the macroeconomic factors, we now believe that these headwinds are more specific to Syneos Health. We believe that as we've grown in recent years, our clinical operating model had begun to lose its traditional strengths of agility, and leadership engagement that was critical to these post revenue SMID customers which began to negatively impact our opportunities for repeat business.

I think the company's CFO was also partly to blame as book-to-bill is a bit more art than science. It appears he simply overestimated orders. This Q3 news cut the stock in half from $50 to the low of $25.70 in one day in November. The company redeemed itself by 1) firing the CFO 2) guiding earnings that showed continued weak revenue growth for 2023, but far from catastrophic declines and more importantly, EBITDA down only about $100mm from 2022, which is about 12%, and adjusted earnings of $3.26-$3.53. The company generated about $450 million of free cash on 2022's $800 million of EBITDA. Tax-affected, I'd expect $100 million less EBITDA translates to about $375 million of free cash.

Syneos valuation

It does not surprise me that the stock drop attracted private equity. Long term I think this company will correct the contract wins and resume growth. This company offers a lot of things private equity seeks: good core growth, no controlling shareholder, low capital intensity, cash generation and leverage capacity. Even after the stock bounced after the Dealreporter article, it's still trading at less than 9x this year's lower EBITDA.

| Market Cap @$40.50 |

| $4.188 billion |

| Cash |

| $112 million |

| Debt |

| $2.899 billion |

| Enterprise Value |

| $$6.975 billion |

| EV/'23 EBITDA (Using $700) |

| 9.96x |

| Leverage |

| 4x |

| Free cash flow yield (using $375 million) |

| 8.9% |

Healthcare LBO's are often completed at 12x EBITDA or higher with an even split between debt and equity. 12x-14x is where comps like Charles River Labs ( CRL ) and IQVIA ( IQV ) are trading. Just using this year's depressed EBITDA and a 12x multiple implies an incremental $1.4 billion of potential value to shareholders in a buyout. That would be a 33% increase on the stock. Using 12x and normalized $800 EBITDA, would be $1.6 billion or close to 40% higher on the stock, implying a valuation around $55/share.

Carve outs

The company's 2029 bonds have a poison put in the event of a change of control where they are puttable at 101. There is a specific carve out for Advent and Thomas H. Lee, where a buyout by them wouldn't trigger the poison put. The carve outs exists as both firms owned predecessor businesses to SYNH. Both firms were listed as potential bidders this time around by Dealreporter. Not having to buyback the bonds, gives Advent and TH Lee a $600 million financing advantage over other bidders.

Risk

I am a bit surprised that the company is conducting an auction process after the multiple has contracted and the stock has fallen so much. Even a $55 price is a far cry below where the stock was trading at the beginning of last year. Should the board reject bids and performance deteriorate, the stock could drop again. Considering the process has moved from first to second round bids, the board was likely satisfied with initial price ranges. That does not mean a transaction will happen, however. There are a million and one reasons why public company buyouts don't happen.

Conclusion

I like the SYNH business on a standalone. I like the stock at this lower valuation even if a buyout doesn't happen as I think growth can come back and the company can buyback a lot of stock down here in the meantime. It becomes a quick home run if a buyout happens. If you can tolerate some temporary downside if a deal doesn't materialize, I think you can win in almost any situation.

Launching Catalyst Hedge Investing

My new investment group, Catalyst Hedge Investing , is launching on April 27. That's only two weeks away. Please mark your calendars or PM me so you can reserve your spot as a Legacy Discount Member. There will be generous introductory prices for early subscribers that will continue for the life of your subscription. Keep reading my articles for more details, and thank you for following my work.

For further details see:

Syneos Health: Rumors Of Private Equity Circling, Potential 40% Upside