ROP - Synopsys: Robust Semi Exposure To Deal Calmly With Recession Fears

2023-04-29 03:53:04 ET

Summary

- Synopsys is a leading EDA and IP designer.

- The firm is supported by strong tailwinds such as China's rising Chip Industry, EV and AI-driven solutions adoption.

- Rock solid fundamentals makes it a very attractive play should we enter into recession.

During the gold rush it's a good time to be in the pick and shovel business - Mark Twain

Introduction

It's been now more than a year that investors are fearing a potential recession.

Within this environment where macro indicators have been and remain contradictory, it has been very hard to follow where the market would and will go.

Thus, many reallocated their portfolios in a hurry and this more than once. In 2022, investors mainly focused on energy, health care, and utility stocks due to a context of strong inflation and war in Ukraine. Because of these two main factors, macro-economists and analysts were expecting an economic recession striking whether natively or due to a FED interest rate overshooting.

For now, the recession doesn't seem to be here but the sentiment remains very mitigated. This situation is very frustrating for investors who don't want to stay away from growth. This is my case and it might also be yours. There are many interesting hot topics out there but we might not want to take position due to this fear of under or overestimating this potential recession risk.

Thus, in such a complex environment, I tend to favor highly qualitative players belonging to very promising industries supported by secular growth opportunities.

Being particularly bullish on the long-term horizon regarding the semiconductor industry, I believe that one of the best ways to play this sector is by focusing on top-tier "pick and shovels" providers, such as Synopsys ( SNPS ), a leader in the Electronic Design Automation ((EDA)) segment.

Let's now dive into why I believe SNPS stock represents an interesting qualitative play to get direct software exposure to the semiconductors industry without being too much dependent on semis cycles.

Synopsis presentation

Founded in 1986 and headquartered in Mountain View, California, SNPS is a leading Electronic Design Automation ((EDA)) company that provides software and intellectual property ((IP)) for the design and verification of complex integrated circuits ((ICS)) and electronic systems.

EDA is an essential element of the electronics and semiconductor industry. Indeed, EDA is used by designers to create and verify complex chips and systems with speed, accuracy, and efficiency.

This kind of software is used by many companies in various industries such as automotive, aerospace, defense, consumer electronics... Through their use, designers can simulate, synthesize, verify, and test IC designs so they can ensure the product they are focusing on is working before being fabricated on a large scale. Once knowing that, you can understand how SNPS mission is critical. And for good reasons, the cost of a design error can be very high, both in terms of time and money.

SNPS provides a wide range of EDA solutions that address various stages of the design and verification process, including digital and mixed-signal simulation, logic synthesis, physical design, and verification. They also offer IP solutions for various types of ICs, including microprocessors, memory, and interfaces. In addition to software and IP solutions, SNPS also offers training, consulting, and support services.

The firm has a strong reputation and is known for its ability to provide end-to-end solutions that help its customers achieve faster time-to-market and improve productivity while reducing design costs.

Serving customers worldwide, in more than 25 countries, SNPS has a very strong reputation thanks to the quality of its products and its capacity to innovate and disrupt the industry.

{kind=link}

A Play Poised to Capitalize on Semiconductor Secular Growth, China's rising Chip Industry, and AI-driven Solutions

The semiconductor market is a giant half-trillion-dollar market. This market is expected to grow consistently during the upcoming years.

Indeed, according to a report from DIGITIMES Research , the global semiconductor market is expected to exceed US$1 trillion in 2030, with a CAGR of 7%. The report highlights that the semiconductor industry has been growing rapidly and is expected to continue this growth due to the increasing demand for semiconductors in various applications, especially in automotive, industrial, and electronics.

As more OEMs are developing their EV offer increasing the need for chip-making tools I expect SNPS to thrive. I also expect the demand for EDA solutions to continue to be driven by the growing complexity of integrated circuits and electronic systems.

China could also become a key opportunity to seize for the firm. Indeed, during the last few years, the US has been taking more and more sanctions against China, especially regarding the semiconductor industry.

This has forced China to act. This phenomenon has been recently highlighted by Huawei's rotating chairman Eric Xu in an interview given to CNBC . He mentioned that China's semiconductor industry is expected to flourish again despite US sanctions that have crippled the country's ability to manufacture high-tech chips.

Xu stated that the sanctions had actually spurred China to focus on developing its own capabilities in the chip industry and that the country had made significant progress in areas such as design, materials, and equipment. He also highlighted that China had increased its investment in research and development to accelerate its progress.

Finally, SNPS seems to be capitalizing on the current AI trend to stay ahead of the curve. According to this article from Seeking Alpha :

At its annual Synopsys Users Group ((SNUG)) Silicon Valley Conference, Synopsys, Inc. today launched Synopsys.ai, a suite of AI-driven solutions for the design, verification, testing, and manufacturing of the most advanced digital and analog chips. For the first time, engineers can now use AI at every stage of chip design, from system architecture to design and manufacturing, and access the solutions in the cloud.

In my view, this confirms the firm's capacity to innovate in an environment characterized by clients that are more and more demanding with very technical and specialized needs.

Qualitative Positioning Supported by Rock solid Fundamentals

SNPS is characterized by several elements that make it a quality stock of choice:

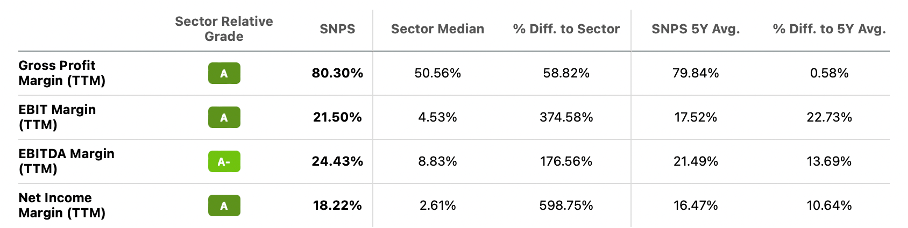

- The group has a leading position in the oligopolistic EDA market (50% of market share). Its global presence and the quality of its products have built a strong reputation among its customers and also among its peers. The quality of SNPS products answering to a very strong demand allows the group to have among the best margins of the sectors whether on the top-line or the bottom-line side.

Also, when looking at last data, it is encouraging to notice that margins are all above the 5Y average showing improvements in the firm profitability.

{kind=link}

- When talking about profitability, I love to have a look at Free Cash Flows and especially at Free Cash Flow yields. First, the Free Cash Flow metric is essential as it gives us insight into firm profitability and financial flexibility. Indeed, seeking quality, we have to focus on firms with strong FCF generation assessing the sustainability of firm dividends, and buybacks policies but also potential expansion and growth strategy. Going back to FCF Yield, it represents the amount of Free Cash Flow generated by a company relative to its market capitalization or enterprise value. This ratio is essential as it provides insights into a company's valuation, financial strength, quality of earnings, and risk profile. SNPS currently has an FCF Yield of 2.89% which is way above all its peers.

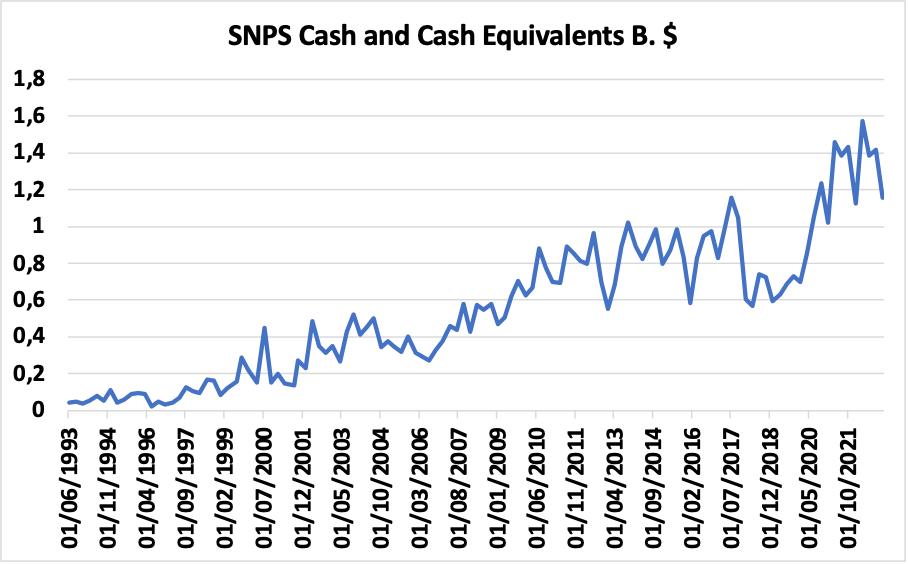

- Regarding debt, the firm has almost none which is a key point to consider in my view. This robust balance sheet is characterized notably by an interest coverage ratio of 685 meaning the EBIT covers 685 times the firm interest payments. The firm also has a negative debt of $ 909 m. meaning it has more cash and cash equivalents than its financial obligations.

Cash is King

As mentioned previously, SNPS has an important amount of cash and close to no debt. This element is appreciable, especially in the current context. It means it has flexibility in terms of capital allocation. Thus, many choices are offered:

The firm has the flexibility to make strategic investments, acquisitions, or share repurchases. High-interest rates prohibit the use debt. In this sense, having ample cash on hand can allow the firm to take advantage of opportunities without having to take on debt. Finally, if none of these opportunities seems suitable, it can save, lend or invest its cash on the money market where it will earn for example 3.8% over a 3-year horizon. Not bad, isn't it?

{kind=link}

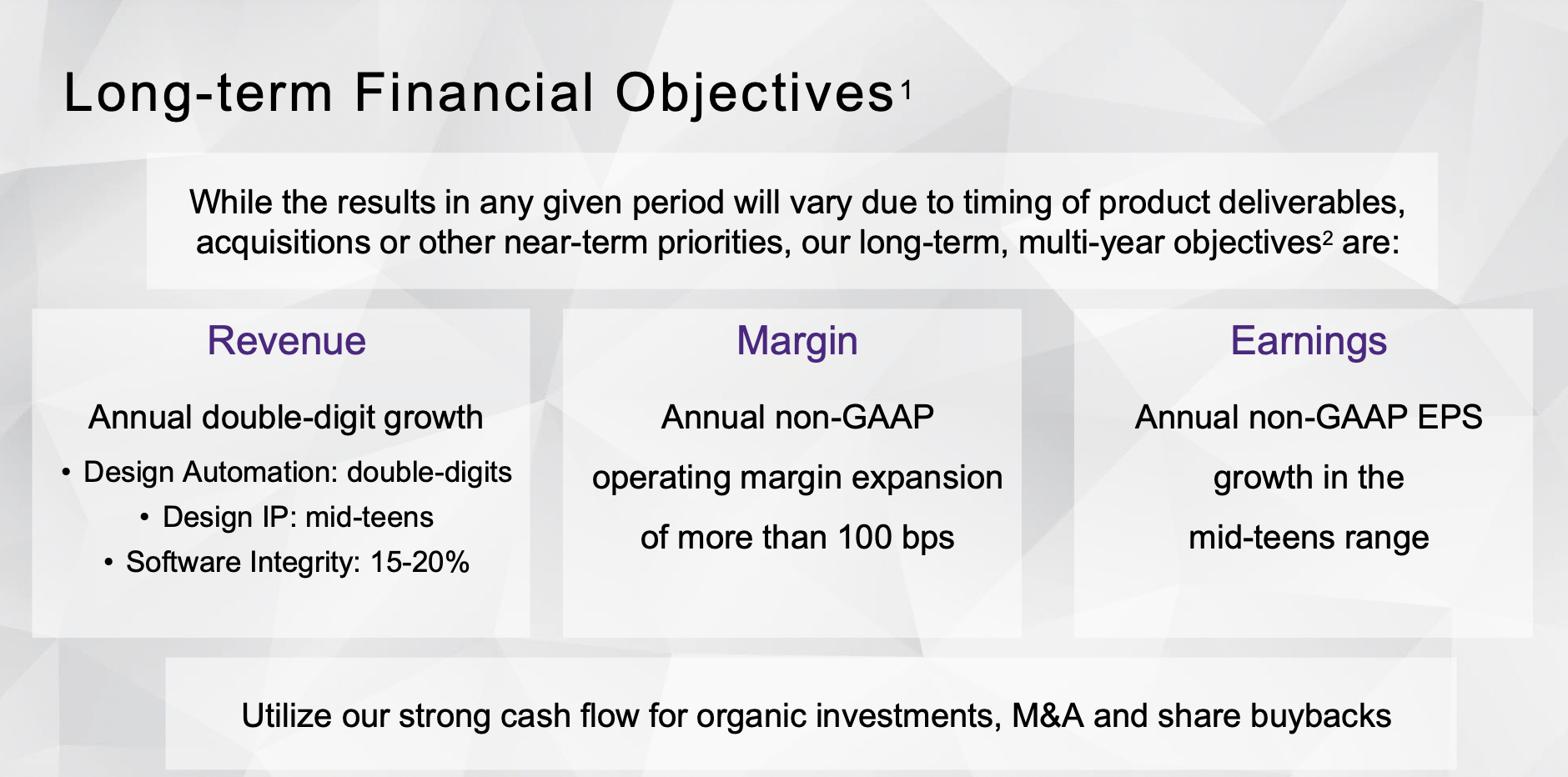

Note that the management seems to consider all 3 options very carefully as shown in the firm's February overview :

{kind=link}

A high recurring revenue profile

SNPS has a high recurring revenue profile (Close to 80% of next Quarter's revenues are coming from backlogs). This kind of actor is thus known to be more resilient in case of a recession.

A high recurring revenue profile generally implies a higher retention rate which makes sense in the EDA and IP solutions segments where there are few actors operating and where clients don't want to change frequently the software they use.

With such a profile, the stock can be considered as a bond proxy with the vast majority of its cash flows are predictable. However, this makes SNPS stock valuation more sensitive to interest rates.

In my view, as the biggest part of the FED hiking process has been done, this should put less pressure on SNPS valuation which is also an interesting point to consider.

Let's now have a deeper look at SNPS and its peers' fundamentals to compute our valuation.

Ratios and Valuation

{kind=link}

{kind=link}

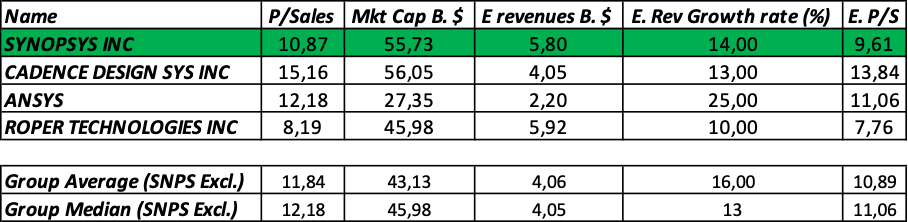

The peers I choose are SNPS direct competitors all operate in the EDA or IP segments. Their names are Cadence Design ( CDNS ), Ansys ( ANSS ) and Roper Technologies ( ROP ).

When looking at Debt, SNPS stands out with the best ratios whether regarding FCF/Debt, Debt to Assets, and Debt to Equity highlighting the strong credit profile of the firm.

Profitability is in line with peers average. However, management is focusing more and more on IP solutions as an opportunity to improve both the firm growth and margins.

SNPS PE might appear a bit expensive but it is in my view justified by higher EPS growth expectation and focus on IP solutions for the upcoming years which should drive margins up.

Looking at price to Sales, SNPS trade at a slight discount (10%) compared to its peers which in my view is not justified. Taking into account consensus revenues growth expectations (14% for next year) and expecting SNPS to close the valuation gap with its peers a 15% upside seems reasonable to me for the upcoming year leading us to a $ 423 TP.

Risks

SNPS risks to consider are the following:

- The cyclical nature of the semiconductor industry makes SNPS relatively macro-dependent (still less than a pure semi/hardware manufacturer.)

- Should the group have a more aggressive M&A policy, there's a risk to proceed to a bad acquisition with suboptimal synergies.

- Even though the market is segmented, the competition remains tough between the few actors operating in this sector.

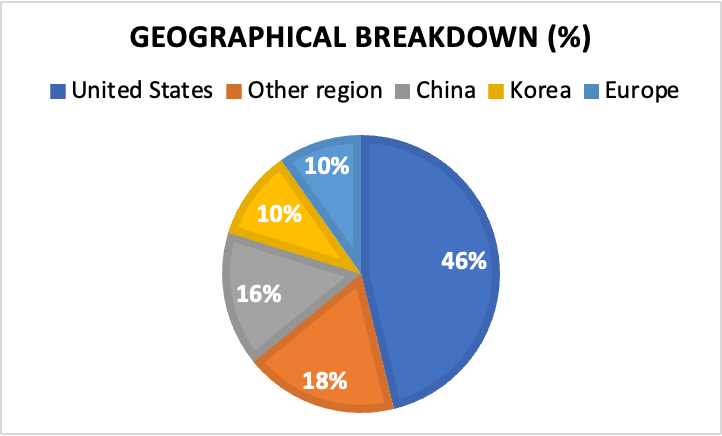

- Potential US export restrictions regarding China, knowing that the Chinese segment Growth is the most dynamic one (15% of revenues in 2022 vs 10% in 2021).

Conclusion

To conclude, I believe that SNPS is an interesting way to have an exposure to the semiconductor industry's secular growth trend. The EDA and IP segments are in my view under-appreciated. With its robust track-record, the group is characterized by a strong reputation, and a capacity to innovate, to deliver while having a rock-solid balance sheet with plenty of cash thanks to its recurring revenue profile. Despite the current environment, I expect the firm to perform well.

Should we be in recession, and should you want to have a Semi-conductor exposure, SNPS is in my view the play to consider.

For all these reasons, I initiate on SPNS stock with a Buy rating and a TP of $ 423 representing a 15% upside.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Synopsys: Robust Semi Exposure To Deal Calmly With Recession Fears