TROW - T. Rowe Price: A 4.4% Yielding Dividend Growth Christmas Present For 2023

Summary

- T. Rowe Price has had a rough year in 2022 with shares down over 40% YTD.

- Despite a weaker environment this year, the margin profile has remained attractive and the balance sheet is still rock solid. AUM has also been increasing over the last couple months.

- Shares trade just over 14x earnings, an attractive valuation in my opinion. In the past, buying TROW in a huge selloff has turned out well for investors.

- The yield now sits at 4.4% and is due for another dividend hike. They have also bought back 2.5% of the common stock so far in 2022.

- I'm looking to add below $100, which would provide a good margin of safety for this potential Christmas gift.

It’s been a couple months since I wrote my last article on T. Rowe Price (TROW), and I figured it was time to write an update as we head into 2023. The stock remains on my watchlist (which is very short outside of the REIT sector), and I plan to add shares in coming months. For long term investors, I think the current price could be a potential Christmas gift for those looking to add a stock with a good mix of current yield and dividend growth.

Investment Thesis

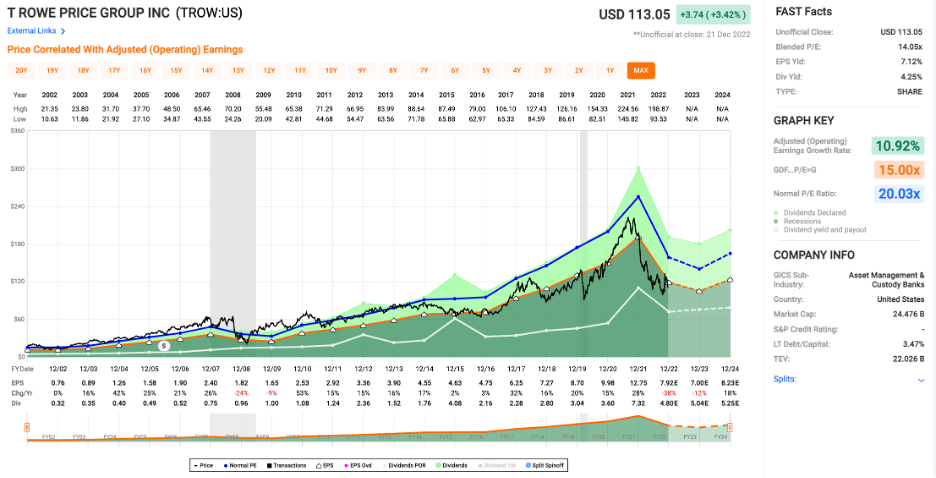

While markets have been tough in 2022, things have been even worse for T. Rowe Price, which is down over 40% YTD. T. Rowe Price has a balance sheet so good they don’t even bother to get a S&P Credit rating, and despite a rough operating environment so far in 2022, they have managed to maintain net margins of 26%. AUM has also increased over the last couple months, a sign that Q4 could be better than Q3.

The valuation is attractive today at 14.1x earnings, and I think the current selloff has created an opportunity for investors take advantage of a cyclical downturn for the company. The yield now sits at 4.4% and is due for another hike. Management is also returning capital to investors via buybacks, which are now happening at a very attractive price. I’m looking to add shares below $100, which would provide a good margin of safety and be a nice Christmas present for 2023.

Q3 Update

T. Rowe Price has had to deal with a rough operating environment for an asset manager in 2022. I won’t sugarcoat the fact that revenues and earnings are down significantly from 2021 levels, but after reading the most recent 10-Q, I don’t think it’s a reason to worry about the long-term health of the company. Despite the decline in operating results, net margins for the first nine months of 2022 were 26%. It’s not the heady 41% margin posted in the first nine months of 2021, but it’s still a high margin business. If T. Rowe Price is this profitable during a downturn in markets, it’s a sign to me that the company should be able to stay profitable in just about any market environment.

As always, the company maintains what is arguably the best balance sheet of any financial, with $2.4B in cash and equivalents, another $2.5B in investments, and no debt. Some might argue Berkshire Hathaway ( BRK.A ) ( BRK.B ) has a better balance sheet, but they belong in their own category if you ask me. Despite the decline in AUM in 2022, things have improved on that front in recent months. AUM increased from $1.23T at the end of Q3 to $1.34T at the end of November. If that trend continues Q4 results will likely be a bit better than Q3. While the company has very impressive financials, the drawdown in stock price in 2022 has created a better entry point for long-term investors.

Valuation

T. Rowe Price currently trades at a price to earnings multiple of 14.1x, which isn’t dirt cheap, but it is below the average 20x multiple. In more recent years, the average multiple has stuck closer to 15x, so I wouldn’t count on multiple expansion. We might see some, but the bullish thesis is more reliant on EPS growth. Estimates show another decline for 2023, but it will be hard to predict exactly where EPS heads because it’s hard to predict which way markets will go. Either way, T. Rowe Price looks like a high-quality company at an attractive price today.

{kind=link}

While the earnings picture isn’t too clear in my opinion, buying shares of T. Rowe Price in a large selloff has turned out to be a good strategy in the past. Shares had a massive drawdown in the 2008-2009 period, going from the mid-60s to the mid-20s. To be fair, shares were expensive going into it at 32x earnings, but if you had the foresight to buy with shares in the 12-14x earnings range after the selloff, you made a killing. Shares are down over 40% YTD, and we could go further from here. I think the risk/reward profile is pretty good, especially considering the 4.4% dividend combined with buybacks.

Dividends & Buybacks

One of the other things that makes me think T. Rowe Price could be a timely buy is the large and growing dividend. If the company’s pattern of dividend increases continues, we are set for another increase with the next quarterly dividend. It might not be a huge increase, but there haven’t been many chances to buy shares with a yield over 4% in the past. I will be looking to add to the position if shares drop below $100, which would push the yield near 5% and create a nice margin of safety.

The other part of T. Rowe Price’s capital return program is the buyback authorization. In the first nine months of the year the company spent $744M to buyback 5.7M shares (2.5% of the common stock). The average price was just over $130 per share, but my guess is they will continue to get more aggressive with repurchases as the share price has dropped. They bought back over 1.3M shares in September alone (average price of $112), so I’m assuming they will buy back a good chunk of stock in Q4.

Conclusion

T. Rowe Price has had a rough year in 2022, with shares down over 40% YTD. Despite the rough year, the company still has an impressive margin profile and has maintained the rock-solid balance sheet. Shares trade just over 14x earnings, and you also get a nice dividend to go with it. I’m hoping to add below $100 per share, which would put the forward yield somewhere in the 5% ballpark. I’m also expecting the dividend growth to continue. It has for 36 years, and I don’t see any reason it would stop in the near future.

Throw in a decent sized buyback program and there is a lot to like about the stock. Earnings might be weak in 2023, but over time, I think investors can expect growing revenue, growing earnings, and growing dividends from T. Rowe Price. Over the last couple months, I have been evaluating my portfolio, making a list and checking it twice. I might end up with a bit of coal in my stocking this year with Peabody Energy ( BTU ), but I also plan to buy myself a gift with shares of T. Rowe Price. It represents a chance for long-term investors to buy themselves a gift in a high-quality, high margin business at an attractive price.

For further details see:

T. Rowe Price: A 4.4% Yielding Dividend Growth Christmas Present For 2023