TROW - T. Rowe Price: Cheap Because Of Some Good Reasons

2023-12-27 11:12:51 ET

Summary

- T. Rowe Price stock looks cheap; but the company operates in a challenged industry, leading to negative earnings growth expectations.

- The company's focus on active investing faces headwinds due to the industry's struggles to consistently outperform benchmarks and the rise of information accessibility.

- T. Rowe Price's equity-heavy asset class and relative lack of fixed income positioning have led to significant outflows in 2023.

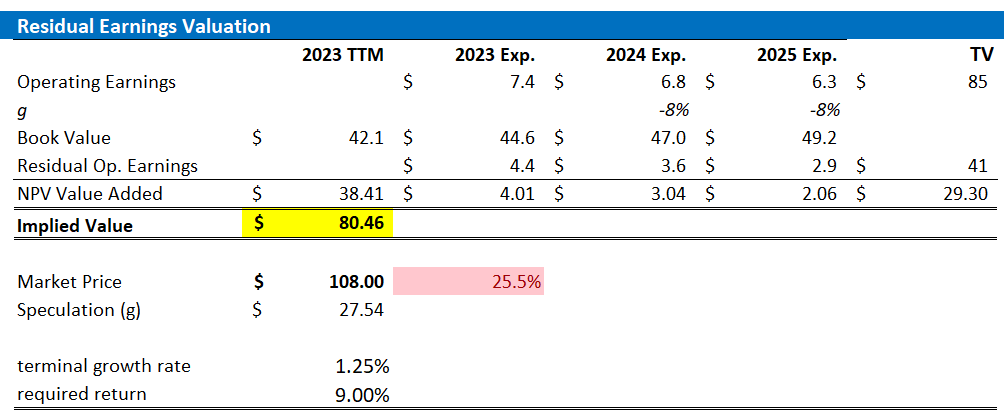

- Based on a residual earnings model framework, I calculate TROW's intrinsic value at $80.46/share.

T. Rowe Price stock ( TROW ) looks cheap at a P/E of 13.30 on consensus 2024 earnings. But a closer look at the underlying company’s fundamentals reveals that TROW is cheap for a reason: The company operates in a highly challenged industry, active investing, while being strongly under-positioned in the fixed income vertical. This combination has recently led to notable outflows of funds, contracting the company's assets under management base to generate earnings. Accordingly, the company's earnings growth is broadly expected to be negative. Reflecting on the high likelihood of negative growth, I personally think that TROW stock is currently overvalued, by approximately 25%. My confidence relating to this assessment is anchored on a residual earnings valuation framework based on analyst consensus EPS estimates.

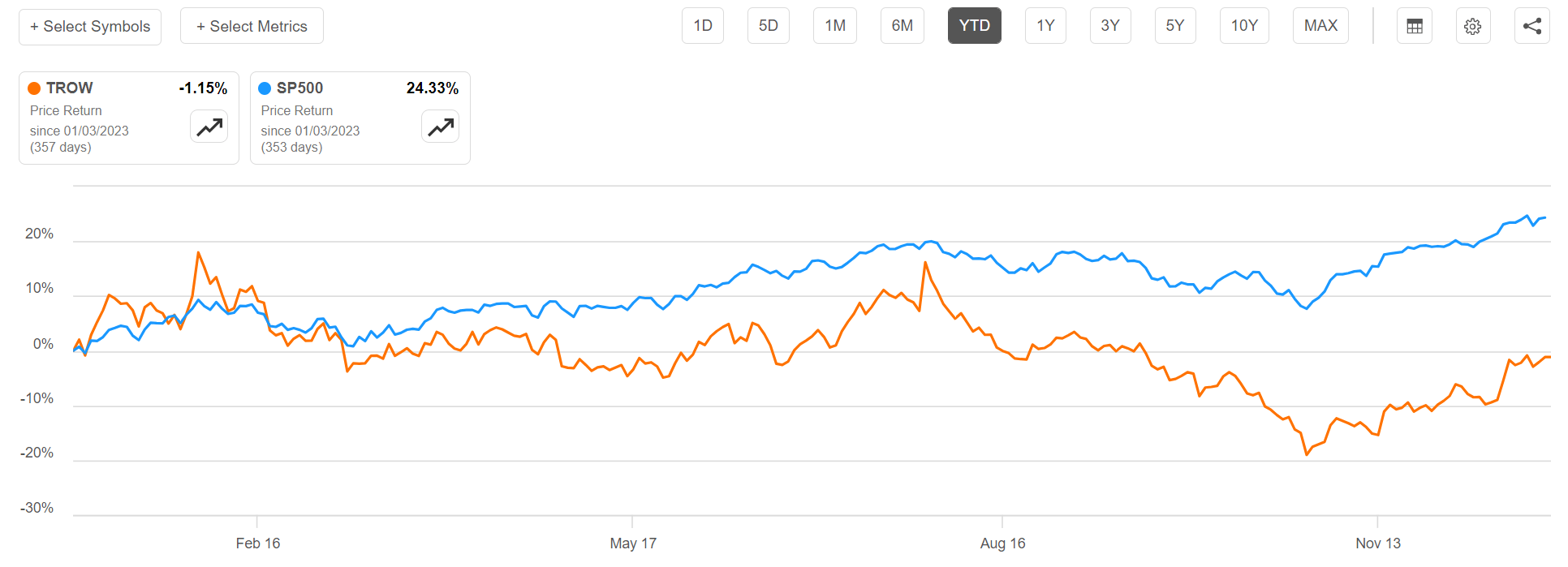

For reference, TROW stock has strongly unperformed recently. For the trailing twelve months, shares are down approximately 1%, compared to a gain of about 24% for the S&P 500 (SP500).

{kind=link}

Active Investing Is Out

T. Rowe Price is an asset manager focused on active investing -- which can be viewed as a structurally declining business model. One of the most prominent criticisms of active investing relates to the well-broadcasted struggle to outperform benchmarks consistently over time. In that context, multiple academic studies, as well as empirical evidence, has shown that a majority of actively managed funds fail to beat their respective benchmarks after accounting for fees and expenses. In fact, fees associated with actively managed funds can be as high as 2.5% annually, posing quite a significant headwind to an investor's performance. And investors have certainly taken note.

Another headwind to the active investing business model is anchored on the rise of information accessibility, which not only made it increasingly more challenging for active managers to consistently exploit market inefficiencies or identify undervalued assets, but also allowed retail investors to more efficiently invest themselves, without having a middle man like T. Rowe Price. Lastly, I point out that the growing trend of passive investing has led to a concentration of assets in a relatively smaller pool of stocks within popular indices. Think Apple (AAPL), Google (GOOGL), Amazon (AMZN), etc. This concentration poses liquidity risks and potential distortions in market pricing, making it even more challenging for active managers to find opportunities outside these heavily invested stocks.

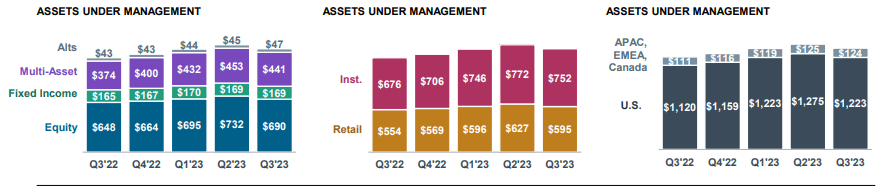

T. Rowe Price's foe of a structurally challenged position in active investing is compounded by the company's business model skew towards the equity asset class, accounting for more than half of the firm's AUM. As benchmark interest rates across the world have been rising, equity investments have broadly become increasingly unattractive compared to fixed income opportunities. But T. Rowe Price's pure fixed income positioning accounts for less than 15% of AUM.

{kind=link}

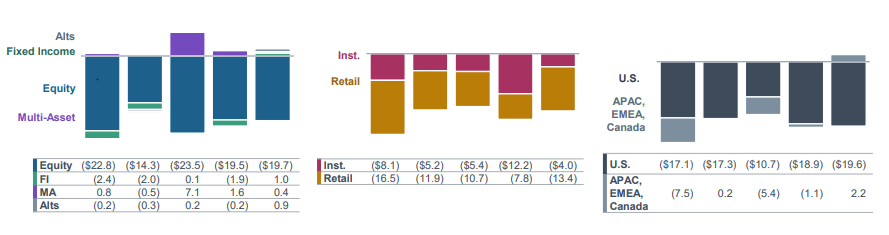

This led to large outflows in AUM, across investor type (institutional and retail) and geographies. The outflow in the Equities business totaled $99.8 billion.

{kind=link}

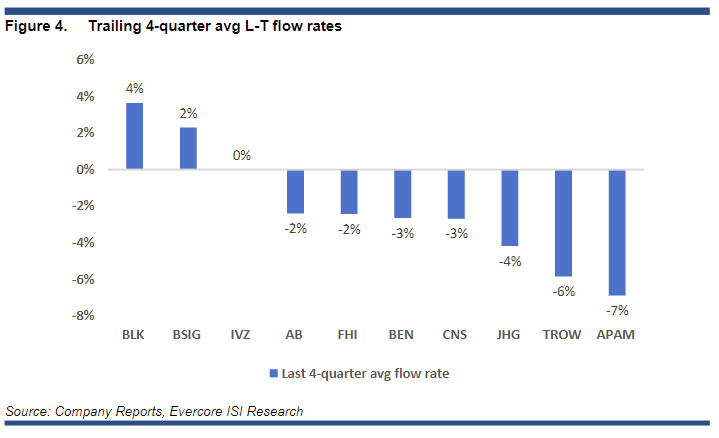

In fact, for the trailing twelve months, TROW has suffered 6% of net outflows, the second worst performance in the industry, and only behind Artisan Partners Asset Management ( APAM ). ( Source: Evercore ISI, research note dated 21st November: Adventures in Asset Mgmt-Land: What's Inflowing Amid the Tough Backdrop? )

{kind=link}

In the context of outflows, it certainly does not help investor confidence that T. Rowe Price management expects a QoQ worsening in outflows during Q4 (mostly seasonal patterns), as commented by

... we expect November and December to have elevated outflows . And November, in particular, is impacted by a single large mandate. December should be consistent with what we've seen in December for the last couple of years.

Consistent with the observation of challenged fundamentals, analyst consensus sees contracting earnings in 2024, with EPS for the twelve months starting January '24 expected to be $6.82 (-8% YoY vs. 2023).

{kind=link}

Likely ~25% Overvalued

In my opinion, companies with steady and relatively predictable business fundamentals like TROW are quite easily and precisely valued with a residual earnings model, which anchors on the idea that a valuation should equal a business' discounted future earnings after capital charge. As per the CFA Institute :

Conceptually, residual income is net income less a charge (deduction) for common shareholders' opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company's capital.

With regard to my TROW stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal till 2026. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor on TROW's cost of equity at 9%, which is approximately in line with the CAPM framework.

- For the terminal growth rate after 2025, I apply 1.25%, which is about 100 basis points below the estimated nominal global GDP growth, due to reasons discussed earlier in the article

Given these assumptions, I calculate a base-case target price for TROW stock of about $80.46/share.

Analyst Consensus; Company Financials; Author's Calculations

{kind=link}

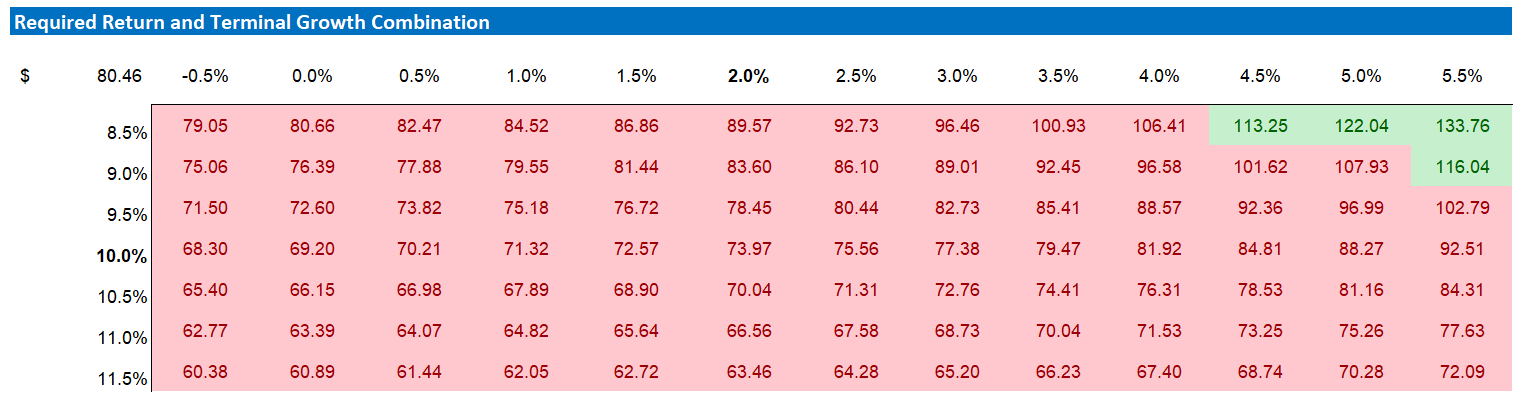

I acknowledge that investors may hold varying assumptions regarding these rates. Therefore, I've included a sensitivity table to test different scenarios and assumptions. See below.

Analyst Consensus; Company Financials; Author's Calculations

{kind=link}

Upside Risk To The Thesis

In my opinion, an unexpected pivot from asset outflows to asset inflows may be a major upside catalyst for TROW's share price. On that note, I view the possibility of 2024 rate cuts, which may stimulate asset & wealth management volume, as the likely key driving factor for this. Moreover, I point out that rate cuts may be supportive of T. Rowe Price's equity-heavy investing strategy.

Investor Takeaway

T. Rowe Price stock looks cheap at first glance, looking at a 14x P/E for the trailing twelve months earnings. However, I don't think TROW shares are a buying opportunity, because negative business momentum on AUM, as well as a structurally shrinking business model (active investing) is suggesting negative growth not only for 2024, but likely also beyond. On that note, I calculate TROW's intrinsic value at $80.46/share.

For further details see:

T. Rowe Price: Cheap Because Of Some Good Reasons