TROW - T. Rowe Price: Transformation Is Too Slow The Stock Is Overvalued

2023-11-27 13:15:17 ET

Summary

- T. Rowe Price Group, Inc. faces serious challenges due to the underperformance of major equity funds like Blue Chip Growth, leading to billions in net outflows in 2022.

- In response to declining AUM, TROW has expanded its offerings to Separately Managed Accounts (SMAs) and ETFs, diversifying into new categories and strategic acquisitions. These have yet to bear major fruit.

- TROW's stock appears overvalued compared to its sector, with high Price to Earnings (P/E) and Price/Book ratios, suggesting a mismatch between market price and sector fair multiples.

Investment Thesis

T. Rowe Price Group, Inc. ( TROW ) is grappling with significant challenges, most notably the sustained underperformance of its key equity funds, including Blue Chip Growth, Growth Stock, and Mid-Cap Growth. These funds, which once accounted for nearly 30% of TROW's assets, have lagged behind their benchmarks over the past 3-5 years, leading to substantial net outflows. In 2022 alone, TROW witnessed over $30 billion in net outflows, a trend that continued into early 2023. This decline in Assets Under Management ((AUM)) is a critical concern, as it directly impacts the company's revenue and profitability.

Further complicating matters is the broader industry shift from active management to passive strategies, such as index funds and ETFs. This trend has posed significant headwinds for TROW, prompting a strategic pivot. In response, the company has expanded its offerings in retail Separately Managed Accounts (SMAs) and Exchange-Traded Funds (ETFs). While this diversification aligns with evolving investor preferences, it is not without challenges. The transition to retail SMAs, in particular, requires managing a higher number of accounts with smaller asset sizes, a shift that could impact TROW's revenue due to lower fees and potentially higher costs to service these accounts.

Despite these challenges, TROW's valuation suggests that the market may be overestimating its growth prospects. The company's valuation metrics, including Price to Earnings (P/E) ratios and Price/Book ratios, indicate an overvaluation compared to its sector. This raises concerns about whether TROW's current market price adequately reflects its financial health and future growth potential. In my opinion the stock is a Sell.

Background: Why is AUM Dropping?

The primary driver of TROW's declining Assets Under Management ((AUM)) is the sustained underperformance of its large-cap growth equity strategies over the past 3 years, especially the Blue Chip Growth, Growth Stock, and Mid-Cap Growth funds. However, they have posted disappointing returns over the 3- and 5-year periods relative to benchmarks and peers.

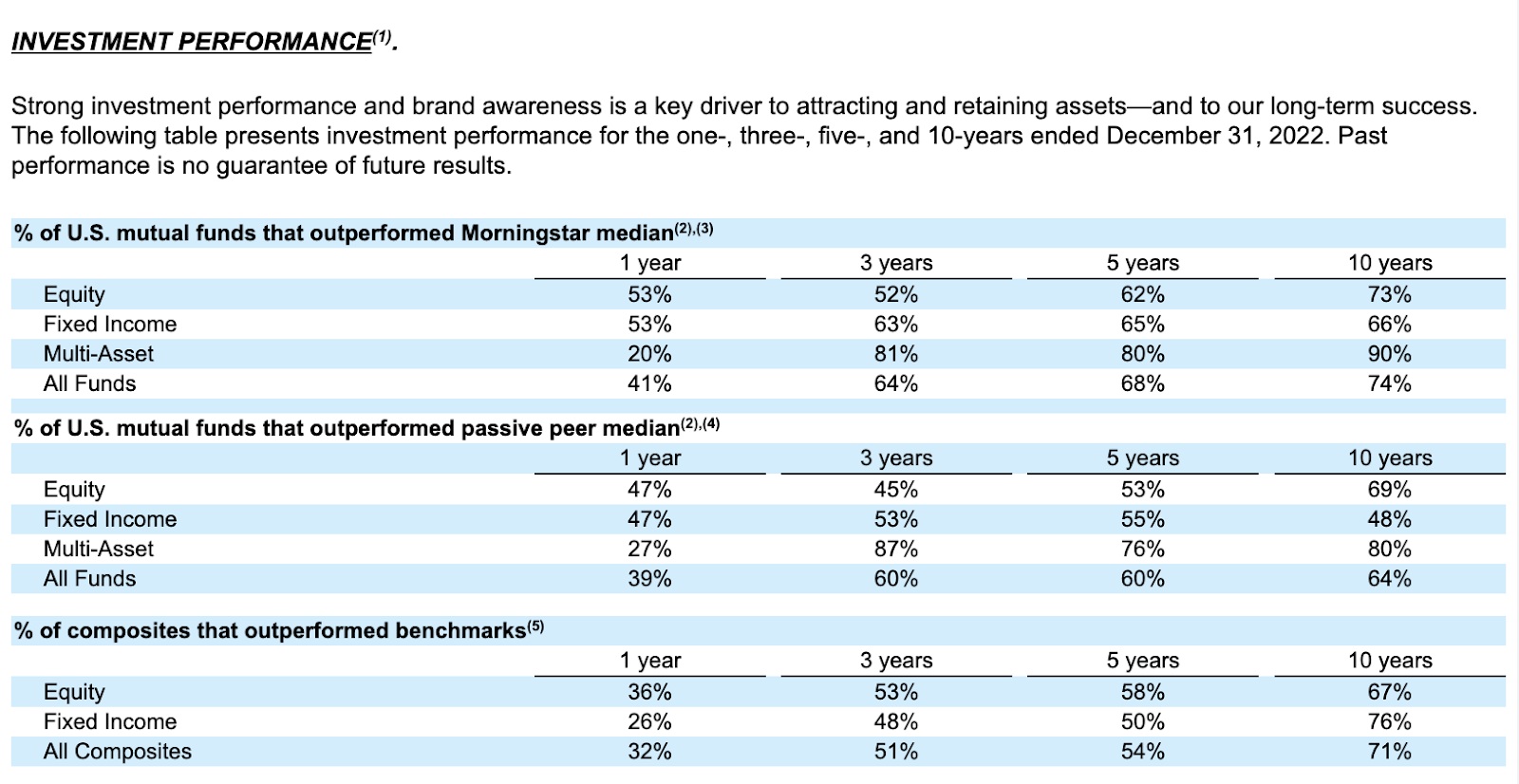

TROW Investment Fund Performances (TROW 2022 10K)

{kind=link}

Many of their funds are simply falling behind the benchmarks. For example, the one of the firm's flagship funds (Blue Chip Growth) has returned just 2.6% annualized over 3 years and 12.53% over 5 years compared to 22.56% and 21.98% compounding returns for the category for over the same periods. This sustained underperformance has led to over $60 billion in net outflows from these strategies in 2022 and continued redemptions in early 2023 ( TROW Earnings Releases ).

In addition to performance challenges, TROW faces broader industry headwinds impacting active equity managers. Investors have rotated significant assets from active growth-oriented funds to passive index strategies and lower-cost ETFs. This shift reflects a tough backdrop for justifying higher fees in exchange for alpha generation. As a result, TROW and peers focused on active U.S. equities have experienced elevated outflows despite improved near-term performance.

In total, these dynamics help explain the $61.7 billion in net outflows for TROW in 2022. While strategic initiatives around expanding product shelf space are encouraging, substantial AUM declines present an earnings headwind until sustained performance improvement and asset gathering emerge.

The Bull Case: Management's Response

In response to the significant challenges of asset outflows and changing market conditions, T. Rowe Price management has embarked on a multifaceted strategic response. A key element of this strategy has been the expansion of their offerings in retail Separately Managed Accounts (SMAs) and Exchange-Traded Funds (ETFs). They have increased the number of investment strategies available in retail SMAs by over 20%, including the introduction of four municipal and two equity SMA strategies, and launched five active equity ETFs. This expansion has led to a growing ETF lineup that has reached $2 billion in assets under management ((AUM)), indicating a positive reception and inflows from clients????.

Further diversifying their product offerings, T. Rowe Price has ventured into new categories and completed strategic acquisitions. Notable developments include finalizing the seed commitment for the T. Rowe Price OHA Select Private Credit Fund and acquiring Retiree Inc., which is expected to enhance their retirement income and social security claiming strategies. These initiatives represent a broader plan to cater to a wider client base with varied needs??.

Concurrently, T. Rowe Price has aggressively managed its expenses and operational efficiency in response to the downturn. The firm has reduced its global workforce by approximately 2% and slowed down hiring and headcount growth. These measures are projected to remove or relocate over $200 million in operating expenses by 2024, aiming for low-single digit adjusted operating expense growth in the same year ( Q2 2023 Earnings Call ). This is a strategic effort to align the firm's cost structure with its current size and scale while maintaining financial discipline??.

Despite these efforts, the firm continues to face challenges in specific segments. Outflows have been particularly pronounced in its U.S. large-cap growth equity products, driven by market volatility and performance issues. However, there have been areas of positive inflow, such as U.S. equity research, capital appreciation, international core, all-cap opportunities, and international fixed income. Target date products have also recorded significant inflows, with $9.9 billion in the first half of the year (Q2 Earnings Call). Yet, these positive developments have not been sufficient to offset the outflows in other areas entirely??.

Why Management's Actions Are Not Enough

Despite TROW management's response to challenges, this may not be sufficient to overcome the scale of its current difficulties. A deeper analysis of its expansion into retail Separately Managed Accounts (SMAs) and diversification in retirement products, show that uphill challenges lie ahead even in the green shoots of the business.

Fee Challenges in Retail SMAs Expansion

T. Rowe Price's entry into the retail SMA business involves adapting existing mutual fund offerings to the SMA format. The firm's initial lineup includes U.S. growth and value strategies based on three existing T. Rowe mutual funds: the U.S. Growth Stock Fund, the U.S. Value Fund, and the U.S. Blue Chip Growth Fund. While this diversification aligns with the evolving needs of clients and distributors, it presents challenges in execution and market penetration. Retail SMAs require managing a higher number of accounts with lower asset levels compared to institutional mutual fund companies, which typically manage high asset levels with fewer accounts. Additionally, while the move to SMAs can help T. Rowe Price retain client assets in lower-cost vehicles, it also involves commanding lower fees compared to mutual funds , potentially impacting revenue.

Operational Challenges in Retail SMA Business

The operational shift to managing a larger number of smaller accounts necessitates significant changes in technology and operational support. T. Rowe Price has partnered with Archer for technology and operational support to simplify its entry into the SMA space. However, this shift also requires a change in focus for the product team, including additional staff for reporting and marketing but no additional distribution hires. Keep in mind the cost controls management has already indicated they're undertaking. There's definitely a risk here that they are malnourished this new division/offering.

Overvalued Compared to the Sector

In spite of continued outflows from key products, T. Rowe Price still appears overvalued when compared to its sector. The company's overall valuation grade is a "C-", with specific areas such as forward and trailing Price to Earnings (P/E) ratios receiving a "D+" grade according to Seeking Alpha valuation metrics . Their FWD Price/Sales ratio is 47.39% higher (3.43x vs. 2.35x) and the FWD Price/Book ratio is 124.84% higher than the sector median, (at 2.37x vs. 1.05x), indicating another significant overvaluation relative to peers. TROW's trailing twelve-month GAAP P/E ratio (using GAAP since it's already been reported) aligns with the historical average (14.01x vs. 14.62x), but the company's FWD Non-GAAP P/E estimates are currently 41.55% above the sector average (13.30x vs. 9.39x). The firm is trading at a premium to the sector in spite of AUM outflows and poor performance. This is not a recipe for a premium valuation in my opinion.

Takeaway

In my opinion, T. Rowe Price presents a clear case for divestment. The company's struggles with underperforming key equity funds, coupled with the industry's pivot towards passive investment strategies, mark significant business changes that do not warrant a premium valuation. The overvaluation of TROW's stock, as indicated by various valuation metrics, suggests a disconnect between its market price and intrinsic value. These factors, combined with operational challenges and the uncertain efficacy of its strategic responses, paint a concerning picture for TROW's future performance. I believe TROW is a sell.

For further details see:

T. Rowe Price: Transformation Is Too Slow, The Stock Is Overvalued