TROW - T. Rowe Price: Why I Would Buy The Dip

2023-10-24 13:12:34 ET

Summary

- T. Rowe Price Group shares have fallen -53% since hitting an all-time high in August 2021.

- TROW operates in a competitive industry but has a strong track record which has created a competitive advantage.

- TROW has a strong balance sheet, shareholder-friendly capital allocation, and trades at an attractive valuation compared to its historical norms.

- I am initiating TROW with a buy rating.

Shares of T. Rowe Price Group ( TROW ) have had a tough go of it lately. Since hitting an all-time high in August 2021, TROW shares have returned -53% on a total return basis compared to a total return of -3.5% for the S&P 500 and -12.4% for the financial sector ( XLF ) during the same period.

I believe this dip has proven investors with an opportunity to buy a very strong asset management franchise at a great valuation. Thus, I am initiating TROW with a buy rating and standing with fellow Seeking Alpha contributors who are bullish on TROW despite bearishness of Wall Street analysts.

Seeking Alpha

Company Overview

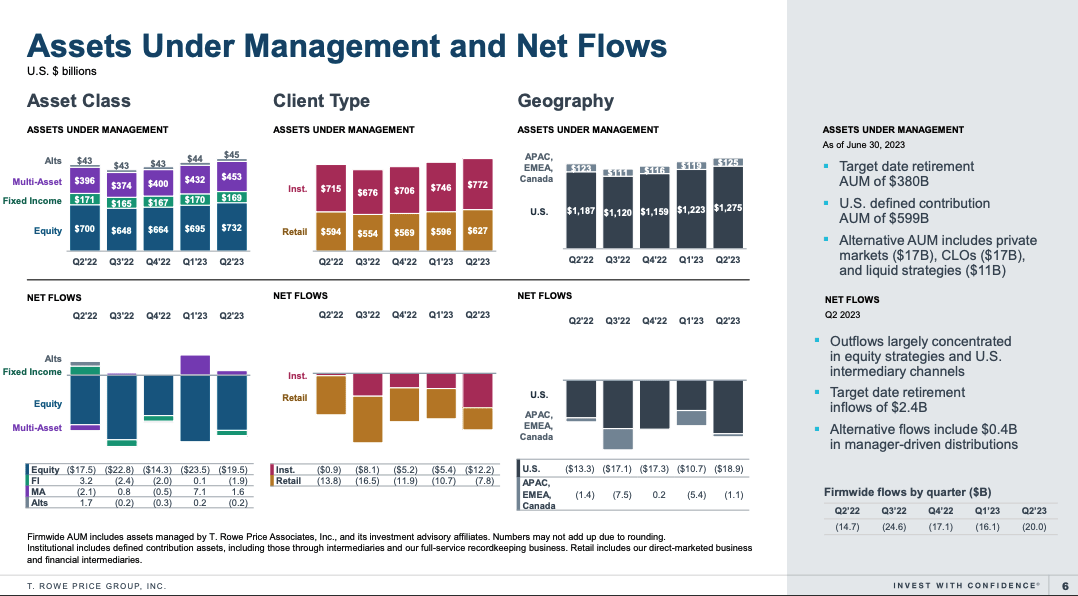

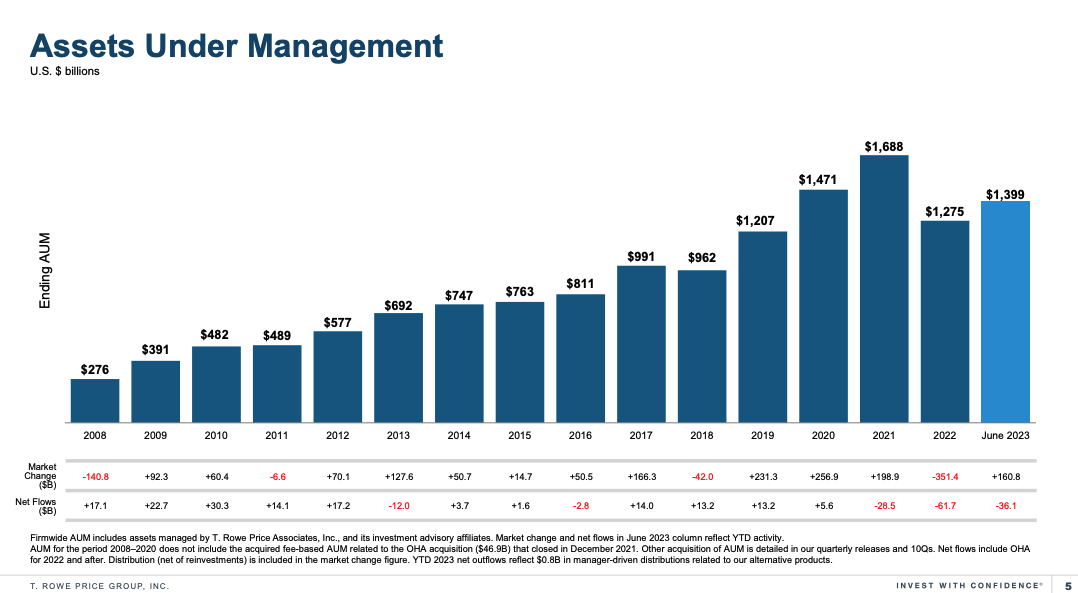

TROW is a large asset management firm with ~$1.4 trillion in assets under management ("AUM"). TROW currently ranks as the 16th largest asset management firm in the world. TROW manages strategies across equities, fixed income, multi-asset, and alternative investments. Equities represent the largest business for TROW accounting for ~52% of total AUM. TROW manages assets for both individuals and institutions with the institutional business slightly larger accounting for ~55% of AUM.

TROW has a long history of steadily growing its AUM but has suffered recent outflows, primarily driven by the equities business, since late 2021.

{kind=link}

{kind=link}

Asset Management Industry Dynamics

TROW operates in a highly competitive business and competes against a host of very strong firms including BlackRock ( BLK ), Vanguard, State Street ( STT ), BNY Mellon ( BK ), Fidelity Investments, JPMorgan ( JPM ), Goldman Sachs ( GS ), UBS ( UBS ), Morgan Stanley ( MS ), Franklin Resources ( BEN ), Invesco ( IVZ ), and many others.

Despite the highly competitive business landscape, TROW has been able to achieve very strong results historically. Over the past 20 years TROW has delivered a total return of 706% compared to 497% by the S&P 500 and 126% by the financial sector ((XLF)).

TROW, along with other large asset management firms, tend to enjoy very healthy profit margins and high return on invested capital. This is important as it indicates despite the fact that a lot of high quality firms are competing in the asset management space the intensity of the competition is lower. While active management fees have declines over-time due to pressures from passive we have not seen active fund managers aggressively undercutting each other on fees. Part of the reason for this is that fund flows tend to be sticky (particularly in the retail segment) and once funds have been allocated to a given firm it is not easy for other players to win those dollars away.

Strong Track Record Creates Competitive Advantage

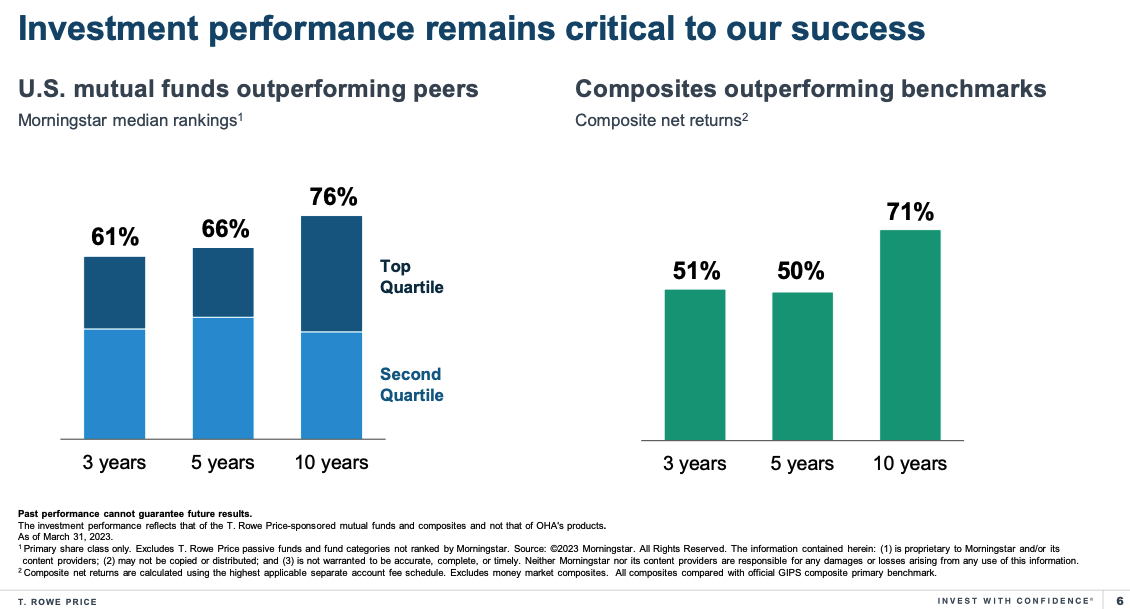

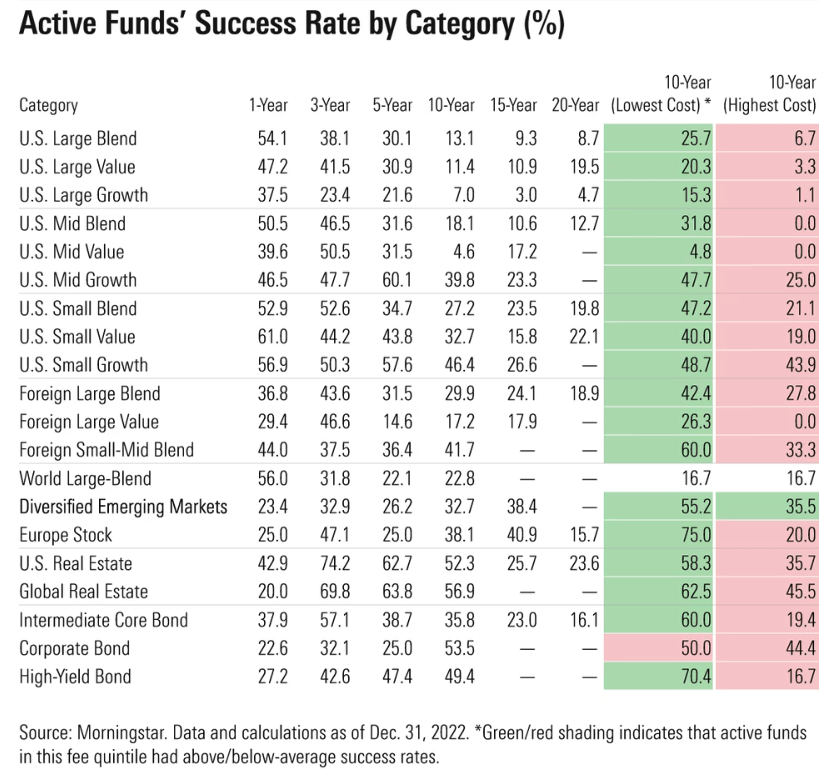

TROW's enjoys a few characteristics which I believe have helped to create a defensible competitive advantage despite a highly competitive industry. The first part of TROW's competitive advantage comes from its strong long-term performance track record. As shown by the chart below, 71% of TROW's composites were outperforming over the past 10 years as of March 31, 2023. Comparably, just 13.1% of active large U.S. Blend funds have outperformed over the past 10 years. Active success rates are also dismally low in other equity products as well. Thus, when competing for new mandates or trying to retain assets in a world where passive is constantly gaining share TROW has a strong advantage relative to peers in that it possesses a strong historical track record. Moreover, this strong track record is not something that can be easily replicated by other managers and has allowed TROW to outperform peers (with the exception of BLK which has benefited from its passive business.)

{kind=link}

{kind=link}

Strong Balance Sheet

Currently, TROW has $2.25 billion in cash on its balance sheet and no debt. TROW's net cash position represents $10.03 in cash per share or ~10.4% of the current share price. TROW's strong balance sheet is a major positive as it insulates the company from the impact of rising rates in terms of interest impact. Moreover, TROW's strong balance sheet creates the potential to take advantage of potential M&A opportunities. In October 2021, TROW announced the acquisition of Oak Hill Advisors for $4.2 billion which helped kickstart TROW's push into alternative investments.

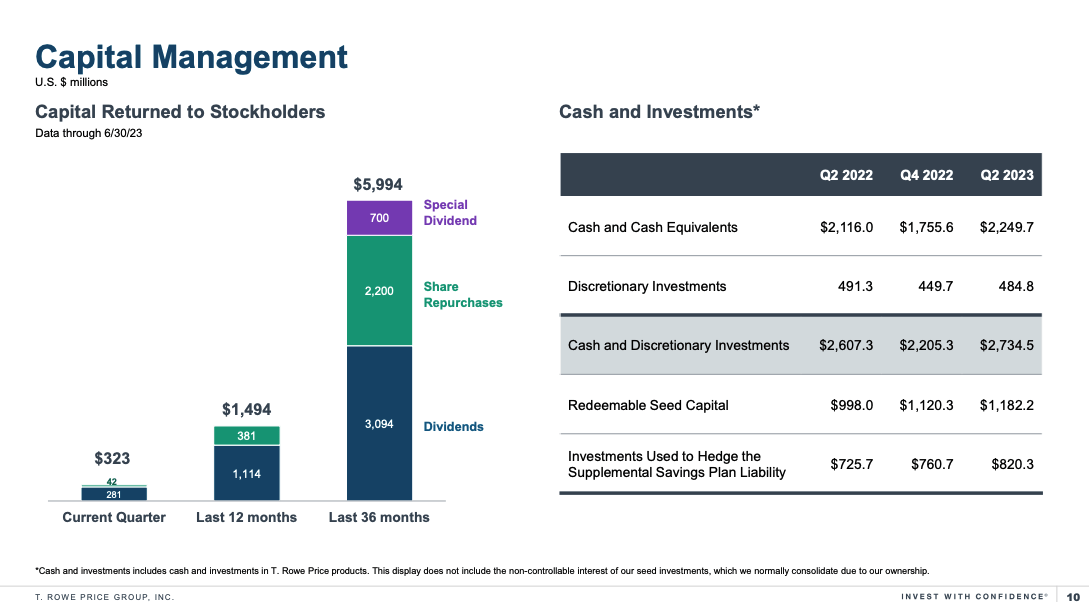

Shareholder Friendly Capital Allocation

As shown below, TROW has a very friendly capital allocation policy and has returned nearly $6 billion in capital to shareholders over the past 2 years alone in the form of dividends and share buybacks. To put this in context, TROW currently has an enterprise value of ~$21 billion.

TROW has raised its regular dividend for 37 consecutive years and recently announced a 1.7% increase in March 2023. Currently, TROW yields 5.08% and enjoys very strong Seeking Alpha dividend grades.

Seeking Alpha

{kind=link}

Relative Valuation

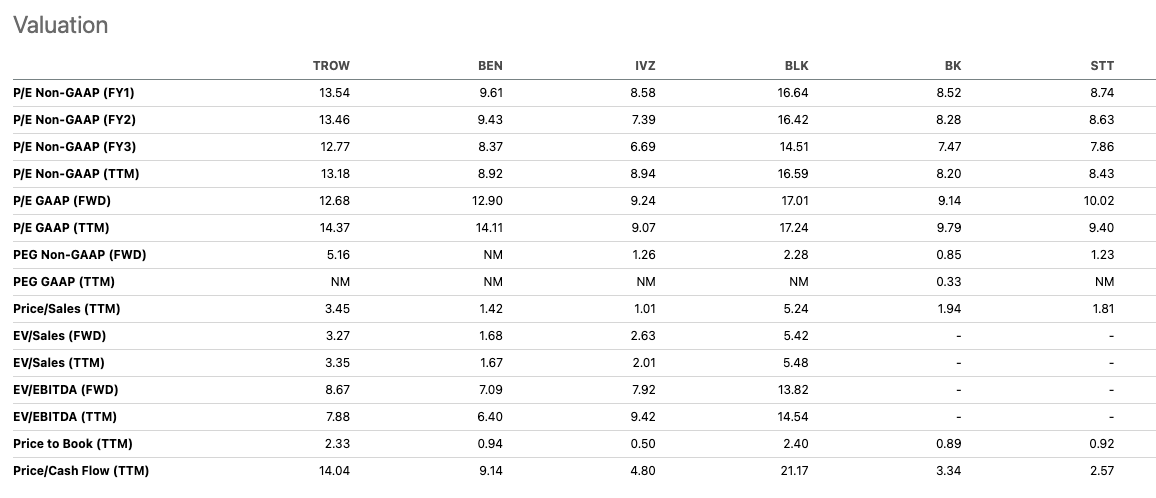

TROW currently trades at 13.5x forward earnings (12.1x after backing out the net cash) compared to 17.9x for the S&P 500. While TROW is clearly cheap on an outright basis, it is also important to compare valuations relative to growth expectations. Over the past 10 years, TROW has grown EPS by ~7% per year. However, over the past 2 years, TROW has only been able to grow earnings by ~2%. I believe the past 2 years have been especially challenging given the market climate due to rising rates and thus I believe the company can grow long-term EPS by ~6% which is roughly in line with consensus estimates. Thus on a forward PEG ratio basis I see TROW trading at 2.25x compared to 1.49x for the S&P 500 (assuming the consensus 12% growth rate.) While TROW is more expensive based on this metric, I believe the premium is worth it given TROW's high quality business and competitive advantage which is difficult for peers to emulate.

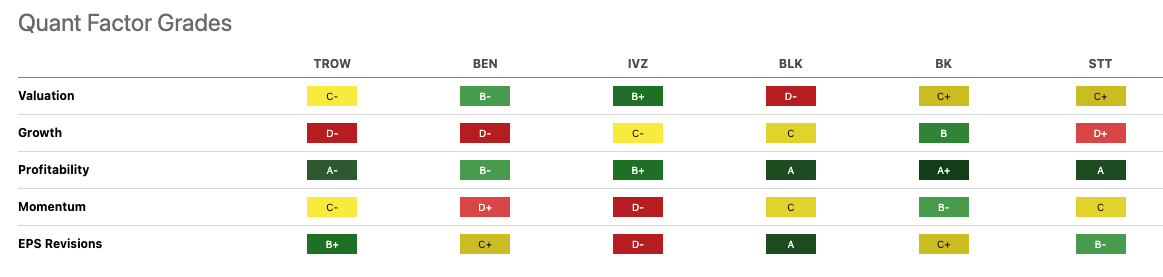

As shown by the tables below, TROW is generally trading at a higher valuation than its peer group with the exception of BLK. TROW receives a Seeking Alpha quant valuation grade of C- compared to B- for BEN, B+ for IVZ, and C+ for BK and STT. I believe TROW is worth the premium due to its strong historical track record and strong balance sheet.

{kind=link}

{kind=link}

Historical Valuation

TROW is currently trading at a significant discount relative to its own historical valuation average. Thus, I believe TROW's valuation is attractive relative to its own historic norms.

Potential M&A Target

The asset management industry has experienced a wave of consolidation in the past few years. Some key deals have included Morgan Stanley's 2021 acquisition of Eaton Vance for $ 7 billion, Franklin Resources' $ 4.5 billion acquisition of Legg Mason in 2020, and a number of other smaller deals. In my opinion, TROW is the pre-eminent asset manager that remains in play from an M&A perspective. I believe potential suitors for TROW include Goldman Sachs ((GS)), Prudential, BNY Mellon, and State Street. All of these firms are focused on growing their asset management businesses and the potential synergies gained due to further scale could be substantial. Moreover, TROW's historically strong track record could be used to allow weaker funds at any of these firms to merge into existing TROW funds thereby improving historical results of any combined franchise.

Q3 2023 Earnings Preview

TROW is scheduled to report Q3 2023 results on October 27, 2023. Consen sus estimates call fo r the firm to report EPS of $1.78 per share which represents a 4.3% decline on a year-over-year basis. Revenues are expected to come in at $1.64 billion, up 3.4% on a year-over-year basis. Given the recent weakness in the stock price, I believe the stock could rally substantially in the event of any positive news while the negative impact related to negative news may be more muted.

Risks to Consider

The most significant risk I worry about with TROW is potential decay in its long-term product performance track record. While TROW's 10 year historical performance remains strong (71% of composites have outperformed their benchmark), performance relative to benchmarks over the past 3 and 5 years has been more challenged with just 50% of composites outperforming. If TROW fund performance suffers in the future, this is something that would lead to be re-consider my buy rating.

Conclusion

TROW has delivered strong shareholder returns historically over long-periods of time. However, the stock has declined sharply over the past 18 months due to falling AUM and thus lower earnings. Like all active asset managers, TROW faces challenges to its business due to the increasing popularity of passive products. That said, I believe TROW is a differentiated franchise due to its strong historical investing track record. TROW's strong historical track record gives it an advantage relative to other active managers with weaker historical performance. Additionally, TROW's strong historical track record makes it an attractive acquisition target for larger asset managers.

TROW trades at relatively low valuation of just 12.1x earnings after backing out the company's substantial net cash position. This represents a significant discount to the S&P 500's forward PE ratio of 17.9x. TROW trades at a moderate premium to other weaker asset management peers. I believe this premium is warranted given TROW's competitive advantage due to its strong investing track record.

In addition to trading at an attractive valuation TROW also currently yields over 5%. I believe the dividend is safe and the company has an impressive 37-year history of raising its regular dividend.

I am initiating TROW with a buy rating but will be closely following performance metrics in the quarters ahead as well as fund flows. Substantial deterioration in performance relative to benchmarks would lead me to reconsider my rating given that a large part of my thesis regarding TROW is related to the company's strong investing track record relative to active peers.

For further details see:

T. Rowe Price: Why I Would Buy The Dip