TBLA - Taboola And Outbrain: The Future Of The Open Web?

2023-08-31 13:34:14 ET

Summary

- Taboola and Outbrain, the dominant players in the online recommendation market, have seen decreasing profitability in 2022 and 2023.

- Both companies are investing heavily in new initiatives to expand outside of their core markets and capture a larger share of the digital advertising industry.

- Taboola is focusing on ecommerce, header bidding, and its Taboola News app, while Outbrain is betting on pre-roll video ads and its internal DSP.

- Both are cheap based on more normalized FCF measures, but it's unclear when or even if new business lines will pay off like management says.

- Overall, with the Yahoo deal expected to contribute significantly to revenue and earnings growth in 2024 and beyond, and the recent commerce investments looking like a promising area of the market to focus on, Taboola appears to be the better bet between the two.

Taboola (TBLA) and Outbrain (OB) are a bit of a conundrum. The two combined control the vast majority of the lucrative online recommendation market, and have seen improving growth over the last few years. But each company has seen decreasing profitability throughout 2022 and 2023, with both investing heavily into future initiatives to expand outside of their core markets.

As a result, both companies are down a lot from their SPAC IPOs, with Outbrain losing roughly 75% of its market value and Taboola losing roughly 65%.

The two companies operate in their own area of the digital advertising market. They claim that they're pioneering advertising and content discovery on what they call the "Open Web" - essentially, the internet outside of the big tech walled gardens. Based on their SEC filings and shareholder communications, the companies are clearly couching themselves as a bet on the further disintermediation of the big tech gatekeepers.

And, regardless of whether you believe they're pioneering the open internet, there's no denying that the two have created an independent content discovery and advertising network. They have strong direct relationships with both advertisers and publishers. Taboola has said that 90% of its advertising revenue comes directly from brands/advertisers, with only 10% coming from new "open internet" DSPs like The Trade Desk. Combined with this is the fact that the companies could benefit from the eradication of the traditional third-party cookie. TTD is doing a good job of implementing its own, but Taboola's and Outbrain's direct relationship with large publishers across the internet gives them an edge in the amount of accurate first-party data they can offer to advertisers.

The business models of both companies still rely primarily on the traditional direct marketing chumbox ads. For Taboola, this is still ~70% of their total business, and for Outbrain, it's probably something similar, or even higher (though they don't break out the number).

You know what types of ads I'm talking about, they're the clickbait-type images and headlines that populate the bottom of most news websites. This business is considered undesirable by many in the media (even though it ironically supports almost every major online publisher), but it's undisputable that both companies have found something that works.

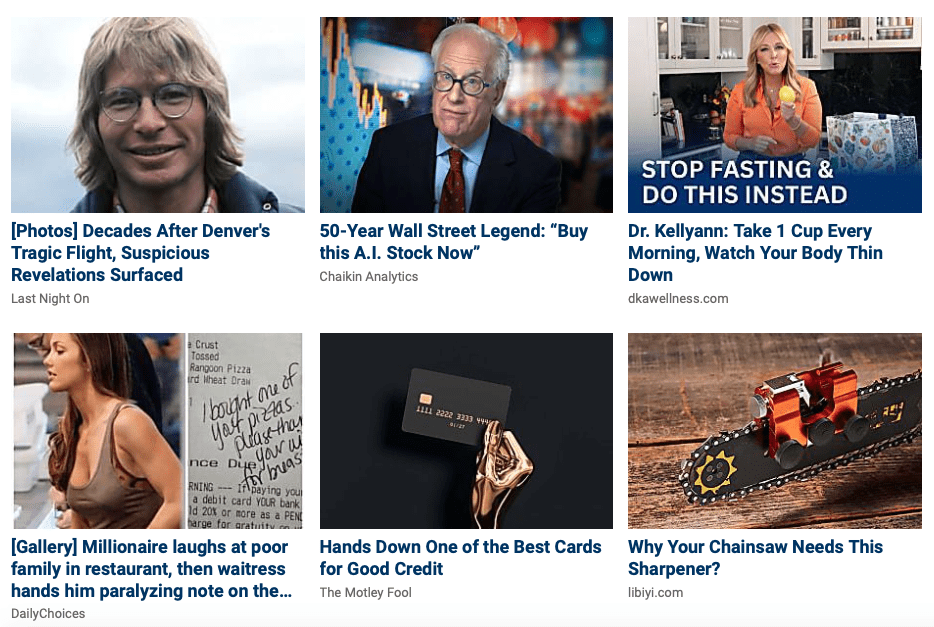

An example of Taboola recommendations:

{kind=link}

{kind=link}

{kind=link}

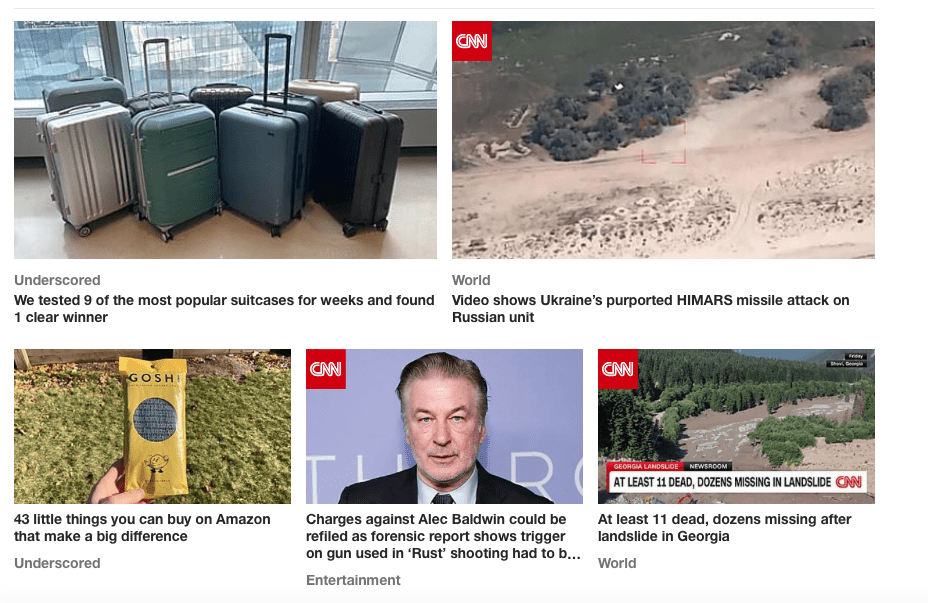

And from Outbrain:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

As you can see, both sets of pictures contain a mixture of direct response-type traditional chumbox advertising, more brand-like advertising, and also recommendations for other articles on the actual site that Taboola/Outbrain is operating on.

This is the core of both companies' business models. But they're both investing pretty heavily in new initiatives to expand outside of this core business.

Recommendation's Place in the Digital Advertising Industry

I don't think it's any secret that the recommendation market (and by that I mean Taboola and Outbrain) are kind-of social pariahs in the digital advertising market. They offer ads (not all of their ads, mind you) that are not welcome on larger social media platforms like Facebook and from sites that people don't typically search for in Google (some sites that even intentionally avoid showing up in Google).

From this characterization, it's easy to see why the two describe themselves as the search engines of the open internet. And they very well could be - they do drive clicks across a range of interconnected websites. But a good chunk of their revenue is generated by ads placed across these websites - otherwise known as chumbox ads. Many (though not all) of these ads are from companies that are essentially cut off from the walled gardens of the big tech ecosystems. But they are used by a majority of the larger premium news and entertainment websites across the internet. And I'm not here to judge the ads - Taboola and Outbrain obviously provide a traffic-generation service that was needed by a certain type of business and wasn't being met by other marketing methods.

Some of Taboola's largest publishing partners include NBCUniversal (which uses Taboola on CNBC, NBC.com, etc.), Yahoo (which they have an exclusive 30-year partnership with now), Microsoft MSN, Conde Naste, Univision, Huffington Post, etc.

Outbrain's large publishing partners CNN, Fox News, Axel Springer, The Washington Post, Sky News, Daily Mail, Fortune, Coindesk, etc.

Both companies claim a large number of advertisers - Taboola with 18,000 and Outbrain with 30,000. And while some of these are larger brands like Nike, it seems that the biggest spenders are various players in the direct marketing industry.

And this is who Taboola and Outbrain's recommendation systems appeal most to. Direct marketers are used to the days when their advertorials would appear in magazines and newspapers, masquerading as an article. The website-native nature of the recommendations that Taboola and Outbrain offer are a 21st-century version of this.

Roughly $567 billion was spent on digital advertising worldwide in 2022. The numbers aren't perfect, but it's estimated that a little over a third of this spend goes to the "open web" while the rest goes to the "walled gardens" - Google, Facebook, YouTube, TikTok, Amazon, etc. In fact, it's estimated that just under 40% of total digital advertising spend went to search (which is primarily Google).

This 37% number - worth $209.8 - obviously doesn't all go to Taboola and Outbrain though. The two primarily operate with the leading news publishers across the internet - rarely straying too far from their core market (a large number of articles, produced daily, play well for a recommendation engine). Even outside of Facebook and Google, there are still a large number of walled-garden tech ecosystems (Amazon, Twitter, Pinterest, TikTok, etc.) that are capturing a large share of the digital advertising spend.

Let's take a look at total internet traffic, though, to get a sense of the two's place in the massive digital media market - and how much room for growth they actually have.

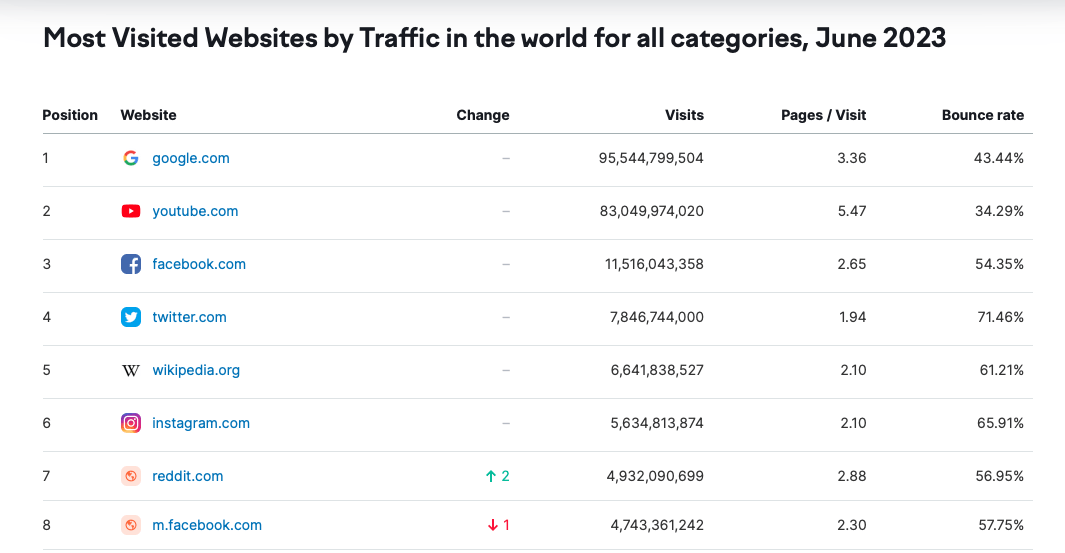

Here's a look at the most visited websites on the internet:

{kind=link}

{kind=link}

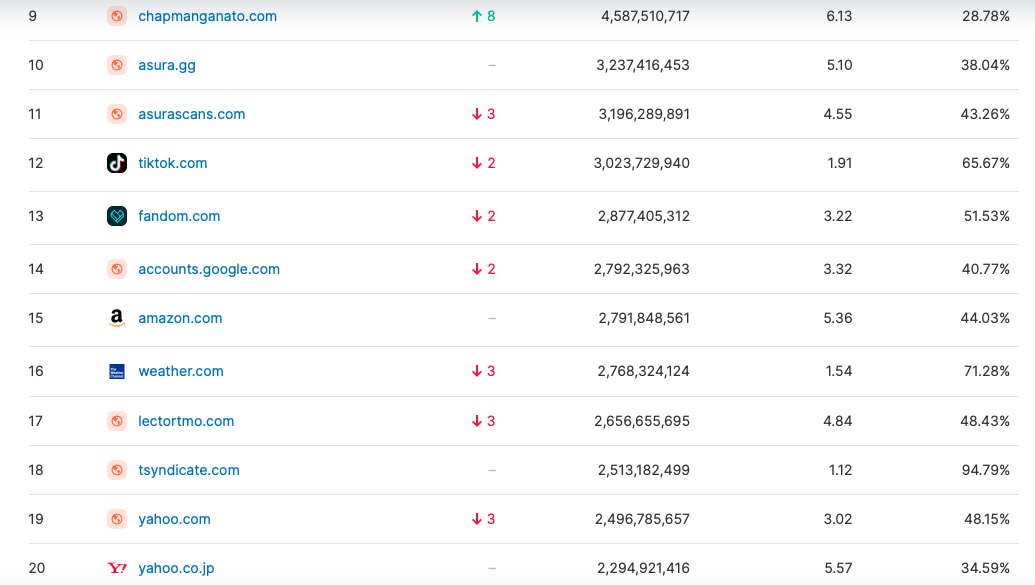

As you can see, the majority of the total views in the month of June went to the tech walled gardens - the vast majority going to Google though (95.5 billion) which itself is then likely sending the visitors to other parts of the internet. If you take Google out of the equation, the top 20 is still filled with big tech and their subsidiaries - YouTube (Alphabet), Facebook, Instagram (Facebook), TikTok, Reddit, Amazon, Twitter. All of these are locations that are walled off from the rest of the internet and have their own advertising ecosystem. It's also debatable how much of the 95 billion views Google got also went to Amazon, Facebook, etc. after stopping at Google first.

I will say though that one Taboola name made its way into the list. Yahoo, who Taboola just entered into a 30-year partnership with to be the exclusive ad partner across its properties, brought in over 2 billion views in the U.S. and a similar amount in Japan. But, as you'll see below, this is Yahoo's homepage, which a lot of people may be using for search or to enter into their Yahoo Mail account. The actual portions of Yahoo that Taboola will be advertising the most on - Yahoo News, Yahoo Finance, etc. - are seeing monthly visits in the 100 million range.

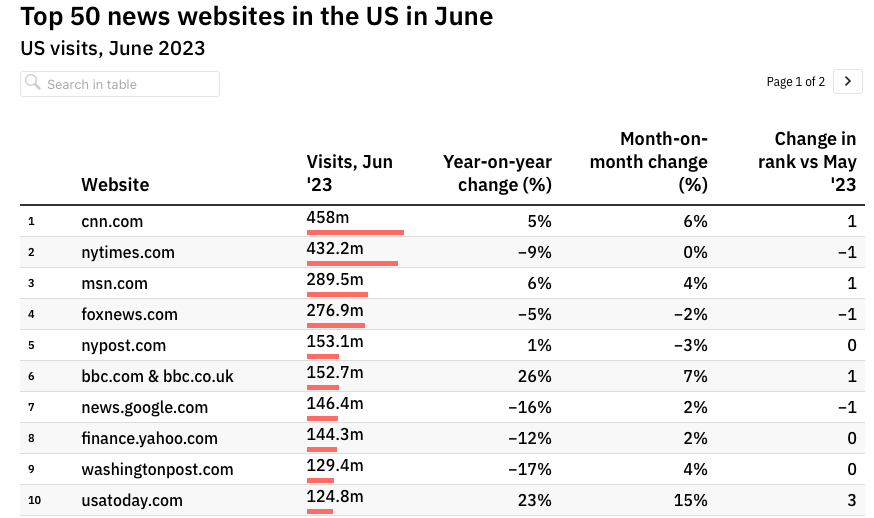

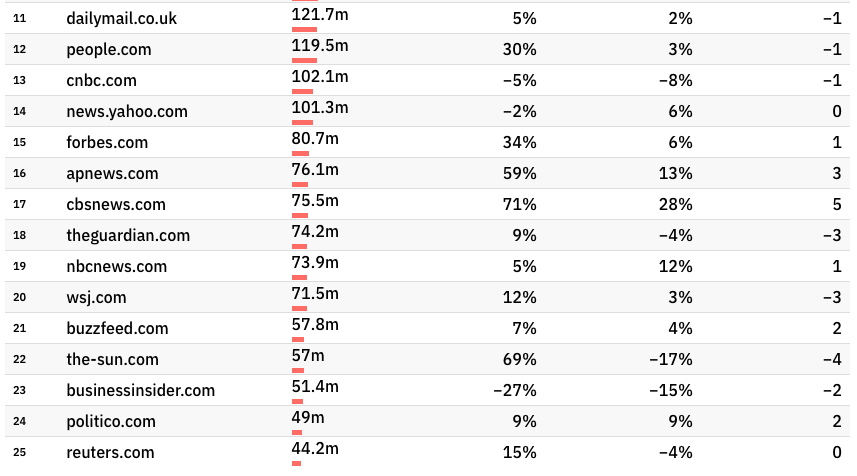

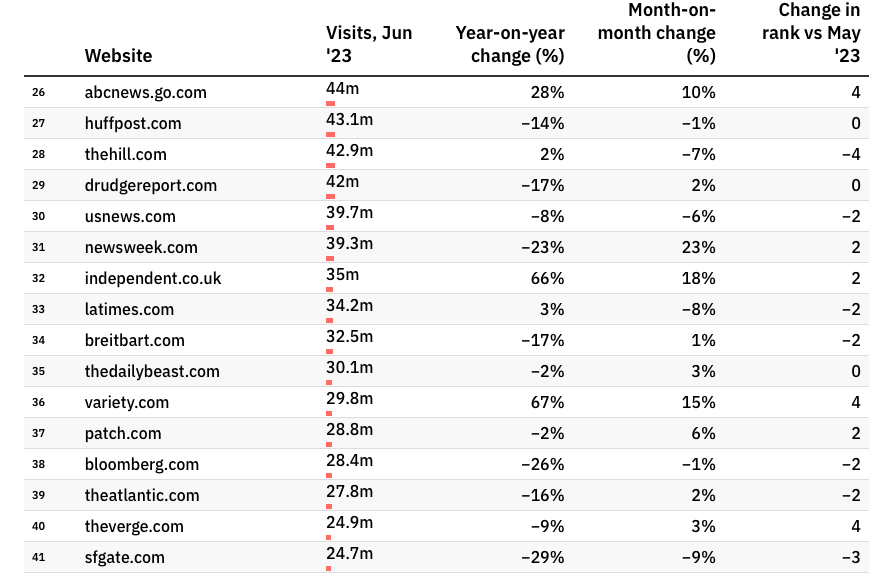

Besides Yahoo, though, the majority of the publishers that Taboola/Outbrain work with are premium news websites. To compare the kind of traffic they get, I've included a list of the most visited news websites below - a list that is very representative of Taboola/Outbrain clients.

{kind=link}

{kind=link}

{kind=link}

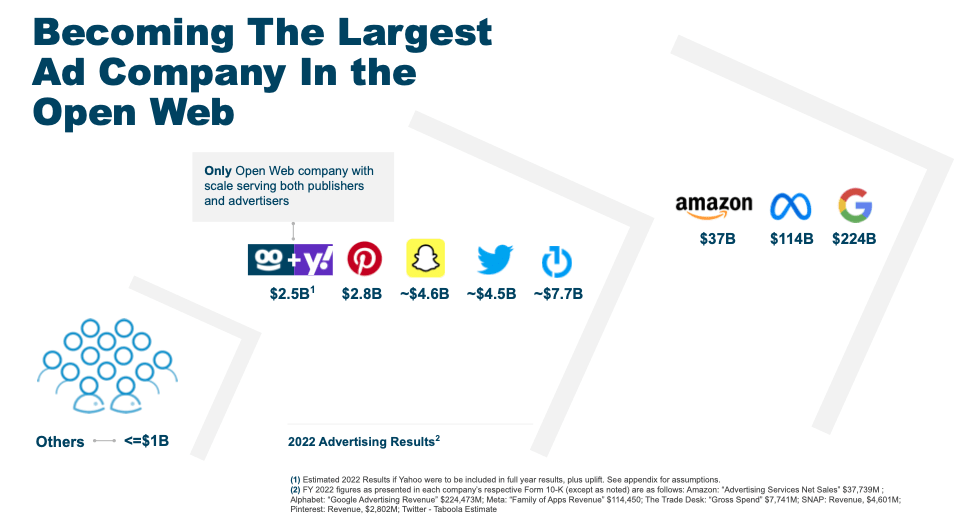

As you can see, the largest property - CNN - still gets less than 500 million monthly visits (less than 5% of Facebook's monthly traffic alone). But as far as the monetization of traffic outside of the walled gardens, Taboola and Outbrain might have everyone else beat. Taboola included the following slide in its presentation about the Yahoo partnership, and it's actually pretty eye-opening if you think about it.

{kind=link}

Obviously, the other walled gardens of tech are still larger than Taboola. And there are companies out there - like The Trade Desk, Magnite, and Pubmatic - that are pretty large (and getting larger) by serving either the advertisers or the publishers, but not both. Taboola (with Outbrain following closely behind) claims that it's the largest "open web" company serving both publishers and advertisers.

Basically, if someone wants to advertise outside of a social media platform and wants to avoid being one of a million advertisers on Google adwords, Taboola and Outbrain are increasingly the places to go.

What Kind of Businesses Are These?

Taboola and Outbrain have - for all intents and purposes - a duopoly on a type of advertising that they created. There are no real challengers in their neck of the woods, but there's a different problem. There aren't really any more new partners to convert.

For the most part, Taboola and Outbrain own the premium news publisher market - the ideal channel for recommendation ads. And there aren't really any more premium publishers being created. You've had a few, mind you, like Business Insider (which is relatively new), Coindesk, etc.

But the pair is running out of room to grow, as far as partnering goes. Taboola really scored a homerun with the Yahoo deal, which it said would have generated $2.5 billion in revenue total in 2022 if it was completely online at that point. For comparison, Taboola generated $1.4 billion in total revenue in FY 2022.

Overall, though, their core business isn't necessarily poised for growth unless (1) they can attract bigger and better brands, or two (2) a large portion of the ad spend on the walled gardens shifts to more of the Taboola/Outbrain partner websites. Personally, I find the second option a little unlikely considering the walled gardens capture such a large number of eyeballs. As much as Taboola and Outbrain tout the Open Web, I just don't think they have a large chunk of it.

Don't get me wrong, though, the core recommendation business has been good to them, and it has driven growth over the last three years.

{kind=link}

{kind=link}

As you can see, the two businesses have seen (for the most part) increasing demand from both publishers and advertisers.

The core recommendation business is a sticky one and a good base to grow from. Both companies have reported net retention rates of over 100% in the past - though Outbrain has been seeing 75%-80% during Q3 because of ad spend cuts as well as the closure of several customers. Most of their contracts with publishers only last a couple of years, but they seem to be renewed pretty regularly unless the publisher chooses to go with the other option - Taboola or Outbrain, depending on which one they were with before.

And, I think the reason they've had such high retention rates in the past is that they're more service-type companies than you think. Unlike Google, which does offer an ad platform for publishers, Taboola and Outbrain are actually partners with the companies. They're addressing concerns the companies have, sharing revenue with them, and actively trying to improve monetization and customer-use on the sites.

After all, I think half of the recommendations at the bottom of the publisher articles are typically recommendations for other articles on their own website. Say what you want, but Taboola and Outbrain may have driven reading time more than any other company the publishers have partnered with.

On top of that, both companies can definitely claim that they have access to a veritable treasure trove of first-party data. With the death of third-party cookies, a lot of advertisers are looking for easy ways to utilize first-party data.

{kind=link}

This may lead to a temporary increase in interest in both Taboola and Outbrain (though it's really not coming through in 2023's muted ad market), but TTD is rapidly taking advantage of this as well. Further cementing its place as the king of the open web (a position that Taboola and Outbrain aspire to), TTD has essentially created its own third-party cookie, which may end up poking a hole in Taboola and Outbrain's hopes for an improved value offer.

Which One's the Better Choice Going Forward?

Both companies have seen some recent slowing in their traditional performance marketing business. But, more importantly, both have, over the last couple of years, become unprofitable and started burning cash to fund the new initiatives they're pursuing. So, what are these new initiatives, and which company is the better investment for the future?

Taboola

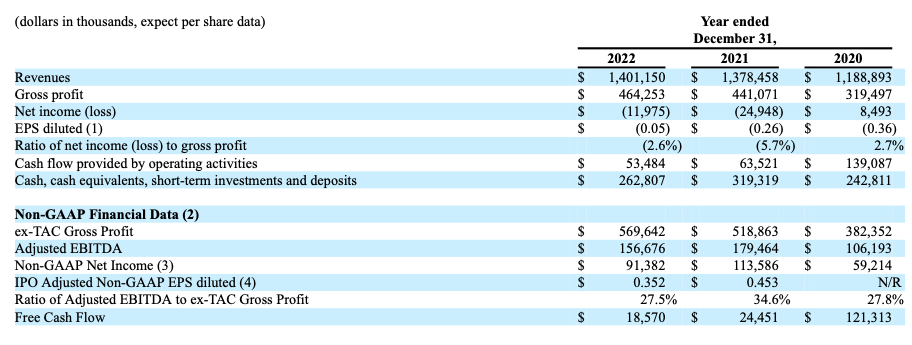

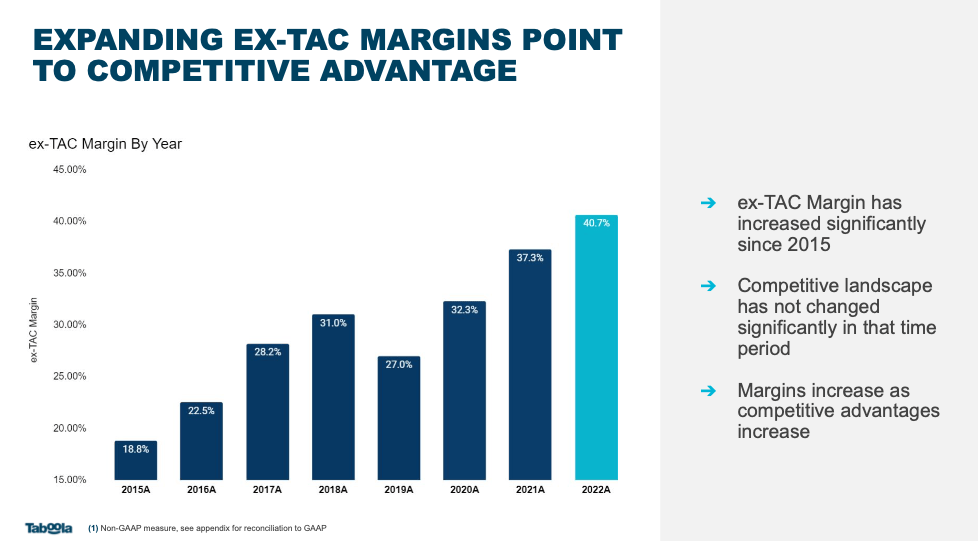

Back in 2020, Taboola generated roughly $120 million in FCF. Since that time, its revenue has grown by ~18%, but its operating cash flow dropped $53 million and FCF to less than $20 million. Taboola's gross margin (both regular and ex-TAC), by contrast, has been growing pretty much every year.

{kind=link}

In 2022, its Gross Margin was ~33% compared to 26.8% in 2020. Revenue has grown over the same period, so what's the deal with FCF and earnings? Earnings turned negative in 2021 and 2022, primarily as the result of rapidly increasing opex, which is currently at 34% of revenue in 2022 compared to 24% of revenue back in 2020.

The core business itself hasn't really changed much. The bigger issue has been ever-inflating operating costs since the company has gone public. But according to management, this is still a non-issue. Taboola's been adding new segments to its business over the last several years but has yet to receive a commensurate level of revenue.

Management believes, however, that these investments and new cost structures are the future of the company. Regardless of the near-term payoff, this is how they expect to sustainably grow going forward. And, so far, the new segments have done well.

First, ecommerce has grown to 20% of ex-TAC gross profit as of Q2 2023 (up from 15% in Q1 2023). After the Connexivity acquisition (which at $800 million is a little less than the size Taboola's entire market cap now), Taboola has been looking to break into what it believes is one of the largest growth markets for publishers going forward.

Taboola is betting that commerce is going to be a major monetization channel for publishers in the future. It believes that a third of the total open web publisher revenue will be generated from ecommerce-related spending, and it wants to capture a large chunk of that.

Taboola Q2 2023 Investor Presentation

Publications are moving towards commerce-based content/monetization, and Taboola hopes to cash in on that through its ecommerce product connectivity platform and through its new service Taboola Turnkey Commerce.

Turnkey essentially allows publishers to outsource their commerce-based strategy to Taboola. They don't want to create affiliate product-based content themselves? Outsource it to Taboola. They don't have the resources to buy a Wirecutter-type publication like the New York Times did? Outsource it to Taboola. TIME Inc., for instance, is one of the first adopters of the Turnkey platform, and they have already seen affiliate articles rank at the top of the SERPs in Google.

Outside of the commerce trend, Taboola is also hoping to leverage its existing publisher relationships to get into the header bidding market. Management estimates that the 8,000 publishers they have on their platform generate roughly $25 billion a year in display advertising revenues. They hope to, with their new header bidding offering, capture just 5% of that total, eventually garnering an additional $1.25 billion in display ad revenue. And, even though Google has a stranglehold on that business, and there are numerous other competitors, it does appear that Taboola is making progress. They've already converted Microsoft's MSN to their header bidding offering - no easy feat, considering (before the Yahoo partnership) Microsoft was their largest customer at 3% of total revenues. Microsoft's commitment may go a long way towards convincing other publishers to give it a try.

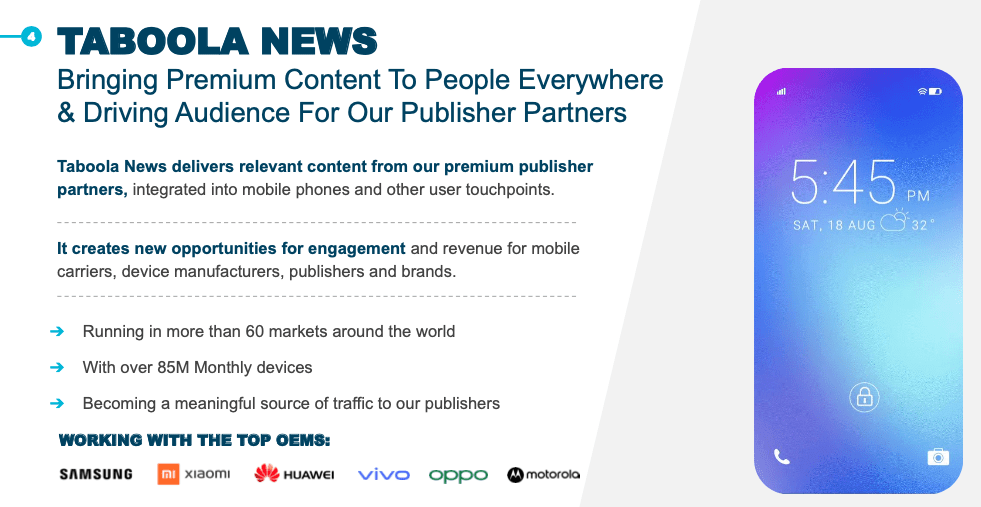

Finally, Taboola is making a foray into the Android-native news recommendation market by offering its own Taboola News app. Much like the Apple News app on the iPhone, the Taboola News app allows users to access their favorite news articles all in one app. And Taboola uses its recommendation algorithm to recommend articles - kind of a pure-play testing ground for the effectiveness of its recommendation engine. Taboola News was still small in 2022, generating $50 million in revenue for the year. But Taboola's already predicting that revenues will double in 2023, coming in at an expected $100 million for the year.

{kind=link}

Outside of all of those future initiatives, the Yahoo deal is also going to be a near-term boon to the company. As of Q2 2023, management said that it still wouldn't be seeing profit from the combination. This seems to have worried the market, playing into fears about decreasing profitability, a weak advertising market, and a never-ending promise to generate increased revenue and profitability from Yahoo.

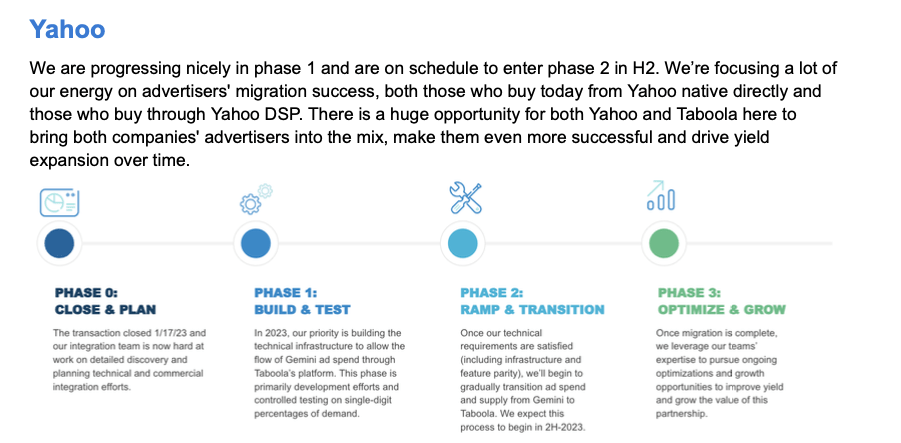

And, honestly, I don't know what exactly to think. The company claims they're beginning phase 3 of a 4-phase plan to integrate with Yahoo.

{kind=link}

But I haven't heard anything about a $2.5 billion revenue run-rate since Q1 2023. The company stated in its Q2 2023 letter that the revenue from Yahoo will be minimal to nothing in 2023, and it isn't giving clear guidance on 2024 - definitely nothing hinting at $2.5 billion in revenue (though it should be noted that management hasn't said this isn't the case anymore).

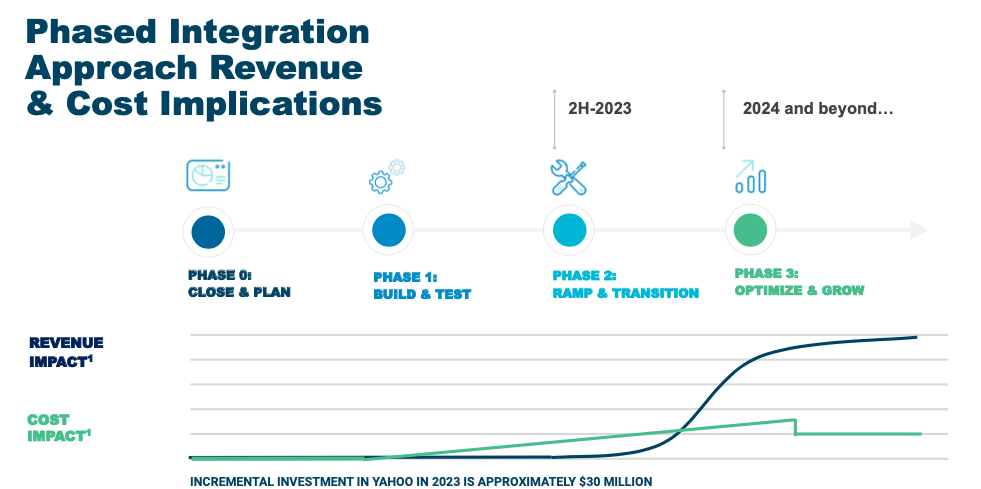

In its March 2023 Yahoo investor, however, Taboola predicted that Yahoo's operations would start to have an impact on revenue at the beginning of the final phase. Until that point, Taboola will be incurring cost associated with starting-up and running Yahoo's ad tech system - which the company estimates will run to about $30 million total in 2023.

{kind=link}

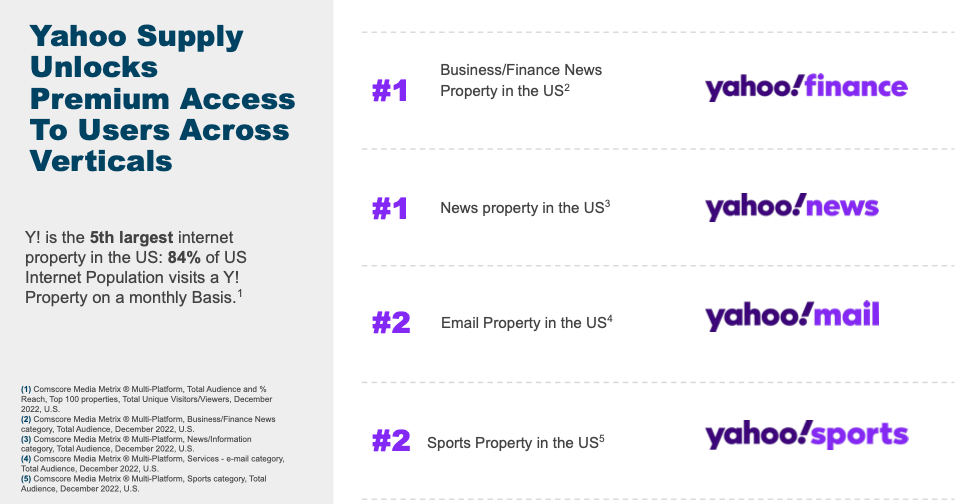

We know that the integration seems to be taking a while, but its undeniable that Taboola is getting access to top-tier websites, even compared to what it usually monetizes. Yahoo is number 1 in some of the most valuable categories (Finance and News especially, which are big for the kinds of performance marketers that Taboola caters to).

{kind=link}

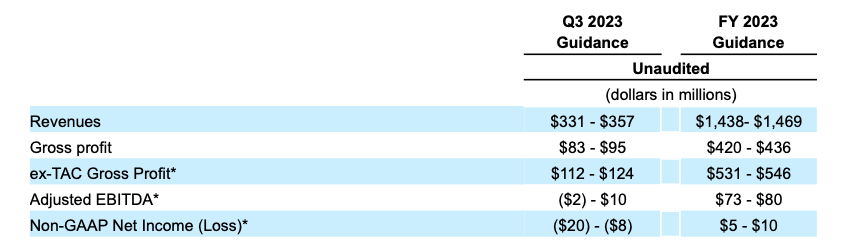

Like I said though, as of right now, the company isn't promising anything out of the ordinary. As a midpoint, they're guiding to around $1.45 billion in revenue for FY 2023, around $75 million in adjusted EBITDA, and $8 million in Net Income.

{kind=link}

A jump to $100 million from what could be less than $20 million this year probably means a lot will be riding on the Yahoo integration starting to generate some revenue. Even then, when you think about it, $100 million is kind of disappointing, considering Taboola was bringing in around $120 million just a few years ago.

Outbrain

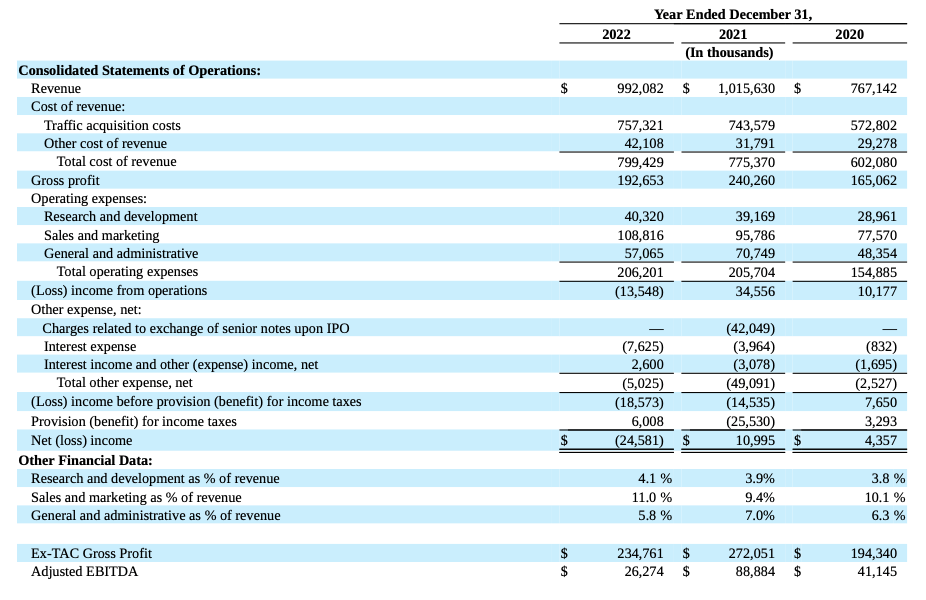

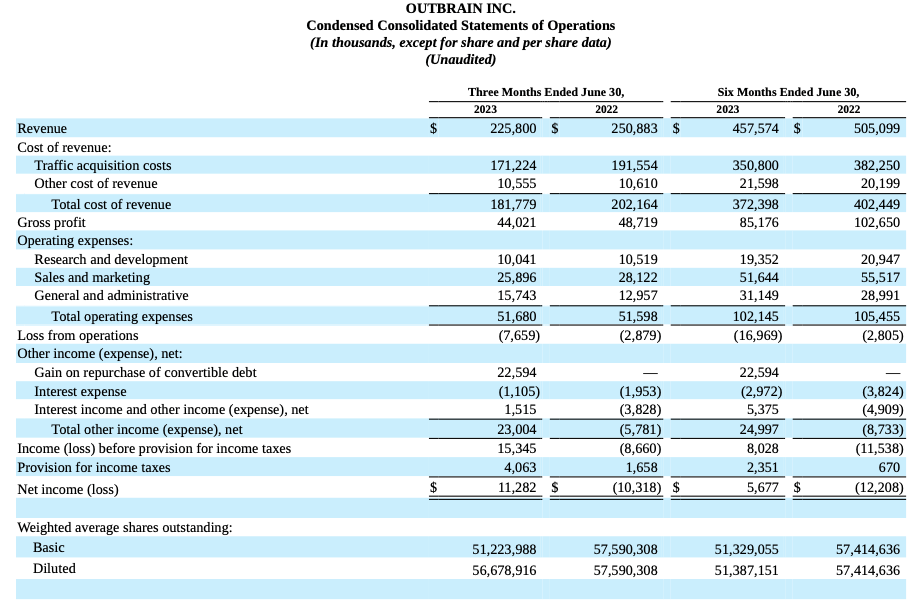

Outbrain, like Taboola, has seen its earnings drift into the red, even as it's grown its revenue from the time of its IPO (and earlier). In 2022, its net income dropped to -$24.6 million compared to just under $11 million in 2021. Its Operating Cash Flow has similarly dropped to around $4 million in 2022 from over $50 million in 2021 and 2020.

So far in 2023, the company has seen a 10% YOY drop in revenue in Q2 2023 and has seen its net revenue retention rate drop to an all-time low of 78%. Like Taboola, they laid off a decent chunk of their workforce - cutting 10% of total jobs in May of 2023.

Outbrain has over 30,000 advertisers using their platform - which is more than Taboola, indicating that most of these advertisers are probably spending less than those using Taboola. The top 20 advertisers accounted for 20% of revenue in 2022, with the largest accounting for 2%. The top 20 publishing partners accounted for roughly half of 2022 revenue, with the largest making up 10%. Outbrain has also noted how much of its revenue comes from mobile activity. It reports that 72% of its revenue is generated from ads placed on clients' mobile websites and apps. My assumption is that - given the similarity in clients - Taboola could claim a similar statistic, but I don't know for sure.

And, much like Taboola, Outbrain is shifting its resources and focus to growth in areas outside of their traditional recommendation-based digital advertising. While Taboola has chosen to focus on ecommerce, header bidding, and mobile-based applications (like Taboola News), Outbrain has started to bet its future on pre-roll video ads and their own internal DSP.

Outbrain acquired a DSP - Zemanta - back in 2017 to bolster its own internal DSP offering. I honestly don't know how much this has helped so far, but I think they were ahead of the game, getting into the DSP market back in 2017. And I think they see the writing on the wall with TTD. They could be bypassed if they don't offer their advertisers a way to programmatically bid on ad inventory across the open web.

Their most notable expansion outside of recommendation has been pre-roll and premium video ads. Pre-roll has grown from 2% of revenue in 2018 to 10% in 2022. Outbrain acquired Video Intelligence (vi) in 2022 for roughly $55 million - a premium ad video company. And it launched its Onyx platform in June of 2023 - a premium video ad product - and have already signed up 25 partners. They expect Onyx to generate $10 to $20 million in revenue in the second half of 2023 alone.

Onyx appears to be Outbrain's focus for future growth, much like ecommerce and Turnkey is for Taboola. They expect Onyx to double their addressable market, and, as a result, they expect pre-roll video ads to be a much larger part of their business going forward.

This is all part of Outbrain's focus to capture customer attention. They believe that CPM, click-through-rates, and other metrics traditionally used by advertisers and publishers are the wrong way to go about measuring customer connection and acquisition in the future. They think that attention is the single-most important metric, and will be going forward. So, Outbrain has been shifting its focus to premium ads that (1) can capture more customer attention and (2) can generate higher rates from advertisers. And they think they've found it in video ads.

Taboola or Outbrain?

Upfront, I will say that I think Taboola has the edge here as the better investment because of the Yahoo partnership. But we'll put that aside in a minute to discuss the strategies for the future that both companies have.

Outside of the Yahoo deal, you essentially have to decide if the bet on commerce as a monetization tool or video is the better bet going forward. Both are expanding into header bidding (and Taboola may have an edge with MSN as a partner), but both also have relatively static positions in the recommendation market. They might swap some customers every once in a while, but for the most part, they're keeping their market share.

Both companies are cheap based on past metrics, though both are burning cash as of FY 2022, and things aren't necessarily looking that much better in 2023. There's hope going forward (if you believe it) for both companies though.

If Taboola is to be believed, they will be generating $200 million in adjusted EBITDA and $100 million in FCF by 2024. Given a current market cap of ~$1 billion, this implies that the company is trading at ~10x 2024's expected FCF (in an optimistic scenario). This looks cheap, and the company has touted the potential of its future growth initiatives, but with near-term profitability suffering and most of its recent investments still in the early stage (though growing quickly), 10x 2024 FCF seems like an adequate valuation.

Overall, if you believe the company will be generating $100 million in FCF by 2024, you probably also believe that it will be taking advantage of its new investments as well. If Taboola is growing at something like a double-digit rate, this is a pretty cheap valuation. But I have my doubts.

I think that ecommerce is probably the better play than premium video advertising. As noted above, affiliate revenue has become a major profit center for large and small publishers alike. And, with the number of Shopify sellers and others outside of the Amazon ecosystem now, ecommerce is always looking for new ways to grow. But I do worry about advertiser demand.

CNBC

It seems that at decent number of them have started to throw in the towel and move to Amazon after Facebook ads started suffering from the lack of third-party cookies. This doesn't necessarily bode well for Taboola's ecommerce offering (though it is growing). Ad dollars going to Amazon are ecommerce ad dollars that aren't being spent on the open web.

Outbrain, on the other hand, has seen slowing revenue growth in 2023, but all of the increase in earnings have come from a gain on a repurchase of its convertible debt.

{kind=link}

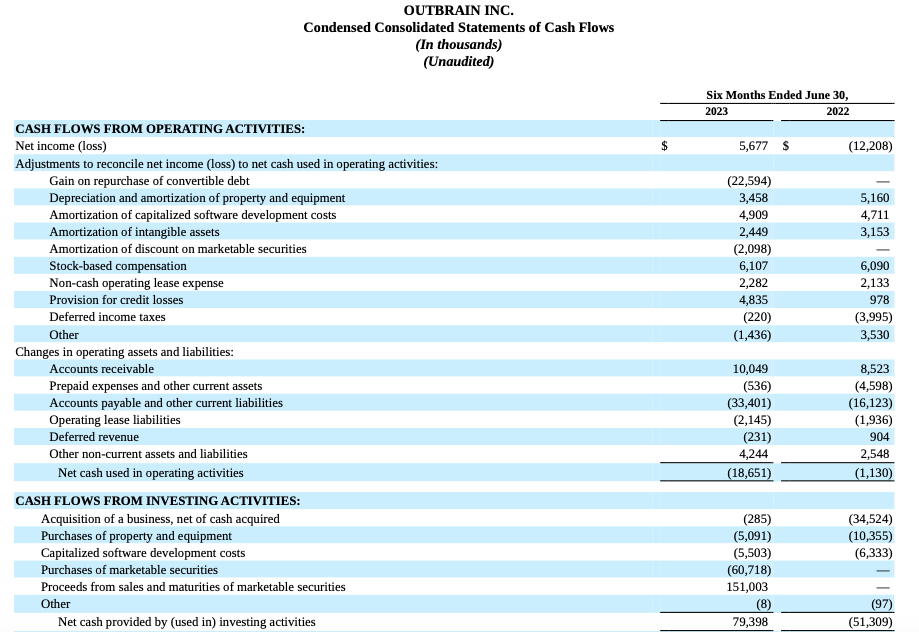

On a cash flow basis, the company (like Taboola) is burning more cash in 2023 than before, investing in its new initiatives without seeing a near-term payoff.

{kind=link}

Today, Outbrain sports a market cap just under $300 million - a good bit smaller than Taboola's ~$1 billion. But if we assume that, for argument's sake, the company can regain its margin profile of 2021 and 2020, and continue generating around $40 million in FCF, it'd currently be trading at about 7x that amount.

On a relative value basis, this makes Outbrain the more undervalued play here, but you have to take the future results into account. If you believe that Outbrain will be able to generate growth and regain its past margins (roughly 5-6% OCF margins), you'd probably want to go with Outbrain. Both companies have a steady recommendation business that probably isn't going anywhere. But what will drive valuations is how they execute with their new initiatives in the future.

I think video is a reasonable and maybe even safe route for Outbrain to go down. They have the publisher relationships, they have the advertisers, and recent studies show that video ads typically outperform static ads by a pretty wide margin. They drive higher CPAs and higher engagement, which will basically mean more revenue for Outbrain. If Outbrain can start gaining a decent share of the video ad inventory offered by its publishing partners, I think it'll have a pretty good growth business on its hands.

But, all of this is relatively speculative compared to Outbrain's position today. The company is losing money and seeing declining growth. Taboola, by contrast, has already struck a deal with Yahoo that will probably add another billion in revenue in the short-term. This is excluding any investments it has made in its commerce initiatives. I understand that the company has seen slowing growth from its traditional business as well as decreased profitability. Taboola's share price has increased by around 2.5x since the announcement of the deal, so obviously the market thinks it is worth something.

Even with Taboola trading at what appears to be a higher price compared to its predicted 2024 FCF, though, I still think it's the better bet. It's got the potential for multiple expansion once the market sees that the Yahoo deal is working out (though I don't know how much this will help, considering it may be priced in already), and on top of that it's got the growth in commerce, Turnkey, and Taboola News.

Conclusion

Overall, I think the recent softening in the advertising market throughout 2023 indicates that there could be more pain for these two companies ahead. Add onto that the current investments both are making to build out their new product lines, and I think results could be challenging in the near-term.

It's too early to tell how well the new initiatives for each company could do, but they've seen promising growth starting out. While both companies are burning cash, they're relatively cheap compared to normalized FCF and expected future FCF. Taboola is probably the better choice out of the two - though neither is very promising right now - considering its already strong growth in its commerce offering and Taboola News offering, as well as its already-inked Yahoo deal which will undoubtedly improve results.

Both companies operate in a duopoly type environment that they're unlikely to lose their position in. Ad tech, however, could potentially change faster than they can keep up with (i.e., publishers could end up going to TTD directly, especially with its new OpenPath offering. Taboola and Outbrain are resisting this by offering more overall monetization management to publishers and taking a large piece of each publisher's total monetization tool kit.

For further details see:

Taboola And Outbrain: The Future Of The Open Web?