TBLA - Taboola: Appears Undervalued And Well-Positioned For Swift Recovery

2023-06-20 13:55:00 ET

Summary

- Taboola is an ad tech platform that has experienced underwhelming share performance and lackluster revenue growth due to macroeconomic slowdowns affecting ad spend.

- Despite these temporary challenges, TBLA's strong fundamentals and market leadership position it well for growth acceleration, possibly in FY 2024.

- My target price model suggests that the stock appears undervalued by 28% - 33%, making it an attractive buy at its current price of ~$3 per share.

Taboola (TBLA) is an advertising technology/ad tech platform that helps content publishers increase page views and generate revenue through referral traffic by embedding the "Around The Web" and "Recommended For You" thumbnail grid ads on their home pages.

Following a failed merger with its rival, Outbrain, the company went public through a SPAC in 2021. Share performance has been underwhelming since then. Share prices were between $8 - $10 shortly after going public, but since the beginning of last year, they have gradually declined and are currently trading between $2 - $4 per share.

Revenue growth has been lackluster over the same period as TBLA was hit by the impact of a macro slowdown that has depressed ad spend. Revenue grew by only ~1.67% in FY 2022, and in response to the macro slowdown, TBLA also made a ~6% cut to its global headcount.

On the flip side, I continue to rate TBLA highly due to its strong fundamentals and market leadership, which should allow it to reaccelerate growth quickly once the slowdown subsides. Near-term catalysts for FY 2023 remain minimal, though my analysis suggests that FY 2024 could be an inflection point.

In this coverage, I am giving TBLA a buy rating. My modeled target price indicates that the stock is 28% - 33% undervalued from my FY 2023 target price of ~$4.

Catalyst

Given the macro downturn creating industry-wide ad budget headwinds, I think that aside from the $40 million share buyback program , near-term catalysts for FY 2023 remain minimal. The question here then becomes whether TBLA can stay resilient today and recover quickly once the temporary headwind subsides.

As I take a deep dive into TBLA’s growth, liquidity, and also cash-flow generation, I conclude that TBLA, having been in the business for over 15 years, is a market leader with solid fundamentals that demonstrate strength across those areas, suggesting that it is well-positioned for both resilience and quick recovery, most likely in FY 2024.

{kind=link}

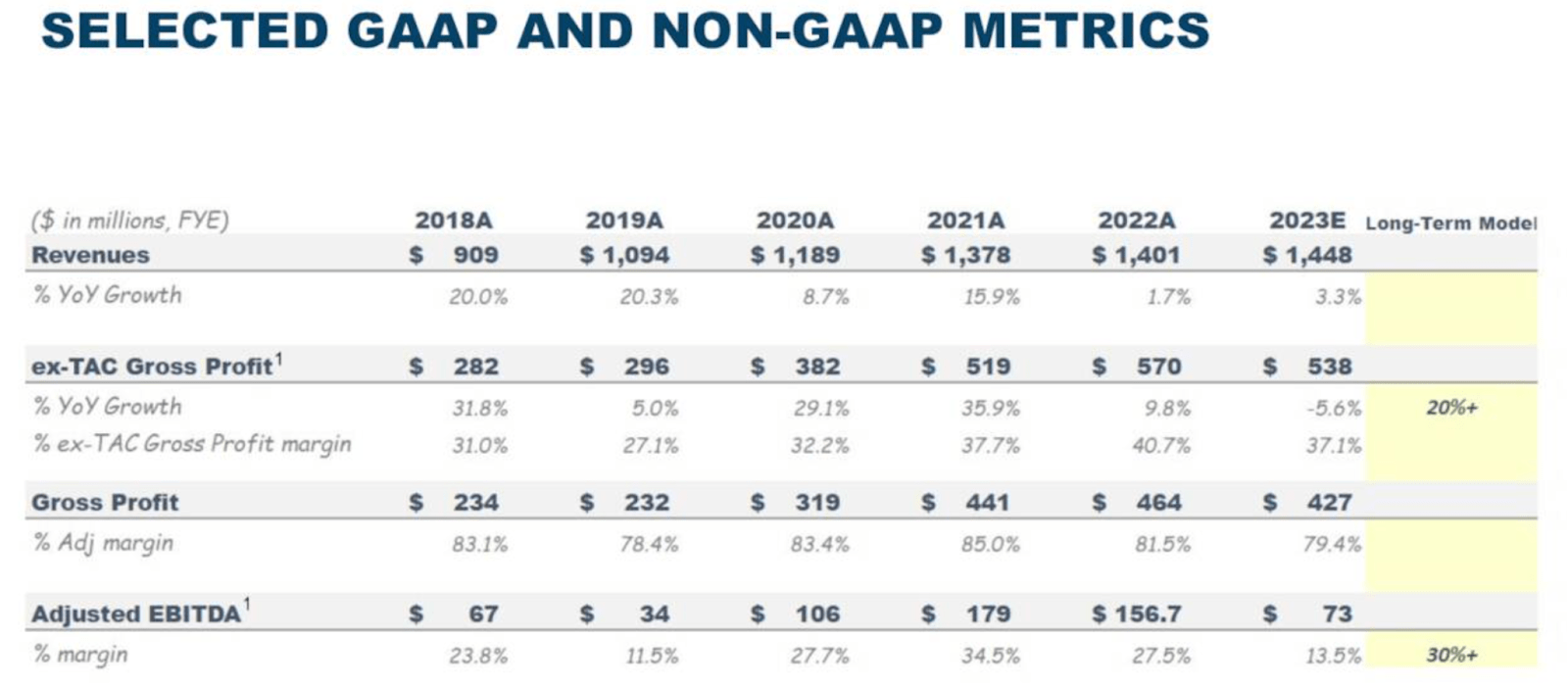

Revenue growth has historically been solid. Except for 2020 and 2022, where the industry slowed down due to COVID-19 and fear of recession, TBLA has actually seen double-digit YoY growth every year for the past 5 years, suggesting strong demand for native ads under a normal situation. TBLA also consistently maintains a double-digit adjusted EBITDA margin.

{kind=link}

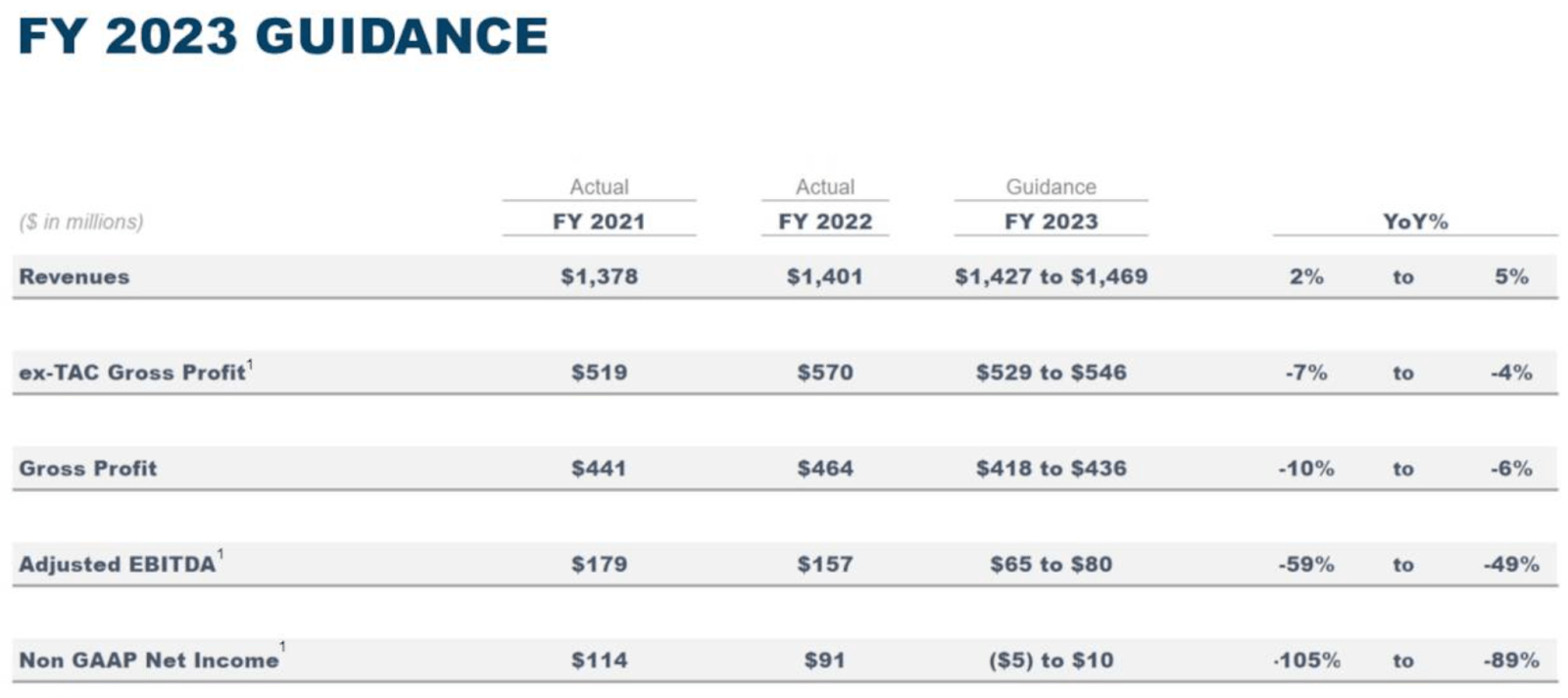

It appears that the growth outlook will remain challenging in FY 2023. Nonetheless, the 3.5% growth expectation at the guidance midpoint seems realistically achievable and decent under the current environment. It also already suggests a slight acceleration from last year’s 1.67%. TBLA also guided to a single-digit ~5% adjusted EBITDA margin, though the CEO suggested that it will be a one-off occurrence and that TBLA should again see a double-digit figure the following year in FY 2024 :

Now, while we are not fully guiding for 2024, we expect a step change in our financial performance, with over $200 million in adjusted EBITDA and over $100 million in free cash flow. I have said in the past that it is rare for a company to have this level of clarity and confidence a full year in advance.

I think that the comment there was interesting. In particular, it seems to imply that the management is baking in the assumption of ad budget headwind subsiding in FY 2024 while key catalysts - such as value creation from the Yahoo partnership - start taking effect.

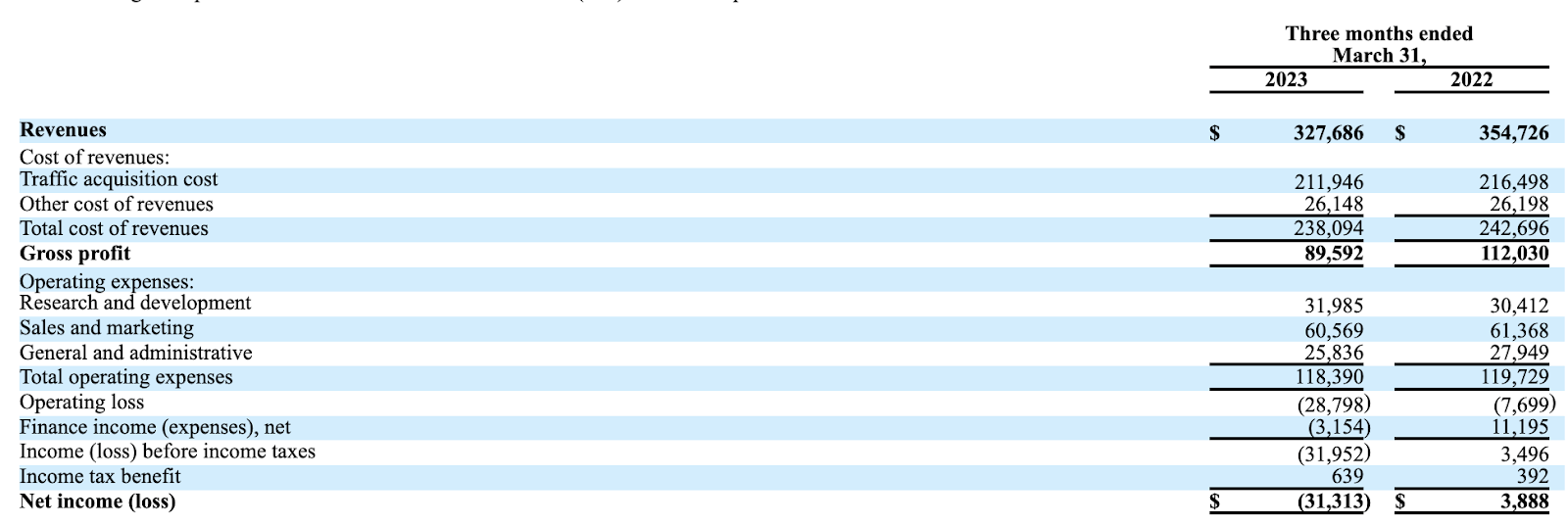

TBLA's earnings report TBLA's earnings report

{kind=link}

{kind=link}

Considering that operating expenses, non-operating expenses, and traffic acquisition cost / TAC remain relatively flat, the only thing driving adjusted EBITDA would be top-line growth. Given the management’s comment that FY 2024’s adjusted EBITDA will probably exceed +$200 million, it seems to suggest the presence of a strong growth catalyst. On that note, I feel that we probably should expect TBLA to start unlocking the full value from Yahoo's exclusive partnership in FY 2024 .

I view Yahoo’s exclusive partnership as a major catalyst for TBLA. TAC remains the biggest expense for native ad platforms like TBLA. But the Yahoo partnership will enable TBLA to get exclusive access to Yahoo’s native ad inventories across its key services used by 900 million active monthly users. Based on the commercial agreement, all of this is achieved in exchange for 25% of Yahoo’s ownership in TBLA, and as such, TAC should remain unaffected by this partnership.

G iven the ongoing integration and the macro downturn today, it is highly unlikely that we will see the impact in FY 2023. The integration work with TBLA’s platform remains critical to ensure effective placement pricing for Yahoo’s native ad inventories. Once it fully completes, though, I expect TBLA to instantly see a material revenue uplift while maintaining TAC at the same level, effectively expanding ex-TAC gross profit and adjusted EBITDA margin.

{kind=link}

{kind=link}

Meanwhile, TBLA also has a strong balance sheet to stay resilient in FY 2023. Cash and cash equivalents / CCE have been steady between $275 million - $320 million in recent times. As of Q1, TBLA had +$275 million of CCE. Prior to FY 2021 when TBLA entered into a ~$300 million loan agreement to help finance the Connexity acquisition, the company also had no debts. Even then, the debt-to-equity ratio post-acquisition has been at a very healthy level and steady between 0.2x - 0.3x.

{kind=link}

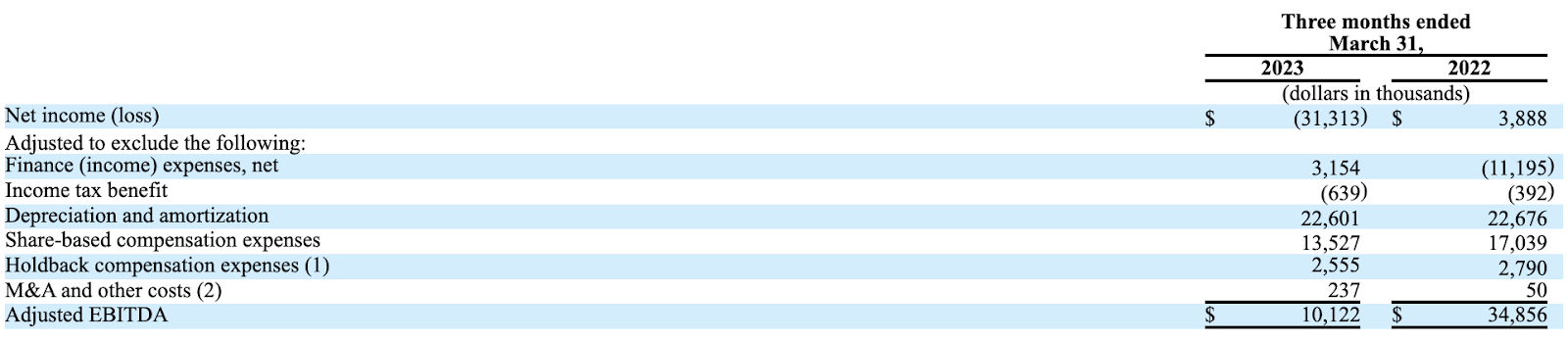

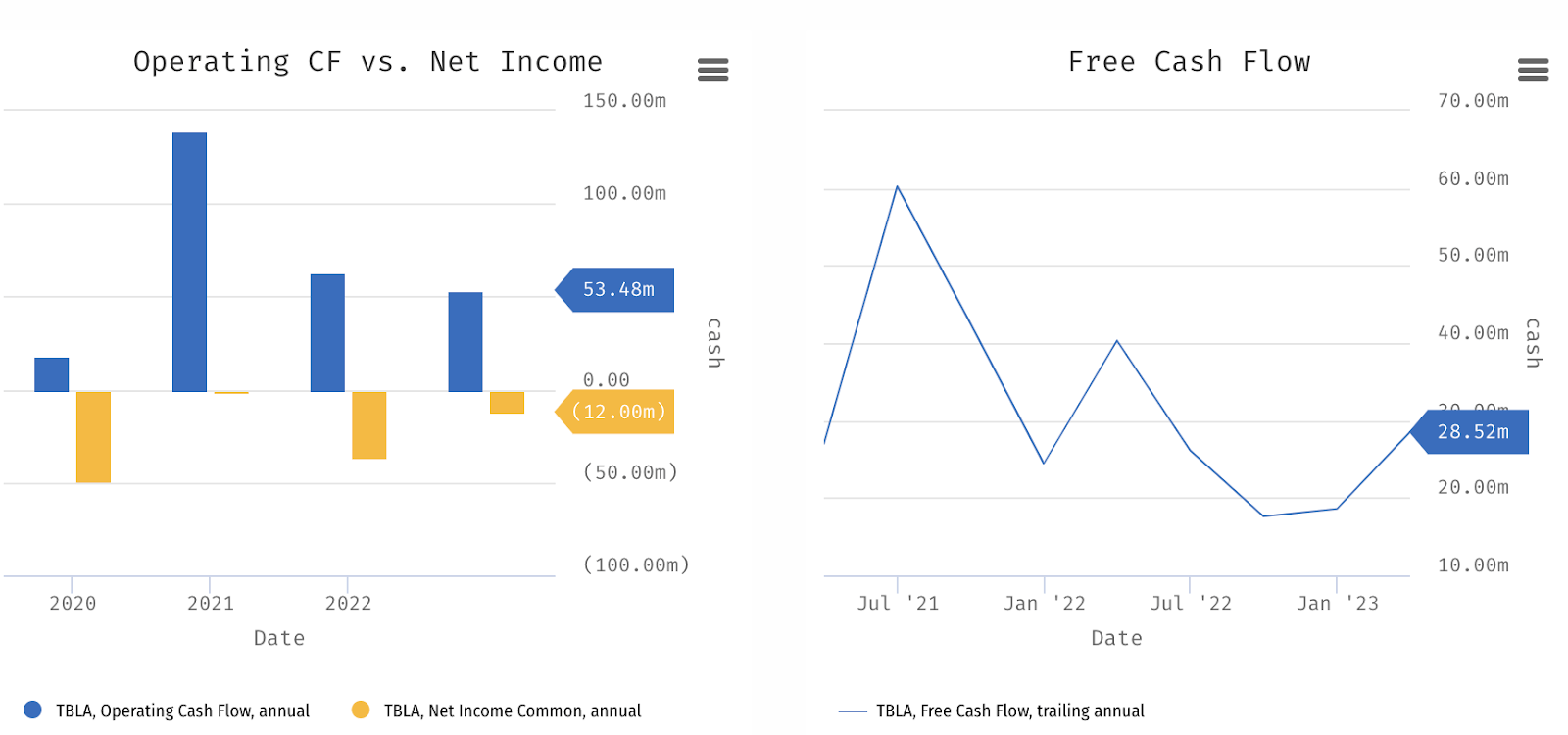

Cash flow generation has also been relatively steady. Operating cash flow / OCF has been trending up since 2020. Though OCF declined to +$53 million in FY 2022 from +$65 in FY 2021, I think that the magnitude was minimal and it is likely that TBLA will maintain that level for FY 2023. In Q1 2023, TBLA already reported ~$17 million of quarterly OCF, which on an annualized basis, will be ~$68 million. Given the still conservative outlook for FY 2023 though, end-year OCF will probably be closer to FY 2022’s figure.

Risk

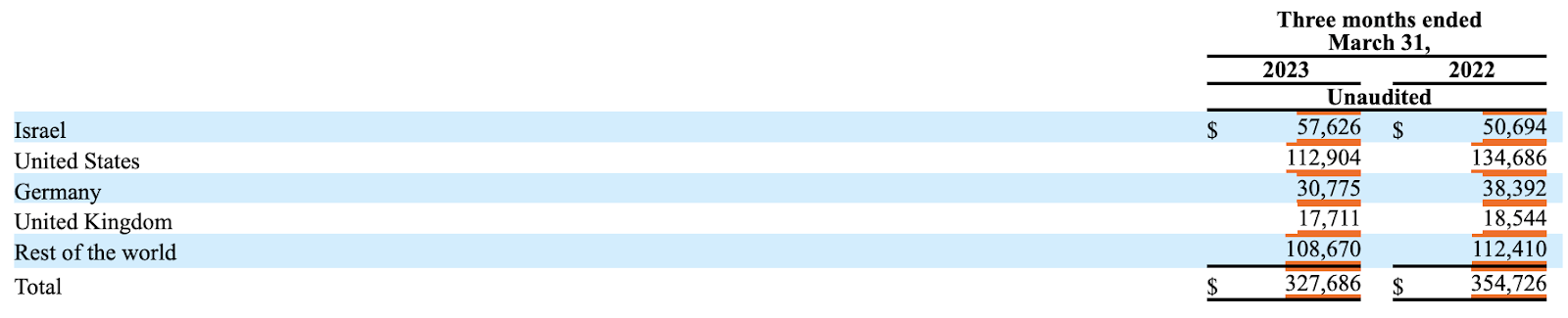

In Q1, TBLA continued to see broad-based decline across its geographies. However, I think that the biggest risk for TBLA today is prolonged macro slow down across its key markets in the US and Europe, where TBLA generated ~34% and ~30% of its revenue respectively.

{kind=link}

As of today, the macro situation has probably not improved since last year, increasing the risk of a potentially prolonged ad budget slowdown into FY 2024 that may delay TBLA in unlocking value from the potential catalysts. Though the rate hike was recently paused in the US, there was a signal that the rate hike is still not over yet. On the other hand, Europe has been in a sort of mild recession for some time now , with the ECB continuing to raise interest rates. Consequently, this recent development may continue to create recession fear among marketers, further maintaining the currently depressed outlook on ad spending.

Valuation / Pricing

Given the management’s suggestion of a potential rebound in FY 2024, I have baked that into my analysis and attempted a target price for FY 2024. My target price for TBLA is driven by the following assumptions for the bull vs bear scenarios:

- Bull scenario (60% probability) assumptions - TBLA to achieve 3.5% growth at the midpoint of its FY 2023 guidance and $1.45 billion of revenue. I expect TBLA to see growth reacceleration to 15% in FY 2024, assuming that slowdown will soften. I assign TBLA a P/S of ~1.5x, considering that the double-digit growth with a better ex-TAC gross profit due to catalysts like Yahoo’s partnership should expand TBLA’s valuation beyond 1x, and probably closer to its FY 2021’s valuation, when it recorded double-digit growth but without the similar catalysts.

- Bear scenario (40% probability) assumptions - TBLA to see $1.41 billion of revenue (1% YoY growth) in FY 2023 as it misses its guidance. This reflects an even further growth decline from last year. I also expect macro slowdown to prolong into most of FY 2024 to result in TBLA’s achieving a merely 3% growth.

author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of +$5 per share. I then discounted that price back to today’s terms with a 15% discount rate to arrive at the PV / Present Value FY 2023 target price of ~$4 per share. Since TBLA is trading at ~$3 per share, my target price indicates that TBLA is undervalued by ~28% to 33%.

With that in mind, I believe that TBLA is an attractive buy today at the current price. I would also note that I apply rather a few conservative assumptions in my target price model. For instance, I did not project a reduction in the number of shares outstanding as a result of the share buyback program for FY 2023.

My bear projection also assumes probably a more extreme case of prolonged slowdown into FY 2023 and FY 2024, while I also assume a 40% chance of that happening. Finally, the discount rate of 15% probably leans towards the high side for companies with a relatively healthy balance sheet and track record of steady growth and cash flow generation like TBLA.

Conclusion

Despite the challenging macroeconomic conditions affecting the advertising industry, the prospects for TBLA in the near term appear limited, aside from the $40 million share buyback program. However, my analysis of TBLA's growth, liquidity, and cash-flow generation reveals strong fundamentals stemming from its market leadership and relatively longstanding expertise and network in online native ad industry. This suggests that the company is well-prepared for resilience and a potential swift recovery, likely to be realized in FY 2024.

The current macro situation has not shown significant improvement since the previous year, raising the risk of a prolonged slowdown in ad budgets that could delay TBLA's growth rebound.

Considering the current price of ~$3 per share, I find TBLA to be an appealing buy. Even with conservative assumptions, it appears that the stock is undervalued by 28% - 33% from my target price of ~$4.

For further details see:

Taboola: Appears Undervalued And Well-Positioned For Swift Recovery