TBLA - Taboola.com: Marching Towards Profitability

2023-06-19 04:44:15 ET

Summary

- Today, we put Taboola.com Ltd. in the spotlight for the first time in more than a year.

- Despite a challenging ad market, the company is well on its way to profitability and continues to pay down debt and improve in key metrics.

- An investment analysis follows in the paragraphs below.

"The superior man understands what is right; the inferior man understands what will sell ."? Confucius

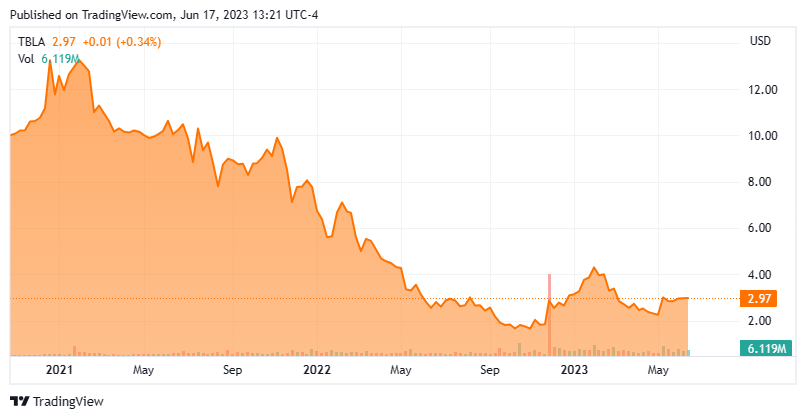

Today, we circle back on small cap concern Taboola.com Ltd. ( TBLA ) for the first time since our initial article on this small adtech concern in May of last year. We concluded that piece with the following take on Taboola stating the stock deserved a small 'watch item' holding pending further developments. The shares are down just over 10% since that conclusion.

Taboola posted first quarter results that beat the consensus and also raised its forward guidance in the first half of May. Therefore, it seems a good time to revisit this company that is marching towards profitability. An updated analysis follows below.

{kind=link}

Company Overview

May Company Presentation

New York City headquartered Taboola.com Ltd. operates an artificial intelligence-based algorithmic engine platform that partners with websites, devices, and mobile apps to recommend editorial content and advertisements on the " open web to users ." The stock currently trades right around three bucks a share and sports a market capitalization just north of $1 billion.

May Company Presentation

The company is partnered with many well-known media properties and publishers. Nearly 18,000 advertisers use Taboola to reach approximately 600 million daily active users.

May Company Presentation

First Quarter Results:

Taboola posted its first quarter numbers on May 10th. The company had a non-GAAP loss of nine cents a share, while the consensus had Taboola losing 16 cents a share in the quarter. Revenues beat by expectations by over $15 million even if they fell just over 17% on a year-over-year basis to $327.7 million.

May Company Presentation

Revenue was just one of many key metrics they managed to exceed the top end of previous management guidance in the quarter. Leadership provided the following up to date guidance for the rest of FY2023.

May Company Presentation

Analyst Commentary & Balance Sheet

Since first quarter results posted, four analyst firms including Oppenheimer and Credit Suisse have reiterated Buy ratings on TBLA. Price targets proffered ranged from $3.50 to $6.00 a share. Needham stated a week ago that both fuboTV ( FUBO ) and Taboola are ' said to be significantly ahead of their competition in integrating generative AI in a way that may impact results' .

Less than one percent of the outstanding shares in this stock is currently held short. The company's president sold $3.3 million worth of stock in February of this year. However, this represented only approximately 10% of his overall holdings. The company's Chief Technology Officer sold some $90,000 worth of shares in June while Taboola's CFO purchased nearly $200,000 worth of equity at the end of May.

The company paid down a bit over $60 million in debt in the fourth quarter 2022 and pared it by another $30 million in the first quarter of this year. Management has stated it plans to reduce debt by another $50 million over the final three quarters of 2023. The company ended 1Q2023 with just over $200 million in long-term debt and nearly $275 million in net cash taking debt into consideration. Leadership also has authorization to buy back up to $40 million worth of stock in FY2023. Taboola had $10 million in adjusted EBITDA in the first quarter and some $11 million in free cash flow.

Verdict

The current analyst firm consensus has Taboola breaking even in FY2023 as revenues rise in the low single digits to $1.44 billion. They see sales growth accelerating to the low 20s in FY2024 and believe the company will make between six and 46 cents a share with a median estimate of 32 cents a share.

Taboola has obviously been impacted by the slowdown in the digital ad market over the past few quarters. Analysts believe sales growth with accelerate substantially in FY2024. I would take those projections with a grain of salt simply because of my view that the economy will likely be in a recession by the end of this year.

May Company Presentation

That said, the company has done good improving its margins over the years and its balance sheet continues to improve. Leadership has guided that it expects Taboola to have adjusted EBITDA of at least $200 million in FY2024 along with at least $100 million in free cash flow. At a market cap of around $1 billion with over 25% of that being net cash, if Taboola achieves close to those metrics by 2024, the shares appear substantially undervalued. Only an uncertain economy and a punk ad market prevent me from putting TBLA in the 'Strong Buy' category. However, the equity continues to merit at least a small ' watch item ' position. There are options against TBLA so I have most of my holdings in this stock within covered call holdings.

"Advertising - A judicious mixture of flattery and threats. "? Stephen Leacock

For further details see:

Taboola.com: Marching Towards Profitability